|

市場調查報告書

商品編碼

1408096

暖氣設備-市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Heating Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

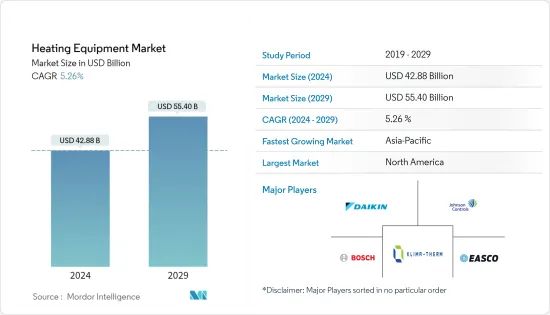

暖氣設備市場規模預計到2024年為428.8億美元,預計到2029年將達到554億美元,在預測期內(2024-2029年)複合年成長率為5.26%。

對節能供暖設備的需求導致了能夠提供經濟高效供暖的機械設備的開拓,從而推動了市場的擴張。快速的技術進步為減少碳排放提供了具有成本效益的選擇,從而推動了暖氣設備市場的發展。這些系統分為自足式單元包和核心系統。

主要亮點

- 全球建設產業的大幅擴張是支撐市場良好前景的關鍵原因之一。此外,對節能供暖系統日益成長的需求正在推動市場擴張。暖氣設備廣泛用於溫度結冰的地方,以提高周圍區域的溫度,同時減少對環境的影響。物聯網以及設備與人工智慧的整合等技術突破也在推動成長。這些技術允許用戶使用智慧型手機或穿戴式裝置遠端控制加熱設備。產品開發商也正在為住宅和小型商業綜合體開發新的自足式暖氣設備裝置。

- 印度、中國等開發中國家的石化和化學工業正在迅速擴張,工業鍋爐的需求預計將增加。由於全球大型發電工程投資增加,市場需求可能進一步上升。這些容器經常用於化學和石化行業,並構成該應用領域工業鍋爐的大部分。據美國環保署稱,新的鍋爐法規旨在大規模減少環境排放。目前,作為重要排放源的鍋爐,超過88%可以每年進行調整以滿足排放法規,而其餘12.0%則需要維修或更換以減少有害排放。

- 對節能設備不斷成長的需求正在推動熱泵等技術的部署,這些技術為最終用戶提供了巨大的潛力,可以為世界各地的可再生能源和氣候目標做出貢獻。熱泵將供應方脫碳與需求方技術協同效應的能力正在被利用,為減少二氧化碳排放做出重大貢獻。熱泵是一種高度通用的技術,並且具有很高的能源效率,因為它們可以在一個裝置中提供加熱、冷卻和熱水。此外,這些設備可用於傳統/混合可再生系統,以使用主動熱感質量儲存剩餘電力。也已知整合電網內的各種能源並最佳化其性能。

- 另一方面,已開發國家政府制定了嚴格的排放要求,以控制排放排放環境中的污染物,影響供熱設備效率、營業成本和市場成長。據美國環保署稱,美國政府已頒布法規規範工業鍋爐的粒狀物、二氧化硫和氮氧化物排放。此外,國際能源總署(IEA)透過其清潔能源技術計劃,正在引進選擇性催化還原(SCR)、排煙脫硫(FGD)、布袋除塵器等技術來減少工業鍋爐的排放,我們鼓勵其使用。此外,工業鍋爐製造商面臨的關鍵問題之一是需要提高效率和蒸汽品質以滿足市場需求。這些嚴格的監管可能會在短期內阻礙市場的成長。

- 建設產業常被認為是一個國家經濟發展的重要指標,因此GDP成長、通貨膨脹、利率、政府支出等宏觀經濟指標的變化都能對建設產業產生直接影響。通貨膨脹導致原物料成本上漲、利率上升導致建築公司借款減少等因素預計將對預測期內所研究市場的成長產生負面影響。

