|

市場調查報告書

商品編碼

1431460

商業建築機器人:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Robots for Commercial Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

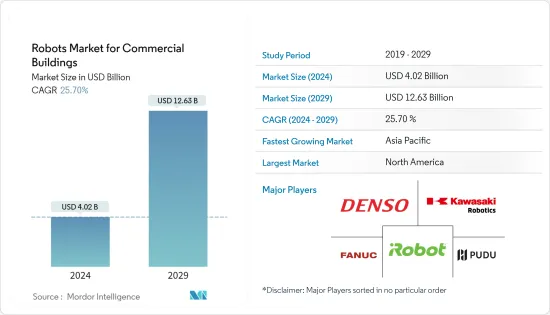

商業建築機器人市場預計將從2024年的40.2億美元成長到2029年的126.3億美元,預測期間(2024-2029年)複合年成長率為25.70%。

主要亮點

- 技術發展的加速和勞動力短缺的加劇正促使設施管理公司轉向自動化工具,以實現更高水準的清潔度、服務和技術力。

- 自動化和人工智慧技術正在改變許多行業,從醫療保健到銀行再到零售,雖然商業建築不是早期採用者,但它們是另一個開始受益於先進技術以提高效率的行業。這絕對是一個行業。

- 商用機器人廣泛用於掃地、拖地、吸塵等清潔任務。這些機器人可以透過編程在特定時間清潔特定區域,從而降低人事費用並提高效率。

- 伺服器機器人因其提高的效率、非接觸式服務、增加的容量和成本效益而在餐廳中越來越受歡迎。這些機器人可以同時提供多種菜餚和飲料,有助於加快服務速度並減少顧客等待時間。

- 因此,各供應商定期進行技術進步並專注於策略投資,以擴大產品陣容並滿足不同的客戶需求。例如,2023 年 2 月,Kum &Go 宣布與 ICE Cobotics 合作,推出自動地板清潔機器人。透過整合無人商店,該品牌可以將員工從重複性任務中解放出來,專注於為貨架和冷藏櫃備貨、提供生鮮食品以及提高店內顧客參與度。

商業建築機器人市場趨勢

掃地機器人可望佔據較大佔有率

- 地板清潔機器人是一種自主設備,旨在無需人工干預即可清潔地板。這些機器人使用各種技術,包括感測器、地圖演算法和攝影機,來導航房間和清潔地板。這些機器人通常具有刷子和吸力來清潔地板上的污垢和碎片。

- 商務用地板清潔機器人可以將清潔人員解放出來,讓他們從事其他無法自動化的任務,讓清潔人員有更多的時間專注於只有人類才能完成的任務,從而幫助最大限度地提高員工的生產力和效率。

- 此外,推動機器人地板清潔需求的主要因素是其便利性。隨著忙碌的生活方式,人們正在尋找簡單有效的方式來維護自己的房屋,而機器人地板清潔機需要更少的人手並提供無憂的清潔體驗。

- 地面清潔機器人廣泛應用於機場,清潔航站入口、安檢口、行李提取區等人流量大的區域。這些區域積聚了大量污垢,機器人可以有效清除這些污垢。

- 由於這些原因,各機場擴大引入地板清潔機器人。例如,2022 年 12 月,夏威夷運輸部機場部門對 Daniel K. Inouye 國際機場進行了現代化改造,安裝了兩台自動地板清潔機來補充清潔服務。丹尼爾井上國際機場平均每天接待 73,000 名旅客。如此大量的日常用戶創造了對自主清潔機器人的需求。

北美佔據主要市場佔有率

- 北美是全球最大、最先進的機器人解決方案市場之一。強勁的經濟、顯著的機場客流量、零售和醫院清潔機器人的使用增加以及餐旅服務業服務機器人的使用都將推動該國對商用機器人的需求。

