|

市場調查報告書

商品編碼

1406198

雲端備份:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029Cloud Backup - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

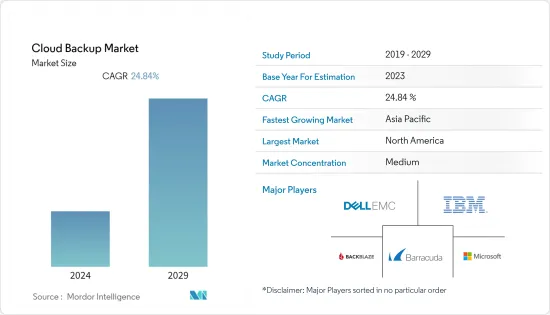

雲端備份市場規模預計將從2024年的57.1億美元成長到2029年的172.9億美元,預測期內複合年成長率為24.84%。

企業採用雲端備份的主要驅動力是面對技術創新加速和競爭顛覆時對敏捷性和彈性的需求。

主要亮點

- 市場主要企業正在增加對雲端技術的投資。例如,Veeam Software 與 Microsoft Azure 合作提供新的 Veeam Backup,這是一款適用於 Microsoft Azure 的企業級雲端備份和復原解決方案。這款新產品可協助客戶和服務供應商將更多應用程式和資料遷移到 Azure,並經濟高效、安全且輕鬆地保護其 Azure 雲端應用程式和資料。

- 例如,2023 年 4 月,BETSOL 推出了 Zmanda Endpoint Backup,這是一種適用於筆記型電腦和 Windows 桌上型電腦的雲端基礎的備份解決方案。 Zmanda Endpoint Backup 是 Zmanda 不斷成長的功能陣容中的最新成員。 Zmanda Endpoint Backup 為您的組織提供可擴充、雲端基礎的集中端點管理。它易於部署並提供經過驗證的備份引擎的可靠性。

- 此外,資料遺失已成為所有行業的主要問題。在最近的一項調查中,大約 33% 的受訪者將資料遺失歸因於硬體或系統故障,而 29% 的受訪者將資料遺失歸因於人為錯誤或勒索軟體。據估計,在災難期間失去伺服器 10 天或更長時間的組織中,高達 93% 在隨後的 12 個月內申請破產,而 43% 的組織從未重新啟動。另一項針對美國和加拿大使用雲端基礎的資料保護服務的IT 專業人員的行業調查發現,雖然74% 的受訪者完全依賴本機Microsoft 365 服務進行備份,但只有15% 的人能夠恢復100%的資料。

- 隨著網路攻擊的增加,Google和微軟等公司正致力於提高其雲端環境的安全性。過去一年,亞馬遜網路服務 (AWS)、微軟 Azure 和谷歌雲端在網路安全領域進行了各種收購。 2022年3月,Google以約54億美元收購網路安全公司Mandiant,為Google雲端提供威脅情報服務。

- 近年來,雲端的採用顯著成長。例如,根據 IBM 的分析,單一製造車間每月可以產生超過 2,200 Terabyte的資料。一條生產線每天可以產生超過 70 Terabyte的資料,而且許多資料仍未分析和保護。因此,企業正在轉向雲端儲存來保護和利用這些資料。

- 此外,IBM 透露,90% 的資料是在過去兩年創建的。產生的大量資料正在增加整個企業對低成本資料備份和儲存的需求。自動備份、惡意軟體防護、加密雲端儲存、檔案級復原、時間點復原等是市場趨勢。

- 但另一方面,雲端備份解決方案是防禦網路攻擊和資料外洩的完整工具之一。但是,如果不加以管理,攻擊者可以輕鬆滲透備份伺服器的資料庫並利用它來攻擊使用者。因此,隱私和安全性問題是採用雲端備份解決方案的主要障礙。

- 隨著雲端備份市場使用的增加,關鍵任務數位產業中未受管理的風險數量呈現爆炸性成長。雲端安全態勢管理 (CSPM) 可實現跨不同雲端基礎架構的雲端安全管理自動化。這促使該領域的收購活動增加。

- 例如,Google在 2022 年 3 月宣布同意以 54 億美元收購網路安全公司 Mandiant,這表明領先的雲端供應商將做出更廣泛的努力,為企業提供更好的保護,抵禦日益成長的威脅。該交易達成之際,俄羅斯入侵烏克蘭進一步增加了企業投資網路安全保護的需求。它也反映了這家雲端巨頭的成長領域。 Mandiant 2021年持續營運收益預計將成長21%,達到8.43億美元,2022年獨立收益預計將超過5.5億美元。

