|

市場調查報告書

商品編碼

1431294

HVAC 現場設備:市場佔有率分析、產業趨勢/統計、成長預測 (2024-2029)HVAC Field Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

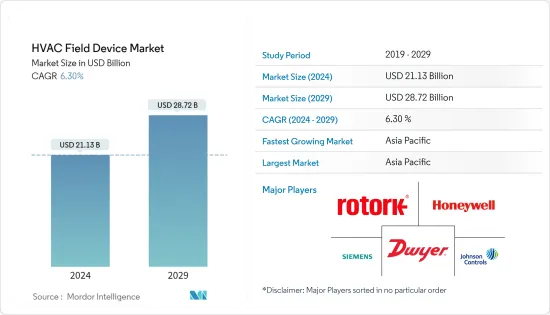

全球HVAC現場設備市場規模預計到2024年將達到211.3億美元,並在2024-2029年預測期內以6.30%的複合年成長率成長,到2029年達到287.2億美元。

疫情對暖通空調產業產生了重大影響,由於挨家挨戶的限制以及企業避免投資新設備,前幾個月的系統需求大幅減少。受疫情影響,世界各地許多建設計劃被取消。商業、住宅和工業建設活動的下降暫時減少了對 HVAC 現場設備的需求。

主要亮點

- 因此,美國政府投入了大量聯邦資金,可用於改善公共設施、學校和其他環境的室內空氣品質。例如,美國救援計畫向州和地方政府提供了 3500 億美元,向學校提供了 1220 億美元用於通風和過濾升級。

- 最終用戶正在採用智慧型 HVAC 設備來在實際問題發生之前預測何時需要維護。利用物聯網 (IoT) 系統的現代 HVAC 技術整合了感測器、軟體和連接功能,使 HVAC 系統能夠與其他聯網設備交換資料。物聯網系統透過感測有關空氣品質和設備健康狀況的資料來增強預防性保養。此外,最新、最實惠的物聯網 HVAC 技術使查看多種設備類型的見解變得更加容易,包括屋頂空氣調節機、風冷和水冷熱泵以及帶再熱系統的可變風量 (VAV) 。 變得。暖通空調設備的這些開拓預計將進一步推動所研究的市場。

- 消費者購買力的上升加上可支配收入的增加,特別是在新興經濟體,也對市場產生正面影響。例如,根據中國國家統計局的數據,中國居民人均可支配收入為36883元,2022年扣除通膨因素的名義收入與前一年同期比較增5.0%,絕對收入增加2.9%。

- 除此之外,製造業的崛起進一步加強了暖通空調設備和現場設備的範圍。根據工業《世界製造業生產第三季報告(2022年)》,亞洲和大洋洲製造業生產成長4.4%,超過北美(3.5%)和歐洲(1.7%)。拉丁美洲和加勒比海地區的製造業成長了 4.9%,而南美洲則成長了 3.0%。

- 此外,東歐氣候寒冷,例如捷克共和國、波蘭和保加利亞,對暖氣解決方案的需求很高。與該地區其他國家一樣,正在採取更多措施來提高暖氣和冷氣產業的能源效率。 Stratego 的共同創辦人歐盟智慧能源歐洲計畫聲稱,2010 年至 2050 年間投資 500 億歐元可以節省足夠的燃料,從而降低能源系統的成本。作為這項投資的一部分,區域供暖的佔有率將達到 50 億歐元,個人熱泵的佔有率將達到 150 億歐元。

- 世界各地的一些政府正在提供財政優惠,以鼓勵在住宅和商業空間中使用節能設備。例如,美國政府推出了2005年能源政策法案,為新建商業建築提供每平方英尺高達1.80美元的扣除額。美國暖氣、冷氣和空調工程師協會認為,政府的努力以及對環境退化和能源管理認知的提高將維持對節能 HVAC 控制系統(包括現場設備)的需求。

HVAC現場設備市場趨勢

住宅領域預計將佔據較大市場佔有率

- 推動暖通空調現場設備市場的主要因素之一是住宅建築能源消耗比例的不斷增加,這導致利用能源維修系統來提高建築物的效率。例如,HomeServe 於 2022 年 8 月推出了家庭 HVAC 訂閱福利計劃。這有助於公用事業公司實現能源效率目標,並透過降低更換昂貴的家庭 HVAC(冷暖氣空調)系統的成本來提高客戶滿意度。

