|

市場調查報告書

商品編碼

1408011

閥門:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

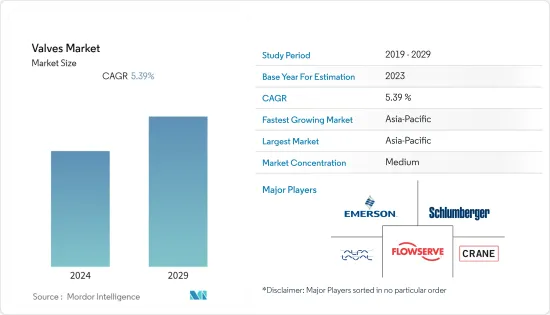

上年度全球閥門市場規模為799億美元,預計未來五年將達到1,082億美元,複合年成長率為5.39%。

主要亮點

- 閥門控制系統或製程內的流量和壓力。它是輸送液體、氣體、蒸氣、泥漿等管道系統的重要組成部分。因此,基礎設施開拓和工業自動化的投資不斷增加,推動新興市場的成長。

- 石油和天然氣行業管道基礎設施投資的增加預計將推動工業閥門的安裝。此外,許多開發中國家的政府供水和衛生計劃正在增加,這可能會推動家用和農業用工業閥門的銷售。例如,2022年5月,中國宣布計劃在未來四年內擴大該地區的天然氣管網。這些發展可能會增加該國對工業閥門的需求。

- 此外,各國加大對供水和用水和污水基礎設施的投資也是推動研究市場成長的另一個主要因素,因為閥門廣泛應用於用水和污水和污水處理廠以及配水管道,這是一個因素。例如,2022年,亞洲基礎設施投資銀行(AIIB)核准了兩個重大計劃:印度大壩維修和改善計劃和烏茲別克斯坦布哈拉地區供水和用水和污水計劃第二期。

- 許多公司正在利用人工智慧 (AI) 和工業物聯網 (IIoT) 等新技術來最大程度地減少因閥門故障而導致的意外停機和其他不良事件。配備感測器的閥門也擴大被採用,以減少故障和整體維護成本。這些先進價值的採用預計將在預測期內進一步提振市場。

- 全球閥門市場擁有大量參與者,提供針對各個最終用戶行業應用的廣泛解決方案。這顯著加劇了供應商之間的競爭,鼓勵他們開發創新解決方案並採用獨特的業務策略來擴大其市場佔有率。因此,市場競爭的加劇預計將在預測期內進一步推動研究市場的成長。

- 然而,市場參與者必須遵守有關閥門製造的各種當地認證和政策,由於閥門在多個最終用戶行業的廣泛應用,導致產品規格多樣化。這是市場成長的抑制因素,因為企業必須根據當地政策修改相同的產品,從而難以達到理想的安裝成本。

- COVID-19疫情對石油和天然氣產業產生了負面影響,油價大幅下跌。世界各國政府實施的各種法規減少了對石油和天然氣的需求,造成供需之間的巨大差距。除石油和天然氣外,水、用水和污水、能源和電力產業也是閥門的主要最終用戶。由於全球大流行,這些產業的需求也出現下降。然而,隨著幾乎所有行業限制的解除,這些行業已開始逐步復甦,預計將在預測期內加速未來市場的成長。

閥門市場趨勢

石油和天然氣產業佔主要市場佔有率

- 大部分石油和天然氣業務,包括精製和分銷,都依賴管道系統。因此,基礎設施和可靠的控制系統對該行業至關重要。油氣閥門對於確保工業管路運作的安全至關重要。

- 作為任何管道系統的重要組成部分,閥門可用於控制流量、隔離和保護設備以及指導原油精製過程。例如,閘閥是用於打開和關閉流體流動的線性運動裝置,通常用於許多管道和管道應用。

- 隨著對石油產品的需求不斷成長,石油和天然氣產業不斷擴大,市場上的供應商正在推出針對石油和天然氣產業應用的創新解決方案。例如,2022 年 2 月,CIRCOR International, Inc. 推出了新型 CIR 3100 控制閥。據該公司介紹,該閥門專為低壓和高壓壓降服務以及重型應用而設計,包括上游、中游和下游石油和天然氣、加工和發電行業,以及海事和可再生能源部門..

