|

市場調查報告書

商品編碼

1435971

汽車智慧玻璃:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Automotive Smart Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

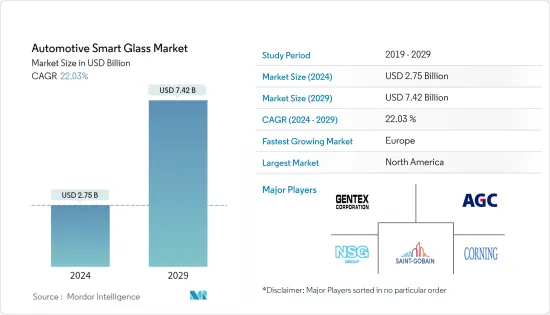

2024 年汽車智慧玻璃市場規模估計為 27.5 億美元,預計到 2029 年將達到 74.2 億美元,在預測期間(2024-2029 年)以 22.03% 的複合年增長率增長。

主要亮點

- 冠狀病毒感染疾病(COVID-19)大流行對市場產生了負面影響,因為汽車產量下降,並且由於製造業關閉而導致市場放緩。然而,隨著監管的放鬆和汽車生產開始成長勢頭,預計市場在預測期內將出現正成長。

- 汽車智慧玻璃的創新以及智慧玻璃在豪華和豪華汽車中的應用不斷增加預計將推動市場需求。此外,預計特斯拉、塔塔、梅賽德斯和寶馬等主要汽車廠商透過積極推出產品以及與汽車智慧玻璃製造商結盟,並不斷增加對市場的參與,進一步支持了預測期內的市場成長。

- 全球汽車產業的擴張以及運動型多用途車(SUV)和豪華車銷量的增加預計將推動汽車智慧玻璃的銷售。梅賽德斯-奔馳在其部分車輛的“Magic Sky Control”車頂中使用了智慧玻璃技術,麥克拉倫將其作為麥克拉倫 720S 的選裝件。捷豹、路虎等一些汽車品牌最近發布了配備加熱擋風玻璃的新車款。加熱擋風玻璃是賓州冬季的理想選擇,因為它們比標準類型的除霧和除霜更快。

- 亞太和歐洲等地區預計將成為成長最快的汽車智慧眼鏡市場。在亞太地區,中國預計將繼續引領市場,而日本預計將成為汽車產業的技術中心。

汽車智慧玻璃市場趨勢

車輛中懸浮顆粒裝置 (SPD) 的普及越來越高

- 全球汽車銷量從2021年的約6,670萬輛增加至2022年的約6,720萬輛。 2020年及2021年,受全球經濟低迷影響,汽車產業進入下行趨勢。 2022年,COVID-19和俄羅斯烏克蘭感染疾病導致汽車半導體市場短缺,供應鏈進一步中斷。儘管面臨這些課題,2023 年銷售額預計仍將成長。

- 懸浮顆粒裝置(SPD)可以改善使用者的駕駛體驗。 SPD 智慧天窗、車頂系統、車窗和遮陽帽可將車輛的玻璃和塑膠轉變為動態可調且響應靈敏的燈光管理系統。根據後處理操作,SPD 玻璃的霧度最低為 2.5%。

- SPD玻璃比其他智慧玻璃效率更高,平均功耗為每平方公尺1.5瓦,而PDLC智慧玻璃的能源需求為每平方公尺3瓦。據大陸集團稱,SPD智慧眼鏡每公里可減少4克二氧化碳,續航里程增加5.5%。梅賽德斯使用 SPD 智慧眼鏡將熱量降低高達 10 攝氏度(18 華氏度)。

- 懸浮顆粒裝置是一種薄膜,可將汽車天窗和其他玻璃的透明度轉變為不透明,防止紅外線和紫外線輻射,防止紅外線和紫外線輻射導致車內過熱以及皮革和其他材料過早老化。例如,SPD 玻璃現在已應用於多種豪華梅賽德斯車型,特別是 S-Class 轎車和 SL Roadster。

- 由於COVID-19的影響,多個國家對原料的分銷和運輸實施了限制,擾亂了智慧薄膜供應鏈。這項限制對智慧眼鏡的定價產生了重大影響。製造工廠的關閉,尤其是汽車行業的製造工廠的關閉,導致市場收入大幅下降。

- 消費者對長期利益缺乏認知,以及高成本等日益複雜的問題很可能成為預測期內智慧窗戶SPD 擴張的市場限制。高價格和容易獲得的物品將是市場成長的最重要和最緊迫的障礙。然而,全球整體汽車銷售的增加預計將加速智慧眼鏡市場的發展。