- 許多家庭和企業正在投資這些技術,以使服務、清潔和消毒任務更有效率、更省時。

- 清潔機器人透過減少接觸有害清潔化學物質和過敏原來幫助改善健康和安全。保持地板和表面清潔乾燥還可以降低滑倒、絆倒和跌倒的風險。

- 根據美國美國職業安全與健康研究所的數據,職場化學品暴露是美國最嚴重的問題之一。美國有超過 1300 萬工人可能透過皮膚接觸化學物質。皮膚病是最常見的職業病之一,在美國每年造成的損失估計超過 10 億美元。

- 基於這些原因,在該地區營運的各種供應商都致力於開發創新解決方案。例如,2022 年 9 月,iRobot Corporation 發布了一款二合一機器人吸塵器、Roomba Combo j7+ 和拖把,配備了 iRobot OS 5.0 更新。 Roomba Combo J7+ 首先清潔地毯,然後同時吸塵和拖地硬地板,一次清潔該區域,從而節省用戶時間。

商業建築機器人產業概況

商業建築機器人市場高度分散,由許多相互競爭的公司組成。從市場佔有率來看,目前由幾家大公司佔據市場主導地位,包括 iRobot Corporation、Omron Adept Technologies Inc. 和 Pudu Robotics。這些擁有重要市場佔有率的領先公司正在擴大其在全部區域的基本客群。許多公司正在與各種新興企業進行策略合作計劃,以提高市場佔有率和盈利。

2023年2月,中國領先的餐飲服務機器人製造商普渡機器人完成C輪資金籌措,融資超過1,500萬美元。公司將利用這筆資金建造生產基地,擴大產能,開發適用於商務用清潔場景的產品。

2022年10月,領先的清潔機器人公司科沃斯發表了兩款新型智慧機器人。除了該公司在全球的機器人清潔產品陣容,包括 DEEBOT(家用地板清潔器)、WINBOT(窗戶和表面清潔器)和 AIRBOT(空氣淨化機器人)之外,科沃斯還在擴大其機器人清潔類別。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買家/消費者的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業價值鏈分析

第5章市場動態

- 市場促進因素

- 政府加大對機器人調查的力度

- 租賃、RaaS(機器人即服務)等多樣化經營模式

- 市場限制因素

- 產品成本高

- 缺乏客戶意識

第6章市場區隔

- 機器人類型

- 地板清潔機器人

- 消毒機器人

- 零售貨架管理機器人

- 服務機器人

- 建築服務機器人

- 按最終用戶產業

- 零售

- 餐廳

- 醫療機構

- 飛機場

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭形勢

- 公司簡介

- iRobot Corporation

- Pudu Robotics

- Denso Corporation

- Fanuc Corporation

- Kawasaki Robotics GmbH

- Kuka AG

- Mitsubishi Electric Corporation

- SoftBank Robotics Corp

- Ecovacs Robotics

- ABB Ltd.

- Nachi Fujikoshi Corporation

- Diversey

- Yaskawa Electric Corporation

- Samsung Electronics Co Ltd.

- Vorwerk & Co. KG

第8章投資分析

第9章 市場未來展望

The Robots Market for Commercial Buildings Industry is expected to grow from USD 4.02 billion in 2024 to USD 12.63 billion by 2029, at a CAGR of 25.70% during the forecast period (2024-2029).

Key Highlights

- The increasing technological developments and the ongoing labor shortage encourage facility management companies to switch to automated tools for higher cleanliness, service, and technological capabilities.

- Automation and AI technology have transformed many industries, from healthcare to banking to retail, and while commercial buildings were not early adopters, they are definitely another industry beginning to benefit from advanced technology for improving efficiency.

- Commercial robots are widely used for cleaning tasks such as sweeping, mopping, and vacuuming. These robots can be programmed to clean specific areas at specific times, reducing labor costs and improving efficiency.

- Serving robots are also becoming increasingly popular in restaurants, as they provide improved efficiency, contactless service, increased capacity, and are cost-effective. These robots can carry multiple dishes or drinks at once, which helps speed up service and reduce wait times for customers.

