|

市場調查報告書

商品編碼

1437376

NFT 遊戲:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)NFT Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

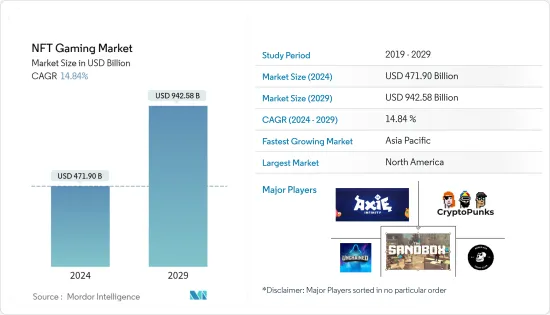

NFT 遊戲市場規模預計 2024 年為 4,719 億美元,預計到 2029 年將達到 9,425.8 億美元,在預測期內(2024-2029 年)複合年成長率為 14.84%。

此外,不可替代代幣(NFT)和數位資產將反映遊戲內容並為遊戲中的區塊鏈技術提供支援。雖然支援 NFT 的區塊鏈網路使玩家能夠擁有所有權並證明稀缺性、互通性和不變性,但這些代幣是獨特的、稀有的和不可分割的。

主要亮點

- 有很多優點。這有幾個優點。例如,在典型的遊戲中,玩家從購買裝甲升級中獲得的唯一好處是在特定遊戲範圍內改進遊戲玩法。然而,在使用(NFT)的遊戲生態系統中,相同的盔甲可以被代幣化,將遊戲內購買轉化為可轉讓資產,在連接的遊戲中授予利益,或者將它們交易為現金或其他數位資產。你可以交換它。

- 此外,收藏型遊戲利用數位資產的稀缺性和稀缺性來提高玩家的參與度,並激勵他們在遊戲中投入時間和金錢。這是透過各種遊戲元素來實現的,包括隨機獎品、限時商品以及實現某些里程碑和目標的獎勵。

- 在區塊鏈遊戲中,B2C和B2B交易都存在。然而,大多數遊戲只關注商業和消費者交易的有效用戶介面。為了獲得最佳的 B2C 用戶體驗,遊戲介面需要支援即時交易和錢包,這可能會阻礙市場成長。

- 儘管 NFT 越來越受歡迎,但它們仍然面臨著版權問題、智慧財產權問題、環境影響和安全風險等課題。目前還不清楚它們是否會成功獲得主流認可,或者是否能夠維持利基市場。

- COVID-19感染疾病對遊戲領域的 NFT 產生了積極影響。封鎖和其他社會隔離措施使人們留在家裡,並增加了對線上遊戲的需求。疫情期間區塊鏈遊戲的接受度提高可歸因於其新的遊戲機制和商業化戰略。

NFT遊戲市場趨勢

元宇宙運動的增加預計將增加市場需求

- 隨著「元宇宙」概念的不斷發展,現在有更多的選擇。 Pioneer 越來越注重自下而上的策略,即遊戲從 NFT 生態系統中湧現,而不是不同遊戲之間的 NFT互通性。例如,想像一下 CryptoKitties 或 Bored Apes 之間在平台之間跳躍的競賽。

- 此外,跨平台傳輸需要設計師幫助改善玩家體驗和平衡。 NFT 很少一致地定義遊戲商品的實際效用。它只是所有權的象徵。例如,一把劍 NFT 很容易從一款遊戲中的相當強大變成另一款遊戲中完全平庸的。

- 圖形介面本身也存在問題。許多設計程式(例如 Unreal 和 Unity)可用於開發遊戲的 3D 圖形資源。這些項目使用連接到特定渲染引擎的專有資料格式。然而,讓他們合作可能很複雜。

- 據思科系統公司稱,預計 2020 年線上遊戲領域的消費者資料流量約為每月 7 Exabyte,高於 2017 年的 1 EB。 2017年至2022年該子區隔的複合年成長率將達到59%。