預計歐洲將以市場最快的速度成長

- 過去幾年,全部區域對豪華車的需求不斷增加。此外,在疫情後的預測期內,對先進便利功能和豪華汽車的需求不斷增加,從傳統功能顯著轉向天窗和自動有色玻璃等先進便利功能。

- 推動市場成長的主要因素包括歐洲主要市場小客車銷量的增加、豪華車銷售的增加以及對汽車天窗的需求和偏好的成長。

- 幾十年來,德國汽車產業一直是歐洲汽車工業的支柱。德國已發展成為高科技汽車產品生產和創新最大的國家之一。此外,由於德國,歐洲汽車產業的研發淨成長了 60%。這顯示強大的創新中心在汽車智慧眼鏡的需求中發揮著舉足輕重的作用。

- 2022 年 5 月,微軟和大眾聯手將擴增實境眼鏡實用化。德國汽車製造商大眾汽車研究人員對移動出行的未來進行了展望。擴增實境被認為是未來行動概念的關鍵要素之一。為了更接近這個願景,大眾汽車與微軟合作,首次在移動車輛上推出 HoloLens 2混合實境眼鏡。

- 受多種因素影響,英國汽車業自英國以來一直處於低迷狀態,其中包括新型冠狀病毒感染疾病(COVID-19)和英國脫歐,影響了汽車銷售。產量,特別是小客車也在下降。

- 法國的外國汽車製造商對其車隊中的人工智慧(AI)和智慧玻璃等新技術的投資有所改善。例如,以色列智慧玻璃技術供應商Gauzy於2022年2月宣布將收購一家法國公司,以擴大其產品範圍,成為全球領先的照明控制和遮陽系統技術解決方案公司。

- 收購 Vision Systems 的條款和條件,Vision Systems 是 Tierone 的法國供應商,為航太、陸地運輸和海洋產業開發遮陽解決方案。 Gauzy 與包括戴姆勒在內的世界各地許多汽車製造商合作,將光控玻璃技術整合到他們的車輛中。並與 BMW、LG、汽車零件供應商 Brose、Vision Systems、Texas Instruments 等合作,提供各種照明和遮陽產品。

- 幾款配備智慧玻璃的新車的推出可能會推動製造商進入這一領域。這就是為什麼奧迪、寶馬、日產和路虎探測車等許多汽車製造商分別在 Q 系列、X 系列、逍客和極光等熱門車型上提供天窗選項。

汽車智慧玻璃產業概況

汽車智慧玻璃市場適度整合,聖戈賓、AGC Inc.、Nippon Sheet Glass、Gentex Corporation、Cornering Inc.等幾大公司憑藉其成熟和開發的產品在市場上佔據了較大佔有率。各種汽車製造商。兩家公司都專注於創新技術,並遵循收購、技術許可和合作夥伴關係等策略,以擴大、維持和捕捉汽車產業快速採用技術趨勢的潛在需求。

例如,2022年4月,AGP集團與OMERS資本市場和BMO金融集團合作簽訂了2.5億美元的債務融資協議,以加速公司的全球擴張計畫。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 汽車對 ADAS 的需求不斷成長

- 市場限制因素

- 高成本

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔(市場規模:金額)

- 依技術類型

- 電致變色

- 聚合物分散液體裝置(PDLC)

- 懸浮顆粒裝置(SPD)

- 依使用類型

- 後窗和側窗

- 天窗玻璃

- 前後玻璃

- 依車型

- 小客車

- 商用車

- 依地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 巴西

- 南非

- 其他國家

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- Corning Inc.

- Guardian Industries

- Saint-Gobain SA

- AGP Glass

- Hitachi Chemical Co. Ltd

- Research Frontiers Inc.

- Nippon Sheet Glass Co. Ltd

- AGC Inc.

- Gentex Corporation

- Gauzy Ltd.

第7章市場機會與未來趨勢

- 與聯網汽車技術整合

The Automotive Smart Glass Market size is estimated at USD 2.75 billion in 2024, and is expected to reach USD 7.42 billion by 2029, growing at a CAGR of 22.03% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic had a negative impact on the market as vehicle production declined, and the shutdown of manufacturing units resulted in a slowdown in the market. However, as restrictions were relieved and automobile production started gaining traction, the market was anticipated to have positive growth during the forecast period.

- Innovations in automotive smart glass and rising applications of smart glass in premium and luxury vehicles are expected to drive demand in the market. Further, the growing participation of key automotive players like Tesla, Tata, Mercedes, BMW, etc., in the market through active launches and collaborations with automotive smart glass manufacturers is anticipated to further support the growth of the market during the forecast period.

