|

市場調查報告書

商品編碼

1404425

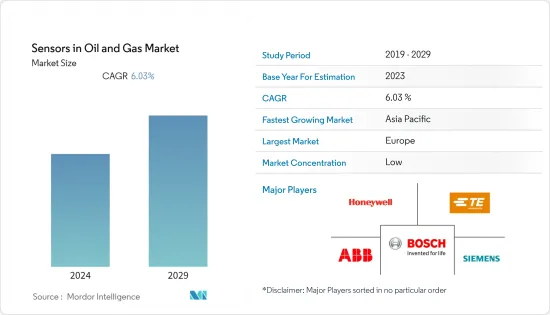

石油和天然氣感測器:市場佔有率分析、行業趨勢和統計、成長預測,2024-2029 年Sensors in Oil and Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

石油和天然氣感測器市場規模預計將從2024年的99.7億美元成長到2029年的133.6億美元,預測期間(2024-2029年)複合年成長率為6.03%。

主要亮點

- 全球經濟依賴石油和天然氣產業。石油和天然氣工業生產世界上大部分基本能源,也是多種化學產品的原料來源,包括農藥、化肥、藥品、溶劑和聚合物。控制和監測對於石油和天然氣產業的高效穩定運作至關重要。提高生產力、降低成本並提高盈利。石油和天然氣行業的控制和監控在很大程度上依賴感測器。

- 影響市場擴張的主要因素是對技術進步的日益關注和政府的支持政策。工業化的進步和各種安全和職業健康法規的收緊降低了市場價值。由於人們對空氣污染的認知不斷增強以及微型無線感測器供應的增加,該市場將會成長。推動市場快速成長的另一個因素是微機電領域的擴張和成長。

- 石油和天然氣產業擴大採用工業物聯網 (IIoT) 感測器,這主要是出於降低成本的需要。由於感測器製造商為最終用戶提供的技術進步和簡單的組裝選項,這些感測器的安裝既快速又便宜。

- 目前的油價環境正在推動整個石油和天然氣產業發生重大變化並做出艱難的決策。需要改善資本支出和營運支出的新營運模式和策略,以因應中短期市場供需動態。對提高安全和環境績效的永續解決方案的長期需求是重中之重。從鑽台到煉油廠,感測器應用可協助營運商透過頻譜上游、中游和下游創新和解決方案實現自身平衡。

- 感測器製造商擴大提供易於組裝的感測器。技術進步加劇了主要感測器製造商和物聯網產品服務供應商之間的競爭,推動了感測器在石油和天然氣行業的採用。

- 此外,石油和天然氣產業也面臨技術純熟勞工短缺的問題。人才庫的薄弱使得石油和天然氣公司僱用具有解決新能源來源所需技術技能的新員工的能力變得複雜。此外,COVID-19期間油價急劇上升以及沙烏地阿拉伯和俄羅斯等國家之間的價格競爭預計將鼓勵石油生產公司提高生產效率並增加該行業的需求。

油氣感知器市場趨勢

上游產業具有成長潛力

- 天然氣和原油是在上游部門發現和生產的。發電、工業流程和運輸嚴重依賴原油。天然氣和原油隱藏在地下深處的岩層中。許多儲存位於水下或氣候惡劣、難以到達的地方。

- 因此,感測器和其他重要的地震影像正在幫助製造商獲得準確的鑽井位置資訊。這有助於降低額外的鑽井成本。此外,價格實惠的感測器、不斷擴大的連接性和不斷提高的運算能力也推動了石油和天然氣採購流程中對感測器的需求。設備中嵌入的感測器提供的即時資料可以幫助企業安排維修和簡化日常業務。

- 石油和天然氣行業的系統、設備和感測器需要通訊資料並相互學習,以提高效率、生產力、健康和安全。因此,無線感測器和個人監控設備可以更輕鬆地識別工人何時接觸到不健康的有毒物質。因此,可以採取有效的措施。因此,上述因素預計將在整個預測期內對石油和天然氣行業感測器市場產生積極影響。