暖氣設備市場趨勢

熱泵預計將佔據主要市場佔有率

- 能源是家庭、醫院和學校的重要動力來源。然而,它們的生產和使用排放大量溫室氣體。因此,世界主要經濟體正在向再生能源來源轉型,以限制溫室氣體排放,同時盡量減少對非可再生能源來源的排放。熱泵技術是減少溫室氣體排放的有效手段。空氣熱熱泵和地熱熱泵提供節能的加熱解決方案。

- 北美地區,尤其是美國,熱泵的部署正在穩定增加。造成這種情況的原因各不相同,包括設備提供的便利性、氣候條件、政府稅額扣抵優惠和法規。此外,熱泵由於其能源效率而受到該地區政府的監管。例如,能源部宣布了風扇能源評級,為住宅爐子中的風扇設定了最低空氣效率標準。

- 根據新的 FER 標準,美國能源部估計,到2030 年,爐風機新標準將節省約3.99 誇脫的能源,減少3,400 萬噸碳污染,並為美國人節省超過90 億美元的電費。我們估計,我們將提供它。根據一項新的州法律,未來五年內,緬因州各城市將招募安裝人員,以實現安裝 10 萬台熱泵的目標。此外,新安布勒熱泵計劃旨在大幅降低村莊的柴油成本。

- 此外,東歐氣候寒冷,捷克、波蘭和保加利亞等國家對暖氣解決方案的需求很高。與該地區其他國家一樣,提高暖氣和冷氣產業能源效率的措施正在增加。根據歐盟智慧能源歐洲計畫共同創立的 Stratego 的說法,2010 年至 2050 年間投資 500 億歐元可以節省足夠的燃料,從而最大限度地降低能源系統成本。此外,該投資的一部分將包括 50 億歐元用於區域供暖和 150 億歐元用於獨立熱泵。

- 2022年7月,新加坡國家環境局(NEA)報告稱,正在考慮在高層住宅(公寓和組屋單位)中使用熱泵熱水器。熱泵熱水器僅耗電 210 瓦,而典型的電或燃氣熱水器耗電量約為 3,000 瓦。採用熱泵節省的能源可能會顯著減少用戶每月的電費支出。

預計亞太地區市場將出現高成長

- 中國廣闊的地理區域被正式分類為五個主要氣候區,具有不同的熱設計要求。我國北方是兩個最寒冷的氣候區,冬季需要暖氣。都市區依賴集中供熱系統,而農村地區主要依賴自營供暖系統。另一個供暖需求增加的氣候區是夏季炎熱、冬季寒冷的氣候區。由於歷史原因,該氣候區的建築物沒有提供區域供暖系統的公共基礎設施或服務,建築物普遍缺乏有效的供暖服務。因此,中國北方和南方面臨的暖氣挑戰不同,需要量身訂製的解決方案。

- 亞太地區可能佔據最高的銷售佔有率。這主要是由於中國和印度等國家建築業的成長,這些國家正在進行大規模的基礎設施投資,特別是在零售空間、商業辦公大樓、製造設施和地鐵線路方面。此外,火力發電行業對鍋爐的需求不斷增加正在推動市場擴張。

- 許多中國家庭仍依賴小煤爐取暖,造成空氣污染,損害健康。為了解決這些問題,中國政府於 2017 年啟動了一項為期五年的清潔供暖計劃,旨在使北方 70% 的家庭擺脫煤炭,轉向更清潔的供暖方式。 2022 年,即該計畫的最後一年,普林斯頓大學研究人員進行的一項開創性研究提供了政策指南:增加農村家庭對熱泵的使用。在調查的選項中,研究人員發現空氣對空氣熱泵提供的空氣品質、健康和氣候效益最大。

- 中國的目標是到2060年實現碳中和,並在減少空氣污染方面做出了成功的努力。土木與環境工程及國際關係教授丹尼斯·莫塞拉爾表示,用清潔取暖器取代都市區住宅的煤爐將顯著改善中國北方冬季的空氣質量,據說過早死亡的人數也有所減少。此外,中國計劃在2060年實現碳中和,電網和供電系統的「脫碳」極為重要。實現這一目標的方法之一是放棄煤炭,轉向更多非化石能源。

