|

市場調查報告書

商品編碼

1430558

全球實踐管理系統-市場佔有率分析、產業趨勢與統計、成長趨勢預測(2024-2029)Global Practice Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

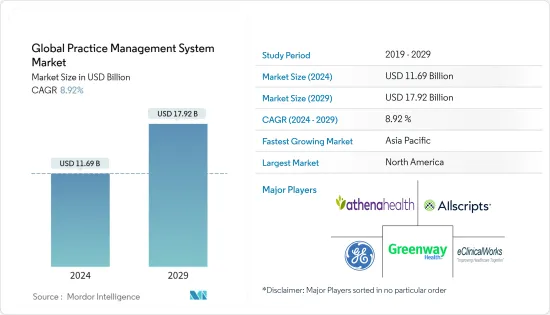

實踐管理系統的全球市場規模預計到 2024 年為 116.9 億美元,預計到 2029 年將達到 179.2 億美元,在預測期內(2024-2029 年)年複合成長率為 8.92%。

隨著感染 COVID-19 的患者數量迅速增加,預計 COVID-19 的爆發將對實踐管理系統市場產生重大影響,而這些解決方案預計將有助於治療過程中工作流程的順利進行。鑑於這種情況,許多主要參與者都在大流行期間推出了用於醫療保健系統管理的新產品。例如,2020 年 3 月,Innovaccer 推出了其 COVID-19 管理系統。該系統使醫療保健提供者能夠透過免費的遠端醫療服務和分析來評估大流行期間其診所和基層醫療診所的風險狀況和分流流入。因此,由於上述因素,預計所研究的市場將受到 COVID-19 的顯著影響。

實踐管理系統市場成長的關鍵促進因素包括提高目前診所和醫療保健組織效率的需求、長期時間和資源節省以及高投資收益。電子資料是醫療保健 IT 市場中一個快速新興的議題。自誕生以來,醫療保健行業由於記錄管理、合規性、監管要求和患者照護而產生了大量資料。一些研究人員和專家建議,透過更好地整合巨量資料,醫療保健每年可以為每個人節省大量金額。傳統上,醫生大部分時間都花在處理文書工作。

實踐管理系統增強了滿足關鍵監管要求的能力,確保醫生透過通知警報完成關鍵監管資料元素,並減少手動輸入詳細資訊所需的時間和資源。它變得越來越受歡迎,因為它增強了此外,這些系統還提供改進和更準確的申請處理和保險詳細資訊的警報,以及提前通知受益人以最大程度地減少申請拒絕。因此,從長遠來看,使用實踐管理軟體可以節省時間和資源,並成為市場成長的催化劑。

除此之外,高投資收益以及提高當前醫療實踐和機構效率的需求等其他因素預計也將在預測期內推動市場成長。然而,醫療保健領域缺乏熟練的 IT 專業人員、高昂的維護成本和安全成本預計將阻礙所研究的市場成長。

醫療實務管理系統(PMS)市場趨勢

雲端基礎的子區隔預計將在預測期內健康成長

實踐管理軟體等技術解決方案正在實現業務和方法的現代化,並改善醫療保健組織。雲端基礎的軟體系統有助於將資料儲存在外部伺服器上,並使其可以透過網路存取。實踐管理中雲端基礎的產品可協助醫療保健提供者實現日常醫療業務的自動化。實施雲端基礎的系統的成本低於本地系統,並且該軟體消除了內部維護的需要。

雲端基礎的實踐管理對於中小型實踐特別有用,因為沒有大量的硬體費用,而且軟體成本固定在較低的訂閱費下。雲端基礎的交付模型使軟體在可擴展性(計量收費儲存使用)方面具有高度彈性。簡化和整合儲存資源以降低成本、消除臨床資訊的部門孤島並增強工作流程。您組織的儲存和伺服器在外部部署。雲端供應商提供所有外部部署系統支援資源。雲端基礎設施還確保真正的災難復原和業務永續營運解決方案,以支援患者照護的品質。因此,雲端基礎的服務預計將繼續受到大量需求。

此外,WRS Health 於 2020 年 8 月推出了電子健康記錄泌尿系統 Cloud,使泌尿系統能夠管理他們的實踐並最大限度地提高效率和盈利的工作流程。此外,2021 年 7 月,經濟高效、雲端基礎的實踐解決方案的領先供應商 Practice EHR 宣布推出企業實踐管理解決方案 Practice EHR Enterprise。此軟體解決方案提供強大的功能來簡化醫療申請工作流程並提高醫院、診所和醫療申請公司的財務績效和生產力。

