|

市場調查報告書

商品編碼

1405373

全球熱泵:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Global Heat Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

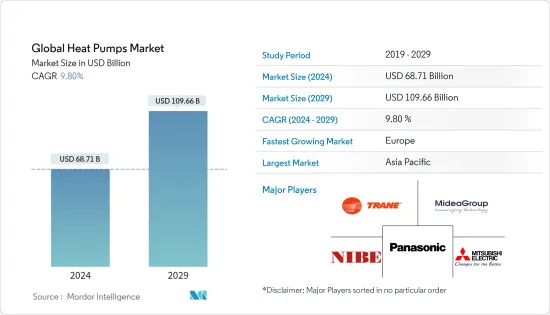

預計2024年全球熱泵市場規模為687.1億美元,預計2029年將達到1,096.6億美元,預測期(2024-2029年)複合年成長率為9.80%。

熱泵的工作原理是機械壓縮循環冷凍,也可以反向加熱或冷卻設施中所需的空間。因此,冷卻和加熱應用的市場正在擴大。

主要亮點

- 熱泵可以從促進環境永續性中策略性地受益。此外,歐盟的產業整合策略指出,到2030年,65%的商業建築將採用電力暖氣。根據這些資料,隨著建築物利用熱泵供暖和製冷,熱泵銷量預計將增加。

- 此外,對節能設備不斷成長的需求正在推動熱泵等技術的部署,為最終用戶提供巨大的潛力,為世界各地的可再生能源和氣候目標做出貢獻。

- 此外,遏制對石化燃料的依賴以及尋求爐子和空調的節能替代品的需求日益成長,預計將在預測期內推動對熱泵的需求。由於熱泵傳遞熱量而不是產生熱量,因此它們可以提供相同的空間調節,而營業成本約為傳統供暖和製冷設備的四分之一。

- 透過加熱設施的某些區域,您也許能夠節省空氣處理裝置 (AHU) 的材料成本。然而,當安裝熱泵作為主要供暖和製冷系統時,這些因素可能會影響整體安裝成本。

- 雖然由於 COVID-19大流行預計熱泵銷售將放緩甚至下降是現實的,但政府政策和消費者需求預計將推動熱泵銷售。

熱泵市場趨勢

住宅熱泵預計將大幅成長

- 各個地區都制定了旨在促進近零能耗建築的法規,指導住宅透過熱泵等高效能源來源來提高能源性能。熱泵通常用作單戶住宅和聯排別墅的熱源。熱泵也擴大應用於多用戶住宅。

- 此外,加州能源委員會(CEC)通過的2022年建築能源效率標準(能源法規)將於2023年1月1日生效,對美國加州的建築引入了多項新要求。根據2022年能源法,新建的單戶住宅必須配備水和空氣的電動熱泵。此外,所有新建多用戶住宅都必須配備電熱泵加熱。

- 供應商也致力於使住宅脫碳,以減少二氧化碳排放。例如,大金最近宣布了一項改造住宅供暖和製冷的四階段計劃。據該公司稱,歐洲建築存量約佔歐盟 (EU) 二氧化碳排放總量的 36%。因此,在新建住宅中安裝了熱泵,從而推動了該地區對熱泵的需求。

- 儘管受到 COVID-19 的影響,許多市場的住宅仍顯著增加,這也支撐了市場的成長。例如,根據德國兩大建築協會ZDB和HDB的數據,德國建築業的銷售額預計將比2021年成長5.5%,達到2022年的1,510億歐元。這一成長預測預計將受到該國住宅建築行業強勁表現的推動,該行業在整個大流行期間保持彈性。

- 此外,2022年4月,大金宣布支援REPowerEU,旨在將熱泵的普及數量從2027年的1000萬台增加到2030年的3000萬台。這與住宅脫碳進一步相關,因為這項運動將幫助歐盟在 2050 年實現其住宅部門脫碳目標。

亞太地區預計將主導市場

- 中國是熱泵的重要市場之一。這是由於政府政策支持該國的節能基礎設施,這將促進市場成長。中國廣闊的土地被正式分類為五個主要氣候區,每個氣候區都有不同的熱設計要求。這些區域供暖解決方案可以量身定做,以滿足巨大的市場機會。

- 在日本,熱泵在私人和商業環境中是眾所周知的產品。此外,各行業都在採用熱泵。這種發展始於幾十年前,並透過節能措施進一步加速。該文件由自然資源和能源局製定,規定2013年至2030年期間將實現節能5,030萬立方公尺原油當量。這些案例可能會增加該國對熱泵的需求。

