|

市場調查報告書

商品編碼

1408869

黃金:市場佔有率分析、行業趨勢和統計數據、2024年至2029年的成長預測Gold - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

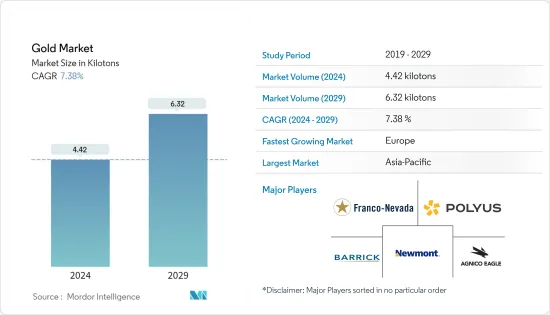

2024 年黃金市場規模預計為 4.42 噸,預計 2029 年將達到 6.32 噸,在預測期內(2024-2029 年)複合年成長率為 7.38%。

2020 年,COVID-19 大流行對多個產業產生了負面影響。大多數地區的封鎖擾亂了採礦和加工活動,對貨物運輸的限制擾亂了供應鏈。然而,到了2021年,情況開始好轉,市場恢復了成長軌跡。

推動市場的主要因素是珠寶飾品、技術和長期儲蓄等形式的黃金需求。在開發中國家尤其如此,黃金經常被用作奢侈品和維持財富的手段。

然而,礦石變質、技術課題和罷工等因素預計將阻礙全球黃金市場的擴張。

然而,預計中國和印度的婚禮市場將在未來幾年為黃金市場提供一些成長機會。

亞太地區在全球市場中佔據主導地位,其中消費量最高的國家來自中國和印度等國家,並且預計這種情況將持續下去。

黃金市場趨勢

珠寶飾品領域主導需求

- 黃金有多種用途,包括珠寶飾品、電子產品、硬幣、獎牌、美術、牙科、醫學和貨幣系統。金的導電性、耐腐蝕、生物相容性和延展性等特性使其適合這些應用。某些醫學問題,如癌症和關節炎,也可以使用放射性同位素和金鹽來治療。

- 透過鑽探、爆破或刮削周圍的岩石,從礦脈礦床中提取黃金。礦脈通常發現於地下深處。礦工透過沿著礦脈在地下挖掘隧道來挖掘礦物。然後,技術人員使用鎬和小型炸藥從周圍的岩石中提取金礦石。

- 通常,在堆浸之前,金礦石被碾碎並結塊。需要進一步加工從高等級礦石和粗粒且耐氰化浸出的礦石中提取金含量。在氰化物浸出前採用破碎、濃縮、焙燒、加壓氧化等加工方法。

- 在預測期內,珠寶飾品業可能佔據黃金市場的最大佔有率。黃金不會失去光澤、生鏽或腐蝕。由於其優異的性能和光澤,它是珠寶飾品製造中最重要的金屬。黃金太軟,不適合日常使用,因此它與金屬組合形成合金,使其更耐用,因此可以用於珠寶。

- 許多其他類型的黃金也用於珠寶的生產。黃金有多種顏色、克拉數和鍍層,每種都有其獨特的品質。市場上大約有15種黃金,包括黃金、白金和玫瑰金。

- 此外,根據世界黃金協會的數據,2022 年第三季珠寶用黃金需求預計為 581.7 噸。這是本季最受歡迎的目標,領先於投資、科技和央行。

- 總體而言,在預測期內,珠寶飾品需求可能會繼續在推動全球黃金市場需求方面發揮重要作用。

亞太地區主導市場

- 亞太地區是最大的黃金生產國之一,以中國和澳洲為首。中國擁有最大的市場佔有率,也是預測期內最大的黃金用戶。

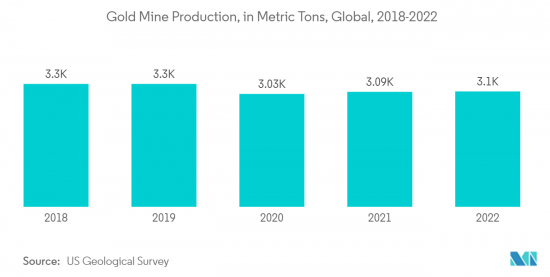

- 根據美國地質調查局的數據,2022年中國金礦的黃金產量位居亞太地區之首。澳洲、烏茲別克和印尼是該地區其他最大生產國,2022 年開採量分別為 320 噸、100 噸和 70 噸。