- 企業家們正在推出解決方案來滿足不斷成長的需求,使元宇宙成為可行的推動者。例如,MetaverseGo 在 2022 年 6 月表示將推出一款應用程式以方便存取基於 NFT 的遊戲。這些遊戲通常要求玩家完成需要時間和精力才能理解的動作,例如創建加密貨幣錢包。只需使用行動電話號碼,該應用程式就可以代表您執行其中一些任務。

- 此外,2023 年 1 月,領先的科技公司之一 NFT Technologies Inc. 宣布,它是 web3 工作室 Run It Wild 和 Animoca Brands 的子公司,也是合作的領先去中心化遊戲虛擬世界 Sandbox 之一。 Sandbox 宣布努力透過引進新合作夥伴來擴展其生態系統。

北美佔最大市場佔有率

- 預計北美地區在預測期內將大幅擴張。該地區的成長可歸功於 Splinterlands、Uplandme Inc.、Mythical Inc. 和 ROKO GAME STUDIOS 等主要行業參與者以及大量精通技術的個人社區的存在。此外,區塊鏈技術和加密貨幣通常得到北美法規結構的支持。

- 隨著不可替代代幣 (NFT) 的日益普及,許多區塊鏈遊戲開發商正在創建自己的 NFT 市場,以允許玩家購買、出售和交易遊戲內資產。因此,遊戲玩家現在可以在二級市場上將其遊戲內資產收益,而該領域的區塊鏈遊戲創作者也獲得了新的收入來源。

- 除了雲端遊戲的成長之外,虛擬伺服器(儲存所有遊戲的地方)還執行渲染遊戲場景、處理遊戲邏輯、視訊編碼和視訊串流等計算。一些玩家已經提供這些商業雲端遊戲服務,包括 Onlive、G-Cluster、StreamMyGame、Gaikai 和 T5-Labs。傳統遊戲市場可能面臨來自該行業的競爭。

- 獨特的數位資產,如不可替代代幣(NFT),保存在區塊鏈上,可以安全、公開地買賣,用於收藏遊戲。因此,對擁有和收集稀有或獨特數位資產感興趣的玩家擁有有吸引力的價值提案,這將推動全部區域的市場擴張。

NFT 遊戲產業概述

全球NFT遊戲市場競爭激烈,主要企業。目前,就市場佔有率而言,很少有大型競爭對手能夠控制大部分市場。然而,由於區塊鏈和雲端運算的普及,該行業的需求正在增加。一些公司正在透過贏得新契約和進入新市場來增加其市場佔有率。

- 2023 年 5 月 - The Sandbox 與 Affyn 合作,Affyn 是一家總部位於新加坡的 Web3Start-Ups,該公司創建具有擴增實境和基於位置的功能的遊戲和元宇宙。這兩個組織將共同努力改善可互通的元宇宙體驗,匯集世界各地的創作者和合作者,創建一個融合虛擬和現實世界的長期生態系統,這是一個突破性的項目,構建一個以社區為中心、可互通、開放的元宇宙。

- 2022 年 6 月 - 以 NFT 為中心的遊戲平台 Cryptoys 在由 Andreessen Horowitz、OnChain Studios 及其母公司領投的 A 輪資金籌措中籌集了 2300 萬美元。該公司計劃利用這筆資金建立一個基於 NFT 的遊戲世界,其中包括可以玩和賺錢的遊戲,以及用戶可以與收藏玩具互動的地方。 Cryptoids 也計劃專注於新的動畫系列。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 遊戲中的 NFT-模式轉移

- 市場概況

- 預期採用趨勢 - 根據向遊戲的轉變,每個階段的比例可能會更大

- 第一代-NFT

- 第二代-NFT+P2E

- 第三代 - 比 NFT+P2E+ 更高的品質/渲染

- 第四代-NFT+P2E+AAA頭銜+傳統遊戲模式的轉變

- 市場促進因素

- NFT 帶來了分配方式的根本轉變,從面向發行商的模式(零和)轉向去中心化模式,其中 DAO 社群、玩家、發行商和遊戲玩家生態系統都從回報中受益。

- 元宇宙的發展和加密產業意識的不斷增強將進一步推動採用。

- 由鄰近市場現有企業提供資金支持的強大生態系統

- 市場課題

- 監管不確定性仍然是一個關鍵問題

- 人們相對缺乏對基於 NFT 的模型的好處以及使用基於區塊鏈的模型的環境課題的認知。

- 產業生態系統分析

第5章 遊戲NFT-產業人口統計

- 遊戲中 NFT 的當前潛在市場和記錄的活躍錢包數量(2020-2021 年)

