|

市場調查報告書

商品編碼

1438104

5G基礎設施:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)5G Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

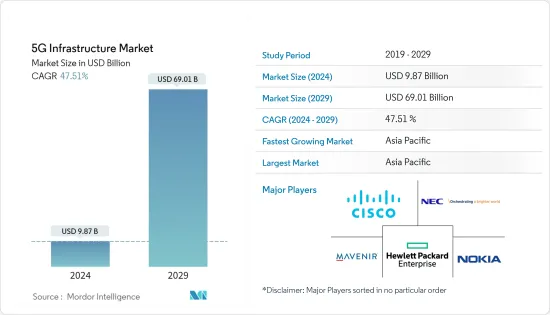

5G基礎設施市場規模預計到2024年為98.7億美元,預計2029年將達到690.1億美元,預測期內(2024-2029年)複合年成長率為47.51%

主要亮點

- 政府推動 5G 部署和物聯網、智慧城市等新技術進步的舉措推動了市場,這鼓勵市場參與者開發新服務/解決方案以佔領市場佔有率。Masu。

- 5G技術將顯著降低延遲率,即接收和傳輸訊息之間的延遲。端到端延遲的減少改善了用戶體驗,並為創新用例創造了新的機會。超可靠低延遲通訊 (URLLC) 也是一種趨勢,它是 5G 網路架構的區隔,可實現資料傳輸的高效調度,並支援工廠自動化、工業網際網路和智慧電網等各種應用。支援先進服務。自動駕駛汽車、機器人手術等因此,上述應用對較低延遲率的需求正在顯著推動全球5G基礎設施市場的成長。

- 根據 GSMA Intelligence 2023 年行動經濟報告,5G 將支援未來的行動創新和服務,並以持續採用和普及為基礎。預計今年 5G 的採用率將達到 17%,到 2030 年將達到 54%(相當於 53 億個連線)。到 2030 年,這項技術將為全球經濟增加約 1 兆美元,惠及所有產業。 5G 採用率的大幅成長將推動所研究的市場的發展。

- 此外,在智慧城市中,5G技術有潛力顯著增強公共。使用快速回應的 5G 網路,智慧城市系統可以從視訊保全攝影機、智慧交通燈和其他物聯網設備等多個來源收集和分析大量資料。例如,拉斯維加斯正在測試三個先導計畫,政府已撥款 5 億美元尋找 2025 年連接整個城市的方法。政府進行的智慧城市計劃數量不斷增加,將影響對5G基礎設施的需求。

- 部署 5G 網路需要大量基礎設施投資,包括安裝新基地台、小型基地台和光纖電纜。與上一代蜂巢式網路相比,5G 基礎設施部署需要更密集的網路架構,因為它依賴較小的小區尺寸和更大的網路容量。密度的增加增加了基礎設施需求和整體資本支出,導致網路營運商和服務供應商的初始成本更高。預計這將對市場成長構成課題。

- 疫情期間,電訊在多個國家擴展了 5G 連線服務。例如,2021年3月,總部位於菲律賓的Globe Telecom宣布將加速向中東和亞洲其他國家推出5G漫遊。 Globe 計劃向新加坡 Singtel、香港 CSL 和科威特 Oordu 的來訪客戶開放 5G 連線。後疫情時代,市場可望進一步成長。

5G基礎設施市場趨勢

5G無線接取網路預計將佔據主要市場佔有率

- RAN 提供跨無線裝置的無線接取網路資源。核心網路中的矽晶片和用戶設備支援 RAN 的功能。無線接取網路(RAN)包括基地台、天線、大型基地台和小型基地台。 5G可以透過兩種方式部署:透過5G核心網路或將5G RAN連接到4G網路。

- 向 5G 的過渡是一個關鍵因素,因為它可以實現更高的頻寬和更低的延遲。雲端 RAN 和開放介面實現的 RAN 分離使通訊業者能夠從更廣泛的生態系統中受益。

- 愛立信預計,2022年至2023年,全球5G用戶數量預計將增加,從超過5.5億增加到超過16.7億。此外,根據GSMA的數據,到2025年,海灣合作理事會國家的5G使用率將略高於全球平均(15%),這主要是由行動通訊業者在政府和行動技術合作夥伴的支持下推動推動的。(預計客戶5G採用率為 16%)。此外,中東和北非地區5G用戶數預計將達到1.2962億。 5G用戶數量的大幅成長將推動市場。