- 區域參與企業正在開發新產品以滿足不同的客戶需求。例如,2022年3月,松下在日本宣布了新設備。 EcoCute解決方案由熱泵和熱水儲存槽組成,透過保持浴缸內的水溫恆定來節省能源。它還利用家中洗澡水的熱量在夜間節省電力。此外,該設備還節省能源和水。配備太陽能充電功能,利用太陽能發電和儲存的剩餘電力。您可以在白天或晚上的任何時間使用電力來加熱水。

供熱設備產業概況

由於競爭激烈,全球暖氣設備市場上競爭公司之間的競爭呈現零碎化。由於 Easco Boiler Corporation、Robert Bosch GmbH、Daikin Industries ltd、Klima-Therm、Johnson Controls 等主要企業的入駐。

- 2023 年 4 月 Kanthal 和 Rath 宣佈建立戰略合作夥伴關係,擴大雙方在工業加熱技術方面的聯合提案,Kanthal 負責工業電加熱技術,Rath 負責高溫耐火材料產品。透過兩家公司的密切合作,我們將支持鋼鐵、石化等產業實現生態轉型。這種合作關係結合了兩家公司的互補優勢,為市場提供了最廣泛的永續工業加熱解決方案選擇。客戶可以受益於 Kanthal 在加熱組件和加熱系統方面的經驗以及 Rath 卓越的隔熱材料和耐火材料解決方案,為他們的工業加熱需求提供獨特的組合。

- 2023 年 4 月,造紙公司 UPM 選擇在其位於德國和芬蘭的工廠建造新的電鍋爐來產生熱量和蒸汽。該公司將安裝八台新鍋爐。這項舉措將使 UPM 能夠階段在其工廠中使用石化燃料。第一台 50 兆瓦電鍋爐已在芬蘭 Valkeakoski 的 UPM Tervasaari 造紙廠安裝並運作。該鍋爐從芬蘭賈姆薩的 UPM Kaipola 工廠搬遷至 Valkeakoski。為了提高效率,該公司計劃今年稍後在該工廠再建造一座 60 兆瓦的電鍋爐。這種大容量鍋爐為工廠生產蒸汽和熱量,並支持這兩個過程。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 供應鏈分析

- 政府法規政策

- 宏觀經濟走勢對產業的影響

第5章市場動態

- 促進因素

- 抑制因素

第6章市場區隔

- 產品類別

- 熱泵

- 爐

- 單元式加熱器

- 鍋爐

- 最終用戶

- 住宅

- 商業的

- 工業的

- 地區

- 北美洲

- 美國

- 加拿大

- 其他

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 其他

- 亞太地區

- 印度

- 中國

- 日本

- 其他

- 其他

- 北美洲

第7章 公司簡介

- Daikin Industries Ltd

- Klima-Therm

- Robert Bosch GmbH

- Carrier Global Corporation(United Technologies Corp.)

- Panasonic Corporation

- Johnson Controls

- Lennox International, Inc.

- Easco Boiler Corporation

- Ariston Thermo Group

- Danfoss A/S

第8章投資分析

第9章 市場機會及未來趨勢

The Heating Equipment Market size is estimated at USD 42.88 billion in 2024, and is expected to reach USD 55.40 billion by 2029, growing at a CAGR of 5.26% during the forecast period (2024-2029).

The requirement for energy-efficient heating equipment has resulted in the development of mechanical devices that can deliver cost-effective heating, assisting the market's expansion. With quick technological advancement, heating equipment provides cost-effective choices for lowering carbon emissions, boosting the heating equipment market forward. These systems are classified as either self-contained packages of units or core systems.

Key Highlights

- Significant expansion in the global construction industry is one of the important reasons driving the market's favorable outlook. Furthermore, the growing need for energy-efficient heating systems is propelling market expansion. Heating equipment is extensively utilized in places with freezing temperatures to raise ambient temperatures with low environmental impact. Technological breakthroughs, like integrating linked devices with the Internet of Things and artificial intelligence, are also driving growth. These technologies allow users to regulate heating equipment remotely via smartphones and wearable devices. Product developers are also creating new and self-contained heating equipment units for residential and small business complexes.