- 依地區分類的需求區隔 - 北美、歐洲、亞太地區和世界其他地區

- 依遊戲類型分類的需求區隔 - 行動遊戲、主機、下載遊戲/盒裝遊戲

第6章 PLAY-TO-EARN 遊戲市場形勢

- 目前P2E遊戲市場規模及在整個遊戲產業的相對佔有率

- 主要市場影響者和推動者

- Gamefi 在促進 P2E 採用方面的作用

第7章 NFT遊戲廠商形勢

- 遊戲產業整體NFT(含遊戲內交易量)

- 頂級 NFT 遊戲報導

- Axie Infinity

- Gods Unchained

- CryptoPunks

- Bored Ape Yacht Club

- The Sandbox

第 8 章 GAMEFI 2.0 - 下一次迭代及其屬性

- GameFi 將基於更好的社交互動、元宇宙屬性的整合以及所有關鍵相關人員更低的進入門檻進行最佳化

- 市場展望

第9章投資分析-遊戲廠商的區塊鏈

The NFT Gaming Market size is estimated at USD 471.90 billion in 2024, and is expected to reach USD 942.58 billion by 2029, growing at a CAGR of 14.84% during the forecast period (2024-2029).

Additionally, non-fungible tokens (NFTs) and digital assets reflect in-game content and power blockchain technology in gaming. The blockchain networks that support NFTs enable player ownership and prove scarcity, interoperability, and immutability, while these tokens are one-of-a-kind, uncommon, and indivisible.

Key Highlights

- It offers many advantages. It has several advantages. For instance, in a typical game, the only advantage a player receives from purchasing an armor upgrade is better gameplay inside the confines of that specific game. However, in a gaming ecosystem that uses (NFTs), the same armor can be tokenized to convert in-game purchases into transferable assets that may bestow benefits across connected games or be traded for cash or other digitall assets.

- Additionally, collectible games use the rarity and scarcity of digital assets to increase player engagement and motivate them to invest their time and money in the game. This is accomplished through various gameplay elements, including randomized awards, goods only available for a limited time, and rewards for reaching certain milestones or objectives.

- In blockchain gaming, both B2C and B2B transactions exist. However, most games only emphasize an effective user interface for business-to-consumer transactions. For the best possible B2C user experience, the gaming interface must support instant trades and a wallet, which might hamper the market growth.

- Although NFTs are becoming more and more popular, they continue to face challenges that include copyright issues, intellectual property concerns, the impact on the environment and security risks. Whether they will succeed in gaining mainstream acceptance or retain a niche market is unclear.

- The COVID-19 pandemic has positively impacted the NFT In the gaming sector, NFT. Lockdowns and other social isolation measures caused people to stay home, increasing demand for online gaming. A rise in acceptance of blockchain-based games during the pandemic can be attributed to their new gameplay mechanics and monetization strategies.

NFT Gaming Market Trends

Increasing Move Towards Metaverse is Expected to Increase the Demand of the Market

- There are now more options because of the growing "metaverse" notion. Pioneers increasingly see a bottom-up strategy where games emerge from NFT ecosystems rather than NFT interoperability between different games. For example, consider races amongst CryptoKitties or platform-jumping Bored Apes.

- Additionally, cross-platform transferability would cause designers to need help with player experience and balance. An NFT hardly defines the real utility of game goods consistently; it is merely a symbol of possession. For instance, an NFT of a sword might easily be changed from being reasonably powerful in one game to utterly overwhelming in another.

- The graphical interface itself has difficulties as well. Many design programs, such as Unreal or Unity, can be used to develop 3D graphic assets for games. These items use exclusive data formats that are connected to certain rendering engines. However, getting them to cooperate can be complicated.