- 因此,主要大型通訊業者請求有關 RAN 分離和開放解決方案的資訊(RFI)。這是因為可以靈活地為 RAN 的不同部分選擇最佳解決方案。例如,虛擬基頻單元 (BBU) 的邊緣伺服器也可用於在邊緣雲端和 RAN 內運行應用程式,以減少延遲。 5G NR 和虛擬RAN架構的融合預計將為低延遲和物聯網服務帶來新的機會。

- 分析了亞太地區已開發經濟體和新興經濟體不斷擴大的夥伴關係,以提高市場成長率。例如,2022 年 12 月,三星電子宣布將提供多種 5G 無線電,以支援 NTT DOCOMO 開放無線電接取網路Open RAN 擴充計畫。除了 Docomo 目前的 3.4 GHz 無線電支援之外,三星還在 3.7 GHz、4.5 GHz 和 28 GHz 頻率範圍內添加新的無線電。該無線電支援 NTT Docomo 的開放無線電接取網路(O-RAN) 擴展,並涵蓋通訊業者持有的所有時分頻寬(TDD)頻譜。隨著三星擴大在日本的通訊,NTT Docomo 將能夠持有其頻譜建立多樣化的 5G 網路,並為日本各地的消費者和企業提供增強的服務。這些新型無線電與來自不同供應商的基頻的互通性測試也在 NTT DOCOMO 的商業網路環境中進行。

亞太地區預計將主導市場

- 亞太地區5G基礎設施投資不斷成長。中國是5G技術最大的投資者之一,甚至超過了美國。因此,它也是5G基礎設施廠商的重要市場之一。中國政府、通訊業者和供應商正在加強盡快部署5G,促使對所研究市場的投資增加。該國也是華為等一些最大的通訊5G 基礎設施供應商的所在地。但受中美貿易戰影響,近兩年部分電子設備領域出口大幅下滑。

- 根據GSMA預測,到2025年,40-50%的中國行動用戶將使用5G。該國在網路融合、網路虛擬和網路切片方面正在變得更加先進。各國政府也開始將獨立網路作為初始 5G 部署的一部分,理由是從頭開始建立 5G 網路,而不是將 4G 網路演進為 5G。這使得該地區所研究的市場得以成長。

- 建立5G是日本政府的首要任務。內務部(MIC) 是 5G 的主導機構。四家公司已向內務部提交了5G網路發展計畫。這四個規劃都是根據具體情況核准的,例如注重都市區地區的需求。保持足夠充足的光纖以提供5G服務。並將採取適當的網路安全措施,包括應對供應鏈風險的措施。

- 根據韓國科學資訊通訊部統計,截至2023年3月,韓國5G用戶約2,960萬人。如此龐大的5G用戶數量將推動所研究市場的需求,並使市場相關人員能夠開發新的解決方案來滿足廣泛的客戶需求並佔領市場佔有率。

- 亞太地區的其他國家包括越南、泰國和印尼。市場的發展、智慧城市的不斷湧現以及新技術的發展也預計將推動亞太地區其他地區對所研究市場的需求。

5G基礎建設產業概況

研究市場中競爭公司之間的敵意強度很高,預計在預測期內將保持不變。研究的市場由多個全球參與者組成,它們在競爭相當激烈的市場空間中爭奪注意力。主要供應商包括 Cisco Systems Inc.、Hewlett Packard Enterprise Development LP、MavenirSystems Inc.、NEC Corporation、Nokia Corporation、Oracle Corporation、Qualcomm Technologies Inc. 等。更多的公司是不同最終用戶和地區備受青睞的 5G 基礎設施提供者。由於多家公司將這個市場視為全球擴張的有利機會,預計公司集中度將在預測期內出現更高的成長。

- 2023 年 2 月 - 諾基亞將與IT基礎設施公司 Kyndryl 的私人 5G 合作夥伴關係再延長三年。兩家公司在聯合聲明中宣布了延期,稱他們將專注於為全球客戶開發和提供 LTE、5G 專用無線服務和工業 4.0 解決方案。