雲端基礎的實踐管理具有成本效益和時間效率,可供醫療保健相關人員使用,並提高患者滿意度。因此,由於對高效醫療實踐和醫療機構的需求不斷增加,預計該市場在預測期內將顯著成長。

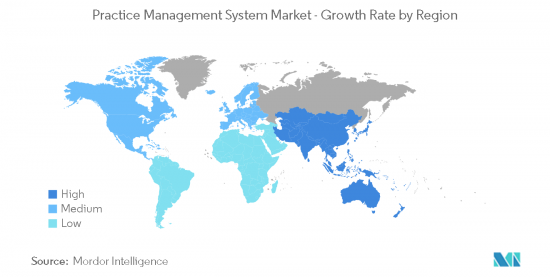

北美佔據主要佔有率,預計在預測期內將主導市場

由於擁有更好的醫療基礎設施和不斷增加的老年人口,預計北美將主導市場。美國的實踐管理可以幫助處理從醫療保健會計、申請、預訂和患者保險詳細資訊等各個方面。在美國,大多數實踐管理軟體系統都是為中小型醫療機構設計的。第三方醫療申請公司將一些實踐管理軟體用於醫療機構。實踐管理軟體通常用於醫療機構和醫療保健提供者的行政和財務事務。政府的資金支持可能會加速醫療保健提供者採用實踐管理,並改變整個行業的運作方式。因此,預計在預測期內,北美醫療保健支付者將擴大採用以患者為中心的方法,需要提高當前醫療實踐和機構的效率,長期節省時間和資源,以及高投資收益調查期間推動市場發展的主要因素是:

此外,政府的資助可能會加速醫療保健提供者採用實踐管理,並改變公司在該領域的運作方式。實踐管理的實施在大多數醫院和州一級都很普遍。醫療保健技術 SaaS 公司 Brevium 於 2021 年 1 月宣布,已擴大其軟體與美國領先的電子實踐管理系統 Nextech 的整合。

此外,醫療保健投資的增加以及醫療保健行業最終用戶對巨量資料分析的快速採用也有望推動該地區的市場成長。根據美國醫療保險和醫療補助服務中心的《2020年國民健康支出資料》,2020年醫療保健支出成長高達9.7%,達到4.1兆美元,約佔國內生產總值的19.7%。預計到 2028 年將達到 6.2 兆美元。因此,上述因素預計將在預測期內推動該地區的市場成長。

實踐管理系統 (PMS) 產業概述

這個市場競爭中等,有各種規模的公司。實踐管理系統市場的一些市場參與者包括 Allscripts Healthcare Solutions Inc.、Athenahealth、CareCloud Corporation、eClinicalWorks、Advanced-Data Systems Corporation、GE Company (GE Healthcare)、Greenway Health LLC、McKesson Corporation、NextGen Healthcare Information Systems LLC等等。主要參與者正在透過收購和聯盟以及新產品發布等各種策略不斷發展,以確保其在全球市場的地位。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 需要提高當前醫療實踐和機構的效率

- 長期節省時間和資源

- 高投資收益

- 市場限制因素

- 醫療保健領域缺乏熟練的 IT 專業人員

- 維護和安全成本高

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔(市場規模)

- 依產品類型

- 獨立的實踐管理軟體

- 綜合實踐管理軟體

- 按成分

- 軟體

- 按服務

- 按規定型態

- 本地

- 雲端基礎

- 按最終用戶

- 藥局

- 診斷實驗室

- 醫院

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太地區

- 中東/非洲

- GCC

- 南非

- 其他中東/非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭形勢

- 公司簡介

- Advanced Data Systems Corporation

- Allscripts Healthcare Solutions Inc.

- Athenahealth

- CareCloud Corporation

- eClinicalWorks

- General Electric(GE Healthcare)

- Greenway Health LLC

- McKesson Corporation

- NextGen Healthcare Information Systems LLC

- Cerner Corporation(Oracle Corporation)

- EPIC Systems Corporation

- Medical Information Technology, Inc.(Meditech)

- Henry Schein(MicroMD)

- AdvantEdge Healthcare Solutions

- Accumedic Computer Systems, Inc.

第7章 市場機會及未來趨勢

The Global Practice Management System Market size is estimated at USD 11.69 billion in 2024, and is expected to reach USD 17.92 billion by 2029, growing at a CAGR of 8.92% during the forecast period (2024-2029).

The COVID-19 outbreak is expected to have a significant impact on the practice management system market as there is a huge surge in the COVID-19 infected patients and these solutions are expected to aid in the smooth workflow during the treatment process. Given this, most of the key players are involved in launching new products for the management of healthcare systems during the pandemic. For instance, in March 2020, Innovaccer launched COVID-19 Management System, which enables providers with free telehealth services and analytics to assess risk profiles and triage the influx at medical practices and primary care clinics during the pandemic. Thus, owing to the aforementioned factors, the studied market is expected to be significantly impacted due to COVID-19.