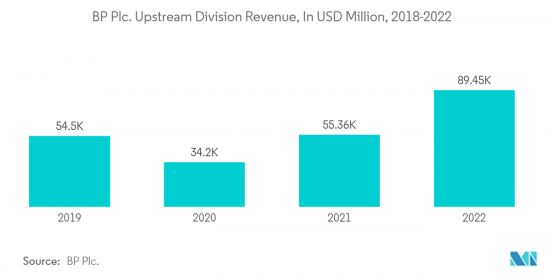

- BP PLC等領導企業的上游和低碳能源業務部門2022年營收894.4億美元。此外,阿布達比國家石油公司 (ADNOC) 宣布修改了上游甲烷強度目標,目標是到 2025 年達到 0.15%。這個新目標是中東地區最低的,鞏固了阿布達比國家石油公司作為低碳能源道德生產先鋒的地位。為了改善甲烷排放的監測,阿布達比國家石油公司也正在探索衛星監測和無人機載感測器等實驗技術。

歐洲佔主要市場佔有率

- 隨著各國政府關注污染預防和能源效率要求,石油和天然氣感測器在德國、法國和英國等歐洲國家變得越來越普遍。擴大最終用戶群和擴大氣體感測器的應用是推動該領域市場成長的兩個因素。

- 歐盟 (EU) 嚴格的排放控制要求和政府提高能源效率的措施有助於擴大歐洲目標市場。這些氣體感測器也用於按照相同原理工作的氣體和煙霧警報器。此外,消費者環境安全意識的提高導致擴大採用空氣監測系統產品來檢測污染水平和揮發性有機化合物。目前主導歐洲市場的是紅外線感測器式氣體感測器技術。

- 歐洲石油和天然氣產業正在擺脫感測器和其他設備等物聯網 (IoT) 智慧對象,並利用這些對象的資料創建更智慧型的業務,以幫助發展其業務。我們專注於制定大膽的策略來建立楷模。

- 石油和氣體純化可以使用物聯網感測器收集的資訊來了解正在輸送的石油類型。這使得公司能夠做出關鍵的製造、庫存和營運決策。使用物聯網感測器和增強連接性的即時庫存管理可以為歐洲石油和天然氣產業提供更有效率的供應鏈。

- 此外,挪威警方在海上石油和天然氣設施安裝了無人機偵測系統,以調查最近的安全違規行為,以應對最近對北溪天然氣管道的破壞。精心佈置的感測器能夠偵測未註冊的無人機並阻止其使用。

油氣感測器產業概況

石油和天然氣感測器市場分散且競爭激烈。感測器正在組織層臉部署在石油和天然氣產業的各種活動:上游、中游和下游。這就創造了玩家之間的競爭環境。例如Honeywell國際公司、西門子公司和 ABB 公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 石油和天然氣產業對安全系統的需求不斷成長

- 無線感測器領域對簡化網路架構的需求日益成長

- 市場抑制因素

- 對石油和天然氣鑽探活動實施嚴格監管

第6章市場區隔

- 依感測器類型

- 氣體感測器

- 溫度感應器

- 超音波感測器

- 壓力感測器

- 流量感測器

- 液位感測器

- 其他

- 連結性別

- 有線

- 無線的

- 按活動

- 上游

- 中產階級

- 下游

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 印尼

- 其他亞太地區

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 北美洲

第7章競爭形勢

- 公司簡介

- Honeywell International Inc.

- TE Connectivity Ltd.

- Robert Bosch GmbH

- ABB Ltd.

- Siemens AG

- Rockwell Automation Inc.

- Analog Devices Inc.

