|

市場調查報告書

商品編碼

1433871

HaaS(硬體即服務)-市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Hardware-as-a-Service (HaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

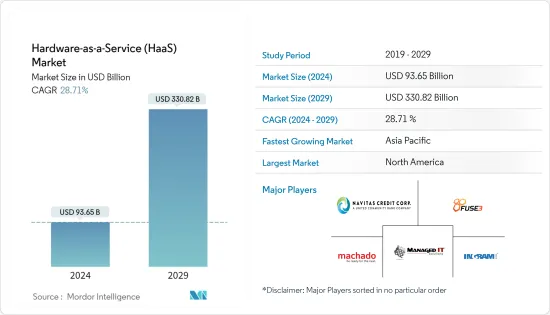

HaaS(硬體即服務)市場規模預計到 2024 年為 936.5 億美元,預計到 2029 年將達到 3,308.2 億美元,預測 2029 年複合年成長率為 28.71%。

實施新IT解決方案的需求不斷增加、數位化不斷提高、小型和大型企業對HaaS硬體和服務的投資增加、技術進步和產品創新以及雲端基礎設施負載的增加,是影響HaaS市場成長的關鍵因素。

主要亮點

- HaaS 模式在那些尋求新方法在競爭激烈的市場中為客戶提供服務、在不給財務營運帶來壓力的情況下獲取技術的公司中越來越受歡迎。對於定期維修或升級設備的公司來說,哈斯的方法更具成本效益。該服務提供廉價的託管解決方案,並包括作為租賃協議一部分的維護和支援。在客戶所在地安裝硬體由客戶和託管服務供應商(MSP) 商定,並且客戶每月支付服務費用。

- 隨著雲端平台變得越來越普及,硬體即服務(HaaS)市場有望發展。該解決方案非常實惠,適合中小型企業。因此,我們將為 HaaS(硬體即服務)領域在全球的擴展做出貢獻。

- 按需服務 (XaaS) 正在取代多個行業的所有權。雲端運算服務也吸引了更多對所研究領域的投資,因為資料儲存伺服器和主動運算設備構成了為消費者遠端提供的服務。

- 採用 HaaS 模型的一個根本障礙及其擴展的限制是缺乏對硬體即服務 (HaaS) 方法所提供的優勢的了解。印度、中國、巴西和印尼等開發中國家的公司不太可能採用這種服務模式,因為他們沒有意識到減少硬體更新、維護和更換成本等好處。

- 由於冠狀病毒感染疾病(COVID-19) 的爆發,服務公司尤其接受了在家工作的文化。這導致需求激增,主要是各種租賃筆記型電腦。然而,供應鏈和生產活動的完全中斷造成了硬體組件的供需之間的巨大錯配,從而在市場上產生了更多的需求。隨著局勢正常化以及在 COVID-19感染疾病等不可預見情況下業務完全關閉的風險降低,HaaS 預計將在未來幾季實現成長。

HaaS(硬體即服務)市場趨勢

零售/批發業佔據最大的市場佔有率

- HaaS 的採用情況因行業而異。在所有組織中,零售/批發組織在更大程度上採用了 HaaS 模式,其次是教育和金融服務業。零售/批發組織在世界各地擁有數百或數千家商店,這使得內部 IT 團隊難以為遠端地點提供服務。

- Spiceworks 對來自北美和歐洲組織的 1,100 多名 IT 決策者進行了調查,以了解硬體即服務 (HaaS) 模型在職場中的滲透情況。調查發現,大約 31% 的零售/批發組織已經在使用 HaaS 模型(一種或多種類型的設備)。另外 7% 的剩餘零售商計劃在未來兩年內實施 HaaS。零件更換、硬體支援和故障排除是此型號最常用的一些服務。

- 在大流行期間,零售業在許多國家被認為至關重要,並被允許保持開放,而其他行業則不得不關閉。由於零售商、批發商、超級市場和百貨公司對眾多硬體系統的需求不斷增加,預計該行業將佔據重要地位。

