|

市場調查報告書

商品編碼

1408235

伺服器作業系統:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Server Operating System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

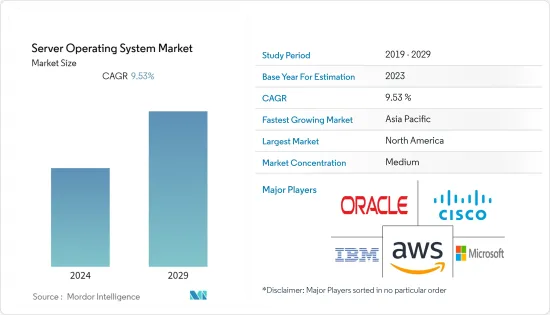

今年全球伺服器營運市場規模為190.7億美元。

預測期內複合年成長率為9.53%,預計到預測年末將達到306.9億美元。

主要亮點

- 該市場的成長歸因於公司在建立強大的資料中心基礎設施方面的支出。此外,混合雲端環境的日益採用和 5G 網路技術的引入正在推動市場成長。此外,技術進步和基礎設施安全要求的提高預計將在預測期內為市場提供有利的擴張機會。

- 許多知名參與企業擴大採用雲端平台和基礎設施,以及增加對資料中心基礎設施的投資,正在推動市場成長。目前先進的基礎設施發展預計將增加全球雲端伺服器用戶的數量。主要的雲端運算服務公司正在投入金額在全球擴展其雲端基礎設施。例如,考慮到雲端服務需求的不斷成長,2023年2月,甲骨文公司宣布了一項新的公共雲端計劃,將在沙烏地阿拉伯投資15億美元。

- 這些伺服器可用於智慧城市中的各種應用,包括為ITS(智慧型運輸系統)和V2X(車對萬物)通訊提供高效能、低延遲的服務,例如5G和AI應用。它還可用於託管公共運輸的雲端基礎的IP 語音 (VoIP)通訊系統,以及儲存和管理來自物聯網感測器和設備的資料。此外,高可用性伺服器還可以在智慧城市服務的安全和身份驗證過程中發揮作用。例如,許多智慧城市計劃和措施正在世界各地實施,促進了全球都市化投資。經合組織估計,2010 年至 2030 年間,智慧城市措施的國際投資將達到約 1.8 兆美元,涵蓋城市基礎建設計劃。這將為公司提供開發新版本作業系統以獲得市場佔有率的機會。

- 為了增加市場佔有率,市場參與企業正在採取新的策略。例如,2023 年 7 月,CIQ 為在企業 Linux 發行版 Rocky Linux 上運行工作負載的企業建立軟體基礎設施,今天宣布啟動 CIQ 合作夥伴計畫。該公司旨在為世界各地尋求穩定性、無縫相容性和成本效益以滿足IT基礎設施和高效能運算需求的組織提供整套解決方案和服務。此次推出強化了 CIQ 合作夥伴優先的通路策略。 CIQ 合作夥伴計畫非常適合向企業和政府機構出售基礎設施的經銷商和整合商,這些企業和政府機構大規模部署和管理資料密集型工作負載,例如產品開發、科學研究、建模、機器學習和人工智慧.

- 然而,對少數應用程式的客製化伺服器作業系統的興趣日益成長,以及與合理伺服器選擇相關的許多困難預計將對市場開拓產生負面影響。此外,高昂的設定和支援成本將成為預測期內推廣該產品的挑戰。無論如何,對 BYOD(自帶設備政策)和整合准入框架的需求不斷成長預計將有助於在預測期內保持對伺服器的興趣。

- COVID-19 大流行極大地推動了世界各地的數位轉型和網際網路服務,很大一部分企業和企業開始在家工作和協作。在 COVID-19 大流行期間,由於需要遠端技術來維持業務營運,因此對資料中心的需求增加。疫情過後,出現了新的企業環境,促進了雲端服務和數位化,企業對其數位基礎設施進行了現代化改造,以支援更好的工作方式。

伺服器作業系統市場趨勢

雲端業務預計將佔據主要市場佔有率

- 越來越多的公司正在使用雲端運算技術來提供高效的應用程式和資料管理,而無需建置和維護自己的IT基礎設施。根據 Flexera 2023 年雲端狀況報告,75% 的企業受訪者表示他們正在採用 Microsoft Azure 來使用公共雲端。