- 在印度,飯店、商場、劇院等熱泵的使用逐漸增加。此外,印度還擁有大量的太陽能。根據新可再生統計,截至2022年11月30日,太陽能發電裝置容量已達約6,197千萬瓦。該國上年度太陽能發電裝置排名世界第四。太陽能集熱器和熱泵相結合的系統對於在世界各地增加可再生能源的空間供暖和生活熱水供應的使用來說是一個有吸引力的選擇。

- 在韓國,政府在節能解決方案方面的措施正在推動市場成長。例如,韓國環境部對現代 Kona Electric 和起亞 Niro EV 進行的一項研究發現,熱泵可顯著減少寒冷條件下的電池消耗。

- 在澳大利亞,澳大利亞綠色建築委員會(GBCA)於2003年推出了綠色之星認證。此外,澳洲政府的目標是到 2030 年將溫室氣體排放量比 2005 年減少 26-28%。這些案例表明,預測期內存在重大的市場成長機會。

- 其他亞太地區包括印尼、新加坡和泰國。印尼是世界上最大的地熱能生產國之一,並雄心勃勃地利用可再生能源進一步發展該產業。例如,在2022年舉辦的第八屆印尼國際地熱會展(IIGCE)上,印尼政府透過《電力供應總體規劃》設定了2030年地熱裝置容量330萬千瓦的發展目標,並宣布做到了。這些舉措可能會為所研究的市場帶來光明的前景。

熱泵產業概況

由於特靈公司、美的集團、松下公司、三菱電機公司和Daikin Industries Ltd.我們不斷創新產品的能力使我們比市場上其他參與者俱有競爭優勢。這些參與者透過研發活動和併購擴大了他們在市場上的足跡。

- 2022 年 11 月 - TRANE 宣布將從領先供應商 Nucor Corporation Econiq 購買低碳鋼並從美國 Steel verdeX 獲得額外撥款,減少其耐用 HVAC 解決方案的碳影響。這些鋼材將用於美國的製造流程,製造特靈的高效熱泵和家用空調,以及學校和資料中心等商業建築的溫度控管系統。

- 2022 年 11 月 - 三菱推出連鎖空氣源熱泵,能夠產生 7.8kW 至 640kW 的熱量。此熱泵無需輔助加熱器即可產生高達 70度C 的熱水。三菱電機推出了這款空氣源熱泵,用於學校和醫院等商業應用。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 對節能解決方案的需求不斷增加

- 政府加大力度減少碳排放

- 市場抑制因素

- 熱泵安裝成本高

第6章市場區隔

- 按類型

- 空氣熱源

- 水熱源

- 地熱(地面)熱源

- 按行業分類

- 工業的

- 商業的

- 設施

- 住宅

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 西班牙

- 法國

- 義大利

- 德國

- 荷蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太地區其他地區

- 世界其他地區(拉丁美洲、中東和非洲)

- 北美洲

第7章競爭形勢

- 公司簡介

- Trane Inc.(Trane Technologies)

- Midea Group

- NIBE Group

- Panasonic Corporation

- Mitsubishi Electric Corporation

- Daikin Industries Ltd

- Stiebel Eltron GmbH & Co. KG(De)

- Glen Dimplex Group

- Viessmann Werke GmbH & Co. KG

- Flamingo Heat Pumps(Flamingo Chillers)

- WOLF GMBH(ARISTON GROUP)

- Efficiency Maine

第8章投資分析

第9章市場的未來

The Global Heat Pumps Market size is estimated at USD 68.71 billion in 2024, and is expected to reach USD 109.66 billion by 2029, growing at a CAGR of 9.80% during the forecast period (2024-2029).

The heat pump works on the principle of mechanical-compression cycle refrigeration that can even be reversed to heat or cool the desired space of a facility. Hence, the market studied is growing for cooling applications and space heating.

Key Highlights

- Heat pumps are strategically placed to benefit from the drive to environmental sustainability. Furthermore, the European Union's strategy of sector integration suggests that 65% of all commercial buildings will be heated by electricity in 2030. The data indicate that heat pump sales are only expected to grow with buildings depending on them for heating and cooling.

- Furthermore, The growing demand for energy-efficient devices has been driving the deployment of technology, such as heat pumps, to provide end users with significant potential to contribute to renewable energy and climate targets across various regions worldwide.

- Moreover, The growing need to curb dependence on fossil fuels and look for an energy-efficient alternative to furnaces and air conditioners is expected to boost the demand for heat pumps over the forecast period. As heat pumps transfer heat rather than generate heat, they can offer equivalent space conditioning at as little as one-quarter of the operating costs of conventional heating or cooling appliances.

- Heating a few areas of the facility may save money on material costs for the air handler unit (AHU). However, these factors may affect the overall installation costs if heat pumps are installed as the main heating and cooling system.