- 最近零售業有大量的投資和發展。透過數位帳本、庫存管理、付款解決方案、物流和履約工具等服務支援零售業的零售技術公司正在增加對 HaaS 服務的需求。

亞太地區的需求預計將推動成長

- 亞洲擁有印度和中國等一些成長最快的經濟體。 IT 和通訊業的大量勞動力和眾多企業預計將推動對 HaaS(硬體即服務)模式的需求。

- 此外,一些生命科學和零售組織、中小型企業數量的增加以及 HaaS 意識的增強預計將在預測期內推動市場發展。

- 亞太地區擁有大量位於中國大陸、台灣、韓國、印度和日本的中小企業,在預測期內將見證最高的成長率,因為 HaaS 模式是提供最佳解決方案的一種經濟有效的方式。經驗。使用資訊科技硬體。此外,該地區是硬體市場上幾家重要供應商的所在地,推動了對 HaaS 的需求。

- HaaS(硬體即服務)可實現軟硬體的及時升級和維護,幫助企業減輕IT負擔。此外,它可以避免技術過時並最終提高生產力。

- IT 和通訊業引入 HaaS(硬體即服務),可以提供經濟實惠的硬體租賃費,減少停機時間,並提供安全和軟體服務以保持設備良好維護,這有助於企業減少 IT 預算。

HaaS(硬體即服務)產業概述

目前,很少有公司提供主導 HaaS 市場的產品,全球市場預計將進行整合。 Navitas Lease Corporation、FUSE3 Communications、Ingram Micro Inc.、Design Data Systems Inc.、Phoenix NAP LLC、Machado Consulting、Managed IT Solutions、富士通有限公司、聯想Group Limited、Amazon.com Inc. 和Dell Inc. 是其中的一部分。我們研究了市場上的主要企業。 Google、IBM 和微軟等產業科技巨頭也與新興企業合作,提供這些服務,以在這個服務市場中競爭。

2022年9月,英邁國際報告稱,其數位體驗平台生態系統推出在美國和德國兩大市場如期上線,其他地區也在快速全球「運作」。我已經證實了這一點。 2023 年。參與企業看到了該技術的實際應用,並了解到 Xvantage 的初步部署目前正在整個拉丁美洲進行。

2022 年 4 月,英邁印度公司贏得了與 Digitate 的經銷協議。 Digitate 的 Ignio 支援從傳統 IT 營運向自主 IT 營運的轉變,提供更好的業務成果、更高的彈性、敏捷性和卓越的客戶服務。為了幫助端到端自主企業利用尖端的機器學習 (ML) 和人工智慧 (AI) 功能為 IT 營運提供情境智慧,英邁印度提供了整個 Digitate 產品組合 To do。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

- COVID-19 市場影響評估

- 市場促進因素

- 擴大雲端平台的採用

- 增加投資吸引力

- 市場挑戰

- 對 HaaS 模式的優勢缺乏認知

第5章市場區隔

- 按服務

- 硬體型號

- Platform-as-a-Service

- Desktop/PC-as-a-Service

- Infrastructure-as-a-Service

- Device-as-a-Service

- 專業的服務

- 硬體型號

- 按最終用戶產業

- 零售批發

- 教育

- BFSI

- 製造業

- 衛生保健

- 資訊科技/通訊

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 其他亞太地區

- 世界其他地區

- 北美洲

第6章 競爭形勢

- 公司簡介

- Navitas Lease Corporation

- FUSE3 Communications

- Ingram Micro Inc.

- Design Data Systems, Inc.

- Phoenix NAP, LLC

- Machado Consulting

- Managed IT Solutions

- Fujitsu Ltd.

- Lenovo Group Ltd.

- Dell Inc.

- Microsoft Corporation

第7章 投資分析

第8章 市場機會及未來趨勢

The Hardware-as-a-Service Market size is estimated at USD 93.65 billion in 2024, and is expected to reach USD 330.82 billion by 2029, growing at a CAGR of 28.71% during the forecast period (2024-2029).

The increasing need to adopt new IT solutions, increased digitization, increasing investment of small and large-scale enterprises in HaaS hardware and services, technical advancements and product innovation, and increasing load on cloud infrastructure are significant factors influencing the growth of the HaaS market.

Key Highlights

- The Haas model is becoming popular for companies searching for new ways to service clients in a cutthroat market to acquire technology with little strain on their financial operations. The Haas approach is more cost-effective when it comes to firms that constantly repair or upgrade their gear. This service offers inexpensive managed solutions and includes maintenance and support as part of the leasing agreement. The hardware installation at the customer's location is agreed upon between the client and managed service provider (MSP), for which the client either pays a monthly charge for the service.