The main drivers for the growth of the practice management systems market include the need to increase the efficiency of current medical practices and institutions, saving time and resources in the long term, and high return on investment. Electronic data is a rapidly emerging topic in the healthcare IT market. Since its inception, the healthcare industry has generated large amounts of data driven by record keeping, compliance and regulatory requirements, and patient care. Several researchers and experts have suggested that by better integrating big data, healthcare can save a huge amount of money for everyone every year. Traditionally, doctors spend most of their time handling paperwork.

Medical practice management systems are becoming increasingly popular, as they enhance the ability to meet important regulatory requirements and ensure the completion of key regulatory data elements by the physician just with a notification alert, along with enhancing the ability to reduce time and resources needed for entry of details, manually. Additionally, these systems also provide improved and more accurate billing procedures and insurance details, and alerts for obtaining advance beneficiary notice that minimizes claim denials. Hence, the usage of medical practice management software saves time and resources in the long run, which acts as a driver for the market's growth. hence, the launch of new softwares in the market is expeted to drive the studied market during study period.

Along with this, other factors, such as high return on investments and the need to increase the efficiency of current medical practices and institutions, are likely to boost the market growth over the forecast period. However, the lack of skilled IT professionals in Healthcare, along with high maintenance and security cost is expected to hinder the studied market growth.

Practice Management Systems (PMS) Market Trends

The Cloud-Based Sub-segment in Mode of Delivery Segment is Expected to Witness a Healthy Growth Over the Forecast period

Modernization of operations and approaches in medical practice, by utilization of technological solutions, such as medical practice management software, has improved healthcare organizations. Cloud-based software systems help in storing the data on external servers, making it accessible via the web, as it requires only a computer with an internet connection to access the data. Cloud-based delivery in medical practice management helps healthcare providers to automate day-to-day medical tasks. The installation cost for Cloud-based systems is lower than the on-premises systems and this software eradicates the need for in-house maintenance, which is expected to be the prime factor driving their increasing demand.

Cloud-based medical practice management is particularly useful for small- to medium-sized practices since there are no large hardware expenditures, and the software expense is consistent with a low subscription rate. The cloud-based delivery model makes the software extremely flexible, regarding scalability (pay-as-you-go storage utilization). It simplifies and consolidates storage resources to reduce costs and enhance workflow, by eliminating departmental silos of clinical information. The storage and server power for the organization are hosted off-premise. The cloud vendor provides all the off-premise system support resources. The cloud infrastructure also guarantees true disaster recovery and business continuity solutions, to support the quality of patient care. Hence, cloud-based services are expected to continue to witness a significant demand.

Additionally, in August 2020, the Urology cloud, an Electronic Health Record, was launched by WRS Health, which enables Urologists to manage their practice and maximize their workflows efficiently and profitably. Moreover, in July 2021, Practice EHR, a leading provider of cost-effective, cloud-based medical practice solutions, announced the launch of its enterprise practice management solution, Practice EHR Enterprise. The software solution provides robust functionality that streamlines the medical billing workflow and improves financial performance and productivity for hospitals, medical practices, and medical billing companies.

Cloud-based medical practice management is cost and time-effective and improves patient satisfaction, as it is accessible to medical professionals. Hence, with an increasing need for efficient medical practices and institutions, the market studied is expected to witness significant growth during the forecast period.

North America Holds the Major Share and is Expected to Dominate the Market Over the Forecast Period

North America is expected to dominate the market owing to the presence of better healthcare infrastructure and a rising geriatric population. Medical practice management in the United States helps in every aspect of healthcare accounts, billing, appointments, and insurance details of the patients. In the United States, most of medical practice management software systems are designed for small to medium-sized medical facilities. Some of the medical practice management software is used by third-party medical billing companies for healthcare facilities. Medical practice management software is often used for administrative and financial matters of medical care facilities and providers. Government funding is likely to speed up the adoption of medical practice management by healthcare providers and change the way players operate, across the sector. Hence, the increasing adoption of a patient-centric approach by healthcare payers, the need to increase the efficiency of current medical practices and institutions, time and resource saving in the long run, and high return on investments are the major factors driving the market studied during the forecast period in the North American region.

Additionally, government funding is likely to speed up the adoption of medical practice management by healthcare providers and change the way players operate across the sector. Medical practice management adoption is widespread across most hospitals and at the state level. Brevium, a SaaS company in the healthcare technology sector, announced that it extended the integration of its software with one of the premier electronic practice management systems in the United States, Nextech, on January 2021.

