|

市場調查報告書

商品編碼

1431659

衛星零件:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Satellite Parts and Components - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

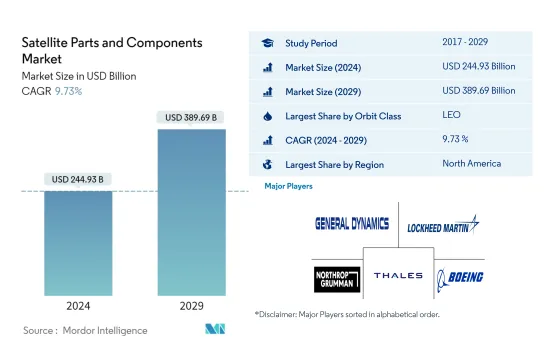

衛星零件市場規模預計2024年為2,449.3億美元,預計2029年將達到3,896.9億美元,在預測期內(2024-2029年)複合年成長率為9.73%成長。

新衛星製造技術的採用有望開啟新的商機

- 近年來,全球衛星零件產業經歷了多種趨勢。隨著技術的進步,小型衛星的性能和成本效率不斷提高,使其成為各種應用的有吸引力的選擇。衛星小型化的趨勢導致對推進系統、電力系統和天線等小型衛星零件的需求增加。

- 積層製造(3D 列印)由於能夠製造複雜零件並降低製造成本,在衛星產業中越來越受歡迎。該技術用於製造衛星零件,如天線、支架和引擎零件。美國太空總署和歐洲太空總署等主要航太機構都在強調這一點。作為全球太空產業的主要企業之一,美國是衛星通訊、遙感和太空探勘先進技術開發的潮流引領者。這些創新包括高性能電子設備、先進感測器、輕質材料、推進系統等。另一個趨勢是在衛星設計和開發中擴大使用商用現成 (COTS) 現有組件和子系統。 COTS 組件可以顯著減少開發時間和成本,同時提高可靠性和效能。

- 2017年至2022年5月,全球製造並發射了4,300多顆衛星。總的來說,這些趨勢正在塑造全球衛星零件產業的未來,各公司在推動該領域創新的同時,也應對不斷變化的市場需求。預計2023年至2029年全球衛星零件市場將成長40%。

全球衛星零件市場趨勢

衛星小型化的重要性日益增加預計將影響衛星質量

- 最近,衛星變得越來越小,小型衛星幾乎可以做傳統衛星能做的所有事情,而成本只是傳統衛星的一小部分,使得建造、發射和運行小型衛星星系變得更加容易,變得更加來越現實。相應地,人們對小型衛星的信心也急劇增加。小型衛星通常具有較短的開發週期、較小的開發團隊和較低的發射成本。

- 超過1000公斤的大型衛星大致上依品質分類。在 2017 年至 2022 年間發射的大型衛星中,約 44 顆由北美組織擁有。中型衛星的質量為500至1000公斤。全球整體已發射了320多顆衛星。衛星依質量分類。質量小於500公斤的衛星稱為小衛星,全球已發射小衛星3800多顆。

- 由於小型衛星的開發時間短且整體任務成本較低,該地區的小型衛星呈現成長趨勢。小衛星的出現使得科技成果的取得時間大大縮短。小型衛星任務的靈活性使其能夠輕鬆應對新的技術機會和需求。美國小型衛星產業得到了針對特定應用設計和製造小型衛星的強大框架的支持。由於商業和軍事航太領域的需求增加,預計2023年至2029年北美地區對衛星零件的需求將大幅成長。

預計各航太機構支出的增加將對衛星產業產生正面影響。

- 衛星技術擴大應用於通訊、導航和地球觀測等各種應用,這就產生了對新型創新衛星組件的需求。公司投資研發來開發滿足這些應用的特定要求的零件。人工智慧、機器學習、積層製造和先進材料的使用等技術進步正在推動衛星零件產業的研發投資需求。這些進步為創新組件的開發創造了新的機會。

- 2022年11月,歐洲太空總署(ESA)宣布將在未來三年內投資25%的太空資金,旨在維持歐洲在地球觀測領域的領先地位,擴大導航服務,並繼續與美國保持探勘合作關係。他們美國提案將金額增加 %。歐洲太空總署 (ESA) 要求 22 個國家為 2023-2025 年提供約 185 億歐元的預算支援。同樣,2022 年 9 月,法國宣布預計將增加國家和歐洲太空計畫的支出。

