|

市場調查報告書

商品編碼

1432927

油田服務 (OFS) -市場佔有率分析、行業趨勢和統計數據、成長預測(2024-2029)Oilfield Services (OFS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

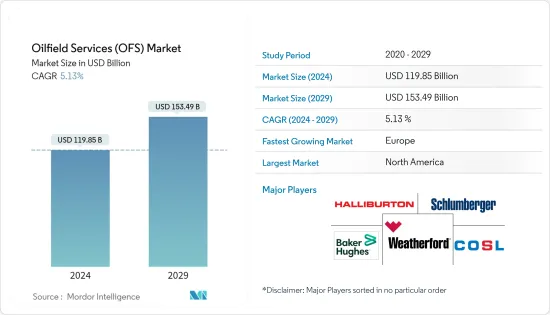

油田服務市場規模預計到2024年為1,198.5億美元,預計到2029年將達到1,534.9億美元,在預測期內(2024-2029年)複合年成長率為5.13%。

主要亮點

- 從中期來看,天然氣蘊藏量的開拓以及先進技術、工具和設備等因素預計將在預測期內推動油田服務市場的發展。

- 另一方面,近期受供需缺口、地緣政治等因素影響,油價大幅波動,限制油田服務市場需求成長。

- 也就是說,對最佳化碳氫化合物生產成本的新技術和製程的關注預計將在預測期內為油田服務(OFS)市場創造一些機會。

- 由於頁岩油田的大量鑽探和生產活動,預計北美將成為預測期內最大的市場。預計北美將在預測期內主導市場。

油田服務 (OFS) 市場趨勢

鑽井服務預計將主導市場

- 預計全球經濟將支持石油需求的大幅成長。強勁的經濟體預計將消耗更多的石油,並且需求預計將在未來幾年顯著成長。預計到 2023 年,印度和中國將佔全球石油需求的 50% 左右。

- 根據石油輸出國組織(OPEC)統計,2022年全球原油需求約9,957萬桶/日,高於2021年的9,708萬桶/日。原油需求的成長將增加全球鑽井服務的需求。

- 因此,石油和天然氣公司面臨越來越大的壓力,需要增加產量以滿足不斷成長的能源需求。因此,隨著傳統型油田開始顯示出成熟的跡象,一些營運公司正在將重點轉向開發傳統型蘊藏量。

- 例如,2022年2月,阿布達比國家石油公司(ADNOC)與四家油田服務供應商簽署了價值19.4億美元的框架協議,以擴大鑽探規模。該協議建立在ADNOC最近對鑽井相關設備和服務的投資基礎上,旨在2030年將原油產能提高到500萬桶/日(mmbpd)。

- 此外,新的海上鑽井承包服務預計將推動油田服務市場。例如,2022年5月,Equinor與三大油田服務公司(Baker Hughes Norge、Halliburton和Schlumberger)簽署了挪威大陸棚(NCS)綜合鑽井和油井服務合約。合約期限自2022年6月1日起兩年。合約總價值約18億美元。

- 鑽井和測井工具的技術進步預計也將促進預測期內的鑽井服務。例如,2022年11月,國家能源服務聯合公司(NESR)宣布,該公司獲得了科威特定向鑽井服務的長期合約。合約範圍包括五年的定向鑽井、隨鑽測量、性能鑽井、油井工程和隨鑽測井(LWD)服務,並可選擇額外延長一年。

- 因此,鑑於上述幾點,預計鑽井服務將在預測期內主導油田服務(OFS)市場。

預計北美將主導市場

- 由於美國、加拿大和墨西哥等國家的存在,北美在世界原油產量中所佔的佔有率很高。美國平均原油產量約為每天1,190萬桶,該地區原油產量大幅增加。與2021年相比,該國原油產量增加5.6%。

- 在北美,由於效率的提高和供應鏈的加強,石油和天然氣計劃變得更具競爭力,從而降低了鑽井成本並提高了計劃的可行性。

- 美國是該地區最大的油田服務市場之一,這主要是由於頁岩蘊藏量中鑽探和水力碾碎的油井數量不斷增加以及儲量緊張。這主要是由於頁岩地層和蘊藏量緊張的鑽井和水力碾碎井數量不斷增加。頁岩地層、水平鑽井和水力壓裂的最新發展顯著增加了該地區油田服務的需求。

- 同樣,加拿大擁有僅次於委內瑞拉和沙烏地阿拉伯的世界第三大石油蘊藏量,其中96%是油砂蘊藏量。加拿大可開採的原油密度大,含有許多沙粒。因此,將石油從井底輸送到地面需要高壓和油井干預,從而增加了該國對油田服務的需求。

- 因此,鑑於上述幾點,預計北美在預測期內將主導油田服務(OFS)市場。

油田服務 (OFS) 產業概覽

油田服務市場分散。該市場的主要企業包括(排名不分先後)斯倫貝謝有限公司、貝克休斯公司、哈里伯頓公司、威德福國際公司和中海油田服務有限公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2028年之前的市場規模與需求預測(單位:美元)

- 2028 年石油和天然氣產量及預測

- 到 2022 年運作的陸上和海上鑽井平台數量

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 增加天然氣蘊藏量和開發先進技術、工具和設備

- 全球油田服務投資增加

- 抑制因素

- 近期原油價格因供需缺口而波動

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

第5章市場區隔

- 服務類型

- 鑽井服務

- 竣工服務

- 生產/干預服務

- 其他服務

- 地點

- 陸上

- 離岸

- 區域市場分析:2028年之前的市場規模與需求預測(按區域)

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Schlumberger Limited

- Weatherford International plc

- Baker Hughes Company

- Halliburton Company

- Transocean Ltd.