- 根據世界黃金協會的數據,隨著山東省的採礦業在 2021 年大部分時間的安全停工後恢復正常,中國的礦場產量在 2022 年增加了 13%,達到 374 噸。

- 從地區來看,在中國產量復甦的推動下,2022年亞太地區礦山產量增幅最大,較2021年增加11噸。

- 2022年黃金回收市場將由印度主導,回收供應量快速增加。在以印度為最大市場的南亞地區,回收供應量較去年同期成長近40%,較上季成長約60%。

- 此外,與2022年(55天)相比,2023年吉祥結婚日的數量將增加(67天),這將刺激黃金首飾的需求。

- 在金融界,黃金是最受歡迎的貴金屬。根據世界黃金協會的數據,從1971年1月到2022年12月,黃金的平均年回報率為7.78%,落後於商品的平均年回報率8.3%。 2002 年至 2022 年期間,黃金投資收益波動較大,但在大多數研究年份中都產生了正收益。 2022年,黃金投資報酬率約為0.44%。由於許多人希望投資黃金以對沖股市,因此對黃金的需求可能會增加。

- 因此,上述所有因素預計將在預測期內推動亞太地區黃金市場的需求。

黃金產業概況

黃金市場部分分散,市場上只有少數大型參與者和許多小型參與者。研究市場的主要企業(排名不分先後)包括紐蒙特公司、巴里克黃金公司、FRANCO-NEVADA CORPORATION、PJSC Polyus、Agnico Eagle Mines Limited 等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 珠寶飾品的黃金需求和長期儲蓄

- 高階電子應用的消耗增加

- 其他司機

- 抑制因素

- 礦石品位下降和其他技術課題

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模)

- 依類型

- 合金金

- 分層金

- 依用途

- 珠寶飾品

- 電子產品

- 獎項和地位的象徵

- 其他應用(牙科、航太等)

- 地區

- 生產分析

- 美國

- 澳洲

- 巴西

- 布吉納法索

- 加拿大

- 中國

- 哥倫比亞

- 迦納

- 印尼

- 哈薩克

- 馬裡

- 墨西哥

- 巴布亞紐幾內亞

- 秘魯

- 俄羅斯

- 南非

- 蘇丹

- 坦尚尼亞

- 烏茲別克

- 其他國家

- 消費分析

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 生產分析

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Agnico Eagle Mines Limited

- Barrick Gold Corporation

- FRANCO-NEVADA CORPORATION

- FURUKAWA CO.,LTD

- Gabriel Resources Ltd.

- Harmony Gold Mining Company Limited

- Jinshan Gold

- Johnson Matthey

- Kinross Gold Corporation

- New Gold Inc.

- Newmont Corporation

- PJSC Polyus

- Tertiary Minerals

- Vedanta Resources Limited

- Zijin Mining Group

第7章 市場機會及未來趨勢

- 增加黃金投資增加外匯存底

- 其他機會

The Gold Market size is estimated at 4.42 kilotons in 2024, and is expected to reach 6.32 kilotons by 2029, growing at a CAGR of 7.38% during the forecast period (2024-2029).

The COVID-19 pandemic affected several industries negatively in 2020. The lockdown in most regions caused disruptions in mining and processing activities, and restrictions in freight transportation disturbed the supply chain. However, the conditions started recovering in 2021, restoring the market's growth trajectory.

The major factor driving the market is the demand for gold in the form of jewelry, technology, and long-term savings. This is especially true in developing nations, where gold is frequently utilized as a luxury item and a way of preserving wealth.

However, factors like declining ore grades, technical challenges, and strikes are expected to hinder global gold market expansion.

Nevertheless, the wedding market sector in China and India is projected to give several growth opportunities for the gold market segment in the future.

The Asia-Pacific region dominated the market globally, with the largest consumption coming from countries such as China and India, and this is expected to remain the same in the future.