- 近年來,石油和天然氣探勘和生產(E&P)活動的增加已成為推動市場成長的主要趨勢。此外,許多國家都在大力投資鑽探活動來開採非傳統資源,全球閥門市場前景看好。例如,預計 2022 年加拿大石油和天然氣鑽探速度將超過大流行前的水平。加拿大能源承包協會稱,2022 年鑽探的油氣井數量預計將增加 27%,達到 6,457 口,為 2018 年以來的最高水準。

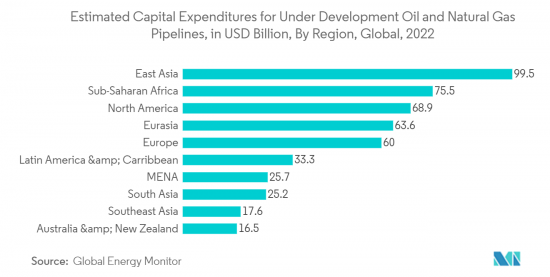

- 此外,對石油和天然氣的需求不斷成長正在推動對石油和天然氣管道基礎設施的投資,從而在所研究的市場中創造機會。例如,根據全球能源監測組織的數據,東亞地區在開發中的石油和天然氣管道方面的投資估計為 995 億美元,位居榜首。

亞太市場成長顯著

- 亞太國家各產業的製造和研發活動市場開拓迅速,佔該地區的高市場佔有率。此外,加大力度確保化學、石油和天然氣等行業工人的安全也支持了該地區的市場成長。

- 印度是製造業和機械工業成長最快的國家之一,創造了對工業閥門的巨大需求。印度政府為設立製造單位的公司提供設施。此外,多項支持製造業的政策也相繼推出。例如,印度政府宣布計劃在2030年將製成品出口額增加至1兆美元。

- 考慮到成長潛力,許多供應商正在擴大在印度的業務。例如,2022 年 2 月,艾默生在印度清奈推出了新的整合製造工廠,為國內和全球客戶提供服務。該工廠將生產電磁閥和氣動閥等流體控制和氣動產品。

- 此外,由於全部區域工業活動的增加,石油和天然氣、化學品、水等製造工廠的增加,中國繼續佔據較大的市場佔有率。因此,對能夠處理高壓的工業閥門的需求不斷增加。例如,2022年4月,蘇伊士透過當地合資企業訂單了中國常熟工業污水處理廠為期30年的建設和營運合約。蘇伊士合資公司將負責污水處理廠的設計、建造和營運,預計於2024年運作。

閥門行業概況

全球閥門市場的特徵是競爭溫和,有許多主導企業。目前,這些主要企業佔據了重要的市場佔有率,並正在積極擴大國際基本客群。為了提高市場佔有率並提高盈利,這些產業巨頭正在結成策略聯盟。

2023 年 6 月,福斯公司宣布其 Valtek Valdisk 高性能蝶閥已獲得授權人核准用於變壓式吸附(PSA) 應用。該核准是在成功完成嚴格的 100 萬次循環耐久性測試後獲得的。新設計的閥門適用於精製和化工廠等設施,這些設施中的控制閥必須在高循環和雙向流動期間保持緊密的關閉能力。

2023 年 5 月,艾默生推出了 ASCO 系列 209 比例流量控制閥。這些閥門的設計符合壓力額定功率、精度、能源效率和流量特性的最高標準。架構也很緊湊。 209 系列可在具有嚴格性能要求的各種設備中實現精確的流體流量控制,包括 HVAC(暖氣、通風和空調)行業、醫療設備、食品和飲料行業等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的敵對關係