- 2023 年 2 月 - NEC Corporation 和 ADVA 將聯合向印尼最大的固定網路營運商 Telkom India 部署時間同步解決方案,以説明該營運商準備其傳輸網路,以在全國範圍內提供時間敏感的 5G 服務。 新業務的貨幣化,如提供超低延遲應用,對於行動營運商在5G時代建立動力至關重要。 為了滿足使用Telkom India服務的行動營運商和合作夥伴的預期需求,該公司正在提高其傳輸網路的定時精度。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 競爭公司之間的敵意強度

- 替代產品的威脅

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 由於各種設備的參與,增加了機器對機器/物聯網的連接

- 行動資料服務需求增加

- 市場限制因素

- 由於網路架構模型實施和頻譜課題,初始資本投資較高

- 推動 5G 發展的關鍵用例

- 車

- 工業的

- 家用電器

- 衛生保健

- 能源和公共

- 公共基礎設施

- 其他用例

第6章市場區隔

- 透過通訊基礎設施

- 5G無線接取網路

- 5G核心網

- 運輸網路

- 依地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 北美洲

第7章 競爭形勢

- 公司簡介

- Cisco Systems Inc.

- Hewlett Packard Enterprise Development LP

- Mavenir Systems Inc.

- NEC Corporation

- Nokia Corporation

- Oracle Corporation

- Qualcomm Technologies Inc.

- Telefonaktiebolaget LM Ericsson

- ZTE Corporation

- Samsung Electronics Co. Ltd

- Qucell Networks Co. Ltd

- Huawei Technologies Co. Ltd

- Airspan Networks Inc.

- CommScope Holding Company Inc.

第8章投資分析

第9章市場的未來

The 5G Infrastructure Market size is estimated at USD 9.87 billion in 2024, and is expected to reach USD 69.01 billion by 2029, growing at a CAGR of 47.51% during the forecast period (2024-2029).

Key Highlights

- The market is driven by government initiatives towards the deployment of 5G and advancement in new technologies like iot, smart cities, and many more, pushing the market players to develop new services/solutions to capture the market share.

- 5G technology offers a significantly lower latency rate, the delay between receiving and sending information. This decrease in end-to-end latency improves user experiences and creates new opportunities for innovative use cases. Also, there is a trend of Ultra-Reliable Low Latency Communications (URLLC), a subdivision of 5G network architecture that enables efficient scheduling of data transfers and caters to various advanced services across applications such as factory automation, the industrial internet, smart grid, autonomous driving, and or robotic surgeries. Hence, demand for lower latency rates among applications above is significantly boosting the growth of the global 5G infrastructure market.

- According to GSMA Intelligence Mobile Economy Report 2023, 5G will underpin future mobile innovation and services, building on ongoing deployments and adoption. 5G adoption will reach 17% this year, reaching 54% (equivalent to 5.3 billion connections) by 2030. The technology will add almost USD1 trillion to the global economy in 2030, spreading benefits across all industries. Such a huge rise in 5G adoption would drive the studied market.

- Further, in smart cities, 5G technology has the potential to enhance public security and safety significantly. Smart city systems can gather and analyze massive volumes of data from several sources, including video security cameras, intelligent traffic lights, and other iot devices, using the fast and responsive 5G network. For instance, Las Vegas is testing three pilot projects, with the government allocating USD 500 million to find ways to connect the entire city by 2025. The increase in the number of smart city projects undertaken by governments influences the demand for 5G infrastructure.

- The deployment of 5G networks requires significant infrastructure investments, including installing new base stations, small cells, and fiber optic cables. Compared to previous generations of cellular networks, 5G infrastructure deployment involves a denser network architecture due to its reliance on smaller cell sizes and increased network capacity. This densification increases the infrastructure requirements and overall capital expenditure, leading to high initial costs for network operators and service providers. This is expected to challenge the market's growth.

- Telecom operators expanded the offering of their 5G connection for several countries during the pandemic. For instance, in March 2021, Philippines-based Globe Telecom announced that it would accelerate its 5G Roaming rollout to other countries in the Middle East and Asia. Globe is set to open its 5G connection to visiting customers of Singtel of Singapore, CSL Hong Kong, and Ooredoo of Kuwait. In the post-pandemic era, the market is expected to grow further.

5G Infrastructure Market Trends

5G Radio Access Networks Expected to Hold Major Market Share

- RAN provides radio access network resources across wireless devices. Silicon chips in the core network, as well as the user equipment, enable the functionality of the RAN. A radio access network (RAN) encompasses base stations, antennas, macro cells, and small cells. 5G can be deployed in two ways, through a 5G core network or connecting a 5G RAN to a 4G network.