- Due to such reasons, various vendors regularly make technological advancements and focus on strategic investments to expand their product offerings and cater to varying customer needs. For instance, in February 2023, Kum & Go announced a partnership with ICE Cobotics to deploy automated floor-cleaning robots. By integrating the autonomous equipment, the brand will help free up associates from repetitive work and allow them to focus on keeping shelves and coolers fully stocked, delivering fresh food offerings, and increasing engagement with in-store customers.

Commercial Buildings Robots Market Trends

Floor Cleaning Robots Expected to Have a Major Share

- Floor-cleaning robots are autonomous devices designed to clean floors without human intervention. These robots use various technologies, such as sensors, mapping algorithms, and cameras, to navigate around the room and clean floors. These robots typically have brushes and vacuum suction to clean dirt and debris from floors.

- Commercial floor cleaning robots free up cleaning staff for other tasks that can't be automated and help to maximize employees' productivity and efficiency so that the cleaning staff has more time to focus on the tasks that only humans can do.

- Moreover, the primary factor driving the demand for robot floor cleaning is its convenience. With busy lifestyles, people are looking for easy and efficient ways to maintain their homes, and robot floor cleaners offer a hassle-free cleaning experience without requiring much human intervention.

- Floor-cleaning robots are widely used in airports to clean high-traffic areas, such as terminal entrances, security checkpoints, and baggage claim areas. These areas accumulate a lot of dirt, which these robots can efficiently remove.

- Due to such reasons, various airports are deploying floor-cleaning robots. For instance, in December 2022, the Hawaii Department of Transportation's Airports Division modernized the Daniel K. Inouye International Airport with two automatic floor cleaners to supplement janitorial services. An average of 73,000 arrivals walk through the Daniel K. Inouye International Airport daily. Such a high daily footfall creates a need for autonomous cleaning robots.

North America to Account for Major Market Share

- North America is one of the largest and most advanced markets for robotic solutions in the world. The strong economy, with notable airport traffic, increased use of cleaning robots in retail and hospitals, and the use of servicing robots in the hospitality sector, is poised to drive the demand for commercial robots in the country.

- Robots in commercial buildings are becoming increasingly popular in the region, as many households and businesses are investing in these technologies to make serving, cleaning, and disinfecting tasks more efficient and less time-consuming.

- Cleaning robots help improve health and safety by reducing exposure to harmful cleaning chemicals and allergens. They also reduce the risk of slips, trips, and falls by keeping floors and surfaces clean and dry.

- According to the National Institute for Occupational Safety and Health, chemical exposure in the workplace is one of the most significant problems in the United States. Over 13 million workers in the country are potentially exposed to chemicals through their skin. Skin disorders are among the most significantly reported occupational diseases, resulting in an estimated annual cost of over USD 1 billion in the United States.

- Due to such reasons, various vendors operating in the region are focusing on developing innovative solutions. For instance, in September 2022, iRobot Corporation introduced a Roomba Combo j7+, a 2-in-1 robot vacuum, and a mop with iRobot OS 5.0 updates. The Roomba Combo j7+ vacuums rugs and carpets first and then vacuums and mops hard floors concurrently, saving users time by cleaning the area in a single job.

Commercial Buildings Robots Industry Overview

The robots market for commercial buildings is highly fragmented and consists of many competitive players. In terms of market share, a few major players, such as iRobot Corporation, Omron Adept Technologies Inc., and Pudu Robotics, currently dominate the market. These major players with a significant share of the market are expanding their customer base across the region. Many companies are forming strategic and collaborative initiatives with various start-ups to increase their market share and profitability.

In February 2023, Pudu Robotics, a leading restaurant service robotics manufacturer based in China, completed its Series C funding round to raise more than USD 15 million. The company will use the funds to build a production base, expand production capacity, and develop products for commercial cleaning scenarios.

