|

市場調查報告書

商品編碼

1431673

複合纖維:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Bicomponent Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

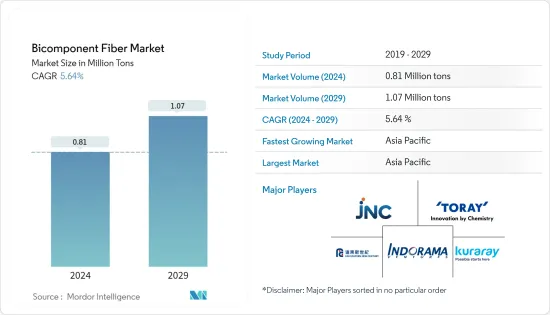

預計2024年複合纖維市場規模為81萬噸,預計2029年將達到107萬噸,預測期(2024-2029年)複合年成長率為5.64%。

COVID-19 大流行迫使汽車製造商、衛生、醫療和不織布紡織產品製造商在全球範圍內暫停營運,從而減少了 2022 年複合纖維的需求。這次疫情幾乎影響了這些產業的方面,從產品需求到勞動力發展,再到疫情爆發時已經出現的加速或放緩趨勢。由於客戶及其臨時停產,生產水準下降,需求的減少對生產過程產生了重大影響。然而,預計情況將在預測期下半年恢復並恢復所研究市場的成長軌跡。

主要亮點

- 從長遠來看,衛生行業擴大採用複合纖維以及不織布行業不斷成長的需求預計將推動市場需求。

- 消費者意識的缺乏和高生產成本預計將阻礙市場成長。

- 然而,再生複合纖維的未來應用預計將為市場提供利潤豐厚的機會。

- 亞太地區佔據了最高的市場佔有率,該地區很可能在預測期內主導市場。

複合纖維市場趨勢

環衛產業主導市場

- 複合纖維用於生產不織布,具有獨特的物理和美觀特性,這對於一次性尿布和衛生產品至關重要。

- 這些纖維還具有清潔、可回收、黏合劑分佈均勻等多功能特性。這些纖維不織布是嬰兒訓練褲、嬰兒尿布、女性護理用品、成人失禁用品、醫用墊片、創傷護理和吸水繃帶等產品的首選材料。

- 此外,由於嬰幼兒衛生意識不斷增強,強烈鼓勵父母使用嬰兒尿布和嬰兒濕紙巾。尿布是嬰幼兒日常護理必備的產品之一,嬰兒擦拭巾有助於預防細菌感染並提供舒適感。

- 根據Parenting Mode預測,到2022年,全球一次性尿布市場每年價值約710億美元。嬰兒在出生後的頭兩年會使用約 6,000 個一次性尿布。此外,金佰利的個人護理品牌(包括嬰兒衛生用品)在 2022 年的收益為 10,620 美元,而 2021 年為 10,270 美元。

- 2023 年 4 月,Millie Moon 嬰兒紙尿褲宣佈在加拿大上市。 Millie Moon 是一個乾淨、高品質的一次性尿布品牌,以實惠的價格為敏感肌膚提供高性能、製作精美的一次性尿布和濕紙巾。該公司還表示,其豪華尿布的材質對嬰兒的皮膚非常柔軟,並採用 CloudTouch 柔軟度設計,以提供最佳的舒適度。

- 2022 年 3 月,作為奈及利亞擴張計劃的一部分,金佰利將在拉各斯 Ikorodu 開設一家新製造工廠,生產 Huggies 嬰兒尿布和 Cortex女性護理用品。我們耗資 1 億美元的最先進製造工廠配備了最新技術,以便更好地為我們的客戶服務。

- 據 EDANA 稱,到 2022 年,衛生和個人護理擦拭巾將佔歐洲所有不織布用量的 45% 以上。

- 因此,考慮到全球衛浴產品和各種計劃的成長趨勢,衛浴產業很可能佔據市場主導地位,預計將在預測期內增加對複合纖維的需求。

亞太地區主導市場

- 亞太地區在 2022 年以巨大的銷售和收益佔有率主導複合纖維市場,預計在預測期內將保持其主導地位。

- 在全球紡織服飾市場領域,中國在過去二十年一直是主要參與者。自加入世界貿易組織(WTO)以來,中國的紡織品和服飾製造和銷售大幅成長,主要得益於西方業務的增加。

- 根據中國不織布工業紡織品協會統計,2022年中國不織布產量與前一年同期比較814萬噸。此外,中國仍然是運動服裝、配件和鞋類的一個有吸引力的市場。

- 中國汽車產量的增加可能會增加汽車紡織品的消費,預計將進一步支撐所研究市場的需求。根據中國工業協會統計,2022年中國汽車產量2,702.1萬輛,與前一年同期比較成長3.4%。 2022年汽車產量中,小客車2,383.6萬輛,商用車產量318.5萬輛。