- 對空調的需求不斷成長是推動該行業市場的最重要因素之一。中央空調預計將成為世界各地人們最受歡迎的居家降溫方式。根據IEA統計,空調和風扇約佔全球建築物總電力消耗量的五分之一,即全球總電力消耗量的10%。未來 30 年,空調的使用預計將迅速增加,並成為全球電力需求的主要推動力之一。

- 此外,推動住宅領域暖通空調現場設備市場擴張的主要因素之一是人們對室內空氣品質日益成長的關注。一些政府也透過頒布法律來滿足能源需求並實施以折扣價銷售這些空調的計畫來鼓勵購買這些高效能設備。例如,能源效率局 (BEE) 和電力部透過定期向上修改能源標籤計畫以支援節能系統來執行有關住宅空調能耗的法規。

- OBERLO 預計,2023 年將有 6,040 萬美國家庭積極使用智慧家庭設備,比 2022 年的 5,740 萬家庭使用智慧家庭設備增加 3%。到2023年,使用智慧家庭科技的家庭比例預計將達到所有家庭的46.5%。這種普及預計將增加對能耗更少的智慧型裝置(包括暖通空調系統)的需求。

- 為了減少二氧化碳排放,供應商和許多政府也致力於住宅脫碳。因此,熱泵在住宅領域的採用預計將加速,幫助住宅減少能源費用,並幫助減少導致全球氣候變遷的石化燃料的使用。開利、大金、江森自控、丹佛斯等主要供應商不斷投資推出住宅產品,這是推動市場的主要因素之一。

亞太地區預計將佔據主要市場佔有率

- 過去幾年,由於永續建設政策和向服務主導經濟的轉變,中國建築業實現了大幅成長。大型基礎建設計劃投資已成為中國政府提振成長策略的重要組成部分。

- 根據中國建設業協會統計,2021年我國完工建築中住宅建築佔比較大。住宅建築面積佔竣工占地面積67%以上。隨著國家經濟的成長,人們從農村地區遷移到大城市,增加了這些地區的住宅需求。此外,用作投資物業的公寓正在推動需求。如此大規模的住宅預計將推動調查市場。

- 根據國土交通省的數據,2022 年日本住宅數約為 85.95 萬套。與與前一年同期比較相比成長了0.4%。 2022年日本開工辦公大樓數量將超過10,200棟。如此龐大的建築數量可能會推動所研究的市場。

- 此外,根據IBEF的數據,印度去年在房地產資產的投資為24億美元,年增率為52%。 2000年4月至2022年9月,該產業的直接投資(包括建設開發和營運)總計551.8億美元。房地產的顯著成長可能會促進所研究市場的成長。

- 此外,韓國的新資料中心建設計劃也支持了市場成長。例如,SK Telecom 的網路基礎設施部門 SK Broadband 最近宣布計劃投資 17.5 億美元,在新興企業園區周圍建造一個全新的超大規模資料中心。資料中心和Start-Ups叢集開發的第一階段預計將於 2024 年完成,包括 4 座資料中心大樓,並計劃在 2029 年再增加 12 座。

HVAC 現場設備產業概述

全球 HVAC 現場設備市場高度分散,主要參與者眾多。從市場佔有率來看,目前少數大公司佔據市場主導地位。這些擁有顯著市場佔有率的領先公司致力於擴大海外基本客群。這些公司利用策略合作計劃來增加市場佔有率和盈利。

2023 年 3 月,Honeywell推出了 Versatilis 變送器,用於對幫浦、馬達、壓縮機、風扇、鼓風機和變速箱等旋轉設備進行狀態監控。HoneywellVersatilis 變送器可為旋轉設備提供正確的測量,提供可提高各行業安全性、可用性和可靠性的智慧。

2022年8月,Airzone宣布將憑藉獨特的HVAC變頻系統智慧控制解決方案進入快速成長的北美市場。 Airzone 的 Aidoo Pro 連接了專有的 HVAC 逆變器和小型分離式製造商通訊協定以及物聯網設備 API,包括流行的 Ecobee、Honeywell 和 Nest 智慧恆溫器。 Aidoo Pro 允許 HVAC 專業人員將 HVAC 逆變器系統與領先的智慧恆溫器整合,保留所有逆變器功能並提供無與倫比的效率、節能、連接性和舒適性。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 對工業的影響評估

