|

市場調查報告書

商品編碼

1429237

乙二醇醚:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Glycol Ethers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

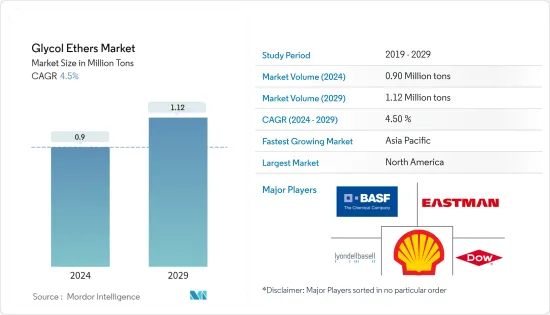

乙二醇醚市場規模預計到2024年為90萬噸,預計到2029年將達到112萬噸,在預測期內(2024-2029年)複合年成長率為4.5%。

COVID-19的爆發、世界各地的封鎖、製造活動和供應鏈的中斷以及生產停頓對2020年的市場產生了負面影響。然而,到了2021年,情況開始好轉,市場恢復了成長軌跡。

主要亮點

- 推動市場成長的主要因素是化妝品和個人保健產品使用量的增加以及油漆和塗料行業需求的增加。

- 另一方面,REACH 和 EPA 關於乙二醇醚使用的法規以及用作清洗產品溶劑的新產品的出現正在限制市場成長。

- 意識的提高導致對低排放氣體柴油燃料的 P 系列乙二醇的需求過剩,可能會在預測期內為同一市場提供機會。

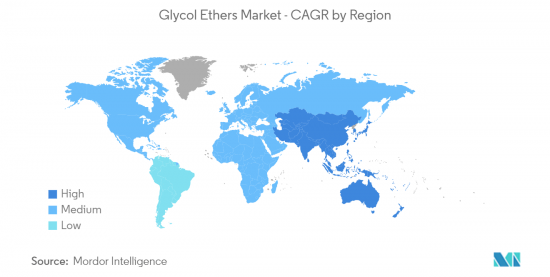

- 北美是全球乙二醇醚市場的關鍵地區,而亞太地區預計在預測期內將以最快的速度成長。

乙二醇醚市場趨勢

油漆和塗料領域佔據市場主導地位

- 乙二醇醚有助於在油漆固化時形成適當的薄膜,並充當樹脂的活性溶劑。有助於最佳化塗料中溶劑的蒸發速率。它還有助於改善油漆徑流特性並消除塗漆時的刷痕。

- 塗料工業是乙二醇醚的最大消費者。油漆和被覆劑廣泛應用於建築、汽車和包裝等多種行業。

- 油漆和塗料市場的許多公司採取了多種商務策略來維持其在全球市場的地位。例如,2022 年 2 月,宣偉公司收購了 AquaSurTech,這是一家為建築應用生產耐用塗料的公司。這加強了公司在建築產品市場塗料行業的地位。

- 同樣,2022 年 6 月,宣偉公司收購了德國領先的曳引機塗料公司 Gross &Perthun GmbH。透過此次收購,宣偉公司鞏固了其在高性能塗料行業的地位。

- 世界各地住宅和商業建築的建設大幅增加,推動了對建築油漆和被覆劑中使用的乙二醇醚的需求。

- 根據印度品牌資產基金會(IBEF)預測,到 2025 年,印度預計每年建造 1,150 萬套住宅,成為第三大建築市場,價值約 1 兆美元。此外,到2023年,美國和中國預計將佔全球建築業成長的60%。因此,對油漆和被覆劑的需求預計將增加,從而導致對乙二醇醚的需求增加。

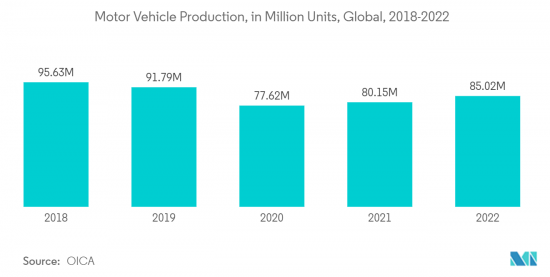

- 此外,全球汽車產量的成長預計將推動油漆和被覆劑的需求。例如,根據OICA的數據,2022年全球汽車產量為85,016,728輛,較2021年成長6%。

- 因此,上述趨勢可能會增加油漆和塗料市場的需求和產量,這可能會進一步推動對乙二醇醚等原料的需求。

亞太地區是成長最快的市場

- 由於中國、印度和日本等主要國家的存在,亞太地區是全球乙二醇醚市場成長最快的地區。

- 汽車、建築、電子和包裝等最終用戶行業對油漆、被覆劑和黏劑等產品的需求正在迅速成長。

- 中國汽車工業產量大幅成長。例如,根據國際汽車組織(OICA)的數據,2022年中國汽車總產量為27,020,615輛,較2021年成長3%。

- 此外,隨著消費者越來越喜歡電動車,該國的轉換趨勢也處於高水準。此外,中國政府預計2025年電動車普及將達20%。這反映在該國的電動車銷售趨勢上,2022年電動車銷量創下歷史新高。根據中國小客車協會的數據,2022年電動車和插電式混合動力車銷量為567萬輛,幾乎是2021年的兩倍。