- 亞馬遜網路服務(AWS)、微軟Azure和Google雲端是全球領先的雲端運算平台供應商。雲端技術的快速採用以及對一站式存取多重雲端服務的需求不斷成長,為雲端服務中介機構創造了機會。雲端的大規模採用將增加對伺服器的需求,並相應地推動對研究市場的需求。

- 此外,Fortinet 的業務永續營運雲端報告顯示,大多數組織正在追求混合(39%,高於 2021 年的 36%)或多重雲端策略(33%),並整合多種服務。 76% 使用多個雲端提供者。企業繼續快速地將工作負載轉移到雲端。 39% 的受訪公司已將超過一半的工作負載轉移到雲端,58% 的公司計劃在未來 12 至 18 個月內達到這一水準。雲端用戶確信雲端兌現了適應性容量和可擴展性 (53%)、更高的敏捷性 (50%) 以及更高的可用性和業務永續營運(45%) 的承諾。

- 由於突然需要實現組織現代化並遷移到雲,各種金融機構與雲端服務供應商合作。匯豐銀行計劃與亞馬遜網路服務(AWS)達成雲端協議,德意志銀行與Google雲端簽署十年戰略合作夥伴關係,桑坦德銀行宣布每天將超過200台伺服器遷移到雲端,因此該公司已宣布該計劃的完成日期截至 2023 年。

- 根據泰雷茲集團預測,截至2022年,約60%的企業資料將儲存在雲端。這一比例在 2015 年達到 30%,隨著公司擴大將資源轉移到雲端環境以提高安全性、可靠性和企業敏捷性,這一比例還在持續成長。這些因素為經過市場研究的供應商在未來幾年擴大其服務範圍創造了巨大的成長機會。

- 企業擴大採用雲端運算也擴大了市場研究的範圍。例如,印度市場供應商 Druva Inc. 報告稱,由於存在大量非結構化資料,許多公司主要針對企業資料。該公司還報告稱,這些資料佔企業儲存系統儲存資料的 80% 以上。

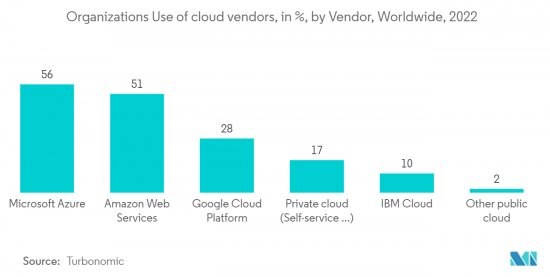

- Turbonomic 2022 年 7 月發布的資料顯示,2021 年,56% 的受訪者表示他們正在使用 Microsoft Azure 進行雲端服務。亞馬遜網路服務 (Amazon Web Services) 一直是排名第一的公司,直到 2020 年被微軟取代。此外,不使用任何雲端的受訪者比例從 2021 年的 4% 增加到 2022 年的 8%。

- 根據疫情期間進行的 CloudPath 調查,89% 的銀行計劃採用混合雲端儲存和部署來運作。根據 Nutanix 第三屆年度金融服務企業雲端指數,混合雲端採用率預計在未來五年內將成長 39%。雲端部署的大規模採用可能會推動所研究市場的需求。

北美地區預計將實現顯著成長

- 預計北美將佔據市場的主要佔有率。由於對伺服器作業系統的需求不斷成長以及網路應用的發展,美國人有望引領國際市場。利用人工智慧技術的伺服器作業系統管理許多應用程式,例如儲存和伺服器管理。該地區的市場受到許多企業擴大採用雲端運算解決方案的推動。因此,一些本地市場參與企業正在增加對雲端運算服務的投資。一些參與企業也專注於提供伺服器作業系統服務。

- 該地區的參與企業正在開拓新的伺服器作業系統 (OS),以贏得市場佔有率。例如,Red Hat Enterprise Linux (RHEL) 9 Beta 現已推出,並提供令人興奮的新功能和許多修復。 RHEL 9 Beta 與上游核心版本 5.14 一起建立,並提供 RHEL 下一個主要更新的預覽。此版本專為滿足從本地、多重雲端到邊緣的混合、混合部署需求而設計。系統安全服務守護程序 (SSSD) 是一個內建的業務單一登入框架,現在擁有有關任務完成時間、錯誤、可能的身份驗證流程等的更詳細資訊。新的搜尋功能允許管理員分析效能和配置問題。

