|

市場調查報告書

商品編碼

1437965

瓦楞包裝:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Corrugated Board Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

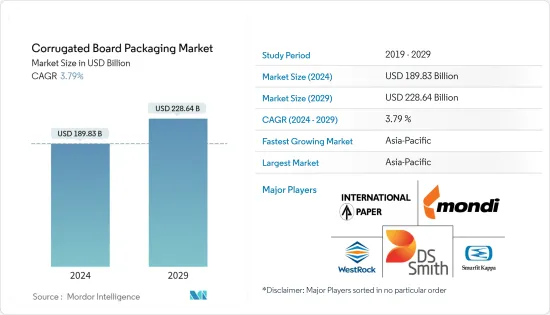

瓦楞包裝市場規模預計到 2024 年為 1,898.3 億美元,預計到 2029 年將達到 2,286.4 億美元,預測期內(2024-2029 年)複合年成長率為 3.79%。

紙板由紙漿和紙製成。因此,與塑膠包裝相比,它的可回收性很高。波紋槽介質可作為避震器,保護包裝產品免受外部衝擊。這些容器可以承受高壓,並且凹槽的不同層數和厚度具有緩衝等優點,可以保護包裝的貨物。

主要亮點

- 近年來,電子商務產業已成為重要的終端使用者產業。亞馬遜等著名電子商務公司使用瓦楞紙箱作為主要包裝,並使用塑膠來包裝單一產品。

- 即使在網路購物已經很普及的國家,電子商務也有望繼續保持成長勢頭。據摩根士丹利稱,由於韓國發達的付款和物流基礎設施,線上銷售佔韓國零售總額的37%。然而,預計成長將持續。由於當日送達和食品配送選擇,韓國的電子商務預計在未來五年內將成長 45%。摩根士丹利預計,電子商務規模可能從 2022 年 6 月的 3.3 兆美元成長到 2026 年的 5.4 兆美元。

- 紙板用途廣泛。因此,它可以呈現各種形狀,包括盒子。永續性問題正在逐漸取代軟性塑膠袋。此外,瓦楞紙箱是各種印刷技術的完美基礎。因此,企業傾向於選擇紙板包裝作為行銷工具。它們還可以充當行動廣告牌,因此企業不必在行銷上花費額外的資金。

- 人們忙碌的生活方式增加了對即食食品的需求。由於瓦楞紙包裝可以防潮並且可以承受較長的運輸時間,越來越多的公司採用這種包裝類型來為客戶提供更好的結果。麵包、肉品和其他生鮮食品等加工食品的需求量很大,因為這些包裝材料只需使用一次。

- 由於 COVID-19感染疾病,食品包裝的成長以及電子商務出貨不斷增加對紙板的需求不斷增加是所研究市場的一些關鍵促進因素。電子商務入口網站對雜貨包裝、醫療保健產品和電子商務運輸的需求急劇增加。同時,對奢侈品、工業和一些 B2B 運輸包裝的需求有所減少。

瓦楞紙板市場趨勢

加工食品領域預計將佔據主要市場佔有率

- 人們忙碌的生活方式增加了對即食食品的需求。因此,準備時間較短的加工食品吸引了許多消費者。隨著人口的成長,對方便加工食品的需求也在增加。

- 由於瓦楞紙包裝可以防止水分從產品中逸出,並且可以承受較長的運輸時間,因此越來越多的公司採用這種包裝來提供更好的客戶成果,特別是在二級或三級包裝中。麵包、肉品和其他生鮮食品等加工食品的需求量很大,因為這些包裝材料只需使用一次。

- 紙板包裝正成為各種食品塑膠包裝的可行替代品。瓦楞紙箱包裝更容易由回收材料製成,並且可以回收或堆肥。

- 消費者,尤其是千禧世代,越來越意識到食品包裝、食品生產和食品浪費對環境的影響。根據斯道拉恩索的一項研究,59% 的千禧世代認為包裝在整個價值鏈中應該是永續的。對永續包裝產品的需求是加工食品包裝的關鍵驅動力,對瓦楞包裝市場的成長產生正面影響。

- 據日本經濟產業省稱,用於加工食品和飲料的紙板消費量正在穩步成長。 2017年,日本加工食品和飲料的消費量為39.3億平方公尺,2021年將增加至41.4億平方公尺。