- The migration to 5G has become a critical factor, as it will enable higher bandwidths, and lower latencies, to name a few. RAN disaggregation enabled by cloud RANs and open interfaces allows carriers to benefit from a wider ecosystem.

- According to Ericsson, 5G subscriptions are expected to increase globally between 2022 and 2023, rising from over 0.55 billion to over 1.67 billion. Further, according to GSMA, the usage of 5G in GCC states will be slightly higher (16% customer 5G adoption) than the global average (15%) by 2025, mainly driven by governments and mobile operators with the support of mobile technology partners. Moreover, the number of 5G subscriptions is expected to reach 129.62 million in the Middle East and North African regions. Such a huge rise in 5G subscriptions would drive the market.

- Therefore, major leading carriers request information (RFIs) for RAN disaggregation and open solutions. This is because they can have the flexibility to choose the best solutions for the different parts of the RAN. For instance, edge servers for virtualized baseband units (BBUs) can also be used to run applications within the edge cloud and RAN to reduce latency. The amalgamation of 5G NR with a virtualized RAN architecture is expected to open up new opportunities for low latency and IoT services.

- The growing partnerships in developed and developing economies in Asia-Pacific are analyzed to bolster the market's growth rate. For instance, in December 2022, in support of the NTT DOCOMO Open Radio Access Network Open RAN expansion plans, SAMSUNG Electronics announced it would provide a range of 5G radios. In addition to its current 3.4GHz radio support in DoCoMo, Samsung is adding new radios with a 3.7Ghz, 4.5Ghz, and 28Ghz frequency range. The radios support NTT DoCoMo's open Radio Access Network (O-RAN) expansion and cover all of the Time Division Duplex (TDD) spectrum bands held by the operator. As Samsung expands its coverage in Japan, the ability of NTT DOCOMO to take advantage of its spectrum holdings will allow it to build a diverse 5G network and offer enhanced services for consumers and enterprises throughout Japan. In the commercial network environment of NTT DOCOMO, they have also carried out interoperability tests on these new radios with basebands from various suppliers.

Asia Pacific Expected to Dominate the Market

- The Asia-Pacific region is witnessing growing investment in 5G infrastructure. China is one of the largest investors in 5G technology, even leaving behind the United States; hence, one of the significant markets for 5G infrastructure vendors too. The growing effort by the Chinese government, telecom operators, and vendors to deploy 5G as quickly as possible is bringing more investment into the market studied. The country also has some of the largest telecom 5G infrastructure providers, like Huawei. However, the US-China trade war has weakened the exports of some electronic segments in the last two years.

- According to the GSMA, by 2025, 40-50% of China's mobile users may be using 5G. The country is gaining more in terms of network convergence, network virtualization, and network slicing. The government also started to include standalone as part of its initial 5G deployment, owing to building a 5G network from the ground rather than evolving a 4G network into a 5G. This would enable the growth of the studied market in the region.

- The establishment of 5G is a high priority for the Japanese government. The Ministry of Internal Affairs and Communications (MIC) is the lead agency on 5G. Four companies submitted plans to MIC for the development of 5G networks. All four plans were approved based on certain conditions, including focusing on the needs of both urban and rural areas; maintaining appropriate and sufficient optical fibers to provide 5G service; and taking adequate cybersecurity measures, including measures against supply chain risks.

- According to the Ministry of Science and ICT (South Korea), As of March 2023, South Korea had approximately 29.6 million 5G subscribers. Such a huge number of 5G subscribers would drive the demand for the studied market and enable the market players to develop new solutions to cater to a wide range of needs of customers and capture the market share.

- The countries that are considered in the rest of Asia-Pacific are Vietnam, Thailand, and Indonesia, among others. The developments happening in the market, the rise in the initiatives towards smart cities, and the development of new technologies are expected to drive the demand for the studied market in the rest of the Asia-Pacific region.

5G Infrastructure Industry Overview

The intensity of competitive rivalry in the market studied is high, and it is expected to remain the same over the forecast period. The market studied comprises several global players vying for attention in a fairly contested market space. Major vendors include Cisco Systems Inc., Hewlett Packard Enterprise Development LP, MavenirSystems Inc., NEC Corporation, Nokia Corporation, Oracle Corporation, Qualcomm Technologies Inc., and many more. And many more are highly preferred 5G infrastructure providers across various end users and regions. The firm concentration ratio is expected to record higher growth during the forecast period because several firms are looking at this market as a lucrative opportunity to expand globally.