- 根據美國小型企業管理局計劃辦公室的數據,2022年,美國小型企業數量達到3,320萬家,幾乎佔全國所有企業的比例(99.9%)。 2022年美國小型企業數量的成長反映了持續成長,比上一年(2021年)成長2.2%,比2017年至2022年成長12.2%。各地區中小企業的大量增加可能會為市場參與企業創造機會,並開發新的解決方案以佔領市場佔有率。如此龐大的中小企業數量很可能會促進所研究市場的成長。

- 而且,隨著雲端運算的興起,虛擬技術也正在成為市場驅動力。在雲端環境中,虛擬用於建立和管理多個虛擬機器 (VM)。提供強大虛擬功能的作業系統,例如具有 KVM(基於核心的虛擬機器)的 Linux 或具有 Hyper-V 的 Microsoft Windows,已成為雲端供應商和使用者的必需品。這些技術可實現高效的資源分配和虛擬機器管理,使某些伺服器作業系統對雲端部署更具吸引力。

- 此外,隨著 5G 部署在日本持續快速成長,對支援所部署的 5G 功能和服務的伺服器作業系統的需求可能會增加。例如,愛立信預計,到2026年5G用戶數將超過1.95億,而在美國,到2029年5G將占美國行動市場總量的約71.5%。 CTIA表示,快速成長將為美國5G經濟奠定基礎。

伺服器作業系統產業概述

全球伺服器作業系統市場由 Oracle、Cisco System、IBM、Amazon Web Services 和 Microsoft Corporation 等多家參與企業適度整合。公司持續投資於策略合作夥伴關係和產品開拓,以大幅提高市場佔有率。以下是一些最近的市場開拓:

2023 年 6 月,專門從事特定應用運算解決方案的公司 HIPER Global 宣布與 Ubuntu Linux 發行版和開放原始碼產品提供商 Canonical 建立新的合作夥伴關係。此次合作旨在為 HIPER Global 的全球客戶提供附加價值服務,包括針對 Ubuntu Linux 的安全修復和長期支援訂閱。此外,客戶還可以使用整合到 HIPER Global 解決方案中的先進 Canonical 產品,包括私有雲端基礎架構、虛擬元件、中央管理系統和支援的 Kubernetes 版本。此外,此次合作也強化了 HIPER Global 為全球客戶提供先進服務的承諾。

2023 年 1 月,全球開放原始碼解決方案供應商紅帽公司與 Oracle 簽訂了多州協議。此次合作旨在為客戶提供 Oracle 雲端基礎架構的更多作業系統選擇。此次合作始於將紅帽企業 Linux 加入 QCI 支援的作業系統清單。此外,此次升級還將有助於依賴OCI和紅帽企業Linux的企業進行數位轉型以及將重要應用程式遷移到雲端。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 由於混合和雲端平台的使用增加,對伺服器作業系統的需求不斷成長

- 超大規模資料中心建設投資的增加將顯著推動市場擴張

- 市場抑制因素

- 伺服器停機時間長和實施成本高可能會阻礙市場擴張

- 安全漏洞的增加可能會阻礙市場成長

第6章市場區隔

- 按成分

- 軟體

- 服務

- 按類型

- Windows

- Linux

- UNIX

- 其他類型

- 透過虛擬

- 虛擬伺服器

- 實體伺服器

- 依實施型態

- 雲

- 本地

- 按公司規模

- 主要企業

- 中小企業 (SME)

- 按行業分類

- 資訊科技/通訊

- BFSI

- 製造業

- 零售/電子商務

- 政府機關

- 醫療保健

- 其他行業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭形勢

- 公司簡介

- Oracle System Corporation

- Cisco Systems, Inc.

- IBM Corporation

- Amazon Web Services(AWS)

- Microsoft Corporation

- NEC Corporation

- Google LLC

- Fujitsu Ltd.

- Delll Technologies Inc.

- Hewlett PAckward Enterprises

- Apple Inc.

第8章投資分析

第9章 市場機會及未來趨勢

The global server operating market was valued at USD 19.07 billion in the current year. It is expected to reach USD 30.69 billion by the end of the forecasted year, registering a CAGR of 9.53% during the forecast period.