中國預計在亞太地區佔較大佔有率

- 中國瓦楞包裝產業深受人均收入成長、社會風氣變化和人口趨勢的影響。這種變化需要新的包裝材料、工藝和形狀。阿里巴巴等不斷發展的電子商務公司預計將在預測期內刺激紙板市場。

- 例如,在2021年阿里巴巴雙11購物活動期間,中國消費者總共購買了價值5,403億元人民幣(約845.4億美元)的產品。此外,據阿里巴巴和京東市場等電子商務供應商稱,中國消費者花費了美元。雙十一消耗了1390億美元,增加了各種產品的庫存和儲存,並增加了對紙板包裝的需求。

- 由於城市人口的增加、電子商務包裝行業的發展、紙漿價格的下降以及公眾對環保包裝意識的增強,中國瓦楞包裝市場預計將成長。瓦楞紙板生產能力的提高和技術進步是該行業的主要趨勢和發展之一。然而,嚴格的法規和產品品質等一些障礙可能會阻礙市場的擴張。

- 目前,中國食品飲料、IT電子、家電等產業對紙板的需求量較大,消費也日益成熟。由於主要終端用戶行業的包裝升級趨勢,中高檔瓦楞紙箱市場規模預計將持續成長。

- 此外,促進該國瓦楞包裝市場加速發展的因素包括城市人口環保意識的增強、對永續包裝的需求、對便利包裝的需求增加、電子商務活動的成長、電子產品需求的增加為了。商品、家居和個人保健產品。

瓦楞紙板行業概況

瓦楞包裝市場分散,許多公司提供瓦楞包裝解決方案。本公司不斷創新,推動永續包裝,提供環保包裝產品。為了利用這個機會,公司已經開始為各種最終用戶產業設計瓦楞紙箱。市場上也見證了市場相關人員的多次聯盟和收購,以加強其在瓦楞包裝領域的產品組合。

- 2022 年 5 月-Mondi 宣布投資 2.8 億歐元增加瓦楞紙板和紙板產量。該投資將有助於擴大捷克共和國、波蘭、德國和土耳其的產能並提高效率。其中,1.85 億歐元將投資於該公司位於中歐和東歐的 Corrugated Solutions 工廠網路。

- 2022 年 4 月 -英國永續包裝供應商 DS Smith 開發並推出了用於醫療設備電子商務運輸的瓦楞紙箱。這種新型瓦楞紙箱採用單一材料解決方案,而不是帶有一次性塑膠插件的黏合包裝。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭公司之間的敵意強度

- 評估新型冠狀病毒感染疾病(COVID-19)對市場的影響

第5章市場動態

- 市場促進因素

- 輕質材料的採用增加以及紙板數位印刷的發展

- 電商產業需求旺盛

- 市場課題

- 增加可回收和可重複使用包裝的使用

第6章市場區隔

- 依最終用戶產業

- 加工過的食品

- 生鮮食品及農產品

- 飲料

- 個人和家庭護理

- 電子商務

- 其他最終用戶產業(電氣電子、醫療保健、工業、紡織、玻璃和陶瓷)

- 依地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 波蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 泰國

- 澳洲

- 馬來西亞

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲

- 北美洲

第7章 競爭形勢

- 公司簡介

- International Paper Company

- Mondi Group

- DS Smith PLC

- WestRock Company

- Smurfit Kappa Group

- Stora Enso Oyj

- Sealed Air Corporation

- Neway Packaging

- Wertheimer Box Corp.

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings Limited

- Oji Holdings Corporation

第8章投資分析

第9章市場的未來

The Corrugated Board Packaging Market size is estimated at USD 189.83 billion in 2024, and is expected to reach USD 228.64 billion by 2029, growing at a CAGR of 3.79% during the forecast period (2024-2029).

Corrugated boards are made of pulp and paper; therefore, they are extremely recyclable compared to plastic packaging. The corrugated board's fluting medium serves as a shock absorber, shielding packaged items from external impact. These containers can bear high pressure, and the flutes' varied layers and thicknesses offer advantages, including cushioning to safeguard packaged goods.

Key Highlights

- The e-commerce industry emerged as a significant end-user industry in recent years. Prominent e-commerce companies, such as Amazon, have been using corrugated board boxes for principal packaging, and they rely on plastic packaging for individual items.

