|

市場調查報告書

商品編碼

1404410

智慧照明:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029Smart Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

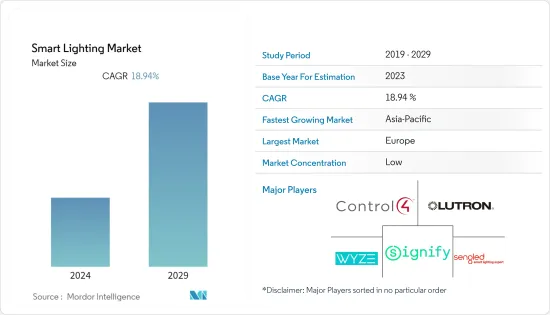

預計2024年智慧照明市場規模為196.5億美元,到2029年預計將達到467.9億美元,預測期內複合年成長率為18.94%。

由於其社會效益,消費者可能會迅速採用節能 LED 技術,從而有可能加速劣質緊湊型螢光和鹵素照明技術的替代品。

主要亮點

- 在商業和住宅空間中,照明的受歡迎程度和需求都在不斷增加,因為它可以連接到物聯網設備,並僅使用智慧型手機或平板電腦即可產生各種環境照明。智慧燈可以根據情況調暗到不同的色調,安排開/關時間,追蹤消費量,並透過 Wi-Fi、藍牙、SmartThings、Z-Wave 和 ZigBee 連接到其他裝置。您可以連接到其他裝置。

- 辦公空間也正在成為流行的智慧照明應用之一。在當今的商業世界中,企業主和管理者越來越重視員工的整體社會福利。透過改用智慧照明,辦公室可以為員工提供更明亮的光線。這可以改善員工的視力並減少眼睛疲勞。此外,燈光的顏色有助於照亮心情並提供舒適感。

- 此外,由於政府對傳統照明和能源消耗的有利法規,預計美國、歐盟 (EU)、中國和印度對連網型照明的市場需求將會增加。

- 然而,智慧照明市場的緩慢成長可能會給創業者帶來挑戰。如果智慧照明產品製造商未能進入市場,他們將遭受重大投資沉沒和聲譽損失。為了解決這些問題,製造商感到有必要考慮消費者如何看待整體智慧家庭技術和智慧照明產品。

- COVID-19 的出現導致整個供應鏈的生產停頓和中斷,損害了工業產出成長並減少了主要製造地的輕工業產能。然而,隨著人們待在家裡的時間越來越多,升級內裝的趨勢增加,這對市場產生了正面影響。此外,LED 在家庭中的使用量不斷增加以及智慧家居技術的普及預計將在未來幾年進一步推動市場成長。

智慧照明市場趨勢

政府法規強制 LED 使用驅動市場

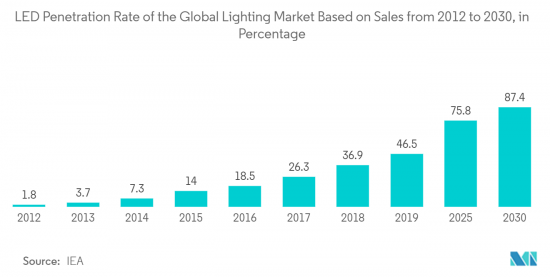

- 強制使用 LED 的政府法規正在推動多個地區的市場需求。例如,在美國,法律要求最常見類型的燈泡每瓦節能 45 流明,而典型的 60 瓦白熾燈泡每瓦節能約 15 流明,而鹵素白熾燈泡則每瓦節能約 15 流明。 ,提供1 瓦。CFL燈泡每瓦產生約20 流明,CFL 燈泡每瓦產生65 流明,LED 每瓦產生80 到100 流明,使用的能量非常少。此外,LED 價格的下降正在推動智慧照明的進一步採用。

- 透過性能標準、標籤和獎勵計劃,世界各地許多政府正在迅速採取行動,逐步淘汰低效光源,例如在歐洲,階段多年前就開始向 LED 技術過渡。歐盟 (EU) 最近更新了《生態設計指令》和《有害物質限制指令》,將在 2023 年之前階段淘汰所有螢光。此外,2023年1月,烏克蘭政府宣布核准一項發光二極體(LED)燈泡取代白熾燈泡的計畫。該計劃是歐盟(EU)對烏克蘭能源領域支持的一部分。

- 組成南部非洲發展共同體 (SADC) 的 16 個非洲國家已採用區域統一的照明標準。該標準的市場將在未來幾年內完全過渡到 LED。東非共同體 (EAC) 也在六個成員國階段螢光。其他地區,包括東南亞國家,也實施了類似的限制。預計這將推動所研究市場的成長。