- The rapidly expanding petrochemical and chemical industries in developing nations such as India and China are expected to increase demand for industrial boilers. The market demand is likely to climb further due to increased investment in mega power projects worldwide. These vessels are frequently employed in the chemical and petrochemical sectors, which account for the majority of industrial boilers in this application area. According to the US Environmental Protection Agency, new boiler restrictions are intended to reduce environmental emissions on a massive scale. Currently, more than 88 percent of significant source boilers can fulfill emission regulations with annual tune-ups, but the remaining 12.0 percent will require refurbishment or replacement to reduce harmful emissions, which is expected to offer opportunities for manufacturers throughout the forecast period.

- The growing demand for energy-efficient devices has been driving the deployment of technology, such as heat pumps, to provide end users with significant potential to contribute to renewable energy and climate targets across various regions in the world. The ability of the heat pump to provide a synergy between the decarbonization on the supply side and the technology on the demand side is being exploited to make a significant contribution to reducing the emission of CO2. Heat pumps, being a versatile technology, can provide space heating, cooling, and warm water, all from one integrated unit, thus, providing energy efficiency. Furthermore, these devices can be used in conventional/hybrid renewable systems and accumulate surplus electricity with the help of active thermal mass elements. They are also known to integrate and optimize the performance of various energy resources in the electricity grid.

- On the flip side, governments in developed countries have enacted stringent emission requirements to control pollutants discharged into the environment, influencing heating equipment efficiency, operating costs, and market growth. According to the Environmental Protection Agency, the United States government has established rules for controlling particulate matter, sulfur dioxide, and nitrogen oxide emissions from industrial boilers. Furthermore, the International Energy Agency encourages the usage of technology such as selective catalytic reduction (SCR), flue gas desulfurization (FGD), and fabric filters to reduce emissions from industrial boilers through its Clean Energy Technology Programme. Furthermore, one of the significant issues that industrial boiler manufacturers confront is the necessity to enhance efficiency and steam quality to meet market demand. Such stringent regulations could hinder the market's growth in the short run.

- The construction industry is often considered a key indicator of a country's economic development, and therefore, fluctuations in macroeconomic indicators such as GDP growth, inflation, interest rates, and government spending can have a direct impact on the construction industry. Factors like rising raw material costs due to inflation, higher interest rates leading to less borrowing by builders are anticipated to negatively impact the growth of the studied market during the forecast period.

Heating Equipment Market Trends

Heat Pump is Expected to Hold a Major Market Share

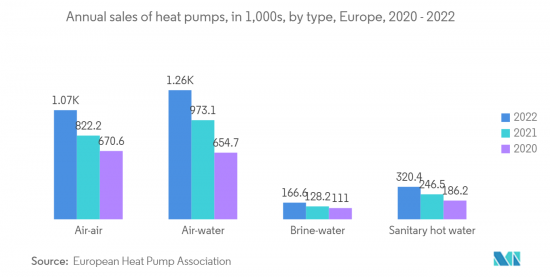

- Energy is a critical power source in homes, hospitals, and schools. However, its manufacturing and use result in significant greenhouse gas emissions. As a result, major economies worldwide are attempting to minimize their reliance on nonrenewable energy sources while progressively shifting toward renewable energy sources to limit greenhouse gas emissions. Heat pump technology is a viable way to reduce greenhouse gas emissions. Aerothermal and geothermal heat pumps offer an energy-efficient solution to space heating.

- The deployment of heat pumps has increased steadily in the North American region, especially in the United States, due to varied reasons, like the convenience of offering the equipment, climatic conditions, government tax credit benefits, and regulations. Furthermore, the heat pumps have been regulated by the governments in the region for their energy efficiency. For instance, the Department of Energy announced Fan Energy Rating, which sets a minimum airflow efficiency standard for residential furnace fans.