- 複合纖維在建設產業中用於隔熱材料材料和地板材料。建築業是中國經濟持續發展的關鍵。中國正在經歷一場建築業的大繁榮。根據中國國家統計局的數據,2022 年建築業產值將達到31.2 兆元(4.5 兆美元),高於2021 年的29.3 兆元(4.2 兆美元),預計建築支出將接近13兆美元到目前為止,接受調查的市場前景樂觀。

- 幾家印度一次性尿布製造商正專注於產品創新和擴張,這可能會進一步提振對複合纖維的需求。例如,2023年1月,金佰利宣布重新推出其標誌性紙尿褲品牌Huggies,在印度推出全新Huggies Complete Comfort系列。

- 2023 年,Reliance Retail 的 Performax Activewear 成為印度足球隊的官方套件贊助商。這個本土運動服飾品牌擁有為所有足球比賽製造套件的獨家權利。它也將成為 AIFF(全印度足球聯合會)(包括男子、女子和青年隊)所有比賽、巡迴賽和訓練服裝的唯一供應商。此外,作為產品贊助商,Performax也將持有這些產品的製造和零售權。

- 因此,上述原因可能會推動預測期內亞太地區複合纖維市場的成長。

複合纖維產業概況

複合纖維市場部分分散,有多家公司在全球和區域層面運作。市場主要企業(排名不分先後)包括 Indorama Ventures Public Company Limited、Far Eastern New Century Corporation、JNC Corporation、KURARAY、TORAY INDUSTRIES, INC.

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 擴大複合纖維在衛生產業的應用

- 不織布產業需求增加

- 抑制因素

- 消費者意識缺乏,生產成本高

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 按材質

- 聚乙烯 (PE)/聚丙烯 (PP)

- 聚丙烯 (PP)/聚對苯二甲酸乙二酯(PET)

- 高密度聚苯乙烯/低密度聚乙烯

- 聚乙烯/聚對苯二甲酸乙二酯(PET)

- 聚酯/PBT

- 其他材料

- 依結構類型分

- 護套芯型

- 並排型

- 海島型

- 其他

- 按最終用戶產業

- 不織布

- 車

- 衛浴業

- 建造

- 醫療保健

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- CHA Technologies Group

- EMS-chemie Holding AG

- Far Eastern New Century Corporation

- Freudenberg Performance Materials

- Huvis Corp.

- Indorama Ventures Public Company Limited

- JNC Corporation

- Kolon Glotech

- Kuraray Co. Ltd.

- OC Oerlikon Management AG

- PTT Global Chemical Public Company Limited

- Shaoxing Yaolong Spunbonded Nonwoven Technology Co. Ltd

- TEIJIN Limited

- TORAY Industries Inc.

- WPT Nonwovens Corp.

第7章 市場機會及未來趨勢

- 再生複合纖維的未來應用

The Bicomponent Fiber Market size is estimated at 0.81 Million tons in 2024, and is expected to reach 1.07 Million tons by 2029, growing at a CAGR of 5.64% during the forecast period (2024-2029).

The COVID-19 pandemic, on a global scale, forced automakers, hygiene, medical, and non-woven textile products manufacturers to shut down their operations, lowering the demand for bicomponent fiber in 2022. The pandemic impacted almost every aspect of these industries, from product demand to workforce development to accelerating or decelerating trends already underway when it struck. Customers and their temporary production stops reduced production levels, and demand reductions significantly impacted production processes. However, the condition is expected to recover, restoring the growth trajectory of the market studied during the latter half of the forecast period.

Key Highlights

- In the long term, the growing adoption of bicomponent fiber in the hygiene industry and rising demand from the non-woven textile industry are expected to drive market demand.

- Lack of consumer awareness and high production cost is expected to hinder the market's growth.

