|

市場調查報告書

商品編碼

1406893

倉庫自動化:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Warehouse Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

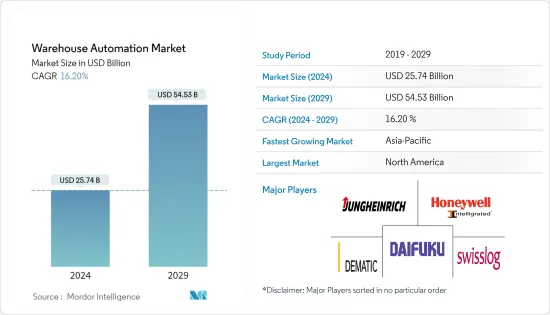

倉庫自動化市場規模預計到 2024 年為 257.4 億美元,預計到 2029 年將達到 545.3 億美元,在預測期內(2024-2029 年)複合年成長率為 16.20%。

主要亮點

- 物流自動化是指使用控制系統、機械和軟體來提高業務效率。它通常適用於必須在倉庫或配送中心執行且需要最少人工干預的流程。自動化物流的好處包括改善客戶服務、擴充性和速度、組織控制以及減少錯誤。

- 倉庫自動化可以在最少的人工協助下,自動將庫存轉移到倉庫、在倉庫內以及從倉庫轉移到客戶手中。作為自動化計劃的一部分,公司可以消除涉及重複體力勞動以及手動資料輸入和分析的集中業務。

- 此外,全球電子商務行業的成長以及對高效倉儲和庫存管理日益成長的需求正在推動市場研究。倉庫管理自動化對於降低整體業務成本和減少產品交付錯誤非常有用。著名的 3PL 公司和倉庫自動化解決方案的重要最終用戶 DHL 表示,儘管有好處,但 80% 的倉庫「仍然是手動操作,沒有自動化的支援」。此外,倉庫,即使用輸送機、分類機和拾取解決方案的倉庫,佔所有倉庫的 15%。同時,目前只有 5% 的倉庫實現了自動化。

- 不可預測的需求以及缺乏透明度以及與供應鏈的協作是許多製造商實現其業務目標的主要障礙。然而,希望透過評估複雜性的來源和最佳化倉庫管理,製造商將更了解其供應鏈,同時有效地應對波動的需求。

- 同樣,倉庫管理系統(WMS)可以提高工作流程效率,減少錯誤,節省與錯誤相關的成本,並減少訂單處理週轉時間,但 WMS 作業對於電子商務企業來說既耗時又昂貴。需要大量的硬體初期成本、廣泛的培訓以及額外的每月維護成本。

- 隨著公司尋求簡化物流和降低成本,COVID-19 增加了對非接觸式環境的關注,並增加了對自動化技術的需求。因此,許多公司正在採用倉庫管理系統 (WMS) 等技術來最佳化任務,例如定位小包裹以及選擇正確的包裝尺寸和類型。

倉庫自動化市場趨勢

零售業顯著成長

- 倉庫自動化應用於各種零售業,包括電子商務和雜貨店。倉庫自動化具有多種好處,從提高生產力到減少與勞動力相關的風險。電子商務倉庫自動化包括將技術引入物流設施以提高營運績效。根據美國商務部和人口普查局的數據,2022 年電子商務銷售額總額為 10,341 億美元,較 2021 年成長 7.7%(0.4%)。 2022年零售總額較2021年成長8.1%(0.9%)。

- 為了滿足這一巨大需求,倉庫自動化正在迅速擴展,將手動倉庫轉變為自動化履約業務。倉庫自動化對於大規模滿足客戶需求並同時控制未來的營運成本至關重要。如今,許多零售商正在實施倉庫自動化解決方案,以跟上電子商務物流業務規模和複雜性不斷成長的步伐,並更快、更經濟高效地滿足不斷成長的客戶需求。

- 零售倉庫可以配備各種自動化解決方案來完成從自動化搬運設備到儲存產品再到數位系統的所有工作,以最大限度地實現產品組織。領先的零售商正在利用自動導引車 (AGV) 與工人以及更高水準的自動化、自動移動機器人 (AMR) 一起工作,以簡化電子商務和全通路設施的履約業務。

- 此外,為了適應快速擴張的電子商務行業並考慮從全球大流行中汲取的經驗教訓,領先的零售商正在努力提高其倉庫的反應、彈性和可靠性。例如,2022 年 4 月,亞馬遜推出了亞馬遜工業 (Amazon Industrial),這是一項專注於自動化和職場機器人技術的 10 億美元新興企業資金計劃,旨在「刺激供應鏈、履約和物流的創新」。,設立了創新基金(AIIF)。