雲端備份市場趨勢

BFSI預計將成為最大規模的招聘

- 銀行業擴大採用數位銀行業務和投資解決方案,BFSI 領域對雲端儲存/備份的需求不斷增加。此外,一些金融部門正在轉向雲端技術以獲得競爭優勢,從而實現創新、競爭和安全。

- 此外,政府機構和私人公司正在與許多公司合作,預計未來五年市場將出現新的成長機會。例如,瑞銀和微軟公司正在擴大合作,以在未來五年內擴大瑞銀的公有雲足跡。 UBS 是一家跨國投資銀行和金融服務公司,計劃在 Microsoft Azure 上運作一半以上的應用程式,包括 UBS 主要雲端平台上的關鍵工作負載。此次合作將加速瑞銀的雲端優先策略及其全球技術資產的現代化。

- 例如,IBM 正在使用混合雲幫助兩家歐洲銀行集團數位化。西班牙銀行 IT 服務供應商 Rural Services Informaticos (RSI) 將利用 IBM 和 Red Hat 的混合技術和行業專業知識,透過 Cloud Office 平台增強其數位產品和服務。因此,許多供應商正在投資混合雲端解決方案,以消除主機管理、維護、更新和擴展服務營運的需求。這些措施預計將增加 BFSI 領域雲端備份解決方案的使用。

- 此外,銀行業資料外洩的數量不斷增加,促使銀行轉向雲端備份解決方案,以便從任何災難中恢復。公有雲解決方案提供增強的備份資源,以確保災難下的業務永續營運。

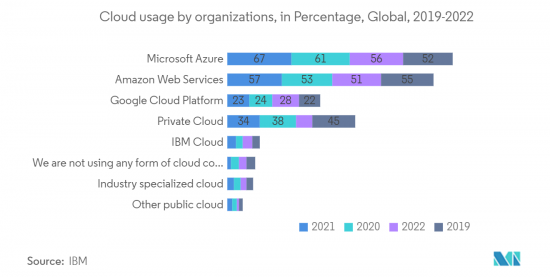

- 雲端基礎的即時付款解決方案的成長趨勢是由於彈性為零售商提供即時付款洞察。在 BFSI,數位付款的採用在全球範圍內不斷增加,預計該市場將在未來五年內成長。根據IBM對組織雲端使用情況的調查,微軟Azure去年的雲端使用率最高,達56%。

預計北美將主導市場

- 各種最終用戶垂直領域的技術的早期採用以及該地區市場領先公司的存在使北美成為一個關鍵的區域市場,並預計將在整個預測期內繼續佔據主導地位。此外,新技術的早期採用、對雲端基礎的解決方案的研發的大量投資以及IT基礎設施的加強預計將進一步推動市場成長。

- 預計未來五年,美國將佔雲端基礎的儲存和備份解決方案需求的很大一部分。支持該市場投資的關鍵因素是新技術的持續發展和應用,釋放了以前被認為是商業性的容量。隨著該國繼續在醫療保健、零售、通訊和製造領域進行投資,雲端基礎的解決方案市場預計將在未來五年內大幅成長。

- 該國已採取各種舉措使其基礎設施現代化。 為了實現這一目標,美國陸軍計劃投資高達2.49億美元來部署私有雲端計算服務和數據中心。 通用動力公司(General Dynamics)、惠普(HP)和諾斯羅普·格魯曼公司(Northrop Grumman)是陸軍私有雲端協定中被選中的服務提供者之一,他們提供雲端計算服務,使用安全的私有雲端整合數據中心。

- 在美國,雲端為基礎的運算的採用進展迅速,國內資料中心的數量也相應增加。根據瑞士信貸統計,美國目前擁有全球最多的超大規模資料中心,佔全國所有超大規模資料中心的三分之一以上。

- 此外,該地區政府舉措的增加也推動了整個預測期內市場的顯著增長。 例如,去年 11 月,GDIT(通用動力資訊技術公司)與雲端、電信和網路巨頭組成了一個新小組,目標是擴大 5G、無線和邊緣技術在政府機構中的採用。 GDIT 5G 和邊緣加速聯盟包括 Cisco、Amazon Web Services (AWS)、T-Mobile US、Splunk 和 Dell Technologies。 利用GDIT的Advanced Wireless Emerge Lab,該公司專注於開發用例、原型和服務,以促進5G和邊緣功能的採用。 它們為聯邦、州和地方機構提供物流、供應鏈和智慧基礎設施等用例支援。