- The hardware as a service (HaaS) market is anticipated to develop as cloud platform penetration increases. The solutions are highly affordable, making them appropriate for small businesses. As a result, it will aid in expanding the worldwide HaaS (hardware as a service) sector.

- On-demand services (XaaS) are replacing ownership in several industries. As data storage servers and active computing gear make up a remotely provided service for consumers, cloud computing services also draw more investment in the sector under study.

- A fundamental barrier to the adoption of the HaaS model and a constraint on its expansion is a lack of understanding of the advantages provided by the hardware-as-a-service approach. As they are unaware of the advantages like lowering the cost of updating, maintaining, and replacing hardware, businesses in developing nations like India, China, Brazil, and Indonesia are less likely to adopt this service model.

- With the outbreak of COVID-19, service firms, particularly, have embraced the work-from-home culture. This has led to a spike in demand for laptops, mainly leased ones of every kind. But, with the complete disruption of the supply chain and production activities, there is a massive mismatch between the demand and supply of hardware components and a need for more in the market. With the situation normal in the coming few quarters, HaaS is expected to grow as it mitigates the risk of a complete business shutdown during unforeseen circumstances like the Covid-19 pandemic.

Hardware as-a Service Market Trends

Retail/Wholesale Sector Holds Largest Share in the Market

- The adoption of HaaS varies from industry to industry. Among all organizations, retail/wholesale organizations are found to have adopted the HaaS model to a more significant extent, followed by Education and Financial services sector. Retail/wholesale organizations have hundreds or thousands of stores spread worldwide, making it difficult for internal IT teams to service more remote areas.

- Spiceworks surveyed more than 1,100 IT decision-makers in organizations across North America and Europe to understand the penetration of the hardware-as-service model in the workplace. The survey showed that around 31% of retail/wholesale organizations already use the HaaS model (one or more types of devices). An additional 7% of the remaining retail businesses plan to adopt HaaS within the next two years. Part replacement, hardware support, and troubleshooting are some of this model's most commonly used services.

- During the pandemic, the retail sector was one of the deemed essential businesses in many countries that were allowed to stay open when other industries had to shut their doors. Due to the growing need for numerous hardware systems among retailers, wholesalers, supermarkets, and department stores, this industry is predicted to hold a significant position.

- The retail sector has seen a lot of investments and developments recently. Retail tech companies supporting the retail industry with services such as digital ledgers, inventory management, payments solutions, and logistics and fulfillment tools enhance the need for HaaS services.

Demand from Asia-Pacific is expected to Drive the Growth

- Asia is home to some of the fastest-growing economies, such as India and China. A large IT and Telecommunication industry workforce and many enterprises are expected to boost the demand for the hardware-as-a-service model.

- Furthermore, several life sciences and retail organizations, the rising number of small and medium-sized enterprises, and the increasing awareness of HaaS are expected to drive the market over the forecast period.

- With many small or mid-sized businesses in China, Taiwan, South Korea, India, and Japan, the Asia-Pacific region is expected to experience the highest growth rate during the forecast period since the HaaS model is a cost-effective method for optimal utilization of information technology hardware. Moreover, the region enjoys the presence of several significant vendors in the hardware market, thus driving the demand for HaaS.

- Hardware-as-a-service enables timely upgrade and maintenance of hardware and software, allowing companies to reduce IT burdens; moreover, it helps avoid technological obsolescence, ultimately enhancing productivity.

- Implementing hardware-as-a-service in the IT and telecommunication industries helps companies reduce IT budgets by providing reasonable rates for renting hardware, decreasing downtime, and adequately managing devices by giving security and software services.

Hardware as-a Service Industry Overview

Few players with their product offerings currently dominate the HaaS market, and the global market is expected to be consolidated. Navitas Lease Corporation, FUSE3 Communications, Ingram Micro Inc., Design Data Systems Inc., Phoenix NAP LLC, Machado Consulting, Managed IT Solutions, Fujitsu Ltd, Lenovo Group Ltd, Amazon.com Inc., and Dell Inc. are some of the major players present in the market studied. Industry tech giants such as Google, IBM, and Microsoft also offer these services collaborating with startups to compete in this as-a-service market.