亞太地區預計將佔據較大佔有率

- 由於該地區工業數量不斷增加以及自動化整合以提高投資收益(ROI),亞太地區倉庫自動化市場正在顯著擴大。預計亞太地區的倉庫自動化將由中國主導,中國自動化產品的生產、銷售和貿易都在成長。

- 此外,隨著中國政府計劃根據「中國製造2025」國家計劃將中國從製造業大國轉變為全球製造強國,倉庫自動化產業預計將受益於此優勢。該計劃還包括加強中國機器人供應商的實力,並進一步提高市場佔有率。

- 倉庫自動化需求包括自動化供應鏈,並得到有利投資的進一步支持。該國正在探索多項投資,以進一步推動市場成長,主要主要企業向該地區擴張,創業投資向未來性的新興企業。馬蘇。

- 製造業也已成為印度高成長產業之一。例如,「印度製造」計畫使印度成為世界地圖上重要的製造地,並讓印度經濟獲得全球認可。印度製造宣傳活動正在支援印度多個新推出的工業機器人,並促進倉庫自動化機會。

倉儲自動化產業概況

倉庫自動化市場競爭激烈。該市場的一些主要全球參與者包括德馬泰克集團、大福有限公司、Swisslog Holding AG、Honeywell Intelligerated 和 Jungheinrich AG。產品發布、收購和合作是倉庫自動化產業市場參與者採取的關鍵策略。

2023年1月,永恆力股份公司收購了總部位於美國印第安納州的貨架和倉庫自動化解決方案領先供應商Storage Solutions Group,以加強其進入美國倉庫管理和自動化市場的能力。

此外,2022 年 9 月,德馬泰克將與 AppShop 合作,提供與雜貨業共同發展的全面履約服務。此次合作將為希望發展履約業務的雜貨商提供儲存和管理消費者資料的工具。德馬泰克提供自動化體驗以及簡單的軟體來連接到目前的 Upshop 流程。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 產業價值鏈分析

- 評估 COVID-19 對產業的影響

- 倉庫投資場景

- 宏觀經濟因素對倉庫自動化市場的影響

第5章市場動態

- 市場促進因素

- 電子商務行業的快速成長和客戶期望

- 增加製造複雜性和技術可用性

- 市場課題

- 高資金投入

第6章市場區隔

- 依成分

- 硬體

- 移動機器人(AGV、AMR)

- 自動搜尋系統(AS/RS)

- 自動輸送機/分類系統

- 卸垛/碼垛系統

- 自動識別和資料收集(AIDC)

- 工件拾取機器人

- 軟體(倉庫管理系統(WMS)、倉庫執行系統(WES))

- 服務(附加價值服務、維護等)

- 硬體

- 依最終用戶

- 食品和飲料(包括生產設施和配送中心)

- 小包裹

- 零售

- 服飾

- 製造(耐用/非耐用)

- 其他最終用戶產業

- 依地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第7章 競爭形勢

- 公司簡介

- Dematic Group(Kion Group AG)

- Daifuku Co. Limited

- Swisslog Holding AG(KUKA AG)

- Honeywell Intelligrated(Honeywell International Inc.)

- Jungheinrich AG

- Murata Machinery Ltd

- Knapp AG

- TGW Logistics Group GmbH

- Kardex Group

- Mecalux SA

- BEUMER Group GmbH & Co. KG

- SSI Schaefer AG

- Vanderlande Industries BV

- WITRON Logistik+Informatik GmbH

- Oracle Corporation

- One Network Enterprises Inc.

- SAP SE

第8章投資分析

第9章市場的未來

The Warehouse Automation Market size is estimated at USD 25.74 billion in 2024, and is expected to reach USD 54.53 billion by 2029, growing at a CAGR of 16.20% during the forecast period (2024-2029).

Key Highlights

- Automation in logistics refers to using control systems, machinery, and software to enhance the efficiency of operations. It usually applies to the processes that must be performed in a warehouse or distribution center, which requires minimal human intervention. Some benefits of automation logistics are improved customer service, scalability and speed, organizational control, and reduction of mistakes, among others.

- Warehouse automation automates inventory movement into, within, and out of warehouses to customers with minimal human assistance. As part of an automation project, a business can eliminate labor-intensive duties that involve repetitive physical work and manual data entry and analysis.