第5章市場動態

- 市場促進因素

- 開拓建築市場

- 支持性政府法規,包括透過稅額扣抵計劃激勵節能

- 物聯網和產品創新的出現支持替代

- 市場限制因素

- 取決於宏觀經濟經濟狀況

- 節能系統的初始成本較高

第6章市場區隔

- 按類型

- 控制閥

- 平衡閥

- PICV

- 風門暖通空調

- 風門致動器HVAC

- 其他類型

- 透過感測器

- 環境感測器

- 多感測器

- 空氣品質感測器

- 運轉率/照明

- 其他感測器

- 按最終用戶產業

- 商業的

- 住宅

- 工業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭形勢

- 公司簡介

- Siemens AG

- Honeywell International Inc.

- Johnson Controls International PLC

- Rotork Plc

- Dwyer Instruments Inc.

- Belimo Holding AG

- Robert Bosch GmbH

- Electrolux AB

- Azbil Corporation

- Danfoss A/S

- Daikin Industries Ltd.

第8章投資分析

第9章 市場未來展望

The HVAC Field Device Market size is estimated at USD 21.13 billion in 2024, and is expected to reach USD 28.72 billion by 2029, growing at a CAGR of 6.30% during the forecast period (2024-2029).

The pandemic significantly influenced the HVAC industry, as demand for the systems observed a significant drop during the initial months, owing to lockdown restrictions and businesses refraining from investing in new equipment. Due to the pandemic, many construction projects were halted across the world. Reduced commercial, residential, and industrial construction activities temporarily dampened the demand for HVAC field devices.

Key Highlights

- Consequently, the US government has significantly invested in federal funds that can be used in public buildings, schools, and other settings to improve indoor air quality. For instance, the American Rescue Plan provided USD 350 billion for state and local governments, along with USD 122 billion for schools, that can be used for ventilation and filtration upgrades.

- The end users are adopting smart HVAC equipment to predict when maintenance is needed before a real issue occurs. The latest HVAC technologies, which utilize an Internet of Things (IoT) system, are embedded with sensors, software, and connectivity, enabling the HVAC system to exchange data with other connected devices. IoT systems enhance preventative maintenance by sensing data on air quality and equipment status. Moreover, the latest and most affordable Internet of Things HVAC technology makes it significantly easier to view insights across several equipment types, such as rooftop air-handling units, air- and water-cooled heat pumps, variable air volume (VAV) with reheat systems, etc. These developments in HVAC equipment are expected to further drive the studied market.

- Rising consumer purchasing power coupled with increasing disposable income, especially in developing economies, also positively impacts the market. For instance, according to the National Bureau of Statistics of China, the average disposable income per capita for residents in China was 36,883 yuan, a nominal increase of 5.0% compared to the previous year and an absolute increase of 2.9% after adjusting for inflation in 2022.

- In addition to this, the rising manufacturing sector has further bolstered the scope of HVAC equipment and field devices. According to the World Manufacturing Production Quarter 3 2022 Report by the United Nations Industrial Development Organization, manufacturing production in Asia and Oceania experienced an output growth of 4.4%, ahead of North America (3.5%) and Europe (1.7%). The manufacturing sector in Latin America and the Caribbean expanded by 4.9%, and South Africa grew by 3.0%.

- Furthermore, Eastern Europe has colder climatic conditions, and the demand for heating solutions is significant in these countries, such as the Czech Republic, Poland, Bulgaria, and others. Like other countries in the region, measures to increase energy efficiency in the heating and cooling sectors are rising. The Intelligent Energy Europe Programme of the EU, which co-founded Stratego, claims that an investment of EUR 50 billion between 2010 and 2050 will save enough fuel to lower the costs of the energy system. As part of this investment, district heating's share stood at EUR 5 billion and individual heat pumps at EUR 15 billion.