- While it is realistic to expect slow growth or even a decline in heat pump sales owing to the COVID-19 pandemic, government policies and consumer demand are expected to drive the sales of heat pumps.

Heat Pump Market Trends

Residential Heat Pumps are Expected to Witness Significant Growth

- The regulations implemented in different regions aimed at promoting nearly zero energy buildings are directing residential buildings to improve energy performance through efficient energy sources, such as heat pumps. Heat pumps are often used as heat sources in single-family and terraced houses. Heat pumps are also increasingly used in apartment buildings.

- Further, the 2022 Building Energy Efficiency Standards (Energy Code) adopted by the California Energy Commission (CEC), which goes into effect January 1, 2023, introduced some new requirements for buildings in California, United States. According to the 2022 Energy Code, new single-family homes must have electric heat pumps for water and air. Electric heat pumps for space heating are also needed in all new multi-family residences.

- Vendors are also focusing on residential decarbonizing to decrease CO2 emissions. For instance, in recent years, Daikin announced a four-step plan to transform residential heating and cooling. According to the company, the European building stock is responsible for approximately 36 % of all CO2 emissions in the European Union. Therefore, heat pumps are being deployed in new residential constructions, thus, driving the need for heat pumps in the region.

- Residential construction has seen a considerable boost in many markets despite the impact of COVID-19, which also supports market growth. For instance, the German construction sector was expected to bring in sales of EUR 151 billion in 2022, up 5.5% from 2021, according to figures from the country's two leading construction associations, ZDB and HDB. The growth projection was anticipated to be led by the strong performance of the country's residential construction sector, which has remained resilient throughout the pandemic.

- Further, in April 2022, Daikin announced its support for the REPowerEU, which has set a goal to boost the rollout of heat pumps from 10 million units in 2027 to 30 million units in 2030. This is further associated with residential decarbonization as the movement can help the European Union achieve the residential sector's decarbonization goals by 2050.

Asia Pacific Expected to Dominate the Market

- China is one of the significant markets for heat pumps, owing to the government's policies to support more energy-efficient infrastructure in the country, thereby augmenting the market growth. China's vast geographic area is officially divided into five primary climate zones with different thermal design requirements. Heating solutions for these regions can be tailor-made to meet the huge market opportunities.

- In Japan, heat pumps are well-known products in private and commercial settings. Various types of industries have also embraced them. This development began several decades ago and has been further pushed by energy conservation measures. These were formulated by the Agency for Natural Resources and Energy, stipulating energy conservation of 50.3 million m3 crude oil equivalent between 2013 and 2030. Such instances are likely to boost the demand for heat pumps in the country.

- Applications of heat pumps in hotels, malls, theatres, etc., are gradually gaining traction in India. Moreover, a tremendous amount of solar energy is available in the country. According to the Ministry of New and Renewable Energy, solar power installed capacity reached around 61.97 GW as of 30th November 2022. The country stood 4th in solar PV deployment across the globe in the previous year. The system combination of solar thermal collectors and heat pumps can be an attractive option for increasing renewable energy usage worldwide for heating and domestic hot water preparation.

- In South Korea, government initiatives concerning energy-efficient solutions are driving the market growth. For instance, a study carried out by Korea's Ministry of the Environment on the Hyundai Kona Electric, and Kia Niro EV found that the heat pump significantly reduced battery consumption in cold conditions.

- In Australia, the Green Building Council of Australia (GBCA) launched the Green Star certification in 2003. Additionally, the Australian Government is focused on a 26-28% reduction in greenhouse gas emissions from 2005 levels by 2030. Such instances demonstrate a significant market growth opportunity over the forecast period.

- The countries considered under the rest of Asia-Pacific include Indonesia, Singapore, and Thailand. Indonesia is one of the leading geothermal energy powers in the world and has set ambitions to grow the sector further as the country embraces renewable energy sources. For instance, During the 8th Indonesia International Geothermal Convention & Exhibition (IIGCE) 2022, the Indonesian government announced that, through the General Plan for the Provision of Electricity, it had set a geothermal development target of 3.3 GW installed capacity by 2030. Such initiatives are likely to create a positive outlook for the studied market.

Heat Pump Industry Overview

The competitive rivalry in the global heat pumps market is high owing to the presence of some major players such as Trane Inc., Midea Group, Panasonic Corporation, Mitsubishi Electric Corporation, and Daikin Industries Ltd, amongst others. Their ability to continually innovate their offerings has enabled them to gain a competitive advantage over other players in the market. These players have expanded their market footprint through R&D activities, mergers & acquisitions.