- Moreover, the growth in the e-commerce industry worldwide and the growing need for efficient warehousing and inventory management are driving the market studied. Automation in warehousing offers extreme convenience when cutting down overall business costs and reducing errors in product deliveries. According to DHL, a prominent 3PL company and a significant end-user of warehouse automation solutions, despite the advantages, 80% of warehouses are 'still manually operated with no supporting automation.' Furthermore, warehouses, i.e., those that use conveyors, sorters, and pick and place solutions, account for 15% of the entire warehouses. In contrast, only 5% of current warehouses are automated.

- Unpredictable demand and a lack of transparency and collaboration with the supply chain present a significant barrier to reaching business goals for many manufacturers. However, when manufacturers evaluate the sources of complexity and optimize warehouse management, they are expected to efficiently meet variable demand while increasing their view of the supply chain.

- Similarly, while warehouse management systems (WMS) can improve workflow efficiency, reduce errors, save on costs associated with errors, and get faster turn-around time for order fulfillment, running a WMS can be time-consuming and expensive for an e-commerce business. It requires huge upfront costs for hardware, extensive training, and additional monthly costs for upkeep.

- COVID-19 increased the focus on a contactless environment as companies looked to improve logistics efficiency and reduce expenses, giving rise to a higher demand for automated technologies. As a result, significant companies adopted technologies such as warehouse management systems (WMS) for optimizing tasks like locating parcels and choosing the right size and type of packaging.

Warehouse Automation Market Trends

Retail to Have a Significant Growth

- Warehouse automation is used in various retail activities, including e-commerce and grocery. For warehouses, automation has multiple advantages, from boosting production to lowering labor-related risks. E-commerce warehouse automation consists of implementing technologies in logistics facilities to boost operational performance. According to the Census Bureau of the Department of Commerce, Total e-commerce sales for 2022 were USD 1,034.1 billion, an increase of 7.7 percent (±0.4%) from 2021. Total retail sales in 2022 increased by 8.1 percent (±0.9%) from 2021.

- To address this massive demand, warehouse automation is rapidly expanding to transform manual warehouses into automated fulfillment operations, which are proving vital to meeting customer demand at scale while managing operating costs in the future. Currently, many retailers are increasingly implementing warehouse automation solutions that seek to handle the growing scale and complexity of their e-commerce logistics operations and meet the ever-increasing demand of their customers more quickly and cost-effectively.

- A retail warehouse can be outfitted with various automated solutions to carry out all tasks, from automatic handling equipment for storing products to digital systems that maximize product organization. Big retailers are utilizing automated guided vehicles (AGVs) and the next level of automation-automated mobile robots (AMRs)-working alongside workers to simplify the fulfillment operations of their e-commerce and omnichannel facilities.

- Moreover, to meet the rapidly expanding e-commerce sector and consider the lessons learned from the worldwide pandemic, leading retailers strive to make warehouses responsive, resilient, and dependable. For instance, in April 2022, Amazon established the Amazon Industrial Innovation Fund (AIIF), a USD 1 billion startup funding program that will be used to "spur supply chain, fulfillment, and logistics innovation," focusing on automation and workplace robotics.

Asia-Pacific is Expected to Hold Significant Share

- The market for warehouse automation in the Asia-Pacific is expanding significantly due to the rising number of industries in the region and their integration with automation to increase the return on investment (ROI). The Asia-Pacific warehouse automation is predicted to be dominated by China with the growing production, sales, and trade of automation products.

- Moreover, The warehouse automation industry is expected to benefit from China's dominance in the manufacturing sector as the Chinese government plans to transform China from a manufacturing giant to a global manufacturing power under the national plan "Made in China 2025". This plan includes strengthening Chinese robot suppliers and further surging their market shares in China and abroad.

- The demand for warehouse automation includes an automated supply chain, further supported by favorable investments. The country has been marked with several investments to further the market's growth studied, with major key players expanding into the region and introducing funds by venture capitalists in emerging start-ups with potential.

- Manufacturing has emerged as one of the high-growth sectors in India as well. For instance, the Make in India program places India on the world map as a significant manufacturing hub and provides global recognition to the Indian economy. The Made in India campaign has bolstered multiple new launches in industrial robots in the country, thus driving opportunities for warehouse automation.

Warehouse Automation Industry Overview

The warehouse automation market is highly competitive. Some key global players in this market are Dematic Group, Daifuku Co. Limited, Swisslog Holding AG, Honeywell Intelligrated, and Jungheinrich AG. Product launch, acquisition, and partnership are key strategies market players operating in the warehouse automation industry adopt.