- Emerson Electric Company

- GE Sensing & Inspection Technologies GmbH

- SKF AB

第8章投資分析

第9章市場的未來

The Oil and Gas Sensors Market size is expected to grow from USD 9.97 billion in 2024 to USD 13.36 billion by 2029, registering a CAGR of 6.03 percent during the forecast period (2024-2029).

Key Highlights

- The global economy depends on the oil and gas industry. In addition to producing most of the world's basic energy, the oil and gas sector also serves as a substantial source of raw materials for various chemical goods, such as insecticides, fertilizers, medicines, solvents, and polymers. Control and monitoring are crucial for efficient and stable oil and gas industry operations. It improves productivity, cuts costs, and promotes profitability. The control and monitoring of the oil and gas industry depend heavily on sensors.

- The primary factors influencing market expansion are a greater focus on technical advancement and supportive governmental policies. Growing industrialization and stricter enforcement of various safety and occupational health regulations reduce market value. The market will grow due to increased awareness of air pollution and the growing supply of miniaturized wireless sensors. Another element contributing to the surge of the market is the expansion and growth of the micro-electromechanical sector.

- The rising adoption of IIoT (Industrial Internet of Things) sensors in the oil and gas industry is mainly driven by the need to reduce costs. The installation of these sensors takes less time and costs less, owing to technological advancements and easy assembling options that sensor manufacturers offer to end users.

- The current oil price environment is driving significant changes and difficult decisions across the oil and gas industry. New operating models and strategies that improve CAPEX and OPEX are required to respond to short- and mid-term market supply and demand dynamics. The long-term requirement for sustainable solutions that reinforce safety and environmental performance is a topmost priority. From drill pad to refinery, the application of sensors helps operators achieve a unique balance through a spectrum of upstream, midstream, and downstream technological innovations and solutions.

- Sensor manufacturers are increasingly offering sensors designed with easy assembling options. Owing to technical advancements, the competition among significant manufacturers of sensors and service providers of IoT products is intensifying, thereby boosting the adoption of these in the oil and gas industry.

- Additionally, the oil and gas industry suffers from a skilled labor shortage. The presence of a shallow talent pool has made it complicated for oil and gas companies to hire new employees who possess the technical skills that are required to work on new energy sources. Moreover, stress with the oil prices during COVID-19 and the price war between countries such as Saudi Arabia and Russia was expected to drive oil-producing companies to enhance their production efficiency and increase the demand in the sector.

Oil & Gas Sensors Market Trends

Upstream Industries Offer Potential Growth

- Natural gas and crude oil are discovered and produced in the upstream sector. Electricity generation, industrial processes, and transportation heavily rely on crude oil. Rock layers hide the deep subterranean locations of natural gas and crude oil. Many reservoirs are located underwater or in hard-to-reach places with harsh climates.

- As a result, sensors and other important seismic images assist manufacturers in obtaining precise drilling location information. This aids them in cutting down on the additional expenses related to drilling. In addition, the demand for sensors during the oil and gas procurement process is driven by affordable sensors, expanding connectivity, and rising computational power. Real-time data provided by sensors built into equipment assist businesses in scheduling repairs and streamlining daily operations.

- The oil and gas sector's systems, equipment, and sensors must communicate data and learn from one another to enhance efficiency, productivity, health, and safety. Therefore, it will be simple to identify when workers are exposed to unhealthy hazardous substances with the aid of wireless sensors and personal monitoring devices. Consequently, effective steps can be taken. Therefore, it is anticipated that the abovementioned factors will favorably affect the oil and gas industry's sensors market throughout the forecast period.

- The upstream and low carbon energy business segment of major firms such as BP PLC generated USD 89.44 billion in 2022. Moreover, the Abu Dhabi National Oil Company (ADNOC) announced that it revised its upstream methane intensity objective and aims to achieve 0.15 percent by 2025. The new goal, the lowest in the Middle East, strengthens ADNOC's position as a pioneer in the ethical production of low-carbon energy. To improve the monitoring of methane emissions, ADNOC is also looking into experimental technologies, including satellite monitoring and drone-mounted sensors.

