|

市場調查報告書

商品編碼

1431006

全球伺服馬達市場:市場佔有率分析、產業趨勢/統計、成長趨勢預測(2024-2029)Global Servo Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

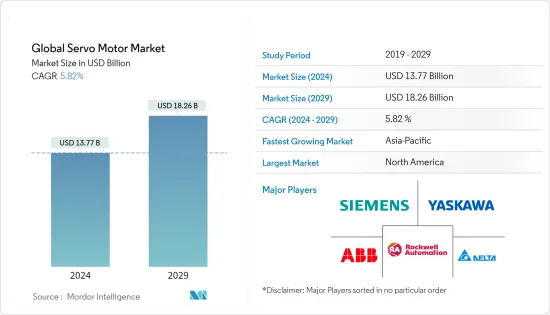

預計2024年全球伺服馬達市場規模為137.7億美元,預計2029年將達到182.6億美元,在預測期內(2024-2029年)複合年成長率為5.82%。

最近的技術進步和政府政策(例如多個國家的最低能源性能標準(MEPS))實現了節能馬達系統,並擴大了伺服馬達和驅動器的市場。

主要亮點

- 最先進的運動控制裝置是伺服馬達。採用先進的設計技術、高磁性磁鐵材料和精確的尺寸公差。雖然不是特定類型的馬達,但這些電氣設備是為需要高性能、快速反轉和精確定位的運動控制應用而設計的。此外,它易於安裝且無需維護,進一步增加了預測期內的需求。

- 推動市場的主要因素是自動化伺服馬達的使用。伺服系統的技術進步正在增加最終用戶的興趣。這些電氣設備用於多種行業,包括汽車製造、包裝器材、食品加工、半導體和醫療保健。

- 截至 2021 年 2 月,Allied Motion Technologies 推出了 H 系列無刷伺服馬達驅動器,包括 Hiperface DSL、多回饋設備支援和安全扭力關閉 (STO) 安全選項。 H-Drive 是 Allied 新型 AMS伺服套件的一部分,旨在驅動 HeiMotion 無刷伺服馬達和 Megaflux 系列無刷力矩馬達。

- 此外,在 Automate 2022 上,科爾摩根推出了新型 TMB2G 機器人就緒無框伺服馬達。在 2022 年 6 月的分組會議上,科爾摩根也談到了透過永磁馬達設計和選擇來提高機器人效率。

- 影響市場成長的關鍵促進因素包括自動化的快速成長和進步、擴大採用節能國際標準等。嚴格的用電規範、電費上漲、需要用高效能伺服馬達馬達預計將在預測期內推動伺服馬達的需求。

- 由於 COVID-19 大流行,全球工業生產受到干擾。鋼材是伺服馬達常用的原料。鋼鐵業發生了一些混亂,影響了伺服馬達的生產。此外,中國也是鋼鐵生產大國。它每年生產世界一半的鋼鐵。鋼鐵生產因工廠關閉和中國政府在疫情期間實施的貿易限制而受到阻礙。

伺服馬達市場趨勢

自動化的進展

- 製造過程自動化程度的提高、數位化和人工智慧的引入是推動汽車行業工業機器人需求的主要因素。

- 近年來,像 KUKA AG 這樣的汽車製造商已經實現了工廠自動化,以減少現場問題、提高效率並降低營運成本。許多公司紛紛效仿,對其工廠進行自動化改造,以提高收益和效率,從而推動伺服馬達和驅動器市場的發展。

- 例如,2022年6月,Aerobotix和Automated Solutions Australia正式宣佈建立國際機器人自動化合作夥伴關係,用於高超音速飛彈的開發、測試和生產。 Aerobotix 和 ASA 之間的合作將使澳洲國防部門和國防承包能夠更好地利用兩家公司的自動化專業知識。

- 伺服馬達用於要求嚴格的應用,例如機器人、數控工具機以及物料輸送、包裝、工廠自動化、工具機、組裝和其他工業領域的自動化製造。因此,在預測期內,自動化和機器人技術的日益普及預計將推動汽車行業的伺服馬達市場。

北美佔有很大佔有率

- 在北美地區,美國是工業機器人的最大用戶,佔該地區總安裝量的79%。墨西哥則位居第二,佔 9%,第三位是加拿大,佔 7%(資料來源:國際機器人聯合會)。

- 例如,根據自動化推進協會的數據,2021 年 12 月,北美工廠和產業相關人員在 2021與前一年同期比較9 個月訂購了 29,000 台機器人,較去年同期成長 37%。