- With the new FER standards, the US DOE estimates that the new standard for furnace fans might save approximately 3.99 quads of energy, minimize carbon pollution by 34 million metric tons, and provides American citizens with savings of more than USD 9 billion in electric bills by 2030. According to new state law,over the next five years, the city of Maine seeks installers to help fulfill the goal of 100,000 heat pumps. Furthermore, the New Ambler heat pump project aims to drastically reduce diesel costs in the villages.

- Furthermore, Eastern Europe has colder climatic conditions in the region, and the demand for heating solutions is significant in these countries such as the Czech Republic, Poland, Bulgaria, and others. Similar to other countries in the region, measures to increase energy efficiency in the heating and cooling sector are on the rise. According to Stratego, which is co-founded by the Intelligent Energy Europe Programme of the EU, an investment of EUR 50 billion during the span of 2010-2050 will save enough fuel to minimize the costs of the energy system. Moreover, as part of this investment, district heating's share amounted to EUR 5 billion, and individual heat pumps at EUR 15 billion.

- In July 2022, the National Environment Agency (NEA) Singapore reported they are exploring using heat pump water heaters in high-rise residences - condominiums and HDB units. Heat pump water heaters use only 210 watts of power, compared to the approximately 3000 watts used by typical electric or gas water heaters. A user's monthly power expenditures would be significantly reduced by the energy savings from employing a heat pump.

The Asia Pacific Region is Expected to Witness a High Market Growth

- China's vast geographic area is officially divided into five primary climate zones with different thermal design requirements. Northern China, which comprises the two coldest climate zones, requires space heating in winter. The urban areas depend on district heating systems, whereas rural regions mainly utilize individual household heating systems. Another climate zone with rising demand for heating is the hot summer and cold winter climate zone. Due to historical reasons, there is no public infrastructure or services to provide district heating systems for buildings in this climate zone, and buildings generally lack effective heating services. Therefore, China's northern and southern regions face different heating challenges and need tailored solutions.

- The Asia Pacific will have the highest revenue share. This is primarily due to the rising construction sector in nations such as China and India, which are witnessing substantial infrastructure investments, particularly in retail spaces, commercial office buildings, manufacturing facilities, and metro train lines. Additionally, increased demand for boilers in the thermal power industry is driving market expansion.

- Many of China's households still depend on small coal stoves for heat, which causes air pollution that damages health. To address these problems, the Chinese government launched a five-year "Clean Heating Plan" in 2017 to transition 70 percent of northern households away from coal and toward cleaner heating options. In 2022, as the plan reaches its final year, a novel study by Princeton University researchers offered policy guidance: Increase the usage of heat pumps in rural households. Among the options studied, the researchers found air-to-air heat pumps provide the most air quality, health, and climate benefits.

- China aims for carbon neutrality by 2060 and has engaged in a successful effort to reduce air pollution. According to Denise Mauzerall, professor of civil & environmental engineering & international affairs, replacing coal stoves in urban and rural residences with clean heaters dramatically improves air quality throughout northern China in winter while decreasing premature deaths. Also, given that China plans to be carbon neutral by 2060, "decarbonizing" their power grid or the system that delivers electricity is critical. One way to achieve this is by moving away from coal and toward more non-fossil energy.

- The regional players are developing new products to cater to a diverse range of customers' requirements. For instance, in March 2022, Panasonic introduced a new device in Japan. The Eco Cute solution comprises a heat pump and a hot water storage tank to save energy by maintaining consistent bathwater temperatures. It also saves electricity at night by utilizing the heat from a household's bathwater. Furthermore, the device conserves energy and water. The product includes a solar charging capability that uses extra power generated and stored by PV sources. It can boil water at any time of day or night using electricity.

Heating Equipment Industry Overview

The competitive rivalry in the Global Heating Equipment Market is fragmented in nature due to high competition. The high owing to the presence of some key players such as Easco Boiler Corporation, Robert Bosch GmbH, Daikin industries ltd, Klima-Therm, Johnson Controls and many more.