Europe Holds a Significant Market Share

- Due to governments' increased focus on pollution control and energy efficiency requirements, oil and gas sensors have become more common in European countries, including Germany, France, and the United Kingdom. An expanding end-user base and expanded applications for gas sensors are two factors that would fuel market growth in this sector.

- The strict emission control requirements and government activities in the European Union to promote energy efficiency are credited with expanding the target market in Europe. These gas sensors are also used in gas or smoke alarms, which operate on the same principles. Additionally, consumers' growing awareness of environmental safety is driven by the increased adoption of goods used in air monitoring systems to detect pollution levels and volatile organic compounds. The infrared sensors type of gas sensor technology currently rules the European market.

- The more forward-thinking oil and gas industry in Europe is refocusing its attention away from the Internet of Things (IoT) smart objects like sensors and other devices and toward developing audacious strategies for using the data obtained from these objects to build more intelligent business models that help their business grow.

- Oil and gas refineries can be informed about the sorts of oil that have been delivered using the information gathered by IoT sensors. This allows businesses to decide on crucial manufacturing, inventory, and operational decisions. Real-time inventory management with IoT sensors and enhanced connectivity can provide a more efficient supply chain for the European oil and gas industry.

- Moreover, the Norwegian police put drone detection systems on offshore oil and gas facilities to investigate recent safety violations in reaction to recent damage to the Nord Stream gas pipelines. Strategic placement of the sensors allowed for the detection of unregistered drones and the prevention of their use.

Oil & Gas Sensors Industry Overview

The oil and gas sensors market is fragmented and competitive. The deployment of sensors at different oil and gas industry activities, such as upstream, midstream, and downstream, is growing at an organizational level. This creates a competitive environment among the players. Some players are Honeywell International Inc., Siemens AG, and ABB Ltd.

In March 2023, The Ministry of Electronics and Information Technology announced the launch of three IoT sensor-based products, which include a Smart Digital Thermometer, IoT Enabled Environmental Monitoring System, and a Multichannel Data Acquisition System in the CoE in IoT Sensors.

In October 2022, Honeywell displayed its latest sensor technologies at the Abu Dhabi International Petroleum Exhibition and Conference to help the transition to sustainable energy. The technologies displayed included energy storage systems, emission monitoring systems, the business's advanced plastics recycling technology, its portfolio of worker safety solutions, and carbon capture and hydrogen generation technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Safety Systems in the Oil and Gas Industry

- 5.1.2 Increasing Need for a Simplified Network Architecture in the Wireless Sensor Segment

- 5.2 Market Restraints

- 5.2.1 Rigid Regulations Imposed on Oil and Gas Drilling Activities

6 MARKET SEGMENTATION

- 6.1 By Sensor Type

- 6.1.1 Gas Sensor

- 6.1.2 Temperature Sensor

- 6.1.3 Ultrasonic Sensor

- 6.1.4 Pressure Sensor

- 6.1.5 Flow Sensor

- 6.1.6 Level Sensor

- 6.1.7 Other Sensor Types

- 6.2 By Connectivity

- 6.2.1 Wired

- 6.2.2 Wireless

- 6.3 By Activity

- 6.3.1 Upstream

- 6.3.2 Midstream

- 6.3.3 Downstream

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Indonesia

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Mexico

- 6.4.4.2 Brazil

- 6.4.4.3 Argentina

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 TE Connectivity Ltd.

- 7.1.3 Robert Bosch GmbH

- 7.1.4 ABB Ltd.

- 7.1.5 Siemens AG

- 7.1.6 Rockwell Automation Inc.

- 7.1.7 Analog Devices Inc.

- 7.1.8 Emerson Electric Company

- 7.1.9 GE Sensing & Inspection Technologies GmbH

- 7.1.10 SKF AB