- 據美國能源局稱,LED照明的廣泛普及預計將對美國的節能產生重大影響。因此,許多照明裝置將採用 LED 技術,到 2035 年,LED 照明每年節省的能源可能達到 569 TWh,相當於約 92 個 1,000 MW 發電廠的年發電量。

亞太地區將經歷最快的成長

- 物聯網(IoT)的日益普及預計將進一步開拓中國的照明市場,並加速中國連網型智慧照明系統的成長。 GSMA預計,到2025年,中國的物聯網連線數將達到約41億個,佔全球物聯網連線數的近三分之一。預計智慧照明系統將成為預測期內此趨勢的最大受益者。

- 在日本市場,Google、亞馬遜等全球高科技巨頭正在陸續發布專為日本訂製的智慧家居產品。在日本,人們擔心傳統家電的普及與前一年同期比較有所下降,但隨著配備人工智慧的產品和服務擴大引入家庭,智慧家庭產業預計未來將成長。可能性將是無限的。

- 中國的智慧照明市場也受到智慧型裝置(包括智慧型手機)日益普及的推動,智慧型手機可以方便地與物聯網設備連接。日本智慧型手機安全協會 (JSSEC) 預測,到 2022 年,日本智慧型手機用戶數可能達到 6,880 萬人。

- 由於對語音辨識、遠端控制和智慧家庭自動化卓越體驗等功能的需求不斷增加,印度對智慧照明的需求預計將成長。 LED照明在住宅、醫療保健以及酒店和工作場所等商業空間等各個領域的日益採用,以及可支配收入的增加,也是未來幾年推動這些設備成長的因素。

- 在亞太地區,韓國、泰國、新加坡、馬來西亞、斯里蘭卡、孟加拉、澳洲、印尼等也有可能在智慧照明市場獲得重要佔有率。

智慧照明產業概況

智慧照明市場競爭激烈,多家主要參與者進入該市場。然而,許多公司正在透過贏得新契約或收購其他公司來擴大在智慧照明市場的影響力。主要企業包括 Signify Holding、Control4 Corp. (Snap One LLC)、Wyze Labs Inc.、Eaton Corporation 和 Savant。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 產業價值鏈分析

- COVID-19 對智慧照明產業的影響

- PESTLE分析

第5章市場動態

- 市場促進因素

- 家庭節能需求不斷增加

- 強制使用 LED 的政府法規

- 市場挑戰

- 對產品選擇和安裝缺乏認知

- 市場機會

- 物聯網在新興國家的普及

第 6 章住宅智慧照明產品中使用的無線連線標準類型

- Wi-Fi

- Bluetooth

- ZigBee

第7章市場區隔

- 依產品類型

- 控制系統

- 有線

- 無線的

- 智慧燈具/照明設備

- 控制系統

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 拉丁美洲

- 中東/非洲

- 北美洲

第8章競爭形勢

- 公司簡介

- Control4 Corp.(Snap One LLC)

- Lutron Electronics Co. Inc.

- Signify Holding

- Wyze Labs Inc.

- Sengled

- GE Lighting(Savant Systems Inc.)

- Inter IKEA Holding BV

- Acuity Brands Inc.

- Hubbell Incorporated

- Crestron Electronics Inc.

- Insteon(Smartlabs Inc.)

- EGLO Leuchten GmbH

- Eve Systems GmbH

- LG Electronics Inc.

- Wiz Connected Lighting Co. Ltd

- Wipro Lighting Limited

- Xiaomi Corporation

- LIFX(Feit Electric)

第9章控制系統供應商市場佔有率分析

第10章投資分析

第11章市場的未來

The Smart Lighting Market size is estimated at USD 19.65 billion in 2024 and is expected to reach USD 46.79 billion by 2029, registering a CAGR of 18.94% during the forecast period. Due to its societal benefits, consumers might adopt energy-efficient LED technology more rapidly, so replacing the inferior compact fluorescent or halogen lighting technologies could be accelerated.

Key Highlights

- The popularity and demand for lights have grown in both commercial and residential spaces due to their ability to connect with IoT devices and generate a variety of ambient lighting using only smartphones or tablets. Smart lights can be dimmed with different color tones depending on the situation, schedule their on/off times, track their energy consumption, and connect to other devices via Wi-Fi, Bluetooth, SmartThings, Z-Wave, or ZigBee.

- Office spaces are also emerging as one of the common smart lighting applications. In today's business world, owners and managers are placing more emphasis on the overall well-being of their employees. By switching to smart lighting, offices can provide bright light for their employees. This helps them see better and experience less eye fatigue. Additionally, the color of the light can help brighten moods and provide comfort.

- Furthermore, favorable government regulations regarding conventional lighting and energy consumption across the United States, the European Union, China, and India are anticipated to favor the market demand for connected LED lighting.