- 替代品的威脅

- 產業價值鏈分析

- COVID-19 爆發對產業的影響

第5章市場動態

- 市場促進因素

- 基礎建設相關發展的增加

- 採用新技術

- 市場挑戰

- 缺乏標準化政策

第6章市場區隔

- 按類型

- 球

- 蝴蝶

- 門/手套/檢查

- 插頭

- 控制

- 其他類型

- 按最終用戶產業

- 油和氣

- 發電

- 化學

- 用水和污水

- 礦業

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章競爭形勢

- 公司簡介

- Emerson Electric Co.

- Schlumberger Limited

- Alfa Laval Corporate AB

- Flowserve Corporation

- Crane Co.

- Rotork plc

- IMI Critical Engineering

- Samson Controls Inc.

- KITZ Corporation

- Spirax Sarco Limited

第8章投資分析

第9章市場的未來

The global valves market was valued at USD 79.9 billion in the previous year and is expected to register a CAGR of 5.39%, reaching USD 108.2 billion by the next five years.

Key Highlights

- A valve controls the flow and pressure within a system or process. It forms an essential piping system component that conveys liquids, gases, vapors, slurries, etc. Hence, the growing investment in infrastructure development and the automation of industries are driving the growth of the studied market.

- Rising investments in pipeline infrastructure in the oil and gas sector are expected to boost the installation of industrial valves. Additionally, many developing countries are witnessing increased water supply and sanitation projects by governments, which will likely propel the sales of industrial valves for domestic and agricultural applications. For instance, in May 2022, China announced plans to expand the region's natural gas pipeline grids over the next four years, which would enable it to transport greater volumes to more clients and utilities. Such developments will enhance the demand for industrial valves in the country.

- Furthermore, the growth in investments made by various countries to develop the water and wastewater infrastructure is another major factor driving the studied market's growth, as valves are widely used in water and wastewater plants and distribution pipelines. For instance, in 2022, the Asian Infrastructure Investment Bank (AIIB) approved two major projects: the Dam Rehabilitation and Improvement Project in India and the Bukhara Region Water Supply and Sewerage Project, Phase II in Uzbekistan.

- Many companies are leveraging emerging technologies such as artificial intelligence (AI) and industrial Internet of Things (IIoT) to minimize unplanned downtime and other unfavorable incidents due to valve failures. Valves equipped with sensors are also being increasingly adopted to reduce failures and overall maintenance costs. Adoption of these advanced values is expected to further boost the market over the forecast period.

- The global valve market has many players offering a broad range of solutions targeting applications across various end-user industries. This significantly drives competition among the vendors, encouraging them to develop innovative solutions and adopt unique business strategies to expand their market presence. Hence, the growing market competitiveness is anticipated to drive the studied market's growth further during the forecast period.

- However, the market players need to comply with the various certifications and policies of different regions with respect to valve manufacturing, resulting in diversity in product specifications due to the widespread application of valves in several end-user industries. This acts as a restraint for market growth as the companies have to amend the same product according to the regional policies, making it difficult for them to achieve an ideal cost of installation.

- The COVID-19 pandemic had a negative impact on the oil and gas industry, with oil prices slashing drastically. The decline in the demand for oil and gas due to various restrictions imposed by governments worldwide created a huge gap between supply and demand. Besides oil and gas, water and wastewater treatment and energy and power industries are also among the key end-users of valves. All these industries also witnessed reduced demand due to the global pandemic. However, with the restrictions lifted from almost everywhere, these industries have started recovering gradually, which will accelerate the market growth going forward during the forecast period.

Valves Market Trends

Oil and Gas Vertical Accounts for a Major Market Share

- Many oil and gas operations, such as refining and distribution, rely on pipeline systems. Infrastructure and trustworthy control systems are, therefore, crucial in the business. Oil and gas valves are essential to ensure the safety of the industrial operations of pipelines.