Key Highlights

- The market's growth is attributed to enterprise spending on creating a robust data center infrastructure. In addition, the increasing adoption of hybrid cloud environments and deployment of 5G networking technologies fuel the market's growth. Further, technological advancements and increasing security requirements in infrastructure are anticipated to provide lucrative expansion opportunities for the market during the forecast period.

- Increasing adoption of cloud platforms & infrastructure and rising data center infrastructure investments by most of the prominent players are assisting the market growth. The development of current advanced infrastructure is anticipated to boost the number of cloud server users worldwide. The key cloud computing service firms are investing a considerable portion of money in expanding cloud infrastructure around the globe. For instance, In February 2023, Oracle Corporation announced a new plan for public cloud in Saudi Arabia with an investment of USD 1.5 billion, considering the increasing demand for cloud services.

- Servers can be used in various applications in smart cities, including delivering high-performance, low-latency services such as 5G and AI applications for intelligent transportation systems (ITS) and vehicle-to-everything (V2X) communication. They can also be used to host cloud-based voice-over-IP (VoIP) communication systems for public transportation and storing and managing data from IoT sensors and devices. Additionally, high-availability servers can play a role in smart city services' security and authentication processes. For example, Globally, many smart city projects and efforts are being implemented, encouraging global investments owing to urbanization. The OECD estimates that between 2010 and 2030, international investments in smart city initiatives would total around USD 1.8 trillion for all urban city infrastructure projects. This would create an opportunity for the players to develop a new version of OS to capture the market share.

- To expand their market share, the market players are incorporating new strategies; for instance, In July 2023, CIQ, which builds software infrastructure for enterprises running workloads atop the Rocky Linux enterprise Linux distribution, announced today the launch of its CIQ Partner Program. The company said the launch reinforces CIQ's partner-first channel strategy as it aims to deliver its suite of solutions and services to organizations worldwide that desire stability, seamless compatibility, and cost-effectiveness for their IT infrastructure and high-performance computing needs. The CIQ Partner Program is ideal for resellers and integrators selling to enterprises and government organizations deploying and managing infrastructure at scale, data-intensive workloads for product development, scientific research, modeling, machine learning, and AI.

- However, the expanded interest in server operating systems with customized arrangements for a few applications & the many difficulties related to choosing a reasonable server is expected to affect the market development negatively. Besides, high establishment & support expenses represent a test to advertise product during the forecast period. In any case, the Bring Your Device Policy (BYOD) & the rising requirement for unified admittance frameworks are considered to assist with keeping the interest up for servers over the forecast period.

- The Covid-19 pandemic significantly boosted digital transformation and Internet services worldwide, with a significant part of businesses and enterprises that have started cooperating and working from home. The need for data centers has grown since remote technologies are demanded to keep companies operating during the Covid-19 pandemic. Following the pandemic, a new company environment has materialized, boosting cloud services and digitization as corporations modernize their digital infrastructure to support better working practices.

Server Operating System Market Trends

Cloud Segment is Expected to Hold a Significant Share of the Market

- A growing number of companies are increasingly using cloud computing technologies to provide efficient application and data management with no need for constructing or maintaining IT infrastructures on site. As per Flexera 2023 State of the Cloud Report, 75% of enterprise respondents indicated adopting Microsoft Azure for public cloud usage.

- Amazon Web Services (AWS), Microsoft Azure, and Google Cloud are the leading cloud computing platform providers globally. This rapid adoption of cloud technologies and the rising demand for one-stop access to multi-cloud services have created opportunities for cloud services brokerage. Such huge adoption of the cloud would increase the demand for servers, proportionately driving the demand for the studied market.

- Further, according to the Fortinet cloud report 2022, Most organizations pursue a hybrid (39%, up from 36% in 2021) or multi-cloud strategy (33%) to incorporate multiple services for scalability or business continuity reasons. 76% percent are utilizing two or more cloud providers. Firms continue to move workloads to the cloud at a rapid pace. 39% of surveyed members have more than half of their workloads in the cloud, while 58 percent plan to get to this level in the next 12-18 months. Cloud users guarantee that the cloud is delivering on the promise of adaptable capacity and scalability (53%), increased agility (50 percent), and improved availability and business continuity (45%).