- According to Cisco Systems, in 2020, consumer data traffic in the online gaming segment is expected to be about 7 exabytes per month, an increase from 1 EB in 2017. The 2017-2022 CAGR of this subsegment amounts to 59 percent.

- Entrepreneurs have launched solutions in response to the rising demand, making the metaverse an attainable factor. For instance, MetaverseGo stated in June 2022 that it would publish an app to facilitate access to NFT-based games. These games frequently demand players to complete actions that take some time and effort to understand, such as creating a cryptocurrency wallet. With just a mobile number, the app can do some of these tasks for the user.

- Furthermore, in January 2023, NFT Technologies Inc., one of the leading technology companies, partnered with web3 studio Run It Wild and Sandbox, one of the leading decentralized gaming virtual worlds, a subsidiary of Animoca Brands. The Sandbox announced efforts to expand its ecosystem by onboarding new partners.

North America to hold largest Market share

- Over the forecast period, North America is anticipated to have significant expansion. The region's growth can be ascribed to major industry companies like Splinterlands, Uplandme Inc., Mythical Inc., and ROKO GAME STUDIOS and the presence of a sizable community of technologically savvy people. Additionally, blockchain technology and cryptocurrencies are usually supported by the regulatory framework in North America.

- Many blockchain game developers are creating their own NFT marketplaces so that players can buy, sell, and trade in-game assets as non-fungible tokens (NFTs) become more popular. As a result, gamers can now monetize their in-game assets on a secondary market, and blockchain game creators in the area also have a new source of income.

- In addition to the growth of cloud gaming, the virtual server (where all of the games are kept) performs computations such as game scene rendering, game logic processing, video encoding, and video streaming. Several players, including Onlive, G-Cluster, StreamMyGame, Gaikai, and T5-Labs, already provide these commercial cloud gaming services. The traditional gaming market is potentially facing competition from this industry.

- Unique digital assets, like Non-fungible Tokens (NFTs), which are kept on a blockchain and can be bought or sold securely and openly, are used in collectible games. As a result, players interested in owning and collecting rare or unique digital assets have a compelling value proposition that fuels market expansion throughout the region.

NFT Gaming Industry Overview

The global NFT gaming market is highly competitive and consists of major players. Few of the big competitors now control the majority of the market in terms of market share. However, the industry is experiencing increased demand due to the widespread implementation of blockchain and cloud computing. By winning new contracts and entering new markets, several corporations are expanding their market share.

- May 2023 - The Sandbox has partnered with Affyn, a Singapore-based Web3 startup creating games and metaverses with built-in augmented reality and geolocation features. Together, these two organizations will improve the interoperable metaverse experiences and create a groundbreaking, community-focused interoperable and open metaverse that will bring together the world's creators and collaborators to build long-term ecosystems that merge the virtual and real worlds.

- June 2022 - Cryptoys, an NFT-centric gaming platform, in a Series A fundraising round headed by Andreessen Horowitz, OnChain Studios and its parent business, raised USD 23 million. The business plans to utilize the money to create an NFT-based gaming world that will have play-and-earn games and let users interact with collector toys. Cryptoys will also be putting in effort on a fresh animated series.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 NFT IN GAMING - A PARADIGM SHIFT

- 4.1 Market Overview

- 4.2 Anticipated Adoption Trends - A Broader Percentage for Each Stage to be Attributed Based on Switch to Gaming

- 4.2.1 First Gen - NFT

- 4.2.2 Second Gen - NFT + P2E

- 4.2.3 Third Gen - NFT + P2E + Higher quality/rendering

- 4.2.4 Fourth Gen - NFT + P2E + AAA Titles + Shift from traditional gaming modes

- 4.3 Market Drivers

- 4.3.1 NFT has Led to a Fundamental Change in Distribution from a Publisher-oriented Model (Zero-Sum) to a Distributed Model Where DAO Community, Players, Publishers and Gamer Ecosystem Stand to Benefit from the Returns.