- 在北美,全球政府在太空項目上的支出在 2021 年達到約 1,030 億美元的歷史新高。該地區是太空創新和研究的中心,也是世界上最大的航太機構美國太空總署的所在地。 2022年,美國政府將在太空計畫上花費約620億美元,成為全球太空支出最高的國家。在美國,聯邦機構每年接受政府資助,其中323.3億美元用於其子公司。該地區的空間和研究津貼預計將激增,從而提高該行業在全球經濟所有領域的重要性。

衛星零件行業概況

衛星零件市場集中度較高,前五家企業佔比達90.12%。該市場的主要企業是(按字母順序排列)通用動力公司、洛克希德馬丁公司、諾斯羅普格魯曼公司、泰雷茲公司和波音公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章執行摘要和主要發現

第2章 檢舉要約

第3章簡介

- 研究假設和市場定義

- 調查範圍

- 調查方法

第4章 產業主要趨勢

- 衛星小型化

- 衛星質量

- 太空探索支出

- 法律規範

- 世界

- 澳洲

- 巴西

- 加拿大

- 中國

- 法國

- 德國

- 印度

- 伊朗

- 日本

- 紐西蘭

- 俄羅斯

- 新加坡

- 韓國

- 阿拉伯聯合大公國

- 英國

- 美國

- 價值鍊和通路分析

第5章市場區隔

- 地區

- 亞太地區

- 歐洲

- 北美洲

- 世界其他地區

第6章 競爭形勢

- 主要策略趨勢

- 市場佔有率分析

- 公司形勢

- 公司簡介

- AAC Clyde Space

- BAE Systems

- General Dynamics

- Innovative Solutions in Space BV

- Jena-Optronik

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- OHB SE

- SENER Group

- Sitael SpA

- Thales

- The Boeing Company

第7章 CEO 面臨的關鍵策略問題

第8章附錄

簡介目錄

Product Code: 50001258

The Satellite Parts and Components Market size is estimated at USD 244.93 billion in 2024, and is expected to reach USD 389.69 billion by 2029, growing at a CAGR of 9.73% during the forecast period (2024-2029).

The adaptation of new satellite manufacturing techniques is expected to open new scope of opportunities

- The global satellite parts and components industry has been experiencing several trends in recent years. With the advancements in technology, small satellites have become more capable and cost-effective, making them an attractive option for various applications. The trend of satellite miniaturization resulted in an increasing demand for small satellite components, such as propulsion systems, power systems, and antennas.

- Additive manufacturing, or 3D printing, has been gaining popularity in the satellite industry due to its ability to produce complex parts and reduce manufacturing costs. This technology is being used to produce satellite components such as antennas, brackets, and engine parts. The major space agencies such as NASA and the European Space Agency have emphasized that. One of the major players in the global space industry, the United States, is a trendsetter in the development of advanced technologies for satellite communications, remote sensing, and space exploration. These innovative technologies include high-performance electronics, advanced sensors, lightweight materials, and propulsion systems. Another trend is the increasing use of pre-existing components and subsystems commercial-off-the-shelf (COTS) in satellite design and development. COTS components can significantly reduce development time and costs while improving reliability and performance.

- Between 2017 and May 2022, around 4300+ satellites were manufactured and launched globally. Overall, these trends are shaping the future of the global satellite parts and components industry as companies work to meet the demands of an ever-changing market while also driving innovation in the field. The global satellite parts and components market is expected to grow by 40% between 2023 and 2029.

Global Satellite Parts and Components Market Trends

The increased importance of satellite miniaturization is expected to affect the satellite mass

- Satellites are getting smaller nowadays, and a small satellite can do almost everything that a conventional satellite can at a fraction of the cost of the conventional satellite, which has made the building, launching, and operation of small satellite constellations increasingly viable. Correspondingly, reliance on them has been growing exponentially. Small satellites typically have shorter development cycles, smaller development teams, and cost much less for launch.

- The major classification types according to mass are large satellites that are more than 1,000 kg. During 2017-2022, around 44 large satellites launched were owned by North American organizations. A medium-sized satellite has a mass between 500 and 1000 kg. Globally, organizations operated more than 320 satellites launched. Satellites are classified according to mass. Satellites with a mass of less than 500 kg are considered small satellites, and around 3800+ small satellites were launched globally.

- There is a growing trend toward small satellites in the region because of their shorter development time, which can reduce overall mission costs. They have made it possible to significantly reduce the time required to obtain scientific and technological results. Small spacecraft missions tend to be flexible and can, therefore, be more responsive to new technological opportunities or needs. The small satellite industry in the United States is supported by a robust framework for designing and manufacturing small satellites tailored to serve specific application profiles. The demand for satellite parts and components in the North American region is expected to surge during 2023-2029 due to increasing demand in the commercial and military space sector.