- 在日本,多個製造流程正在自動化,伺服馬達需要精度和可重複性。與液壓泵和感應馬達不同,伺服馬達可以在運行過程中打開和關閉,從而減少高達 65% 的功耗。

- 伺服解決方案基於最新的單一來源、基於系統的設計理念。它採用了科爾摩根AKD2G伺服驅動器和AKM2G伺服馬達的性能。由於馬達和驅動器在各個方面(驅動器開關頻率、換向演算法、馬達磁性等)都精確匹配,因此工程師在選擇不同製造商的組件時可以避免微不相容。

- Applied Motion Products 擴大了供應商對 MDX Integrated伺服馬達的接受度。此認證確保馬達符合高品質的美國電氣安全標準。 Integrated 的馬達經過了 ANSI/UL 標準 1004-1 旋轉馬達、1004-6 伺服和步進馬達以及 61800-5-1 可調速驅動器測試。認證列為 UL 檔號 E472271。

伺服馬達產業概況

由於市場參與企業熱衷於克服處理器的缺點並加強對新產品開拓的關注,預計伺服馬達市場在預測期內將競爭激烈。公司也注重合作、併購和收購,以擴大其消費者基礎。 ABB Ltd.、Allied Motion Technologies, Inc.、Ametek, Inc.、通用電氣公司、日本電產株式會社、羅克韋爾自動化公司、施耐德電氣、艾默生電氣公司、西門子AG、WEG Industries、日立製作所、東方電機、三菱電機安川電機株式會社、安川電機株式會社等公司是全球主要的伺服馬達製造主要企業。

- 2021 年 11 月,羅克韋爾自動化宣布擴展其 PowerFlex 交流變頻驅動器產品組合,以支援更廣泛的馬達控制應用。客戶可以受益於採用 TotalFORCE 技術的下一代驅動器,該驅動器具有更高的彈性、性能和智慧性。

- 2021 年 4 月 透過增加新的伺服馬達,西門子擴大了 Sinamics S210 單電纜伺服伺服系統的應用範圍。該公司推出了 Simotics S-1FS2,這是一款具有不銹鋼外殼、最高防護等級 IP67/IP69 和高解析度 22 位元絕對式多圈編碼器的馬達版本,適用於製藥和食品行業。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 更多採用國際能源效率標準

- 自動化的進展

- 市場課題

- 擴大低成本替代品的可用性

第 6 章 區隔

- 依馬達類型

- 交流伺服馬達

- 直流伺服馬達

- 依最終用戶產業

- 油和氣

- 化學/石化

- 發電

- 用水和污水

- 金屬/礦業

- 食品和飲料

- 離散製造業

- 其他最終用戶產業

- 地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 義大利

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲/紐西蘭

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 智利

- 其他拉丁美洲

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東和非洲

- 北美洲

第7章 供應商市場佔有率

第8章 競爭形勢

- 公司簡介

- Yaskawa Electric Corporation

- ABB Ltd.

- Siemens AG

- Rockwell Automation, Inc.

- Delta Electronics, Inc.

- Maxon Precision Motors, Inc.

- Mitsubishi Electric Corp.

- FANUC Corp.

- SANMOTION R.

- Schneider Electric

第9章投資分析

第10章投資分析市場的未來

The Global Servo Motor Market size is estimated at USD 13.77 billion in 2024, and is expected to reach USD 18.26 billion by 2029, growing at a CAGR of 5.82% during the forecast period (2024-2029).

Recent technological advancements and government policies such as Minimum Energy Performance Standards (MEPS) in several countries have resulted in energy-efficient motor systems, which has increased the market for servo motors and drives.

Key Highlights

- The most advanced motion control devices are servo motors. It employs advanced design techniques, high-force magnet materials, and precise dimensional tolerance. Although not a specific type of motor, these electrical devices are designed and intended for motion control applications requiring high performance, quick reversing, and precise positioning. Furthermore, it is simple to install and requires no maintenance, further driving their demand over the forecast period.

- The primary factor driving the market is the use of servo motors for automation. Technological advancements in servo systems have increased end-user interest. These electrical devices are used in various industries, including automobile manufacturing, packaging machines, food processing, semiconductors, and healthcare.