- Expansion of the automotive industry across the globe, along with increasing sales of sports utility vehicles (SUVs) and premium cars, is expected to drive sales of automotive smart glass. Mercedes-Benz uses smart glass technology for the "Magic Sky Control" roof on some of its vehicles, and McLaren offers it as an option in the McLaren 720S. Some car brands, including Jaguar and Land Rover, have recently released new car models with heated front windshields. A heated front windshield is ideal for Pennsylvania winters because it's able to defog and defrost faster than standard types.

- Regions like Asia-Pacific and Europe are forecasted to be the fastest-growing automotive smart glass market. In Asia-Pacific, China is expected to continue to be the driver of the market, with Japan being the hub of technology in the automotive sector.

Automotive Smart Glass Market Trends

Rise in penetration of suspended particle devices (SPD) in vehicles

- Worldwide car sales grew to around 67.2 million automobiles in 2022, up from around 66.7 million units in 2021. In 2020 and 2021, a faltering global economy caused the industry to experience a downward trend. In 2022, COVID-19 and the Russian war in Ukraine contributed to shortages in the automotive semiconductor market and additional supply chain disruptions. Despite these challenges, 2023 sales growth is anticipated.

- Suspended particle devices (SPD) can improve users driving experience. SPD-smart sunroofs, roof systems, windows, and visors turn car glass or plastic into a dynamically adjustable and responsive light-management system. Depending on the post-processing operations, SPD glasses provide a minimum haze of 2.5%.

- SPD glasses are more efficient than other smart glasses, with an average consumption of 1.5 watts per sq. m compared to the 3 watts per sq. m of the energy requirement of PDLC smart glass. According to Continental, SPD smart glass results in a 4 g per km carbon dioxide reduction, improving the driving range by 5.5%. Using SPD smart glass, Mercedes reduced the heat by up to 10 Celsius (18 Fahrenheit).

- A suspended particle device, a film that converts the transparency of car sunroofs and other glass to opaque, prevents the infrared and ultraviolet radiation that overheats interiors and prematurely ages leather and other materials. For instance, SPD glass is now available on a few high-end Mercedes models, notably the S-class sedan and SL roadster.

- Several countries implemented limitations on the distribution and transit of raw materials due to the impact of COVID-19, disrupting the supply chain of smart films. The limits had a significant influence on smart glass pricing. Shutdowns of manufacturing plants, particularly in the automobile sector, resulted in a massive decline in market income.

- Lack of consumer awareness of long-term advantages and a rising number of complications, such as high cost, would most likely operate as a market restraint for the expansion of SPD for smart windows in the projected period. The high cost of items and their ease of availability will be the most significant and immediate barrier to the market's growth. However, increased vehicle sales across the Globe are anticipated to fuel the market for smart glass.

Europe is Expected to Grow at the Fastest Rate in the Market

- The demand for luxury cars has increased across the region over the past few years. Additionally, there has been a huge shift from traditional features toward advanced convenience features, such as a sunroof and automatic tinted glass, owing to the increasing demand for advanced convenience features and luxury cars over the forecast period post-pandemic.

- Some of the major factors driving the growth of the market are a rise in sales of passenger cars in the major markets of Europe, increasing sales of luxury cars, and the increasing demand and preference for a sunroof in the vehicles.

- The German automotive sector has been the backbone of the European automotive industry for the last decades. Germany has evolved into one of the largest countries when it comes to the production and innovation of high-tech automotive products. In addition, a net of +60% growth has been observed in Europe's automotive sector for R&D on the back of Germany. This showcases that the strong innovation hub plays a pivotal role in the demand for automotive smart glass.

- In May 2022, Microsoft and Volkswagen collaborated to put augmented reality glasses in motion. The future of mobility by researchers at German automaker Volkswagen, who see augmented reality as one of the key elements of the future mobility concept. To get a little closer to this vision, Volkswagen has worked with Microsoft to make the mixed-reality glasses HoloLens 2 available for the first time in mobile vehicles.

- The automotive industry in the United Kingdom witnessed a downturn due to various factors, including COVID-19 and Brexit, which impacted vehicle sales from 2017 onward. The production figures, especially for passenger cars, have also been decreasing.

- France has witnessed some improved investments in new technology like artificial intelligence (AI) and smart glass in automotive fleets from foreign automakers. For instance, in February 2022, Israeli smart glass technology provider Gauzy announced that it would acquire a French company to expand its offerings and become the world's leading solution company for lighting control and shading system technology.

- Terms and conditions for the acquisition of Vision Systems, based in France, a Tieronesupplier developing shading solutions for the aerospace, land transportation, and marine industries. Gauzy has worked with many automakers around the world, including Daimler, to integrate its optical control glass technology into automobiles. We partner with BMW, LG, and auto parts suppliers Brose, Vision Systems, Texas Instruments, and others to offer a variety of lighting and shading products.