- 由於西方文化的影響以及年輕人對化妝品需求的增加,該地區對化妝品和個人保健產品的需求正在以驚人的速度成長。同時,市場相關人員不斷加大投資和生產,拉動對含乙二醇醚原料的需求。

- 印度、韓國和東南亞國協的製藥業正在進行大量外國投資,以開拓市場機會,這可能會增加預測期內該地區對乙二醇醚的需求。

- 中國的製藥業是世界上最大的製藥業之一。該國涉及學名藥、治療藥物、原料藥和草藥的生產。

- 因此,這種有利的市場趨勢預計將在預測期內推動該地區乙二醇醚市場的成長。

乙二醇醚產業概況

乙二醇醚市場較為分散,眾多參與者各自持有的市場佔有率不足以影響市場動態。該市場的一些知名參與者包括BASF股份公司、伊士曼化學公司、利安德巴塞爾工業控股公司、殼牌和陶氏化學公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 擴大在化妝品和個人保健產品中使用

- 加速在油漆和塗料行業的應用

- 其他司機

- 抑制因素

- REACH 和 EPA 關於乙二醇醚使用的規定

- 用作清洗產品溶劑的新產品的出現

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 類型

- E系列

- 乙二醇甲醚

- 乙二醇乙醚

- 乙二醇丁醚

- P系列

- 丙二醇單甲醚 (PM)

- 二丙二醇單甲醚 (DPM)

- 三丙二醇單甲醚 (TPM)

- 其他丙二醇醚

- E系列

- 目的

- 溶劑

- 防凍劑

- 液壓/煞車油

- 化學中間體

- 最終用戶產業

- 畫

- 印刷

- 藥品

- 化妝品/個人護理

- 黏劑

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率**/排名分析

- 主要企業策略

- 公司簡介

- BASF SE

- Dow

- Eastman Chemical Company

- FBC Chemical

- India Glycols Ltd

- Ineos Group Limited

- Kemipex

- KH Neochem Co. Ltd

- LyondellBasell Industries Holdings BV

- Nippon Nyukazai Co. Ltd

- Oxiteno

- Recochem, Inc.(HIG Capital)

- Shell

- Sasol Limited

第7章 市場機會及未來趨勢

- 意識不斷增強,導致對用於低排放氣體燃料的 P 系列乙二醇的需求過剩

- 其他機會

The Glycol Ethers Market size is estimated at 0.9 Million tons in 2024, and is expected to reach 1.12 Million tons by 2029, growing at a CAGR of 4.5% during the forecast period (2024-2029).

The COVID-19 outbreak, nationwide lockdowns around the world, disruption in manufacturing activities and supply chains, and production halts negatively impacted the market in 2020. However, the conditions started recovering in 2021, thereby restoring the growth trajectory of the market.

Key Highlights

- The major factors driving the growth of the market studied are the increasing usage of cosmetics and personal care products and accelerating demand in the paints and coatings industry.

- On the flip side, REACH and EPA regulations regarding the usage of glycol ethers, and the emergence of new products to use as a solvent for cleaning agents are restraining the growth of the market studied.

- The growing awareness leading to excess demand for P-series glycol for low emission oxygenated diesel fuel, is likely to provide opportunities for the market studied, during the forecast period.

- North America is the dominating region in the global glycol ethers market and Asia-Pacific is expected to grow at a fastest rate during the forecast period.

Glycol Ethers Market Trends

Paints and Coatings Segment to Dominate the Market

- Glycol ether helps in the formation of a proper film during coating cure and acts as an active solvent in resins. It helps in optimizing the evaporation rate of the solvent in a coating. It is also helpful in improving the flow out characteristics of the paint, and in eliminating brush marks during painting.

- The paints and coatings industry is the largest consumer of glycol ethers. Paints and coatings are extensively used in various industries, such as construction, automotive, and packaging.

- Many companies in paints and coatings market are adopting several business strategies in order to maintain their position in the global market. For instance, in February 2022, The Sherwin-Williams Company has acquired AquaSurTech, a producer of durable coatings for building applications. This helped the company to strengthen its position in coating industry for the building products market.

- Similarly, in June 2022, The Sherwin-Williams Company has acquited Gross & PerthunGmbH, a Germany based leading tracter coating company. This acquisition has helped the company to stregthen its position high-performance coatings industry.