- As an important part of any piping system, valves can be used to control flow rates, isolate and protect equipment, and guide and direct the refining process of crude oil. For instance, gate valves, which are linear motion devices used to open and close the flow of fluid, are commonly used in many piping and pipeline applications.

- With the oil and gas industry expanding owing to a growing demand for petroleum products, vendors operating in the market are launching innovative solutions, targeting applications of the oil & gas industry. For instance, in February 2022, CIRCOR International, Inc. launched its new CIR 3100 control valve. According to the company, the valve is designed for both low and high-pressure drop services and severe applications, including upstream, midstream, and downstream oil and gas, processing, and power generation industries, as well as the maritime and renewables sectors.

- In recent years, the increase in oil and gas exploration and production (E&P) activities is a major trend responsible for driving market growth. Besides, many countries are making heavy investments in drilling activities to tap unconventional resources, creating a positive outlook for the global valves market. For instance, the pace of oil and gas drilling in Canada in 2022 is expected to exceed the pre-pandemic levels. As per the Canadian Association of Energy Contractors, the number of oil and gas wells to be drilled in 2022 is forecasted to rise by 27% to 6,457, which is the highest since 2018.

- Furthermore, the growing demand for oil & gas is driving investment in oil and gas pipeline infrastructure, which in turn is creating opportunities in the studied market. For instance, according to the Global Energy Monitor organization, the East Asian region leads the chart with an estimated investment in under development oil & natural gas pipeline of USD 99.5 billion.

Asia Pacific Market to Grow Significantly

- Due to the growing development in manufacturing and R&D activities in various industries across the Asia Pacific countries, the region holds a high market share. Further, the rising number of initiatives taken to ensure the safety of the workers in industries such as chemicals and oil and gas also support the market growth in the region.

- India is one of the fastest-growing countries in manufacturing sectors and machinery, creating a significant demand for industrial valves. The Indian government provides benefits to companies setting up manufacturing units. It has also outlined various policies to boost the manufacturing sector. For instance, the Indian government has outlined a plan to take the value of its manufactured goods exports to USD 1 trillion by 2030.

- Considering the growth potential, many vendors are expanding their presence in India. For instance, in February 2022, Emerson launched a new integrated manufacturing facility in Chennai, India, to serve the company's local and global customers. This facility will manufacture fluid control and pneumatics products, including solenoid valves and pneumatic valves, among others.

- Furthermore, China continues to account for a significant market share due to the growing industrial activities across the region and the rise in the number of manufacturing plants for oil and gas, chemical, and water, among others. This has increased the demand for industrial valves that can handle high pressure. For instance, in April 2022, SUEZ was awarded a 30-year build-and-operate contract for an industrial wastewater treatment plant in Changshu, China, through a local joint venture. The SUEZ joint venture is responsible for designing, constructing, and operating the wastewater treatment plant, which is expected to be commissioned in 2024.

Valves Industry Overview

The global valves market is characterized by moderate competitiveness and features several influential players. Currently, these key actors hold significant market shares and are actively expanding their customer bases internationally. To bolster their market presence and enhance profitability, these industry leaders engage in strategic collaborations. Notable market players include Emerson Co. Ltd., Alfa Laval Corporate AB, Flowserve Corporation, and Crane Co.

In June 2023, Flowserve Corporation made a noteworthy announcement, stating that its Valtek Valdisk high-performance butterfly valve has received licensor approval for use in pressure swing adsorption (PSA) applications. This approval was granted following the successful completion of a rigorous one-million-cycle endurance test. The newly designed valve is specifically tailored for applications in oil refineries, chemical plants, and other facilities where control valves are required to maintain tight shutoff capabilities amidst high cycles and bi-directional flows.