- Valaris PLC

- China Oilfield Services Limited

- Nabors Industries, Inc.

- Basic Energy Services Inc.

- OiLSERV

- Expro Group

第7章 市場機會及未來趨勢

- 越來越關注最佳化碳氫化合物生產成本的新技術和方法

簡介目錄

Product Code: 55022

The Oilfield Services Market size is estimated at USD 119.85 billion in 2024, and is expected to reach USD 153.49 billion by 2029, growing at a CAGR of 5.13% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as the increasing development of gas reserves and advanced technology, tools, and equipment are expected to drive the oilfield services market during the forecast period.

- On the other hand, the volatile oil prices over the recent period, owing to the supply-demand gap, geopolitics, and several other factors, have been restraining the growth in the demand for the oilfield services market.

- Nevertheless, the focus on new technologies and methods to optimize the production cost of hydrocarbons is expected to create several opportunities for the oilfield services (OFS) market during the forecast period.

- North America is expected to be the largest market during the forecast period, owing to high drilling and production activity in shale fields. It is expected to dominate the market during the forecast period.

Oilfield Services (OFS) Market Trends

Drilling Services Expected to Dominate the Market

- The global economy is expected to underpin a substantial increase in oil demand. Strong economies are anticipated to consume more oil, and the demand is expected to grow significantly over the years. India and China are expected to contribute around 50% of the global oil demand by 2023.

- According to Organization of the Petroleum Exporting Countries (OPEC) statistics, in 2022, the worldwide crude oil demand was around 99.57 million barrels per day, increasing from 97.08 million barrels in 2021. The rising demand for crude oil increases the demand for drilling services worldwide.

- Hence, there is increasing pressure among the top oil and gas operating companies to increase their production and meet the increasing energy demand. As a result, several operating companies have shifted their focus toward exploiting unconventional reserves, as the conventional fields have started showing signs of maturity.

- For instance, in February 2022, Abu Dhabi National Oil Company (ADNOC) awarded framework agreements to four oilfield services providers valued at USD 1.94 billion to enable drilling growth. The awards aim at ADNOC's recent investments in drilling-related equipment and services to boost crude oil production capacity to 5 million barrels per day (mmbpd) by 2030.

- Further, new offshore contract drilling services are expected to drive the oilfield services market. For instance, in May 2022, Equinor had contracts with three oilfield services giants - Baker Hughes Norge, Halliburton, and Schlumberger for integrated drilling and well services on the Norwegian continental shelf (NCS). The contract is for two years, starting from 1st June 2022. The total value of the contract is about USD 1.8 billion.

- Technological advancements in drilling and logging tools are also expected to drive drilling services during the forecast period. For instance, In November 2022, National Energy Services Reunited Corporation (NESR) announced that the company had been awarded a long-term contract for directional drilling services in Kuwait. The contract scope includes directional drilling, measurements while drilling, performance drilling, well engineering, and logging while drilling (LWD) services for five years with an option to extend an additional year.

- Therefore, owing to the above points, drilling services are expected to dominate the oilfield services (OFS) market during the forecast period.

North America Expected to Dominate the Market

- The share of North America in global crude oil production is high owing to the presence of countries such as the United States, Canada, and Mexico. The crude oil production in the region is increasing significantly, as United States's average crude oil production was around 11.9 million barrels per day. The crude oil production for the country grew from 5.6% compared to the year 2021.

- In North America, oil and gas projects are becoming more competitive, owing to improving efficiencies and tightening of the supply chain, which has led to declining drilling costs and has, in turn, made many projects viable.

- The United States in the region is to be one of the largest markets for oilfield services, mainly due to the increasing number of wells being drilled and fracked in the shale and tight reserves. The low breakeven price of the basins supports this. The recent development of shale plays, horizontal drilling, and fracking has resulted in a massive increase in demand for oilfield services in the region.

- Similarly, Canada has the world's third-largest crude oil reserves, after Venezuela and Saudi Arabia, of which 96% are oil sand reserves. The oil available in the country is of high density and has high sand particle content. Due to this, oil transport from the bottom hole of the oil well to the surface requires high pressure and wellbore intervention, thus increasing the demand for oilfield services in the country.

- Therefore, owing to the above points, North America is expected to dominate the oilfield services (OFS) market during the forecast period.

Oilfield Services (OFS) Industry Overview

The oilfield services market is fragmented. Some of the major players in the market (in no particular order) include Schlumberger Limited, Baker Hughes Company, Halliburton Company, Weatherford International Plc, and China Oilfield Services Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Crude Oil and Natural Gas Production and Forecast, till 2028

- 4.4 Onshore and Offshore Active Rig Count, till 2022

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Increasing Development of Gas Reserves and Advanced Technology, Tools, and Equipment

- 4.7.1.2 Increasing Investment in the Oilfield Services across World

- 4.7.2 Restraints

- 4.7.2.1 The Volatile Oil Prices Over the Recent Period, Owing to the Supply-Demand Gap

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes Products and Services

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Service Type

- 5.1.1 Drilling Services

- 5.1.2 Completion Services

- 5.1.3 Production and Intervention Services

- 5.1.4 Other Services

- 5.2 Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Schlumberger Limited

- 6.3.2 Weatherford International plc

- 6.3.3 Baker Hughes Company

- 6.3.4 Halliburton Company

- 6.3.5 Transocean Ltd.

- 6.3.6 Valaris PLC

- 6.3.7 China Oilfield Services Limited

- 6.3.8 Nabors Industries, Inc.

- 6.3.9 Basic Energy Services Inc.

- 6.3.10 OiLSERV

- 6.3.11 Expro Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Focus on New Technologies and Methods to Optimize its Production Cost of Hydrocarbons