- Several governments worldwide are offering financial benefits to promote the use of energy-saving equipment in residential and commercial spaces. For instance, the U.S. government introduced the Energy Policy Act of 2005, which provides a tax deduction of up to USD 1.80 per square foot for new commercial buildings. Buildings that reduce their regulated energy consumption by 50% in comparison to the specifications outlined in the American Society of Heating, Refrigerating, and Air-Conditioning Engineers, Inc.'s 2001 new construction standard (ASHRAE 90.1) were eligible for the tax benefit. Government initiatives and rising awareness about environmental degradation and energy management are expected to keep the demand for energy-efficient HVAC control systems, including field devices.

HVAC Field Device Market Trends

Residential Sector is Expected to Hold Significant Market Share

- One of the key drivers propelling the market for HVAC field devices is the growing percentage of energy consumption in residential buildings, which has led to the usage of energy retrofit systems to increase the efficiency of buildings. For instance, HomeServe introduced its benefits program for home HVAC subscriptions in August 2022. This helps utilities accomplish energy efficiency goals and improve customer satisfaction by lowering the cost of replacing an HVAC (heating and air conditioning) system, which is expensive for households.

- Growing demand for air conditioners has been one of the most critical factors driving the market in this sector. Central air conditioning is expected to become the most common way people across the globe cool their homes. According to the IEA, air conditioners and electric fans account for about a fifth of the total electricity in buildings worldwide, or 10% of all global electricity consumption. Over the next three decades, the use of ACs is set to soar, becoming one of the top drivers of global electricity demand.

- Furthermore, one of the key factors propelling the expansion of the HVAC field device market in the residential sector is the rising concern for indoor air quality. Also, several governments are encouraging the purchase of this high-efficiency equipment by enforcing laws to satisfy energy demand and implementing sales programs for these air conditioners at discounted prices. By routinely making upward changes to the Energy Labeling Program in favor of energy-efficient systems, the Bureau of Energy Efficiency (BEE) and the Ministry of Electricity, for instance, have been enforcing rules on the amount of electricity consumed by residential air conditioners.

- According to OBERLO, 60.4 million US homes were expected to be actively utilizing smart home devices in 2023, which was 3% more than in 2022, when 57.4 million households used smart home devices. In 2023, the proportion of households utilizing smart home technology is expected to be 46.5% of all households. This penetration is likely to lead to an increase in demand for smart devices with low energy consumption, including HVAC systems.

- To reduce CO2 emissions, vendors and numerous governments are also focused on residential decarbonization. As a result, it is anticipated that the adoption of heat pumps in the residential sector will gain traction, which will aid homeowners in reducing their utility costs and promote a decrease in the use of fossil fuels, which feed global climate change. Major vendors like Carrier, Daikin, Johnson Controls, Danfoss, and others are constantly investing in residential product launches, which is one of the major factors driving the market.

Asia-Pacific is Expected to Hold Significant Market Share

- The construction industry in China has witnessed massive growth due to sustainable construction policies and a shift toward a service-led economy over the past few years. Investing in large-scale infrastructure projects has been a vital part of the Chinese government's strategy to boost growth.

- According to the China Construction Industry Association, in 2021, residential structures accounted for a significant share of finished construction in China. Buildings intended for housing accounted for over 67% of the completed floor space. As the country's economy grows, people migrate from rural areas to major cities, increasing demand for residential accommodation in these locations. Furthermore, apartments utilized as investment properties drive up demand. Such massive residential construction is expected to drive the study market.

- According to MLIT (Japan), there were about 859.5 thousand home starts in Japan in 2022. Compared to the prior year, this represented an increase of 0.4%. Over 10,200 office building construction projects began in Japan in 2022. Such a vast number of constructions would drive the studied market.

- Further, according to IBEF, India invested USD 2.4 billion in real estate assets over the last year, a 52% increase annually. From April 2000 to September 2022, FDI in the industry, comprising construction development and operations, totaled USD 55.18 billion. Such a massive rise in real estate would allow the studied market to grow.

- Further, the new data center construction projects in the country are also pushing the market's growth in South Korea. For instance, SK Broadband, the internet infrastructure division of SK Telecom, recently announced plans to invest USD 1.75 billion in the creation of a brand-new hyperscale data center encircling a startup campus. The first phase of the data center and startup cluster development is expected to be completed by 2024 and comprise four data center buildings, with plans to add 12 more by 2029.