- Nevertheless, future applications of recycled bicomponent fibers is expected to offer lucrative opportunities to the market.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Bicomponent Fiber Market Trends

Hygiene Industry to Dominate the Market

- Bicomponent fibers are utilized to produce nonwoven fabrics with a soft touch, along with other unique physical and aesthetic properties, which are deemed essential for diapers and hygiene products.

- These fibers are also used due to their versatile properties of being clean, recyclable, and have a uniform distribution of adhesive. These fiber nonwovens are the material of choice for products such as toddler training pants, infant diapers, feminine care products, adult incontinence products, medical underpads, wound care, and absorbent bandages, among others.

- Furthermore, owing to the increasing awareness about infant hygiene, parents are strongly adopting the usage of baby diapers and baby wipes. Diapers are among the essential infant daily care products, and baby wipes help prevent bacterial infection and provide comfort.

- According to the Parenting Mode company, the global disposable diaper market accounted for approximately USD 71 billion/year by 2022. Babies use about 6,000 diapers during their first two years of life. In addition, the personal care brands of Kimberly Clark, which include baby hygiene products, generated a revenue of USD 10.62 thousand in 2022 as compared to USD 10.27 Thousand in 2021.

- In April 2023, Millie Moon baby diapers announced their launch in Canada. Millie Moon claims to be a clean, luxury diaper brand offering high-performance and beautifully crafted diapers and sensitive wipes at affordable prices. The company also claims that the materials in its Luxury Diapers are extremely soft on babies' skin and engineered with CloudTouch Softness for optimum comfort.

- In March 2022, as part of its expansion plans in Nigeria, Kimberly-Clark opened a new manufacturing facility in Ikorodu, Lagos, which will manufacture Huggies baby diapers as well as Kotex feminine care products. With the investment of USD 100 million in its new state-of-the-art manufacturing facility, the company is equipped with the latest technology to serve its customers better.

- According to EDANA, in 2022, hygiene and personal care wipes accounted for more than 45% of all nonwoven use across Europe.

- Therefore, considering the growth trends and various projects of hygiene products in different regions worldwide, the hygiene industry is likely to dominate the market, which, in turn, is expected to enhance the demand for bicomponent fiber during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominated the bicomponent fiber market in 2022, with a considerable volume and revenue share, and is expected to maintain its dominance during the forecast period.

- In the global textile and clothing market segment, China has always been a major player for the last two decades. Since becoming a member of the World Trade Organization, China's textile and clothing manufacturing and sales have increased dramatically, largely due to increased business from the West.

- According to the China Nonwovens and Industrial Textiles Association, the output of nonwovens in China was 8.14 million tons Y-o-Y in 2022. In addition, China continues to be an attractive market for selling athletic apparel, accessories, and footwear.

- The rising production of automobiles in China is likely to enhance the consumption of automotive textiles, which is expected to further support the demand for the studied market. According to the China Association of Automobile Manufacturers (CAAM), China produced 27,021 thousand units of automobiles in 2022, registering a growth rate of 3.4% compared to the previous year. Out of the automobile production in 2022, passenger cars accounted for 23,836 thousand units, whereas commercial car production accounted for 3,185 thousand units.

- Bicomponent fiber is used for insulation and flooring underlayment in the construction industry. The construction sector is key to China's continued economic development. China is amid a construction mega-boom. According to the National Bureau of Statistics of China, The value of construction output accounted for 31.2 trillion yuan (USD 4.5 trillion) in 2022, up from 29.3 trillion yuan (USD 4.2 trillion) in 2021, China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for the studied market.

- Several diaper manufacturing companies in India are focusing on product innovation and expansion, which is further likely to drive the demand for bicomponent fibers. For instance, in January 2023, Kimberly-Clark announced the relaunch of its iconic diaper brand, Huggies, with the new 'Huggies Complete Comfort' range in India.

- In 2023, Reliance Retail's Performax activewear became the official kit sponsor for the Indian football team. The homegrown sportswear brand will have the exclusive rights to manufacture kits across all formats of the game. The firm will also be the sole supplier for all matches, travel, and training wear for the AIFF (All India Football Federation), including men's, women's, and youth teams. In addition to this, as the merchandise sponsor, Performax is also expected to hold the rights to manufacture and retail these products.

- Hence, the reasons mentioned above are likely to fuel the growth of the bicomponent fiber market in Asia-Pacific over the forecast period.