- As organizations had to modernize and migrate to the cloud abruptly, various financial organizations partnered with cloud service providers. Such as HSBC's planned cloud contract with Amazon Web Services (AWS), Deutsche Bank striking a 10-year strategic partnership with Google Cloud, and Santander's made announcement that it is shifting its over 200 servers to the cloud per day, the company has declared the deadline to complete this project is the year 2023.

- According to Thales Group, as of 2022, around 60% of all corporate information is stored in the cloud. As companies progressively move their resources into cloud environments to enhance security, dependability, and enterprise agility, this proportion hit 30% in 2015 and has since continued to grow. These factors create a massive growth opportunity for the market-studied vendors to expand their offerings in the coming years.

- The growing adoption of cloud computing among enterprises also expands the market studied scope. For instance, India-based market vendor, Druva Inc., reported that many companies primarily target enterprise data due to a large amount of unstructured data. The company also reported that this data claim accounts for over 80% of the data stored in enterprise storage systems.

- According to Turbonomic, they released data in July 2022 stating that, in 2021, 56% of respondents stated that they are utilizing Microsoft Azure for their cloud services. Amazon Web Services was on top of the list until 2020 Microsoft took its place. Additionally, the percentage of respondents not utilizing any cloud increased to eight percent in 2022 from four percent in 2021.

- As per CloudPathSurvey conducted during a pandemic, 89% of banks plan to operate with hybrid cloud storage and deployment. As per Nutanix's third annual Enterprise Cloud Index report for financial services, hybrid cloud adoption is expected to grow 39% in the coming five years. Such huge adoption towards cloud deployment would drive the demand for the studied market.

North America Expected to Witness Significant Growth

- North America is expected to hold a significant share of the market. Americans are anticipated to lead the international market due to the increasing demand for server operating systems and the development of Internet applications. Using artificial intelligence technology, the server operating system manages many applications, such as storage and server management. The market in the region is being driven by the growing adoption of cloud computing solutions across numerous corporations. As a result, several provincial market participants are expanding their investments in cloud computing services. Several players are even focused on providing server operating system services.

- The players in the region are developing new operating systems (OS) for servers to capture the market share. For example, Red Hat Enterprise Linux (RHEL) 9 Beta is available and delivers exciting new features and many more modifications. RHEL 9 Beta is established on upstream kernel version 5.14 and delivers a preview of the following major update of RHEL. This release is designed to require hybrid multi-cloud deployments that range from on-premises and public cloud to edge. The System Security Services Daemon (SSSD), the built-in business single-sign-on framework, now adds more detail for possibilities such as time to complete tasks, errors, the authentication flow, and more. New search capabilities allow admins to analyze performance and configuration issues.

- According to the United States Small Business Administration Office of Advocacy, in 2022, the number of small businesses in the United States reached 33.2 million, accounting for nearly all (99.9 percent) firms in the country. The growth in the number of small businesses in the United States in 2022 reflects continuous growth, with a 2.2% increase from the previous year(2021) and a 12.2% increase from 2017 to 2022. Such a massive rise in the SMEs in the various region would create an opportunity for the market players to develop new solutions to capture the market share. Such a huge number of SMEs would allow the studied market to grow.

- Furthermore, virtualization technologies have also been instrumental in driving the market with the rise of cloud computing. Cloud environments use virtualization to create and manage multiple virtual machines (VMs). Operating systems that offer robust virtualization capabilities, for example, Linux with KVM (Kernael-based Virtual Machine) or Microsoft Windows with Hyper-V, become essential for cloud providers and users. Such technologies enable the efficient allocation of resources and managing VMs, further growing the appeal of specific server operating systems in cloud deployments.

- Further, the booming 5G deployments in the country will increase the demand for server operating systems to support the 5G features and services being rolled out. For instance, according to Ericsson, there will be more than 195 million 5G subscriptions by 2026, and by 2029, in the United States, 5G will account for about 71.5% of the entire U.S. mobile market. According to CTIA, rapid growth creates a platform for the US 5G economy.