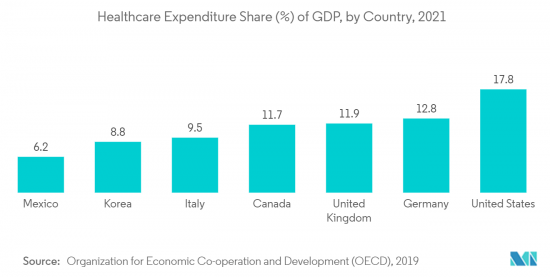

Furthermore, the rising healthcare investment and the surge in adoption of big data analytics among end-users in the healthcare industry will also be expected to boost the market growth in the region. According to the United States Centers for Medicare & Medicaid Services National Health Expenditure Data 2020, the healthcare expenditure grew by up to 9.7% to USD 4.1 trillion in 2020 and accounted for around 19.7% of the gross domestic product. The expenditure is projected to reach USD 6.2 trillion by 2028. Thus, the aforementioned factors are expected to drive the market growth in the region over the forecast period.

Practice Management Systems (PMS) Industry Overview

The market studied is a moderately competitive market owing to the presence of many small and large market players. Some of the market players of the practice management system market are Allscripts Healthcare Solutions Inc., Athenahealth, CareCloud Corporation, eClinicalWorks, Advanced-Data Systems Corporation, GE Company (GE Healthcare), Greenway Health LLC, McKesson Corporation, and NextGen Healthcare Informations Systems LLC among others. the major players are evolving through various strategies such as acquisitions and collaborations, along with new product launches to secure the position in the global market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need to Increase Efficiency of Current Medical Practices and Institutions

- 4.2.2 Time and Resources Saving in the Longer Run

- 4.2.3 High Return on Investments

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled IT Professionals in Healthcare

- 4.3.2 High Maintenance and Security Cost

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - in USD Million)

- 5.1 By Product Type

- 5.1.1 Stand-alone Practice Management Software

- 5.1.2 Integrated Practice Management Software

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Mode of Delivery

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.4 By End User

- 5.4.1 Pharmacies

- 5.4.2 Diagnostic Laboratories

- 5.4.3 Hospitals

- 5.4.4 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Advanced Data Systems Corporation

- 6.1.2 Allscripts Healthcare Solutions Inc.

- 6.1.3 Athenahealth

- 6.1.4 CareCloud Corporation

- 6.1.5 eClinicalWorks

- 6.1.6 General Electric (GE Healthcare)

- 6.1.7 Greenway Health LLC

- 6.1.8 McKesson Corporation

- 6.1.9 NextGen Healthcare Information Systems LLC

- 6.1.10 Cerner Corporation (Oracle Corporation)

- 6.1.11 EPIC Systems Corporation

- 6.1.12 Medical Information Technology, Inc. (Meditech)

- 6.1.13 Henry Schein (MicroMD)

- 6.1.14 AdvantEdge Healthcare Solutions

- 6.1.15 Accumedic Computer Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

醫療保健管理系統的全球市場規模、佔有率和成長分析(按組成部分、提供型態和最終用戶)-產業預測,2024-2031 年

醫療保健管理系統的全球市場規模、佔有率和成長分析(按組成部分、提供型態和最終用戶)-產業預測,2024-2031 年 2024 年實踐管理系統全球市場報告

2024 年實踐管理系統全球市場報告 美國實踐管理系統市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按產品、組件、交付模式、應用程式以及最終用戶和國家/地區

美國實踐管理系統市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按產品、組件、交付模式、應用程式以及最終用戶和國家/地區 全球實踐管理系統市場研究報告 - 2023 年至 2030 年產業分析、規模、佔有率、成長、趨勢和預測

全球實踐管理系統市場研究報告 - 2023 年至 2030 年產業分析、規模、佔有率、成長、趨勢和預測 實踐管理系統市場:2023-2028 年全球行業趨勢、佔有率、規模、成長、機遇和預測

實踐管理系統市場:2023-2028 年全球行業趨勢、佔有率、規模、成長、機遇和預測 實踐管理系統市場規模 - 按類型(整合、獨立)、元件(軟體、服務)、交付模式(基於 Web/雲端、本地)、最終用途和全球預測,2023 年至 2032 年

實踐管理系統市場規模 - 按類型(整合、獨立)、元件(軟體、服務)、交付模式(基於 Web/雲端、本地)、最終用途和全球預測,2023 年至 2032 年 全球實踐管理系統市場

全球實踐管理系統市場 醫師實踐管理全球市場洞察,預測到 2028 年

醫師實踐管理全球市場洞察,預測到 2028 年