- Residential and commercial construction has been increasing significantly across the world, which is driving the demand for glycol ethers, for their application in the production of architectural paints and coatings.

- According to the Indian Brand Equity Foundation (IBEF), by 2025, India is expected build 11.5 million homes a year and become third largest construction market with a value of around USD 1 trillion. Furthermore, by 2023, United States and China are expected to account for 60 per cent of the global growth in the construction sector. This is expected to incraese the demand for paints and coatings, in turn boosting the demand for glycol ethers.

- Furthermore, the global growth in automotive production is expected to propel the demand for paints and coatings. For instance, according to OICA, in 2022, the world motor vehicle production accounted for 85,016,728 units which was increased by 6% compared to 2021.

- Hence, the aforementioned trends are likely to increase the demand and production in the paints and coatings market, which may further drive the demand for raw materials, like glycol ethers.

Asia-Pacific is the Fastest Growing Market

- The Asia-Pacific the fastest growing region in the global glycol ethers market owing to the presence of significant countries such as China, India, and Japan.

- The surge in demand for products, such as paints, coatings, and adhesives, has been increasing in the end-user industries, such as automotive, construction, electronics, and packaging.

- The automobile industry in the China is witnessing a significant growth in terms of productions. For instance, according to International Organization of Motor Vehicles (OICA), in 2022, total production of motor vehicles in China accounted for 27,020,615 units which was increased by 3% compared to 2021.

- Further, switching trends in the country as the consumer are more inclined toward battery-operated vehicles is on the higher side. Moreover, the government of China estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the electric vehicle sales trend in the country, which went record-breaking high in 2022. As per the China Passenger Car Association, the country sold 5.67 million units of EVs and plug-ins in 2022, touching almost double the sales figures achieved in 2021.

- Cosmetics and personal care products demand is increasing at a noticeable rate in the region, owing to the influence of western culture and increased cosmetic demand from the youth population. With this, the market players are increasing investments and production, thereby driving the demand for raw materials, including glycol ethers.

- The pharmaceutical industry in India, South Korea, and ASEAN countries are witnessing huge investments from foreign countries, in order to exploit the market opportunities, which may increase the demand for glycol ethers in the region, during the forecast period.

- The pharmaceutical industry in China is one of the largest in the world. The country is involved in the production of generics, therapeutic medicines, active pharmaceutical ingredients, and traditional Chinese medicine.

- Hence, such favorable market trends are likely to drive the growth of the glycol ethers market in the region, during the forecast period.

Glycol Ethers Industry Overview

The glycol ethers market is fragmented, with numerous players holding insignificant market share to affect the market dynamics individually. Some of the noticeable players in the market include BASF SE, Eastman Chemicals Company, LyondellBasell Industries Holdings B.V., Shell, and Dow, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use in Cosmetics and Personal Care Products

- 4.1.2 Accelerating Use in Paints and Coatings Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 REACH and EPA Regulations Regarding the Use of Glycol Ether

- 4.2.2 Emergence of New Products to Use as a Solvent for Cleaning Agents

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 E-series

- 5.1.1.1 Methyl Glycol Ether

- 5.1.1.2 Ethyl Glycol Ether

- 5.1.1.3 Butyl Glycol Ether

- 5.1.2 P-series

- 5.1.2.1 Propylene Glycol Monomethyl Ether (PM)

- 5.1.2.2 Dipropylene Glycol Monomethyl Ether (DPM)

- 5.1.2.3 Tripropylene Glycol Monomethyl Ether (TPM)

- 5.1.2.4 Other Propylene Glycol Ethers

- 5.1.1 E-series

- 5.2 Application

- 5.2.1 Solvent

- 5.2.2 Anti-Icing Agent

- 5.2.3 Hydraulic and Brake Fluid

- 5.2.4 Chemical Intermediate

- 5.3 End-user Industry

- 5.3.1 Paints and Coatings

- 5.3.2 Printing

- 5.3.3 Pharmaceuticals

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Adhesives

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Dow

- 6.4.3 Eastman Chemical Company

- 6.4.4 FBC Chemical

- 6.4.5 India Glycols Ltd

- 6.4.6 Ineos Group Limited

- 6.4.7 Kemipex

- 6.4.8 KH Neochem Co. Ltd

- 6.4.9 LyondellBasell Industries Holdings B.V.

- 6.4.10 Nippon Nyukazai Co. Ltd

- 6.4.11 Oxiteno

- 6.4.12 Recochem, Inc. (H.I.G. Capital)

- 6.4.13 Shell

- 6.4.14 Sasol Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Awareness Leading to Excess Demand for P-series Glycol for Low Emission Oxygenated Diesel Fuel

- 7.2 Other Opportunities