- 此外,加拿大政府還採取了「雲端優先」策略,在啟動資訊技術投資、舉措、策略和計劃時,將雲端服務確定為主要交付選項並引用。雲端還允許政府利用私人提供者的創新,並使資訊技術更加敏捷。此類措施預計將為雲端備份市場提供許多機會,因為這種模型可實現私有雲端的安全性和公有公共雲端的彈性。

雲端備份產業概況

隨著全球多個市場參與者的出現,雲端備份市場的競爭形勢變得更加緊密。資料儲存雲端處理的日益採用和資料生成的顯著成長預計將推動市場的發展。因此,Dell EMC、IBM Corporation、Backblaze Inc. 和 Barracuda Networks, Inc. 等市場參與企業正在提供比同行更強大的市場解決方案,以最大限度地提高市場吸引力。並實施了多項創新。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 資料產生的顯著增加推動了對低成本、大容量儲存的需求

- SaaS 和其他類似解決方案的採用率增加

- 雲端運算在企業中的採用率不斷提高

- 市場課題

- 政府法規和合規性

- 關於雲端儲存的隱私和安全問題

第6章市場區隔

- 依成分

- 解決方案

- 服務

- 依部署方式

- 公共雲端

- 私有雲端

- 混合雲端

- 依最終用戶產業

- BFSI

- 資訊科技/通訊

- 媒體娛樂

- 零售

- 衛生保健

- 其他

- 依地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 世界其他地區

第7章 競爭形勢

- 公司簡介

- IBM Corporation

- Dell EMC

- Backblaze Inc.

- Acronis International GmbH

- Arcserve LLC

- Rubrik

- Veritas Technologies

- Barracuda Networks Inc.

- Carbonite Inc.

- Commvault Systems Inc.

- Cohesity Inc.

第8章投資分析

第9章 市場的未來

The Cloud Backup Market size is expected to grow from USD 5.71 billion in 2024 to USD 17.29 billion by 2029, registering a CAGR of 24.84% during the forecast period. The primary driver for adopting cloud backup across businesses is the need for agility and flexibility in the face of accelerating innovation and disruptions from competitors due to the increase in cloud adoption across both big and small.

Key Highlights

- Key players in the market are increasing investments in cloud technologies. For Instance, Veeam Software has partnered with Microsoft Azure to provide New Veeam Backup, an enterprise-ready cloud backup and recovery solution for Microsoft Azure. The new product will help customers and service providers to migrate more apps and data to Azure and to cost-effectively, securely, and easily protect cloud applications and data in Azure.

- For instance, in April 2023, BETSOL launched Zmanda Endpoint Backup, a cloud-based backup solution for laptop computers and Windows desktops. It is the most recent addition to Zmanda's expanding feature lineup. Zmanda Endpoint Backup provides scalable, cloud-based, centralized management of the entire organization's endpoints. It's simple to deploy and brings the reliability of our proven backup engine.

- Furthermore, data loss is becoming a significant concern across all industries. In one recent survey, around 33% blamed hardware or system failure for data loss, while 29% reported that their companies lost data due to human error or ransomware. It is estimated that up to 93% of organizations that lose servers for 10 days or more during a disaster filed for bankruptcy within the next 12 months, with 43% never reopening. Another industrial survey of the US and Canadian IT professionals using cloud-based data protection services found that while 74% of respondents rely only on the native Microsoft 365 services for backup, only 15% could recover 100% of their data.

- As cyberattacks keep increasing, companies such as Google and Microsoft, among others, are aiming to make their cloud environments more secure. Amazon Web Services (AWS), Microsoft Azure, and Google Cloud have made various acquisitions in the cybersecurity space over the past year. In March 2022, Google acquired Mandiant, a cybersecurity company, for about USD 5.4 billion to provide threat intelligence services to Google Cloud.

- In recent years, cloud adoption has significantly grown. For instance, according to an IBM analysis, a single manufacturing site may generate more than 2,200 terabytes of data in a month. A single production line can generate more than 70 terabytes per day-yet the vast majority of data remains unanalyzed and unprotected. Therefore, companies are moving to cloud storage to secure and utilize this data.

- Furthermore, IBM revealed that 90% of the data was created in the previous two years. Because of the large amount of data generated, there is a rising demand for low-cost data backup/storage across companies. Automated backup, Malware protection, Encrypted cloud storage, File-level Recovery, and Point-in-time Restore, among others, are some trending services in the market.

- However, Cloud backup solutions, on the other hand, are one of the complete tools for defending against cyber-attacks and data breaches. However, if unmanaged, attackers may smoothly infiltrate the backup server's database and utilize it against the user. Hence, privacy and security issues are major hindrances to adopting cloud backup solutions.