Gold Market Trends

Jewelry Segment to Dominate the Demand

- Gold is used in a variety of applications, including jewelry, electronics, coins, medals, art, dentistry, medicine, and monetary systems. Gold is suitable for these applications due to properties such as conductivity, corrosion resistance, biocompatibility, and malleability. Certain medical problems, such as cancer and arthritis, can also be treated with gold by adopting radioactive isotopes or gold salts.

- Gold is extracted from lode deposits by drilling, blasting, or shoveling the surrounding rock. Lode deposits are typically found deep underground. Miners mine underground by digging tunnels through the earth following the vein. Technicians then use picks and tiny explosives to extract the gold ore from the surrounding rock.

- Typically, before heap leaching, the gold ore is crushed and agglomerated. Further processing is required to extract the gold contents from high-grade ores and ores resistant to cyanide leaching at coarse particle sizes. Before cyanidation, processing methods such as grinding, concentration, roasting, and pressure oxidation may be used.

- During the forecast period, the jewelry sector is likely to have the largest share of the gold market. Gold does not tarnish, rust, or corrode. It is the most significant metal in jewelry manufacturing due to its excellent features and shine. Since gold is too soft for everyday usage, it is alloyed with a metal combination to make it tougher so that it may be used for jewelry.

- Numerous other varieties of gold are used to produce the jewelry. Gold is available in a variety of hues, karats, and coatings, each with its own set of qualities. On the market, there are around 15 distinct varieties of gold available, including yellow gold, white gold, rose gold, and others.

- Moreover, according to the WGC, in the third quarter of 2022, the demand for gold for jewelry applications was estimated to be 581.7 metric tons. This was the most popular purpose in that quarter, ahead of investment, technology, and central banks.

- Overall, the gold jewelry demand is likely to continue playing an instrumental role in driving the global demand for the gold market over the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is one of the largest producers of gold, driven by China and Australia. China has the biggest market share and will also be the top gold user over the forecast period.

- According to the U.S. Geological Survey, in 2022, gold mines in China produced the most gold in the Asia-Pacific region. Australia, Uzbekistan, and Indonesia were the other top producers in the region, with 320 metric tons, 100 metric tons, and 70 metric tons mined in 2022, respectively.

- According to the World Gold Council, mine production in China increased by 13% in 2022 to 374 tons as mining in Shandong province returned to normal, following the widespread safety stoppages for most of 2021.

- Region-wise, mine production in Asia-Pacific saw the largest increase in 2022, up by 11 tons compared to 2021, driven by the recovery in China's output.

- India led the gold recycling market in 2022, with sharp increases in recycling supply. The South Asian region, with India being the biggest market, saw recycling supply up nearly 40% year-on-year and about 60% quarter-on-quarter.

- A higher number of auspicious wedding days in the country in 2023 (67 days) as compared to 2022 (55 days) will also add to the demand for gold jewelry.

- In the financial world, gold is the most popular precious metal. According to the WGC, from January 1971 and December 2022, gold had an average annual return of 7.78%, trailing only commodities, which had an average annual return of 8.3%. The rate of return on gold investments varied greatly from 2002 to 2022 but provided positive returns in the majority of the years studied. In 2022, the return on gold as an investment was around 0.44%. Many people are looking to invest in gold as a hedge against equity markets, which will increase its demand.

- Therefore, all such factors mentioned above are projected to contribute to driving demand for the gold market in the Asia-Pacific region over the forecast period.

Gold Industry Overview

The gold market is partially fragmented, with the presence of a few large-sized players and a large number of small players operating in the market. The major players in the studied market (not in any particular order) include Newmont Corporation, Barrick Gold Corporation, FRANCO-NEVADA CORPORATION, PJSC Polyus, and Agnico Eagle Mines Limited, amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Demand for Gold in the form of Jewelry and Long-term Savings

- 4.1.2 Increasing Consumption in High-End Electronics Applications

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Declining Ore Grades and Other Technical Challenges

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Alloyed Gold

- 5.1.2 Layered Gold

- 5.2 Application

- 5.2.1 Jewellery

- 5.2.2 Electronics

- 5.2.3 Awards and Status Symbols

- 5.2.4 Other Applications (Dentistry, Aerospace, etc.)