- E-commerce is expected to continue to gain traction, even in countries where online shopping is already popular. According to Morgan Stanley, In South Korea, due to well-developed payments and logistics infrastructure, online sales account for 37% of all retail activity. However, the growth is expected to continue further. E-commerce in South Korea is anticipated to increase by 45% in the next five years, driven by same-day delivery and food delivery options. Morgan Stanley estimates suggest that e-commerce could grow from USD 3.3 trillion as of June 2022 to USD 5.4 trillion in 2026.

- The corrugated board is highly versatile. Thus, it can take various forms including box. Due to sustainability issues, it is slowly replacing flexible plastic bags. Moreover, corrugated boxes are a perfect base for several printing techniques. Thus, companies tend to prefer corrugated packaging as a marketing tool. They also act as mobile billboards, where the companies do not have to spend additionally on marketing.

- The demand for convenience foods is rising due to people's busy lifestyles. As corrugated board packaging keeps moisture away and withstands long shipping times, companies are increasingly adopting this packaging type to offer better outcomes to customers. Processed foods, such as bread, meat products, and other perishable items, need these packaging materials to be used just once, thus driving the demand.

- The growth in food packaging and ever-increasing demand for corrugated packages in growing e-commerce shipments are some of the primary drivers of the studied market resulting from the COVID-19 outbreak. In e-commerce portals, demand has sharply increased for grocery packaging, healthcare products, and e-commerce shipments. At the same time, the need for luxury, industrial, and some B2B-transport packaging has declined.

Corrugated Packaging Market Trends

Processed Food Segment Expected to Occupy Significant Market Share

- The demand for convenience foods is rising due to people's busy lifestyles. Hence, processed food, which takes less time to cook, attracts many consumers. The increasing population also drives the demand for processed food, which is convenient.

- As corrugated board packaging keeps moisture away from products and can withstand long shipping times, companies are increasingly adopting this packaging to offer better customer outcomes, especially for secondary or tertiary packaging. Processed foods, such as bread, meat products, and other perishable items, need these packaging materials to be used just once, thus driving the demand.

- Corrugated board packaging is becoming a viable alternative to plastic packaging for many different food products. Corrugated box packaging can be created more simply from recycled materials and recycled or composted.

- Consumers, particularly millennials, are becoming more aware of the impact of food packaging, food production, and food waste on the environment. According to a Stora Enso survey, 59% of millennials think that packaging should be sustainable throughout the value chain. Demand for sustainable packaging products is a key driver in processed food packaging positively impacting corrugated board packaging market growth.

- According to the Ministry of Economy, and Industry of Japan, volume consumption of corrugated cardboard boxes for processed food and beverages has been steadily rising. In 2017, the consumption volume was 3.93 billion square meters for processed food and beverages which increased to 4.14 billion square meters in 2021 in Japan.

China is Expected to Hold Significant Share in Asia Pacific

- The Chinese corrugated board packaging sector is heavily influenced by the rising per capita income, changing social atmosphere, and demographics. As a result of this shift, new packaging materials, processes, and forms are required. Over the forecast period, growing e-commerce companies such as Alibaba are expected to fuel the corrugated packaging market.

- For example, Chinese shoppers purchased a total of CNY 540.3 billion (nearly USD 84.54 billion) value merchandise during Alibaba's Double 11 shopping event in 2021. In addition, according to the e-commerce vendors like Alibaba and JD.com, Chinese shoppers spent USD 139 billion during the Single's day festival, thus raising the inventory and storage of various goods and driving the demand for corrugated packaging.

- The growing urban population, developing e-commerce package industry, declining pulp prices, and improving population awareness about eco-friendly packaging are expected to propel China's corrugated board packaging market. Increased containerboard capacity and technological breakthroughs are among the industry's key trends and developments. However, some obstacles, such as tight rules and product quality, can stifle market expansion.

- Industries, including food and beverage, IT electronics, and home appliances, which have a huge demand for corrugated boxes, are currently witnessing a trend of consumption upgrading in China. The trend of upgrading packaging in leading end-user industries is expected to lead to continued growth in the market size of mid to high-end corrugated cartons.

- Further, factors that are contributing to the acceleration of the corrugated packaging market in the country are the growing environmental awareness by the urban population, demand for sustainable packaging, increasing demand for convenient packaging, growth in e-commerce activity, and rising demand for electronic goods and home and personal care products.