- However, the slow growth of the smart lighting market may result in entrepreneurial challenges. The consequences of a market entry failure for producers of smart-lighting products comprise significant sunk investments and reputational damage. To address these concerns, manufacturers are finding the need to consider consumer views of smart-home technologies in general and smart-lighting products in particular.

- The emergence of COVID-19 caused a halt in production and disruption throughout the supply chain, impairing industrial output growth and reducing the capacity for light manufacturing across important manufacturing hubs. However, as people spent more time at home, they became more inclined to upgrade the interiors, which positively impacted the market. Additionally, it is anticipated that the growing use of LEDs in homes and the penetration of smart home technology will further fuel market growth in the coming years.

Smart Lighting Market Trends

Government Regulations Mandating the Use of LEDs to Drive the Market

- Government regulations mandating the use of LEDs are boosting the market demand in several regions. For instance, in the United States, as the law mandates energy savings to be 45 lumens per watt for the most common types of light bulbs, a typical 60-watt incandescent light bulb puts out about 15 lumens per watt, a halogen incandescent bulb offers about 20 lumens per watt, CFL bulb offers 65 lumens per watt, and LEDs put out 80-100 lumens per watt with a fraction of energy. In addition, the price drop in LEDs has led to a further increase in smart lighting adoption.

- Through performance standards, labeling, and incentive programs, many governments worldwide are moving quickly to phase out inefficient light sources, as in Europe, where the switch to LED technology began more than 10 years ago. Recent updates to the Ecodesign Directive and the Restriction of Hazardous Substances Directive by the European Union will effectively phase out all fluorescent lighting by 2023. Further, in January 2023, the Government of Ukraine announced the approval of a program to replace incandescent light bulbs with light-emitting diode (LED) light bulbs. This initiative is part of the European Union's support of Ukraine's energy front.

- A regionally harmonized lighting standard has been adopted by 16 African nations that make up the Southern African Development Community (SADC). This standard's market will transition entirely to LED in the coming years. The East African Community (EAC) is also phasing out fluorescent lighting in six member nations. Other jurisdictions, including Southeast Asian nations, are implementing similar regulations. This is expected to drive the growth of the market studied.

- According to the US Department of Energy, widespread use of LED lighting is expected to impact energy savings in the US greatly. As a result, many lighting installations are expected to use LED technology, and energy savings from LED lighting could reach 569 TWh annually by 2035, equal to the annual energy output of approximately 92 1,000 MW power plants.

Asia-Pacific to Witness Fastest Growth

- The increasing adoption of the Internet of Things (IoT) is expected to brighten the development of the lighting market in China, thereby increasing the growth of connected smart lighting systems in the country. GSMA estimates that China may account for around 4.1 billion IoT connections, which is almost one-third of the worldwide IoT connections, by 2025. Smart lighting systems are expected to be the biggest beneficiary of the trend during the forecast period.

- The Japanese market has witnessed the launch of a series of smart home products tailored for them from global tech giants, such as Google and Amazon. Amid the gloom surrounding the reduced penetration rate of traditional home appliances Y-o-Y in the country, the smart home industry promises unlimited potential in the future, owing to the rising integration of AI-empowered products and services in homes.

- The market for smart lighting in the country is also driven by the increased adoption of smart devices, including smartphones, due to their ability to connect conveniently to IoT devices. Japan Smartphone Security Association (JSSEC) estimates that the number of smartphone users in the country may reach 68.8 million by 2022.

- The demand for smart lighting in India is expected to grow owing to the increasing demand for features such as voice recognition or remote operation and the exceptional experience of smart home automation. Rising adoption of LED lights in various sectors such as residential, healthcare, and commercial spaces like hotels and workspaces, as well as rising disposable income, are other factors that may drive the growth of these devices in the future.

- Under the Asia-Pacific region, other countries like South Korea, Thailand, Singapore, Malaysia, Sri Lanka, Bangladesh, Australia, Indonesia, etc., also have a high potential for gaining a considerable share in the smart lighting market.

Smart Lighting Industry Overview

The smart lighting market is highly competitive and consists of several major players. However, many companies are increasing their market presence with smart lighting by securing new contracts and acquiring other companies. Signify Holding, Control4 Corp. (Snap One LLC), Wyze Labs Inc., Eaton Corporation, and Savant are key players.

In February 2023, Signify helped the German municipality of Eichenzell become a future-proof smart city through intelligent street lighting. Its BrightSites solution brings fast, wireless broadband connectivity to the city, allowing Eichenzell to cater to next-generation IoT applications and future 5G densification. Signify installed LED lighting, which the Interact City System manages. Eichenzell can continuously monitor and manage all lights from a single dashboard.