HVAC Field Device Industry Overview

The global HVAC field device market is highly fragmented and has several major players. In terms of market share, a few of the major players currently dominate the market. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

In March 2023, Honeywell introduced its Versatilis transmitters for condition-based monitoring of rotating equipment such as pumps, motors, compressors, fans, blowers, and gearboxes. Honeywell Versatilis transmitters provide relevant measurements of rotating equipment, delivering intelligence that can improve safety, availability, and reliability across industries.

In August 2022, Airzone announced it was entering the rapidly growing North American market with an exclusive smart control solution for HVAC inverter systems. Airzone's Aidoo Pro acted as the bridge between proprietary HVAC inverter and mini-split manufacturers' protocols and IoT device APIs, including for the popular Ecobee, Honeywell, and Nest smart thermostats. The Aidoo Pro enables HVAC professionals to integrate HVAC inverter systems with leading smart thermostats, preserving all inverter features and providing unparalleled efficiency, energy savings, connectivity, and comfort.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Development of the Construction Market

- 5.1.2 Supportive Government Regulations Including Incentives for Saving Energy through Tax Credit Programs

- 5.1.3 The Emergence of IoT and Product Innovations to Aid Replacements

- 5.2 Market Restraints

- 5.2.1 Dependence on Macro-economic Conditions

- 5.2.2 High Initial Cost of Energy Efficient Systems

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Control Valve

- 6.1.2 Balancing Valve

- 6.1.3 PICV

- 6.1.4 Damper HVAC

- 6.1.5 Damper Actuator HVAC

- 6.1.6 Other Types

- 6.2 By Sensors

- 6.2.1 Environmental Sensors

- 6.2.2 Multi Sensors

- 6.2.3 Air Quality Sensors

- 6.2.4 Occupancy & Lighting

- 6.2.5 Other Sensors

- 6.3 By End-user Industry

- 6.3.1 Commercial

- 6.3.2 Residential

- 6.3.3 Industrial

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Honeywell International Inc.

- 7.1.3 Johnson Controls International PLC

- 7.1.4 Rotork Plc

- 7.1.5 Dwyer Instruments Inc.

- 7.1.6 Belimo Holding AG

- 7.1.7 Robert Bosch GmbH

- 7.1.8 Electrolux AB

- 7.1.9 Azbil Corporation

- 7.1.10 Danfoss A/S

- 7.1.11 Daikin Industries Ltd.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

2024-2028年非住宅暖通空調租賃設備的全球市場

2024-2028年非住宅暖通空調租賃設備的全球市場 HVAC-R(暖氣、通風、空調、冷凍)的全球市場:分析與預測(2023-2033)

HVAC-R(暖氣、通風、空調、冷凍)的全球市場:分析與預測(2023-2033) 到 2030 年暖氣、通風和空調系統市場預測 - 各產品、技術、最終用戶和地理位置的全球分析

到 2030 年暖氣、通風和空調系統市場預測 - 各產品、技術、最終用戶和地理位置的全球分析 2024 年 HVAC/商業/工業冷卻設備全球市場報告

2024 年 HVAC/商業/工業冷卻設備全球市場報告 HVAC 內建伺服器市場:按外形尺寸、冷卻能力、產業、組織規模分類 - 2024-2030 年全球預測

HVAC 內建伺服器市場:按外形尺寸、冷卻能力、產業、組織規模分類 - 2024-2030 年全球預測 HVAC 電纜市場:按類別、評級- 2024-2030 年全球預測

HVAC 電纜市場:按類別、評級- 2024-2030 年全球預測 暖通空調售後市場:按類型、產品、最終用戶分類 - 2024-2030 年全球預測

暖通空調售後市場:按類型、產品、最終用戶分類 - 2024-2030 年全球預測 暖通空調全球市場 2024-2028

暖通空調全球市場 2024-2028 暖通空調領域 8 大成長機會:2024 年

暖通空調領域 8 大成長機會:2024 年 北美 HVAC 過濾器更換服務市場:規模、佔有率和趨勢分析報告 - 按類型、按過濾器類型、按設備類型、按應用、按國家、細分市場預測,2024-2030 年

北美 HVAC 過濾器更換服務市場:規模、佔有率和趨勢分析報告 - 按類型、按過濾器類型、按設備類型、按應用、按國家、細分市場預測,2024-2030 年