In September 2022, Ingram Micro Inc. reported that its digital experience platform ecosystem has launched on schedule in its two major markets, the United States and Germany, and it confirmed that the global "go live" schedule for the rest of the globe is early 2023. Participants saw the technology in use and learned that the Xvantage initial deployment is now taking place across Latin America.

In April 2022, Ingram Micro India won the distribution agreement with Digitate. Ignio from Digitate supports the transition from traditional IT operations to autonomous IT operations, providing better business outcomes, increased resilience, agility, and greater customer service. To assist end-to-end autonomous enterprises that leverage cutting-edge Machine Learning (ML) and Artificial Intelligence (AI) capabilities to deliver contextual intelligence to IT operations, Ingram Micro India will offer Digitate's whole portfolio.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Value Chain Analysis

- 4.5 Assessment of the impact of COVID-19 on the Market

- 4.6 Market Drivers

- 4.6.1 Growing Deployment of Cloud Platform

- 4.6.2 Increase attraction of Investments

- 4.7 Market Challenges

- 4.7.1 Lack of Awareness of benefits from HaaS Model

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Hardware Model

- 5.1.1.1 Platform-as-a-Service

- 5.1.1.2 Desktop/PC-as-a-Service

- 5.1.1.3 Infrastructure-as-a-Service

- 5.1.1.4 Device-as-a-Service

- 5.1.2 Professional Services

- 5.1.1 Hardware Model

- 5.2 By End-User Industry

- 5.2.1 Retail/Wholesale

- 5.2.2 Education

- 5.2.3 BFSI

- 5.2.4 Manufacturing

- 5.2.5 Healthcare

- 5.2.6 IT and Telecommunication

- 5.2.7 Other End-User Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia Pacific

- 5.3.4 Rest of the World

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Navitas Lease Corporation

- 6.1.2 FUSE3 Communications

- 6.1.3 Ingram Micro Inc.

- 6.1.4 Design Data Systems, Inc.

- 6.1.5 Phoenix NAP, LLC

- 6.1.6 Machado Consulting

- 6.1.7 Managed IT Solutions

- 6.1.8 Fujitsu Ltd.

- 6.1.9 Lenovo Group Ltd.

- 6.1.10 Dell Inc.

- 6.1.11 Microsoft Corporation

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

硬體即服務市場:按硬體型號、公司規模、部署模型和最終用戶分類 - 2024-2030 年全球預測

硬體即服務市場:按硬體型號、公司規模、部署模型和最終用戶分類 - 2024-2030 年全球預測 2024-2032 年基礎設施即服務市場報告(按部署類型、解決方案、最終用戶、垂直行業和區域)

2024-2032 年基礎設施即服務市場報告(按部署類型、解決方案、最終用戶、垂直行業和區域) 2024 年 IaaS(基礎設施即服務)全球市場報告

2024 年 IaaS(基礎設施即服務)全球市場報告 基礎架構即服務(IaaS) 市場:按解決方案、部署類型、最終用戶分類 - 2024-2030 年全球預測

基礎架構即服務(IaaS) 市場:按解決方案、部署類型、最終用戶分類 - 2024-2030 年全球預測 一體化基礎設施市場:按行業、按技術組件、按部署模型、按組織規模、按地區

一體化基礎設施市場:按行業、按技術組件、按部署模型、按組織規模、按地區 IaaS(基礎設施即服務)市場報告:2030 年趨勢、預測與競爭分析

IaaS(基礎設施即服務)市場報告:2030 年趨勢、預測與競爭分析 基礎設施即服務市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件類型、部署模型、企業規模、垂直行業、地區、競爭進行細分。

基礎設施即服務市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件類型、部署模型、企業規模、垂直行業、地區、競爭進行細分。 Infrastructure-as-a-Service市場:按產品、按部署、按組織規模、按應用程式、按地區-2030年之前的世界預測

Infrastructure-as-a-Service市場:按產品、按部署、按組織規模、按應用程式、按地區-2030年之前的世界預測 基礎設施即服務和平台即服務的全球市場

基礎設施即服務和平台即服務的全球市場 IaaS(基礎設施即服務)市場規模/份額分析 - 增長趨勢和預測(2023-2028)

IaaS(基礎設施即服務)市場規模/份額分析 - 增長趨勢和預測(2023-2028)