Corrugated Packaging Industry Overview

The market for corrugated board packaging is fragmented, with many players providing corrugated board packaging solutions. Companies are constantly innovating to promote sustainable packaging and provide eco-friendly packaging products. Companies are launching corrugated box designs for various end-user industries to leverage the opportunities. The market is also witnessing multiple partnerships and acquisitions by market players to strengthen their portfolios in the corrugated board packaging segment.

- May 2022 - Mondi announced to invest EUR 280 million to increase the production of corrugated board and cardboard. This investment will help to expand capacity and increase efficiency in the Czech Republic, Poland, Germany and Turkey. Of this investment figure, EUR 185 million will go to the company's network of Corrugated Solutions plants in Central and Eastern Europe.

- April 2022 - DS Smith, a UK-based sustainable packaging provider, developed and launched a corrugated cardboard box for e-commerce shipments of medical devices. This new corrugated cardboard box features a single-material solution in place of glued packaging with a single-use plastic insert.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Lightweight Materials and Evolution of Digital Print for Corrugated Boards

- 5.1.2 Strong Demand from the E-commerce Sector

- 5.2 Market Challenges

- 5.2.1 Increasing Usage of Returnable and Reusable Packaging

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Processed Foods

- 6.1.2 Fresh Food and Produce

- 6.1.3 Beverages

- 6.1.4 Personal and Household Care

- 6.1.5 E-commerce

- 6.1.6 Other End-user Industries (Electrical & Electronics, Healthcare, Industrial, Textile, Glass & Ceramics)

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.2.5 Spain

- 6.2.2.6 Poland

- 6.2.2.7 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 South Korea

- 6.2.3.5 Indonesia

- 6.2.3.6 Thailand

- 6.2.3.7 Australia

- 6.2.3.8 Malaysia

- 6.2.3.9 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Argentina

- 6.2.4.3 Mexico

- 6.2.4.4 Rest of Latin America

- 6.2.5 Middle-East and Africa

- 6.2.5.1 Saudi Arabia

- 6.2.5.2 South Africa

- 6.2.5.3 United Arab Emirates

- 6.2.5.4 Rest of Middle-East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 International Paper Company

- 7.1.2 Mondi Group

- 7.1.3 DS Smith PLC

- 7.1.4 WestRock Company

- 7.1.5 Smurfit Kappa Group

- 7.1.6 Stora Enso Oyj

- 7.1.7 Sealed Air Corporation

- 7.1.8 Neway Packaging

- 7.1.9 Wertheimer Box Corp.

- 7.1.10 Georgia-Pacific LLC

- 7.1.11 Nine Dragons Paper Holdings Limited

- 7.1.12 Oji Holdings Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

瓦楞包裝的全球市場規模:佔有率、成長分析、類型、最終用途 - 2023-2030 年產業預測

瓦楞包裝的全球市場規模:佔有率、成長分析、類型、最終用途 - 2023-2030 年產業預測 2024年飲料紙盒包裝器材全球市場報告

2024年飲料紙盒包裝器材全球市場報告 紙箱包裝市場:按類型、材料、紙箱類型、應用分類 - 2024-2030 年全球預測

紙箱包裝市場:按類型、材料、紙箱類型、應用分類 - 2024-2030 年全球預測 飲料紙盒包裝器材市場:按類型、功能自動化、應用分類 - 2023-2030 年全球預測

飲料紙盒包裝器材市場:按類型、功能自動化、應用分類 - 2023-2030 年全球預測 全球瓦楞包裝市場評估:按產品類型、按材料類型、按印刷技術、按最終用途行業、按地區、機會、預測(2016-2030)

全球瓦楞包裝市場評估:按產品類型、按材料類型、按印刷技術、按最終用途行業、按地區、機會、預測(2016-2030) 瓦楞包裝軟體全球市場 2023-2027

瓦楞包裝軟體全球市場 2023-2027 飲料紙盒包裝機的全球市場 - 市場規模、佔有率、成長分析:依類型(側面裝載紙盒、頂部裝載紙盒)、依功能自動化(自動機器、半自動機器) - 產業預測(2023-2030)

飲料紙盒包裝機的全球市場 - 市場規模、佔有率、成長分析:依類型(側面裝載紙盒、頂部裝載紙盒)、依功能自動化(自動機器、半自動機器) - 產業預測(2023-2030) 全球飲料紙盒包裝機械市場

全球飲料紙盒包裝機械市場 全球瓦楞包裝市場

全球瓦楞包裝市場 全球紙箱包裝市場

全球紙箱包裝市場