Bicomponent Fiber Industry Overview

The bicomponent fiber market is partially fragmented, with several companies operating on both global and regional levels. Some of the major players in the market (Not in any particular order) include Indorama Ventures Public Company Limited, Far Eastern New Century Corporation, JNC Corporation, KURARAY CO., LTD., and TORAY INDUSTRIES, INC., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Adoption of Bicomponent Fiber In the Hygiene Industry

- 4.1.2 Rising Demand From the Non-woven Textile Industry

- 4.2 Restraints

- 4.2.1 Lack of Consumer Awareness and High Production Cost

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume and Revenue)

- 5.1 Material

- 5.1.1 Polyethylene (PE)/Polypropylene (PP)

- 5.1.2 Polypropylene (PP)/polyethylene Terephthalate (PET)

- 5.1.3 High-density Polyethylene/Low-density Polyethylene

- 5.1.4 Polyethylene/polyethylene Terephthalate (pet)

- 5.1.5 Polyester/PBT

- 5.1.6 Other Materials

- 5.2 Structure Types

- 5.2.1 Sheath-core

- 5.2.2 Side-by-Side

- 5.2.3 Islands in the Sea

- 5.2.4 Other Structure Types

- 5.3 End-user Industry

- 5.3.1 Non-Woven Textiles

- 5.3.2 Automotive

- 5.3.3 Hygiene

- 5.3.4 Construction

- 5.3.5 Medical

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 CHA Technologies Group

- 6.4.2 EMS-chemie Holding AG

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 Freudenberg Performance Materials

- 6.4.5 Huvis Corp.

- 6.4.6 Indorama Ventures Public Company Limited

- 6.4.7 JNC Corporation

- 6.4.8 Kolon Glotech

- 6.4.9 Kuraray Co. Ltd.

- 6.4.10 OC Oerlikon Management AG

- 6.4.11 PTT Global Chemical Public Company Limited

- 6.4.12 Shaoxing Yaolong Spunbonded Nonwoven Technology Co. Ltd

- 6.4.13 TEIJIN Limited

- 6.4.14 TORAY Industries Inc.

- 6.4.15 WPT Nonwovens Corp.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Applications of Recycled Bicomponent Fibers

2024-2032 年連續纖維複合材料市場(按樹脂類型、產品類型、增強類型、垂直產業和地區分類)

2024-2032 年連續纖維複合材料市場(按樹脂類型、產品類型、增強類型、垂直產業和地區分類) CFRTP 市場:依樹脂類型、產品類型、應用分類 - 2024-2030 年全球預測

CFRTP 市場:依樹脂類型、產品類型、應用分類 - 2024-2030 年全球預測 天然纖維增強複合材料:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測

天然纖維增強複合材料:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測 全球碳纖維增強熱塑性複合材料 (CFRTP) 市場 - 2023-2030

全球碳纖維增強熱塑性複合材料 (CFRTP) 市場 - 2023-2030 纖維增強複合材料市場(產品:短纖維增強複合材料和長纖維/連續增強複合材料;類型:玻璃、碳、芳綸等)-2023 年全球行業分析、規模、佔有率、成長、趨勢和預測-2031

纖維增強複合材料市場(產品:短纖維增強複合材料和長纖維/連續增強複合材料;類型:玻璃、碳、芳綸等)-2023 年全球行業分析、規模、佔有率、成長、趨勢和預測-2031 CFRTP 的全球市場:依產品類型、樹脂類型、應用、地區 - 預測(截至 2028 年)

CFRTP 的全球市場:依產品類型、樹脂類型、應用、地區 - 預測(截至 2028 年) 天然纖維增強複合材料市場:按纖維類型、按聚合物、按最終用戶行業、按地區 - 規模、份額、展望、機會分析,2023-2030 年

天然纖維增強複合材料市場:按纖維類型、按聚合物、按最終用戶行業、按地區 - 規模、份額、展望、機會分析,2023-2030 年 纖維強化複合材料的全球市場

纖維強化複合材料的全球市場 纖維增強複合材料市場:依纖維類型、基體類型、用途- 2023-2030 年全球預測

纖維增強複合材料市場:依纖維類型、基體類型、用途- 2023-2030 年全球預測 連續纖維複合材料市場:按樹脂類型、產品類型、增強類型、行業、地區劃分,2023-2028 年

連續纖維複合材料市場:按樹脂類型、產品類型、增強類型、行業、地區劃分,2023-2028 年