- November 2022 - TRANE announced that it would reduce the carbon impact of its endurable HVAC solutions by buying low-carbon steel from major supplier Nucor Corporation Econiq, with an additional allotment from US Steel verdeX. The steel will be utilized in US manufacturing processes to build Trane high-efficiency heat pumps and air conditioners for homes and thermal management systems for commercial buildings such as schools and data centers.

- November 2022 - Mitsubishi launched a cascaded air source heat pump that can produce between 7.8 kW and 640 kW of heat. The heat pump can generate hot water at a temperature of up to 70 C without boost heaters. Mitsubishi Electric released the air source heat pump for commercial applications, including schools and hospitals.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Degree of Competition

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Energy Efficient Solutions

- 5.1.2 Increasing Government Initiatives to Curb Carbon Emission

- 5.2 Market Restraints

- 5.2.1 High Installation Cost of Heat Pumps

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Air-Source

- 6.1.2 Water-Source

- 6.1.3 Geothermal (Ground) Source

- 6.2 By End-User Vertical

- 6.2.1 Industrial

- 6.2.2 Commercial

- 6.2.3 Institutional

- 6.2.4 Residential

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Spain

- 6.3.2.2 France

- 6.3.2.3 Italy

- 6.3.2.4 Germany

- 6.3.2.5 Netherlands

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Australia

- 6.3.3.6 Rest of Asia Pacific

- 6.3.4 Rest of the World (Latin America, Middle East and Africa)

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Trane Inc. (Trane Technologies)

- 7.1.2 Midea Group

- 7.1.3 NIBE Group

- 7.1.4 Panasonic Corporation

- 7.1.5 Mitsubishi Electric Corporation

- 7.1.6 Daikin Industries Ltd

- 7.1.7 Stiebel Eltron GmbH & Co. KG (De)

- 7.1.8 Glen Dimplex Group

- 7.1.9 Viessmann Werke GmbH & Co. KG

- 7.1.10 Flamingo Heat Pumps (Flamingo Chillers)

- 7.1.11 WOLF GMBH (ARISTON GROUP)

- 7.1.12 Efficiency Maine

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球熱泵市場:按技術(空氣對空氣、空氣對水、水源、地混合、混合動力、PVT)、按冷劑、按類型、按額定容量、按最終用戶、按應用、按地區- 預測(截至2029 年)

全球熱泵市場:按技術(空氣對空氣、空氣對水、水源、地混合、混合動力、PVT)、按冷劑、按類型、按額定容量、按最終用戶、按應用、按地區- 預測(截至2029 年) 2024-2032 年按額定容量、產品類型、最終用途產業和地區分類的熱泵市場報告

2024-2032 年按額定容量、產品類型、最終用途產業和地區分類的熱泵市場報告 熱泵的全球市場:市場佔有率及排行榜·整體銷售額及需求預測 (2024-2030年)

熱泵的全球市場:市場佔有率及排行榜·整體銷售額及需求預測 (2024-2030年) 2024年熱泵全球市場報告

2024年熱泵全球市場報告 全球空氣源熱泵市場規模、佔有率、成長分析、按產品、按應用分類 - 產業預測,2023-2030 年

全球空氣源熱泵市場規模、佔有率、成長分析、按產品、按應用分類 - 產業預測,2023-2030 年 2024 年大型天然冷媒熱泵全球市場報告

2024 年大型天然冷媒熱泵全球市場報告 2024-2032 年泳池熱泵市場報告(按類型(空氣源、水/地熱源)、容量(小於 10kW、10kW-20kW、大於 20kW)、最終用戶(住宅、商業)和地區)

2024-2032 年泳池熱泵市場報告(按類型(空氣源、水/地熱源)、容量(小於 10kW、10kW-20kW、大於 20kW)、最終用戶(住宅、商業)和地區) 住宅管道熱泵市場規模 -按應用(單戶、多戶)、研究報告、國家展望、成長前景和全球預測,2024 年 - 2032 年

住宅管道熱泵市場規模 -按應用(單戶、多戶)、研究報告、國家展望、成長前景和全球預測,2024 年 - 2032 年 變速熱泵市場規模 -按應用(住宅、商業、工業)和預測,2024 年 - 2032 年

變速熱泵市場規模 -按應用(住宅、商業、工業)和預測,2024 年 - 2032 年 混合熱泵市場 - 2019-2029 年全球產業規模、佔有率、趨勢、機會和預測,按產品(壓縮熱泵、吸收式熱泵)、按應用(住宅、商業)、地區和競爭細分

混合熱泵市場 - 2019-2029 年全球產業規模、佔有率、趨勢、機會和預測,按產品(壓縮熱泵、吸收式熱泵)、按應用(住宅、商業)、地區和競爭細分