In October 2022, ECOVACS, one of the leading cleaning robotics companies, announced the launch of two new smart robots. Adding to its global lineup of robotic cleaning products, including DEEBOT robotic home floor cleaners, WINBOT window and surface cleaners, and AIRBOT air purifying robots, the additions expand the robotic cleaning category with ECOVACS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Government Initiatives for Robot Research

- 5.1.2 Various Business Models, Such As Leasing and Robot-as-a-Service

- 5.2 Market Restraints

- 5.2.1 High Product Cost

- 5.2.2 Lack of Customer Awareness

6 MARKET SEGMENTATION

- 6.1 Type of Robots

- 6.1.1 Floor Cleaning Robots

- 6.1.2 Disinfection Robots

- 6.1.3 Retail Shelf Management Robots

- 6.1.4 Serving Robots

- 6.1.5 Building Service Robots

- 6.2 End-user Verticals

- 6.2.1 Retail

- 6.2.2 Restaurants

- 6.2.3 Healthcare Facilities

- 6.2.4 Airports

- 6.2.5 Other End-user Verticals

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 iRobot Corporation

- 7.1.2 Pudu Robotics

- 7.1.3 Denso Corporation

- 7.1.4 Fanuc Corporation

- 7.1.5 Kawasaki Robotics GmbH

- 7.1.6 Kuka AG

- 7.1.7 Mitsubishi Electric Corporation

- 7.1.8 SoftBank Robotics Corp

- 7.1.9 Ecovacs Robotics

- 7.1.10 ABB Ltd.

- 7.1.11 Nachi Fujikoshi Corporation

- 7.1.12 Diversey

- 7.1.13 Yaskawa Electric Corporation

- 7.1.14 Samsung Electronics Co Ltd.

- 7.1.15 Vorwerk & Co. KG

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MAREKET

公共關係機器人市場按產品(遠端臨場公共關係機器人、人形公共關係機器人等)、最終用戶(酒店和餐廳、行動引導和資訊、媒體關係機器人等)和地區2024-2032

公共關係機器人市場按產品(遠端臨場公共關係機器人、人形公共關係機器人等)、最終用戶(酒店和餐廳、行動引導和資訊、媒體關係機器人等)和地區2024-2032 2024年機器人廚房全球市場報告

2024年機器人廚房全球市場報告 全球零售機器人市場規模研究與預測,按類型(移動機器人、固定機器人、半自主)按應用(庫存管理、交付管理、店內服務等)和區域分析,2023-2030 年

全球零售機器人市場規模研究與預測,按類型(移動機器人、固定機器人、半自主)按應用(庫存管理、交付管理、店內服務等)和區域分析,2023-2030 年 2024-2028年全球飯店機器人市場

2024-2028年全球飯店機器人市場 公共關係機器人市場報告:2030 年趨勢、預測與競爭分析

公共關係機器人市場報告:2030 年趨勢、預測與競爭分析 零售機器人市場:按類型、部署和應用分類 - 2024-2030 年全球預測

零售機器人市場:按類型、部署和應用分類 - 2024-2030 年全球預測 核子機器人市場 - 按類型(遠端機械手、履帶式機器人、無人機、水下機器人 (ROV)、人形機器人)、最終用途產業和預測,2023 - 2032 年

核子機器人市場 - 按類型(遠端機械手、履帶式機器人、無人機、水下機器人 (ROV)、人形機器人)、最終用途產業和預測,2023 - 2032 年 全球公關機器人市場

全球公關機器人市場 全球商用機器人市場研究報告 - 2023 年至 2030 年的行業分析、規模、佔有率、成長、趨勢和預測

全球商用機器人市場研究報告 - 2023 年至 2030 年的行業分析、規模、佔有率、成長、趨勢和預測 2023-2030年全球餐旅業機器人市場規模研究和預測,按終端用戶類型和區域分析

2023-2030年全球餐旅業機器人市場規模研究和預測,按終端用戶類型和區域分析