- Several new car launches with smart glass are likely to encourage manufacturers to operate in this segment. Hence, many car manufacturers, like Audi, BMW, Nissan, and Range Rover, are offering sunroof options in their popular models, like Q-series, X-series, Qashqai, and Evoque, respectively.

Automotive Smart Glass Industry Overview

The automotive smart glass market is moderately consolidated, with a few major players such as Saint Gobin, AGC Inc., Nippon Sheet Glass Co. Ltd., Gentex Corporation, and Cornering Inc. having significant shares in the market due to their well-established and developed products among various automakers. The companies are focusing on innovative technologies and following strategies, like acquisition, licensing the technology, and partnership, to expand, sustain, and capture the potential demand for rapid adoption of technological trends in the automotive industry.

For instance, in April 2022, AGP Group partnered with OMERS Capital Markets and BMO Financial Group and entered into a debt financing agreement of USD 250 million to accelerate the company's global expansion plan.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand for ADAS in Automobiles

- 4.2 Market Restraints

- 4.2.1 High Cost

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Million)

- 5.1 By Technology Type

- 5.1.1 Electrochromic

- 5.1.2 Polymer Dispersed Liquid Device (PDLC)

- 5.1.3 Suspended Particle Device (SPD)

- 5.2 By Application Type

- 5.2.1 Rear and Side Windows

- 5.2.2 Sunroof Glass

- 5.2.3 Front and Rear Windshield

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 South Africa

- 5.4.4.3 Other Countries

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Corning Inc.

- 6.2.2 Guardian Industries

- 6.2.3 Saint-Gobain SA

- 6.2.4 AGP Glass

- 6.2.5 Hitachi Chemical Co. Ltd

- 6.2.6 Research Frontiers Inc.

- 6.2.7 Nippon Sheet Glass Co. Ltd

- 6.2.8 AGC Inc.

- 6.2.9 Gentex Corporation

- 6.2.10 Gauzy Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration with Connected Car Technology

2024-2032 年按玻璃類型、材料類型、車輛類型、應用、最終用戶、技術和地區分類的汽車玻璃市場報告

2024-2032 年按玻璃類型、材料類型、車輛類型、應用、最終用戶、技術和地區分類的汽車玻璃市場報告 全球汽車玻璃維修和更換市場(2024年版):按金額、數量、玻璃類型、車輛、推進、應用、地區和國家進行分析、市場分析和考察(2019-2029)

全球汽車玻璃維修和更換市場(2024年版):按金額、數量、玻璃類型、車輛、推進、應用、地區和國家進行分析、市場分析和考察(2019-2029) 中國的汽車用玻璃市場

中國的汽車用玻璃市場 汽車玻璃市場規模、佔有率、趨勢分析報告:2023-2030 年按產品類型、車輛類型、最終用途、地區和細分市場進行的預測

汽車玻璃市場規模、佔有率、趨勢分析報告:2023-2030 年按產品類型、車輛類型、最終用途、地區和細分市場進行的預測 汽車玻璃市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按類型、按應用類型、車輛類型、地區、競爭細分

汽車玻璃市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按類型、按應用類型、車輛類型、地區、競爭細分 汽車用玻璃的全球市場 2023-2027

汽車用玻璃的全球市場 2023-2027 汽車全景擋風玻璃市場:按車型、玻璃類型、擋風玻璃位置、材料類型、銷售管道- 2023-2030 年全球預測

汽車全景擋風玻璃市場:按車型、玻璃類型、擋風玻璃位置、材料類型、銷售管道- 2023-2030 年全球預測 汽車擋風玻璃市場:按玻璃類型(夾層玻璃、強化玻璃玻璃)、按地點(擋風玻璃、後玻璃)、按分佈、按車輛分類 - 全球預測 2023-2030 年

汽車擋風玻璃市場:按玻璃類型(夾層玻璃、強化玻璃玻璃)、按地點(擋風玻璃、後玻璃)、按分佈、按車輛分類 - 全球預測 2023-2030 年 汽車玻璃市場:按類型(夾層玻璃、強化玻璃)、用途(背光、後四分之一玻璃、側鏡、後視鏡)- 2023-2030 年全球預測

汽車玻璃市場:按類型(夾層玻璃、強化玻璃)、用途(背光、後四分之一玻璃、側鏡、後視鏡)- 2023-2030 年全球預測 全球汽車玻璃市場規模、份額、行業趨勢分析報告,類型(夾層玻璃、鋼化玻璃)、車輛類型、最終用戶、應用、地區展望與預測,2023-2029

全球汽車玻璃市場規模、份額、行業趨勢分析報告,類型(夾層玻璃、鋼化玻璃)、車輛類型、最終用戶、應用、地區展望與預測,2023-2029