- February 2023 - Nokia extended its private 5G partnership with IT infrastructure firm Kyndrylfor an additional three years. The two companies announced the extension in a joint statement, noting that the pair will focus on developing and delivering LTE, 5G private wireless services, and Industry 4.0 solutions to clients worldwide.

- February 2023 - NEC Corporation and ADVA will jointly deploy time synchronization solutions for Telkom Indonesia, Indonesia's largest fixed network operator, to help the operator prepare its transport network to deliver time-sensitive 5G services across the country. New service monetization, such as providing ultra-low latency applications, is critical for mobile operators to build momentum in the 5G era. To meet the anticipated demands of mobile operators and partners using Telkom Indonesia's services, the company is enhancing the timing accuracy of its transport network.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Machine-to-Machine/IoT Connections Due to Involvement of Various Devices

- 5.1.2 Increase in Demand for Mobile Data Services

- 5.2 Market Restraints

- 5.2.1 High Initial Capital Expenditure due to Deployment of Network Architecture Model and Spectrum Challenges

- 5.3 Key Use-Cases Driving 5G

- 5.3.1 Automotive

- 5.3.2 Industrial

- 5.3.3 Consumer Electronics

- 5.3.4 Healthcare

- 5.3.5 Energy and Utilities

- 5.3.6 Public Infrastructure

- 5.3.7 Other Use Case

6 MARKET SEGMENTATION

- 6.1 By Communication Infrastructure

- 6.1.1 5G Radio Access Networks

- 6.1.2 5G Core Networks

- 6.1.3 Transport Networks

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Rest of Europe

- 6.2.3 Asia Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 South Korea

- 6.2.3.4 Rest of Asia Pacific

- 6.2.4 Rest of the World

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Hewlett Packard Enterprise Development LP

- 7.1.3 Mavenir Systems Inc.

- 7.1.4 NEC Corporation

- 7.1.5 Nokia Corporation

- 7.1.6 Oracle Corporation

- 7.1.7 Qualcomm Technologies Inc.

- 7.1.8 Telefonaktiebolaget LM Ericsson

- 7.1.9 ZTE Corporation

- 7.1.10 Samsung Electronics Co. Ltd

- 7.1.11 Qucell Networks Co. Ltd

- 7.1.12 Huawei Technologies Co. Ltd

- 7.1.13 Airspan Networks Inc.

- 7.1.14 CommScope Holding Company Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

5G 基礎設施報告:2030 年趨勢、預測與競爭分析

5G 基礎設施報告:2030 年趨勢、預測與競爭分析 2024年5G基礎設施設備全球市場報告

2024年5G基礎設施設備全球市場報告 全球 5G 基礎設施市場 - 預測(~2030 年)

全球 5G 基礎設施市場 - 預測(~2030 年) 全球5G基礎設施市場(2016-2030):按組件、運作頻率、服務類型、網路架構、產業和地區劃分的機會和預測

全球5G基礎設施市場(2016-2030):按組件、運作頻率、服務類型、網路架構、產業和地區劃分的機會和預測 全球 5G 小基地台的成長機會

全球 5G 小基地台的成長機會 5G 基礎設施市場報告:2030 年趨勢、預測與競爭分析

5G 基礎設施市場報告:2030 年趨勢、預測與競爭分析 5G基礎設施的全球市場

5G基礎設施的全球市場 5G基礎設施市場規模、佔有率、趨勢分析報告:按頻譜、按組件、按網路架構、按行業、按地區、細分趨勢,2023-2030年

5G基礎設施市場規模、佔有率、趨勢分析報告:按頻譜、按組件、按網路架構、按行業、按地區、細分趨勢,2023-2030年 5G基礎設施的全球市場 (2023-2030年):產業分析·規模·佔有率·成長率·趨勢·預測

5G基礎設施的全球市場 (2023-2030年):產業分析·規模·佔有率·成長率·趨勢·預測 5G 基礎設施市場:按晶片組、技術、通訊基礎設施、用途分類 - 2023-2030 年全球預測

5G 基礎設施市場:按晶片組、技術、通訊基礎設施、用途分類 - 2023-2030 年全球預測