- 5.3 Geography

- 5.3.1 Production Analysis

- 5.3.1.1 United States

- 5.3.1.2 Australia

- 5.3.1.3 Brazil

- 5.3.1.4 Burkina Faso

- 5.3.1.5 Canada

- 5.3.1.6 China

- 5.3.1.7 Colombia

- 5.3.1.8 Ghana

- 5.3.1.9 Indonesia

- 5.3.1.10 Kazakhstan

- 5.3.1.11 Mali

- 5.3.1.12 Mexico

- 5.3.1.13 Papua New Guinea

- 5.3.1.14 Peru

- 5.3.1.15 Russia

- 5.3.1.16 South Africa

- 5.3.1.17 Sudan

- 5.3.1.18 Tanzania

- 5.3.1.19 Uzbekistan

- 5.3.1.20 Other countries

- 5.3.2 Consumption Analysis

- 5.3.2.1 Asia-Pacific

- 5.3.2.1.1 China

- 5.3.2.1.2 India

- 5.3.2.1.3 Japan

- 5.3.2.1.4 South Korea

- 5.3.2.1.5 Rest of Asia-Pacific

- 5.3.2.2 North America

- 5.3.2.2.1 United States

- 5.3.2.2.2 Canada

- 5.3.2.2.3 Mexico

- 5.3.2.3 Europe

- 5.3.2.3.1 Germany

- 5.3.2.3.2 United Kingdom

- 5.3.2.3.3 Italy

- 5.3.2.3.4 France

- 5.3.2.3.5 Rest of Europe

- 5.3.2.4 South America

- 5.3.2.4.1 Brazil

- 5.3.2.4.2 Argentina

- 5.3.2.4.3 Rest of South America

- 5.3.2.5 Middle East and Africa

- 5.3.2.5.1 Saudi Arabia

- 5.3.2.5.2 South Africa

- 5.3.2.5.3 Rest of Middle East and Africa

- 5.3.1 Production Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Agnico Eagle Mines Limited

- 6.4.2 Barrick Gold Corporation

- 6.4.3 FRANCO-NEVADA CORPORATION

- 6.4.4 FURUKAWA CO.,LTD

- 6.4.5 Gabriel Resources Ltd.

- 6.4.6 Harmony Gold Mining Company Limited

- 6.4.7 Jinshan Gold

- 6.4.8 Johnson Matthey

- 6.4.9 Kinross Gold Corporation

- 6.4.10 New Gold Inc.

- 6.4.11 Newmont Corporation

- 6.4.12 PJSC Polyus

- 6.4.13 Tertiary Minerals

- 6.4.14 Vedanta Resources Limited

- 6.4.15 Zijin Mining Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Investment in Gold to Increase the Forex Reserves

- 7.2 Other Opportunities

全球特種金屬和礦物市場 - 2024-2031

全球特種金屬和礦物市場 - 2024-2031 2024 年金屬世界市場報告

2024 年金屬世界市場報告 2024 年金屬合金世界市場報告

2024 年金屬合金世界市場報告 2024 年金屬與礦物世界市場報告

2024 年金屬與礦物世界市場報告 2024-2032 年按產品類型、金屬類型、最終用途產業及地區分類的金屬及金屬製成品市場

2024-2032 年按產品類型、金屬類型、最終用途產業及地區分類的金屬及金屬製成品市場 2024 年建築與結構金屬全球市場報告

2024 年建築與結構金屬全球市場報告 金屬陽極氧化市場:2023年至2028年預測

金屬陽極氧化市場:2023年至2028年預測 全球食用黃金市場:按類型、純度等級、應用、最終用途產業、分銷管道和地區劃分的評估、機會和預測(2016-2030)

全球食用黃金市場:按類型、純度等級、應用、最終用途產業、分銷管道和地區劃分的評估、機會和預測(2016-2030) 銥回收的全球市場:2018-2029年

銥回收的全球市場:2018-2029年 鉛冶煉和精煉市場 - 按熔爐、方法、按應用和預測,2023 - 2032 年

鉛冶煉和精煉市場 - 按熔爐、方法、按應用和預測,2023 - 2032 年