- 4.3.2 The Move Towards Metaverse Coupled with Increased Awareness on the Crypto Industry will Further Drive Adoption

- 4.3.3 Robust Ecosystem Backed by Funding from Incumbents from Adjacent Markets

- 4.4 Market Challenges

- 4.4.1 Regulatory Uncertainty Remains a Key Concern

- 4.4.2 Relative Lack of Awareness on the Benefits of NFT-Based Models and Environmental Challenges due to use of Blockchain-based Models

- 4.5 Industry Ecosystem Analysis

5 GAMING NFT - INDUSTRY DEMOGRAPHICS

- 5.1 Current Addressable Market for NFT in Gaming & # of Active Wallets Recorded (2020-2021)

- 5.2 Breakdown of the Demand by Region - North America, Europe, Asia-Pacific, and Rest of the World

- 5.3 Breakdown of the Demand by Gaming Type - Mobile, Console and Download/Box

6 PLAY-TO-EARN GAMING MARKET LANDSCAPE

- 6.1 Current Addressable Market for P2E Gaming and its Relative Share in the Overall Gaming Industry

- 6.2 Key Market Influencers and Enablers

- 6.3 Role of Gamefi in Driving P2E Adoption

7 NFT GAMING VENDOR LANDSCAPE

- 7.1 Overall NFT (including in-game transaction volume) in the Gaming industry

- 7.2 Coverage on the top NFT Games

- 7.2.1 Axie Infinity

- 7.2.2 Gods Unchained

- 7.2.3 CryptoPunks

- 7.2.4 Bored Ape Yacht Club

- 7.2.5 The Sandbox

8 GAMEFI 2.0 - THE NEXT ITERATION and its ATTRIBUTES

- 8.1 GameFi to be Optimized on the Basis of Better Social Interactions, Integration of Metaverse Attributes, Lower Barriers to Entry for all the Key Parties

- 8.2 Market Outlook

9 INVESTMENT ANALYSIS - BLOCKCHAIN in GAMING VENDORS

非同質化代幣市場規模、佔有率、趨勢分析報告:按應用、類型、最終用途、地區、細分市場預測,2024-2030 年

非同質化代幣市場規模、佔有率、趨勢分析報告:按應用、類型、最終用途、地區、細分市場預測,2024-2030 年 2024-2028 年全球音樂 NFT 市場

2024-2028 年全球音樂 NFT 市場 NFT(非同質化代幣)世界市場報告 2024年

NFT(非同質化代幣)世界市場報告 2024年 2024-2028 年全球非同質化代幣(NFT) 市場

2024-2028 年全球非同質化代幣(NFT) 市場 NFT(非同質化代幣)市場報告:2030 年趨勢、預測與競爭分析

NFT(非同質化代幣)市場報告:2030 年趨勢、預測與競爭分析 非同質化代幣市場:按產品、應用和最終用戶分類:2023-2032年全球機會分析和產業預測

非同質化代幣市場:按產品、應用和最終用戶分類:2023-2032年全球機會分析和產業預測 不可取代代幣市場:按類型、報價、最終用途分類 - 2023-2030 年全球預測

不可取代代幣市場:按類型、報價、最終用途分類 - 2023-2030 年全球預測 加密電子貨幣、NFT報酬型P2E (Pay-to-Earn) 遊戲的全球市場:考察與預測 (到2029年)

加密電子貨幣、NFT報酬型P2E (Pay-to-Earn) 遊戲的全球市場:考察與預測 (到2029年) 非替代性權標(NFT)的全球市場:規模,佔有率,成長分析-各類型(物理資產,數位資產),各用途(收集品,美術品),各最終用途(個人,商業)-產業預測(2023年~2030年)

非替代性權標(NFT)的全球市場:規模,佔有率,成長分析-各類型(物理資產,數位資產),各用途(收集品,美術品),各最終用途(個人,商業)-產業預測(2023年~2030年) 食品和飲料非同質代幣 (NFT) 市場份額、規模、趨勢、行業分析報告,按類型、按應用、按地區、按細分市場和預測,2023-2032 年

食品和飲料非同質代幣 (NFT) 市場份額、規模、趨勢、行業分析報告,按類型、按應用、按地區、按細分市場和預測,2023-2032 年