- As the cloud backup market sees an increase in use, there has been an explosion in the number of unmanaged risks in the mission-critical digital industry. Cloud Security Posture Management (CSPM) automates cloud security management across the diverse cloud infrastructure. Due to this, there has been an increased acquisition activity in the segment.

- For instance, Google's agreement to buy cybersecurity firm Mandiant for USD 5.4 Billion, announced in March 2022, reflects broad efforts by leading cloud providers to provide enterprises with better protection against a growing set of threats. The deal comes as the Russian invasion of Ukraine further illustrates the need for companies to invest in cybersecurity protections. It also reflects the growth areas of cloud giants. Mandiant's revenue from continuing operations in 2021 was projected to increase by 21% to USD 843 Million, and in 2022, the revenue as an independent company was projected to exceed USD 550 Million.

Cloud Backup Market Trends

BFSI Expected to Exhibit Maximum Adoption

- The banking industry is increasingly embracing digital banking and investing solutions, which is increasing demand for Cloud storage/backup in the BFSI sector. Further, some financial sector businesses are transitioning to cloud technologies to obtain a competitive advantage, enabling innovation, customization, and security.

- Further, Government and private organizations are collaborating with many companies to anticipate new growth opportunities in the market over the next five years. For Instance, UBS and Microsoft Corp have expanded their collaboration to boost UBS's public cloud footprint over the next five years. UBS (multinational investment bank and financial services company) intends to operate more than half of its applications, running on Microsoft Azure, including critical workloads on UBS's primary cloud platform. The partnership furthers UBS's cloud-first strategy and the modernization of its global technology estate.

- For instance, IBM is using a Hybrid Cloud to Help Two European Banking Groups Go Digital. Rural Services Informaticos (RSI), a Spanish banking IT services provider, will increase its digital product and service offerings using hybrid cloud technology and industry expertise from IBM and Red Hat to boost its digital products and service offerings through a Cloud Office platform. Hence, many vendors are investing money in hybrid cloud solutions to eliminate the need to manage hosts, maintain, update, and scale service operations. These developments are projected to increase the usage of cloud backup solutions in the BFSI sector.

- Furthermore, the growing number of data breaches in the banking sector is driving banks to use cloud backup solutions that will allow them to recover from any disaster. Public cloud solutions provide an enhanced backup resource to ensure business continuity despite a disaster.

- The growing trends for cloud-based real-time payment solutions can be attributed to their flexibility in providing real-time payment insights to retailers. The growing adoption of digital payment methods in BFSI globally is anticipated to drive market growth over the next five years. According to an IBM survey on Cloud usage by organizations, Microsoft Azure has the highest percentage of 56% of cloud usage in the last year.

North America Expected to Dominate the Market

- With the early adoption of technologies across various end-user verticals and the presence of market leaders in the region, North America stood as the leading regional market and is expected to continue its dominance throughout the forecast period. Also, early adoption of new technologies, considerable investments in R&D for cloud-based solutions, and enhanced IT infrastructure are expected to drive market growth further.

- The United States is anticipated to occupy a crucial portion of the demand for cloud-based storage/backup solutions over the next five years. A significant driver behind the investments in the market is the continuous evolution and application of new technologies to unlock volumes that were previously considered non-commercial. With a series of investments across healthcare, retail, communications, and manufacturing applications in the country, the market for cloud-based solutions is expected to witness significant growth over the next five years.

- The country has made multiple efforts to modernize its infrastructure. To achieve this, the US Army planned to spend up to USD 249 million to deploy private cloud computing services and data centers. General Dynamics, HP, and Northrop Grumman were among the service providers selected for the Army Private Cloud contract, providing cloud computing services to consolidate data centers using a secure private cloud.

- In the United States, the adoption of cloud-based computing is increasing rapidly, owing to which the data centers in the country are also witnessing an increase. According to Credit Suisse, the United States currently accounts for the highest number of hyperscale data centers worldwide, holding more than one-third of the total hyperscale data centers in the country.

- Furthermore, the rise in government initiatives within the region is also helping the market to grow considerably throughout the forecast period. For instance, in November last year, General Dynamics Information Technology (GDIT) formed a new group with cloud, telecom, and networking giants targeted at growing the adoption of 5G, wireless, and edge technologies across government agencies. The GDIT 5G and Edge Accelerate Coalition includes Cisco, Amazon Web Services (AWS), T-Mobile US, Splunk, and Dell Technologies. It's focused on using GDIT's Advanced Wireless Emerge Lab to develop use cases, prototypes, and services to make deploying 5G and edge capabilities easier. These will support federal, state, and local agencies for use cases, including logistics, supply chain, smart infrastructure, etc.