In May 2023, Emerson introduced the ASCO Series 209 proportional flow control valves. These valves are designed to meet the highest standards in terms of pressure rating, precision, energy efficiency, and flow characteristics. They are also compact in architecture. The Series 209 valves enable precise regulation of fluid flow in a wide range of devices that demand exacting performance, such as those used in the Heating, Ventilation, and Air Conditioning (HVAC) industry, medical equipment, and the food and beverage sector.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness-Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Outbreak on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Infrastructure-Related Developments

- 5.1.2 Adoption of Emerging Technologies

- 5.2 Market Challenges

- 5.2.1 Lack of Standardized Policies

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Ball

- 6.1.2 Butterfly

- 6.1.3 Gate/Globe/Check

- 6.1.4 Plug

- 6.1.5 Control

- 6.1.6 Other Types

- 6.2 By End-User Vertical

- 6.2.1 Oil and Gas

- 6.2.2 Power Generation

- 6.2.3 Chemical

- 6.2.4 Water and Wastewater

- 6.2.5 Mining

- 6.2.6 Other End User Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Emerson Electric Co.

- 7.1.2 Schlumberger Limited

- 7.1.3 Alfa Laval Corporate AB

- 7.1.4 Flowserve Corporation

- 7.1.5 Crane Co.

- 7.1.6 Rotork plc

- 7.1.7 IMI Critical Engineering

- 7.1.8 Samson Controls Inc.

- 7.1.9 KITZ Corporation

- 7.1.10 Spirax Sarco Limited

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2024-2032年按類型(直角迴轉閥門、多迴轉閥門、控制閥)、應用(石油和天然氣行業、水和廢水處理行業)和地區分列的水和燃氣閥門市場報告

2024-2032年按類型(直角迴轉閥門、多迴轉閥門、控制閥)、應用(石油和天然氣行業、水和廢水處理行業)和地區分列的水和燃氣閥門市場報告 按材料類型(不銹鋼、黃銅、碳鋼等)、應用(石油和天然氣、電力、化學品、水和廢水、製藥等)、銷售類型(新銷售、售後市場)分類的單向閥市場報告,以及地區2024-2032

按材料類型(不銹鋼、黃銅、碳鋼等)、應用(石油和天然氣、電力、化學品、水和廢水、製藥等)、銷售類型(新銷售、售後市場)分類的單向閥市場報告,以及地區2024-2032 到 2030 年水閥和燃氣閥市場預測:按閥門類型、材料、應用、最終用戶和地區進行的全球分析

到 2030 年水閥和燃氣閥市場預測:按閥門類型、材料、應用、最終用戶和地區進行的全球分析 2024-2032年按類型(鍍鋅閥門、不銹鋼閥門)、應用(民用、軍用)和地區分類的防爆閥市場

2024-2032年按類型(鍍鋅閥門、不銹鋼閥門)、應用(民用、軍用)和地區分類的防爆閥市場 全球閥門市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測

全球閥門市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測 閥門市場 - 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測

閥門市場 - 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測 水處理產業閥門市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按閥門類型和材料類型

水處理產業閥門市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按閥門類型和材料類型 恆溫散熱器閥門的全球市場 2024-2028

恆溫散熱器閥門的全球市場 2024-2028 燃氣閥門市場 - 按產品類型(閘閥、控制閥、球閥、蝶閥、旋塞閥)、按應用(石油和天然氣生產、天然氣管道運輸、市政燃氣)、最終用戶和預測,2024 - 2032 年

燃氣閥門市場 - 按產品類型(閘閥、控制閥、球閥、蝶閥、旋塞閥)、按應用(石油和天然氣生產、天然氣管道運輸、市政燃氣)、最終用戶和預測,2024 - 2032 年 支氣管瓣膜市場、份額、規模、趨勢、行業分析報告:按產品類型、最終用戶、地區、細分市場、預測,2024-2032 年

支氣管瓣膜市場、份額、規模、趨勢、行業分析報告:按產品類型、最終用戶、地區、細分市場、預測,2024-2032 年