- As of February 2021, Allied Motion Technologies introduced the H Series Brushless Servo Motor Drive, which includes Hiperface DSL, multi-feedback device support, and Safe Torque Off (STO) safety options. The H-Drive is part of Allied's new AMS servo packages and is designed to drive the HeiMotion brushless servo motors and Megaflux series of brushless torque motors.

- Further, at Automate 2022, Kollmorgen debuted the new TMB2G Robot-Ready Frameless Servo Motors. At the June 2022 breakout session, Kollmorgen also talked about improving Robot Efficiency Through Permanent Magnet Motor Design and Selection.

- Some significant drivers influencing the market growth are rapid growth and advancements in automation, and increasing adoption of international energy-efficient standards. Stringent electricity utilization standards, rising electricity prices, and the need to replace outdated low-efficiency electric motors with highly efficient servo motors are expected to drive demand for servo motors over the forecast period.

- Global industrial production was disrupted as a result of the COVID-19 pandemic. Steel is a common raw material used in servo motors. Several disruptions occurred in the steel industry and hampered servo motor production. Furthermore, China is a major steel producer. Every year, the country produces half of the world's steel. Steel production was hampered by factory closures and trade restrictions imposed by the Chinese government during the pandemic.

Servo Motor Market Trends

Increasing Automation Advancement

- The growing use of automation in manufacturing processes and the incorporation of digitization and AI are the primary factors driving demand for industrial robots in the automotive sector.

- Automakers, such as KUKA AG, have automated their plants in recent years to reduce the number of issues on the shop floor, improve efficiency, and lower operational costs. Many companies have followed suit, automating their plants to gain better returns and efficiency, thereby driving the servo motors and drives market.

- For instance, in June 2022, Aerobotix and Automated Solutions Australia officially announced an international robotic automation partnership for developing, testing, and manufacturing hypersonic missiles. The Aerobotix-ASA collaboration will make it easier for the Australian defense sector and defense contractors to access both companies' automation expertise.

- Servo motors are used in material handling, packaging, factory automation, machine tools, assembly lines, and other demanding applications such as robotics, CNC machinery, and automated manufacturing in the industrial sector. As a result, increased automation and robotics adoption is expected to drive the market for servo motors in the automotive sector over the forecast period.

North America to Hold Significant Share

- In North America, the United States is the largest industrial robot user in the Americas, accounting for 79% of total installations in the region. Mexico comes second with 9%, and Canada comes third with 7% (source: International Federation of Robotics).

- For Instance, in December 2021, According to the Association for Advancing Automation, factories and industrial concerns in North America ordered a record 29,000 robots in the first nine months of 2021, a 37 % increase over the previous year (A3).

- Servo motors demand accuracy and repeatability in a country where multiple manufacturing processes are becoming increasingly automated. Unlike hydraulic pumps or induction motors, Servo motors are switched on and off during operation to consume less power saving up to 65%.

- The servo solution is based on the most recent single-source, system-based design ideas. It uses Kollmorgen's AKD2G servo drive and AKM2G servo motor's performance capabilities. It avoids micro-incompatibilities when engineers select components from different manufacturers because the motor and drive are precisely matched in every element (e.g., drive switching frequency, commutation algorithms, and motor magnetics).

- Applied motion products increased MDX Integrated servo motor acceptance on the supplier front. The certification ensures that the motors meet high-quality electrical safety standards in the United States. The motors from Integrated were tested by the ANSI/UL standards 1004-1 Rotating Electrical Machines, 1004-6 Servo and Stepper Motors, and 61800-5-1 Adjustable Speed Drives. The certifications are listed as UL file number E472271.

Servo Motor Industry Overview

The market for servo motors is expected to be highly competitive over the forecast period, as market participants are increasingly focusing on new product development with a sharp focus on overcoming the processor's shortcomings. The players are also focusing on partnerships, mergers, and acquisitions to broaden their consumer base. Organizations such as ABB Ltd., Allied Motion Technologies, Inc., Ametek, Inc., General Electric Company, Nidec Corporation, Rockwell Automation Inc., Schneider Electric, Emerson Electric Company, Siemens AG, WEG Industries, Hitachi Ltd., Oriental Motor, Mitsubishi Electric Corp., Yaskawa Electric Corp. are the key performers in manufacturing servo motor globally.

- November 2021- Rockwell Automation, Inc. announced the expansion of its PowerFlex AC variable frequency drive portfolio to support a wider range of motor control applications. Customers will benefit from increased flexibility, performance, and intelligence in their next-generation drive thanks to TotalFORCE Technology.