The increasing expenditures of different space agencies is expected to positively impact the satellite industry

- The increasing use of satellite technology in various applications, including communication, navigation, and earth observation, has created a need for new and innovative satellite components. Companies are investing in R&D to develop components that meet the specific requirements of these applications. Technological advancements, such as the use of AI and machine learning, additive manufacturing, and advanced materials, are driving the need for R&D investment in the satellite parts and components industry. These advancements are creating new opportunities for the development of innovative components.

- In November 2022, ESA announced that it proposed a 25% boost in space funding over the next three years designed to maintain Europe's lead in Earth observation, expand navigation services, and remain a partner in exploration with the United States. The European Space Agency (ESA) is asking its 22 nations to back a budget of some EUR 18.5 billion for 2023-2025. Likewise, in September 2022, France announced that it is expecting to increase spending on national and European space programs.

- In North America, global government expenditure for space programs hit a record of approximately 103 billion in 2021. The region is the epicenter of space innovation and research, with the presence of NASA, the world's biggest space agency. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space in the world. In the United States, federal agencies receive aid from the government every year, known as funding, USD 32.33 billion for its subsidiaries. The spending on space and research grants is expected to surge in the region, growing the sector's importance in every domain of the global economy.

Satellite Parts and Components Industry Overview

The Satellite Parts and Components Market is fairly consolidated, with the top five companies occupying 90.12%. The major players in this market are General Dynamics, Lockheed Martin Corporation, Northrop Grumman Corporation, Thales and The Boeing Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Satellite Mass

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Global

- 4.4.2 Australia

- 4.4.3 Brazil

- 4.4.4 Canada

- 4.4.5 China

- 4.4.6 France

- 4.4.7 Germany

- 4.4.8 India

- 4.4.9 Iran

- 4.4.10 Japan

- 4.4.11 New Zealand

- 4.4.12 Russia

- 4.4.13 Singapore

- 4.4.14 South Korea

- 4.4.15 United Arab Emirates

- 4.4.16 United Kingdom

- 4.4.17 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Region

- 5.1.1 Asia-Pacific

- 5.1.2 Europe

- 5.1.3 North America

- 5.1.4 Rest of World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 AAC Clyde Space

- 6.4.2 BAE Systems

- 6.4.3 General Dynamics

- 6.4.4 Innovative Solutions in Space BV

- 6.4.5 Jena-Optronik

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 Northrop Grumman Corporation

- 6.4.8 OHB SE

- 6.4.9 SENER Group

- 6.4.10 Sitael S.p.A.

- 6.4.11 Thales

- 6.4.12 The Boeing Company

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

衛星通訊設備市場:按類型、技術、產品和最終用戶分類 - 全球預測 2024-2030

衛星通訊設備市場:按類型、技術、產品和最終用戶分類 - 全球預測 2024-2030 2024-2032 年混合衛星蜂窩終端市場(按平台、頻段、服務、最終用戶和地區分類)

2024-2032 年混合衛星蜂窩終端市場(按平台、頻段、服務、最終用戶和地區分類) 2024 年行動衛星通訊世界市場報告

2024 年行動衛星通訊世界市場報告 衛星組件:市場佔有率分析、產業趨勢、成長預測(2024-2029)

衛星組件:市場佔有率分析、產業趨勢、成長預測(2024-2029) 2024 年衛星通訊(SATCOM) 設備全球市場報告

2024 年衛星通訊(SATCOM) 設備全球市場報告 衛星通訊行動全球市場:機會與策略(~2032)

衛星通訊行動全球市場:機會與策略(~2032) 到 2030 年經濟型 4 通道接收器市場預測:按類型、應用和地區分類的全球分析

到 2030 年經濟型 4 通道接收器市場預測:按類型、應用和地區分類的全球分析 全球衛星通訊終端市場:趨勢、預測與競爭分析(截至2030年)

全球衛星通訊終端市場:趨勢、預測與競爭分析(截至2030年) SOTM(行動衛星通訊)市場報告:至2030年的趨勢、預測與競爭分析

SOTM(行動衛星通訊)市場報告:至2030年的趨勢、預測與競爭分析 混合蜂巢式終端市場報告:至2030年的趨勢趨勢、預測與競爭分析

混合蜂巢式終端市場報告:至2030年的趨勢趨勢、預測與競爭分析

▼