- April 2023: Kanthal and Rath, players in their respective fields - Kanthal in industrial electric heating technology and Rath in high-temperature refractory products, announced a strategic alliance to extend their joint offering in industrial heating technology. Their services will help industries such as steel and petrochemical to make the green transition through close collaboration. The collaboration combines the complementing qualities of both firms, resulting in the market's most extensive choice of sustainable industrial heating solutions. Customers will benefit from Kanthal's experience in heating components and systems and Rath's superior insulation and refractory solutions in a one-of-a-kind combination offering for their industrial heating needs.

- April 2023: UPM, a paper mill company, opted to build new electric boilers to produce heat and steam at its plants in Germany and Finland. The company will install eight new boilers. This effort will enable UPM to phase out the usage of fossil fuels in its mills. The first 50MW electric boiler at the company's UPM Tervasaari paper mill in Valkeakoski, Finland, has already been commissioned. The boiler had been relocated to Valkeakoski from the UPM Kaipola mill in Jamsa, Finland. To improve efficiency, the business plans to build another 60MW electric boiler at the mill later this year. This large-capacity boiler will produce steam and heat for the mill, assisting in both processes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Supply Chain Analysis

- 4.4 Government Policies and Regulations

- 4.5 Impact of Macro Economic Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.2 Restraints

6 MARKET SEGMENTATION

- 6.1 Product Type

- 6.1.1 Heat Pumps

- 6.1.2 Furnaces

- 6.1.3 Unitary Heaters

- 6.1.4 Boilers

- 6.2 End User

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 US

- 6.3.1.2 Canada

- 6.3.1.3 Others

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 UK

- 6.3.2.3 France

- 6.3.2.4 Russia

- 6.3.2.5 Spain

- 6.3.2.6 Others

- 6.3.3 Asia Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Others

- 6.3.4 Rest of the World

- 6.3.1 North America

7 Company Profiles

- 7.1 Daikin Industries Ltd

- 7.2 Klima-Therm

- 7.3 Robert Bosch GmbH

- 7.4 Carrier Global Corporation [United Technologies Corp.]

- 7.5 Panasonic Corporation

- 7.6 Johnson Controls

- 7.7 Lennox International, Inc.

- 7.8 Easco Boiler Corporation

- 7.9 Ariston Thermo Group

- 7.10 Danfoss A/S

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

感應加熱系統的全球市場:2024 年

感應加熱系統的全球市場:2024 年 加熱設備市場:按應用、產品類型、燃料類型和國家進行分析和預測(2023-2033)

加熱設備市場:按應用、產品類型、燃料類型和國家進行分析和預測(2023-2033) 2024年全球暖氣設備市場報告(不包括熱風爐)

2024年全球暖氣設備市場報告(不包括熱風爐) 美國商務用暖氣設備市場規模、佔有率和趨勢分析報告:按產品、建築占地面積、最終用途、地區和細分市場預測,2024-2030 年

美國商務用暖氣設備市場規模、佔有率和趨勢分析報告:按產品、建築占地面積、最終用途、地區和細分市場預測,2024-2030 年 到 2030 年低頻加熱系統市場預測:按產品類型、應用和地區分類的全球分析

到 2030 年低頻加熱系統市場預測:按產品類型、應用和地區分類的全球分析 2024年全球熱風供暖設備市場報告

2024年全球熱風供暖設備市場報告 熱風加熱機市場、份額、規模、趨勢、產業分析報告:按類型、按應用、按地區、細分市場趨勢,2023-2032

熱風加熱機市場、份額、規模、趨勢、產業分析報告:按類型、按應用、按地區、細分市場趨勢,2023-2032 美國暖氣設備市場規模、佔有率、趨勢分析報告:按設備、應用、地區和細分市場預測,2023-2030 年

美國暖氣設備市場規模、佔有率、趨勢分析報告:按設備、應用、地區和細分市場預測,2023-2030 年 加熱設備市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

加熱設備市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 熱空氣加熱器的全球市場:按產品類型、燃料類型、應用和最終用戶 - 2023-2030 年預測

熱空氣加熱器的全球市場:按產品類型、燃料類型、應用和最終用戶 - 2023-2030 年預測