- April 2021- By adding new servo motors, Siemens is expanding the range of applications for its Sinamics S210 single-cable servo drive system. The company is launching the Simotics S-1FS2, a motor version with a stainless-steel housing, the highest level of protection IP67/IP69, and high-resolution 22-bit absolute multiturn encoders for use in the pharmaceutical and food industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing the adoption of international energy-efficiency standards

- 5.1.2 Growing Automation Advancements

- 5.2 Market Challenges

- 5.2.1 Growing the availability of low-cost alternatives

6 SEGMENTATION

- 6.1 By Motor Type

- 6.1.1 AC Servo Motor

- 6.1.2 DC Servo Motor

- 6.2 By End-user Industry

- 6.2.1 Oil & Gas

- 6.2.2 Chemical & Petrochemical

- 6.2.3 Power Generation

- 6.2.4 Water & Wastewater

- 6.2.5 Metal & Mining

- 6.2.6 Food & Beverage

- 6.2.7 Discrete Industries

- 6.2.8 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 Italy

- 6.3.2.4 France

- 6.3.2.5 Russia

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Australia & New Zealand

- 6.3.3.6 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Chile

- 6.3.4.4 Rest of Latin America

- 6.3.5 Middle-East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 Turkey

- 6.3.5.4 Rest of Middle-East and Africa

- 6.3.1 North America

7 VENDOR MARKET SHARE

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Yaskawa Electric Corporation

- 8.1.2 ABB Ltd.

- 8.1.3 Siemens AG

- 8.1.4 Rockwell Automation, Inc.

- 8.1.5 Delta Electronics, Inc.

- 8.1.6 Maxon Precision Motors, Inc.

- 8.1.7 Mitsubishi Electric Corp.

- 8.1.8 FANUC Corp.

- 8.1.9 SANMOTION R.

- 8.1.10 Schneider Electric

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

交流伺服馬達和驅動器市場 - 按類別、應用和預測,2024 年 - 2032 年

交流伺服馬達和驅動器市場 - 按類別、應用和預測,2024 年 - 2032 年 伺服馬達市場:按類型、系統和應用分類:2023-2032 年全球機會分析和產業預測

伺服馬達市場:按類型、系統和應用分類:2023-2032 年全球機會分析和產業預測 2024-2032 年伺服馬達和驅動器市場報告(按產品類型、電壓範圍、系統、通訊協定、最終用途產業和地區分類)

2024-2032 年伺服馬達和驅動器市場報告(按產品類型、電壓範圍、系統、通訊協定、最終用途產業和地區分類) 模擬伺服馬達和驅動器市場 - 按驅動器、按應用(石油和天然氣、金屬切割和成型、物料搬運設備、機器人、醫療機器人、倉儲、自動化、半導體機械、AGV、電子)和預測,2024 年 - 2032 年

模擬伺服馬達和驅動器市場 - 按驅動器、按應用(石油和天然氣、金屬切割和成型、物料搬運設備、機器人、醫療機器人、倉儲、自動化、半導體機械、AGV、電子)和預測,2024 年 - 2032 年 數位伺服馬達和驅動器市場規模 - 按驅動器(交流驅動器、直流驅動器)、按應用(石油和天然氣、金屬切割和成型、物料搬運設備、包裝和標籤機械、機器人及其他)和預測,2023 - 2032 年

數位伺服馬達和驅動器市場規模 - 按驅動器(交流驅動器、直流驅動器)、按應用(石油和天然氣、金屬切割和成型、物料搬運設備、包裝和標籤機械、機器人及其他)和預測,2023 - 2032 年 伺服馬達及驅動器的全球市場:2018-2029年

伺服馬達及驅動器的全球市場:2018-2029年 伺服馬達和驅動器市場:按產品、標稱功率、最終用戶分類 - 2023-2030 年全球預測

伺服馬達和驅動器市場:按產品、標稱功率、最終用戶分類 - 2023-2030 年全球預測 RC 伺服市場報告:2030 年趨勢、預測與競爭分析

RC 伺服市場報告:2030 年趨勢、預測與競爭分析 2023-2030 年全球伺服電機和驅動器市場規模研究與預測(按類型、電壓範圍、最終用戶行業和區域分析)

2023-2030 年全球伺服電機和驅動器市場規模研究與預測(按類型、電壓範圍、最終用戶行業和區域分析) 伺服馬達和步進馬達的全球市場

伺服馬達和步進馬達的全球市場