In January 2023, JungheinrichAG acquired Indiana-based Storage Solutions group, a leading provider of racking and warehouse automation solutions in the United States, to gain enhanced access to the US warehousing and automation market.

Further, in September 2022, Dematic partnered with Upshopto to offer integrated fulfillment services that grow with the grocery industry. With the help of the alliance, grocery stores wishing to expand their fulfillment businesses will have access to tools that let them store and manage their consumer data. Dematic will offer its experience in automation along with simple software to connect with current Upshop processes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

- 4.5 Warehouse Investment Scenario

- 4.6 Impact of Macro-economic Factors on the Warehouse Automation Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Exponential Growth of the E-commerce Industry and Customer Expectation

- 5.1.2 Increasing Manufacturing Complexity and Technology Availability

- 5.2 Market Challenges

- 5.2.1 High Capital Investment

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.1.1 Mobile Robots (AGV, AMR)

- 6.1.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3 Automated Conveyor & Sorting Systems

- 6.1.1.4 De-palletizing/Palletizing Systems

- 6.1.1.5 Automatic Identification and Data Collection (AIDC)

- 6.1.1.6 Piece Picking Robots

- 6.1.2 Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES))

- 6.1.3 Services (Value Added Services, Maintenance, etc.)

- 6.1.1 Hardware

- 6.2 By End-User

- 6.2.1 Food and Beverage (Including Manufacturing Facilities and Distribution Centers)

- 6.2.2 Post and Parcel

- 6.2.3 Retail

- 6.2.4 Apparel

- 6.2.5 Manufacturing (Durable and Non-Durable)

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dematic Group (Kion Group AG)

- 7.1.2 Daifuku Co. Limited

- 7.1.3 Swisslog Holding AG (KUKA AG)

- 7.1.4 Honeywell Intelligrated (Honeywell International Inc.)

- 7.1.5 Jungheinrich AG

- 7.1.6 Murata Machinery Ltd

- 7.1.7 Knapp AG

- 7.1.8 TGW Logistics Group GmbH

- 7.1.9 Kardex Group

- 7.1.10 Mecalux SA

- 7.1.11 BEUMER Group GmbH & Co. KG

- 7.1.12 SSI Schaefer AG

- 7.1.13 Vanderlande Industries BV

- 7.1.14 WITRON Logistik + Informatik GmbH

- 7.1.15 Oracle Corporation

- 7.1.16 One Network Enterprises Inc.

- 7.1.17 SAP SE

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2024 年倉庫自動化世界市場報告

2024 年倉庫自動化世界市場報告 2024 年貼片機全球市場報告

2024 年貼片機全球市場報告 全球倉庫自動化市場:趨勢、預測、競爭分析

全球倉庫自動化市場:趨勢、預測、競爭分析 自動化倉庫揀選市場:按揀選類型、方法、發展、應用分類 - 2024-2030 年全球預測

自動化倉庫揀選市場:按揀選類型、方法、發展、應用分類 - 2024-2030 年全球預測 取放機市場 - 2023-2031 年全球產業分析、分享、成長、趨勢與預測

取放機市場 - 2023-2031 年全球產業分析、分享、成長、趨勢與預測 倉庫自動化市場(物流自動化):到2028年將達到440億美元-按技術、按行業、按地區劃分國家(第四版)

倉庫自動化市場(物流自動化):到2028年將達到440億美元-按技術、按行業、按地區劃分國家(第四版) 自動導引車(AGV)/自主運輸機器人(AMR)的全球市場 - 預測(2024-2030)

自動導引車(AGV)/自主運輸機器人(AMR)的全球市場 - 預測(2024-2030) 倉庫自動化市場 - 2018-2028F 全球產業規模、佔有率、趨勢、機會和預測,按產品、自動化程度、技術、按應用、垂直、地區、競爭細分

倉庫自動化市場 - 2018-2028F 全球產業規模、佔有率、趨勢、機會和預測,按產品、自動化程度、技術、按應用、垂直、地區、競爭細分 語音揀選解決方案市場、份額、規模、趨勢、產業分析報告:按組件、產業、地區、細分市場預測,2023-2032 年

語音揀選解決方案市場、份額、規模、趨勢、產業分析報告:按組件、產業、地區、細分市場預測,2023-2032 年 倉庫自動化市場、份額、規模、趨勢、行業分析報告:按類型、按技術、按應用、按地區、細分市場趨勢,2023-2032

倉庫自動化市場、份額、規模、趨勢、行業分析報告:按類型、按技術、按應用、按地區、細分市場趨勢,2023-2032