Server Operating System Industry Overview

The Global Server Operating System market is moderately consolidated with the presence of several players like Oracle, Cisco System, IBM, Amazon Web Services, Microsoft Corporation, etc. The companies continuously invest in strategic partnerships and product developments to gain substantial market share. Some of the recent developments in the market are:

In June 2023, HIPER Global, a company specializing in application-specific computing solutions, announced a new partnership with Canonical, the provider of Ubuntu Linux distribution and open-source products. The collaboration aims to offer HIPER Global's worldwide customers value-added services, including a subscription to security fixes and long-term support for Ubuntu Linux. Additionally, customers will have access to advanced Canonical products integrated into HIPER Global solutions, such as private cloud infrastructures, virtualization components, centralized management systems, and supported versions of Kubernetes. Furthermore, the partnership strengthens HIPER Global's commitment to delivering advanced service to its customer worldwide.

In January 2023, Red Hat, Inc., the global provider of open-source solutions, and Oracle formed a multi-state agreement. The collaboration aims to provide clients with additional operating system options for Oracle Cloud Infrastructure. The partnership begins with adding Red Hat Enterprise Linux to QCI's supported operating systems list. Furthermore, this upgrade will assist enterprises that rely on OCI and Red Hat Enterprise Linux for digital transformation and cloud migration of essential applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing hybrid and cloud platform usage will increase demand for server operating systems

- 5.1.2 Rising investments in the building of hyperscale data centers are significantly driving the market expansion

- 5.2 Market Restraints

- 5.2.1 High server downtime and implementation costs could impede market expansion

- 5.2.2 The growing number of security flaws could hamper the growth of the market

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Service

- 6.2 By Type

- 6.2.1 Windows

- 6.2.2 Linux

- 6.2.3 UNIX

- 6.2.4 Other Types

- 6.3 By Virtualization

- 6.3.1 Virtual Server

- 6.3.2 Physical Server

- 6.4 By Deployment Mode

- 6.4.1 Cloud

- 6.4.2 On-premise

- 6.5 By Enterprise Size

- 6.5.1 Large Enterprises

- 6.5.2 Small and Medium-sized Enterprises (SMEs)

- 6.6 By Industry Vertical

- 6.6.1 IT and Telecom

- 6.6.2 BFSI

- 6.6.3 Manufacturing

- 6.6.4 Retail and E-Commerce

- 6.6.5 Government

- 6.6.6 Healthcare

- 6.6.7 Other Industry Verticals

- 6.7 Geography

- 6.7.1 North America

- 6.7.2 Europe

- 6.7.3 Asia-Pacific

- 6.7.4 Latin America

- 6.7.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Oracle System Corporation

- 7.1.2 Cisco Systems, Inc.

- 7.1.3 IBM Corporation

- 7.1.4 Amazon Web Services (AWS)

- 7.1.5 Microsoft Corporation

- 7.1.6 NEC Corporation

- 7.1.7 Google LLC

- 7.1.8 Fujitsu Ltd.

- 7.1.9 Delll Technologies Inc.

- 7.1.10 Hewlett PAckward Enterprises

- 7.1.11 Apple Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球伺服器市場規模、佔有率、成長分析,依企業規模(微型、小型)、最終用途(BFSI、能源)- 2024-2031 年產業預測

全球伺服器市場規模、佔有率、成長分析,依企業規模(微型、小型)、最終用途(BFSI、能源)- 2024-2031 年產業預測 2024 年人工智慧伺服器世界市場報告

2024 年人工智慧伺服器世界市場報告 2024 年伺服器作業系統世界市場報告

2024 年伺服器作業系統世界市場報告 住宅代理伺服器市場 – 2024 年至 2029 年預測

住宅代理伺服器市場 – 2024 年至 2029 年預測 HFT(高頻交易)伺服器市場、份額、規模、趨勢、行業分析報告:按處理器、按外形尺寸、按應用、按地區、按細分市場、預測,2024-2032 年

HFT(高頻交易)伺服器市場、份額、規模、趨勢、行業分析報告:按處理器、按外形尺寸、按應用、按地區、按細分市場、預測,2024-2032 年 2024 年 OPC 伺服器軟體世界市場報告

2024 年 OPC 伺服器軟體世界市場報告 2024 年儲存與伺服器支援服務全球市場報告

2024 年儲存與伺服器支援服務全球市場報告 2024-2028 年全球伺服器市場

2024-2028 年全球伺服器市場 伺服器導軌套件的全球市場 2024-2028

伺服器導軌套件的全球市場 2024-2028 2024-2028年全球伺服器主機板市場

2024-2028年全球伺服器主機板市場