- Moreover, the government of Canada has adopted a "cloud-first" strategy, whereby cloud services are identified and estimated as the principal delivery option when initiating information technology investments, initiatives, strategies, and projects. The cloud will also let the government harness the innovation of private-sector providers and thus make its information technology more agile. Such initiatives are expected to offer plenty of opportunities to the cloud backup market, as this model enables private cloud security and public cloud flexibility.

Cloud Backup Industry Overview

The Cloud Backup Market's competitive landscape could be more cohesive due to the presence of several global market players. The increasing adoption of cloud computing for data storage and a massive increase in data generation is expected to boost the market. Hence, market players such as Dell EMC, IBM Corporation, Backblaze Inc., and Barracuda Networks, Inc. are making several innovations to provide enhanced solutions in the market compared to their peers and gain maximum market traction.

In March 2022, Barracuda disclosed that it added three new cloud-to-cloud backup data centers in France, UAE, and India. Now, a total of 11 regions would be included in Barracuda's solution. Office 365 backup data for clients would be stored locally in each location, which is essential for clients who work in regulated industries or reside in nations with strict data protection laws. Incorporating these new data center locations would help satisfy customer needs for local data protection.

In February 2022, IBM acquired Neudesic, a major cloud services consultant in the United States specializing mainly in the Microsoft Azure platform and offering expertise in multi-cloud. This acquisition was to significantly enhance IBM's offering of hybrid multi-cloud services and further advance the company's hybrid cloud and AI strategy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Massive Growth in Data Generation Stimulating the Demand for Larger Storage Space at Low Cost

- 5.1.2 Increasing Adoption of SaaS and Other Similar Solutions

- 5.1.3 Increasing Adoption of Cloud Computing Amongst Enterprises

- 5.2 Market Challenges

- 5.2.1 Government Regulations and Compliance

- 5.2.2 Privacy and Security Concerns regarding Cloud Storage

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Solution

- 6.1.2 Services

- 6.2 By Deployment Mode

- 6.2.1 Public Cloud

- 6.2.2 Private Cloud

- 6.2.3 Hybrid Cloud

- 6.3 By End-User Industry

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Media and Entertainment

- 6.3.4 Retail

- 6.3.5 Healthcare

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Dell EMC

- 7.1.3 Backblaze Inc.

- 7.1.4 Acronis International GmbH

- 7.1.5 Arcserve LLC

- 7.1.6 Rubrik

- 7.1.7 Veritas Technologies

- 7.1.8 Barracuda Networks Inc.

- 7.1.9 Carbonite Inc.

- 7.1.10 Commvault Systems Inc.

- 7.1.11 Cohesity Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2024-2032 年按元件、服務供應商、組織規模、部署模式、垂直產業和區域分類的雲端備份市場報告

2024-2032 年按元件、服務供應商、組織規模、部署模式、垂直產業和區域分類的雲端備份市場報告 雲端備份與復原軟體市場報告:到2030年的趨勢、預測與競爭分析

雲端備份與復原軟體市場報告:到2030年的趨勢、預測與競爭分析 雲端備份市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件、部署模式、最終用戶產業、地區和競爭細分

雲端備份市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件、部署模式、最終用戶產業、地區和競爭細分 雲端備份市場:按元件、按服務供應商、按部署、按組織規模、按產業 - 2023-2030 年全球預測

雲端備份市場:按元件、按服務供應商、按部署、按組織規模、按產業 - 2023-2030 年全球預測 雲端備份和恢復軟件市場:按部署模型、按用戶類型、按行業、按地區 - 規模、份額、展望、機會分析,2022-2030 年

雲端備份和恢復軟件市場:按部署模型、按用戶類型、按行業、按地區 - 規模、份額、展望、機會分析,2022-2030 年 雲端備用的全球市場

雲端備用的全球市場 雲端備用和修復的全球市場 2023-2027

雲端備用和修復的全球市場 2023-2027 全球雲備份市場預測(~ 2028 年):按部署、組件、最終用戶和地區進行分析

全球雲備份市場預測(~ 2028 年):按部署、組件、最終用戶和地區進行分析 雲端備用的全球市場:各組件、解決方案、服務、部署模式、組織規模、產業、地區 - 預測(2022年~2028年)

雲端備用的全球市場:各組件、解決方案、服務、部署模式、組織規模、產業、地區 - 預測(2022年~2028年)