In January 2023, Savant company GE Lighting announced the expansion of its smart home ecosystem, Cync. Cync unveiled its entire Dynamic Effects entertainment lineup, which includes 16 million colors, pre-set and custom light shows, on-device music syncing, and other features. In addition, following a successful launch last year, Cync has expanded its Wafer light fixture line.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Smart Lighting Industry

- 4.5 PESTLE Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Energy Saving at Homes

- 5.1.2 Government Regulations Mandating the Use of LEDs

- 5.2 Market Challenges

- 5.2.1 Lack of Awareness Regarding Selection and Installation of Products

- 5.3 Market Opportunities

- 5.3.1 Increasing Adoption of IoT in Emerging Economies

6 WIRELESS CONNECTIVITY STANDARD TYPES USED IN RESIDENTIAL SMART LIGHTING PRODUCTS

- 6.1 Wi-Fi

- 6.2 Bluetooth

- 6.3 ZigBee

7 MARKET SEGMENTATION

- 7.1 By Product Type

- 7.1.1 Control System

- 7.1.1.1 Wired

- 7.1.1.2 Wireless

- 7.1.2 Smart Lamps and Fixtures

- 7.1.1 Control System

- 7.2 By Geography

- 7.2.1 North America

- 7.2.1.1 United States

- 7.2.1.2 Canada

- 7.2.2 Europe

- 7.2.2.1 United Kingdom

- 7.2.2.2 Germany

- 7.2.2.3 France

- 7.2.2.4 Spain

- 7.2.2.5 Rest of Europe

- 7.2.3 Asia-Pacific

- 7.2.3.1 China

- 7.2.3.2 Japan

- 7.2.3.3 India

- 7.2.3.4 Rest of Asia-Pacific

- 7.2.4 Latin America

- 7.2.5 Middle East and Africa

- 7.2.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Control4 Corp. (Snap One LLC)

- 8.1.2 Lutron Electronics Co. Inc.

- 8.1.3 Signify Holding

- 8.1.4 Wyze Labs Inc.

- 8.1.5 Sengled

- 8.1.6 GE Lighting (Savant Systems Inc .)

- 8.1.7 Inter IKEA Holding BV

- 8.1.8 Acuity Brands Inc.

- 8.1.9 Hubbell Incorporated

- 8.1.10 Crestron Electronics Inc.

- 8.1.11 Insteon (Smartlabs Inc.)

- 8.1.12 EGLO Leuchten GmbH

- 8.1.13 Eve Systems GmbH

- 8.1.14 LG Electronics Inc.

- 8.1.15 Wiz Connected Lighting Co. Ltd

- 8.1.16 Wipro Lighting Limited

- 8.1.17 Xiaomi Corporation

- 8.1.18 LIFX (Feit Electric)

9 VENDOR MARKET SHARE ANALYSIS FOR CONTROL SYSTEMS

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

無線智慧照明控制系統市場:依通訊技術、產品、安裝類型、應用、部署 - 2024-2030 年全球預測

無線智慧照明控制系統市場:依通訊技術、產品、安裝類型、應用、部署 - 2024-2030 年全球預測 戶外 LED 智慧照明解決方案市場 - 全球產業規模、佔有率、趨勢、機會和預測,按安裝類型、組件、最終用戶、地區、競爭細分,2019-2029F

戶外 LED 智慧照明解決方案市場 - 全球產業規模、佔有率、趨勢、機會和預測,按安裝類型、組件、最終用戶、地區、競爭細分,2019-2029F 2024-2032 年智慧照明市場報告(按產品、通訊技術、安裝類型、光源、應用和地區分類)

2024-2032 年智慧照明市場報告(按產品、通訊技術、安裝類型、光源、應用和地區分類) 2024 年智慧照明全球市場報告

2024 年智慧照明全球市場報告 手勢控制燈全球市場規模、佔有率和趨勢分析報告:價格分佈、應用、分銷管道和地區分類的展望和預測,2023-2030年

手勢控制燈全球市場規模、佔有率和趨勢分析報告:價格分佈、應用、分銷管道和地區分類的展望和預測,2023-2030年 全球智慧照明市場評估:按組件、連接類型、最終用途、地區、機會、預測(2016-2030)

全球智慧照明市場評估:按組件、連接類型、最終用途、地區、機會、預測(2016-2030) 智慧照明市場規模、佔有率、趨勢分析報告:按組件、連接性、應用、地區、細分市場預測,2023-2030 年

智慧照明市場規模、佔有率、趨勢分析報告:按組件、連接性、應用、地區、細分市場預測,2023-2030 年 室內智慧照明市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按產品、通訊技術、安裝類型、地區、競爭進行細分。

室內智慧照明市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按產品、通訊技術、安裝類型、地區、競爭進行細分。 戶外智慧照明市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按產品、通訊技術、安裝類型、地區、競爭進行細分。

戶外智慧照明市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按產品、通訊技術、安裝類型、地區、競爭進行細分。 全球智慧照明市場(2023-2030):規模、佔有率、成長分析和用途預測(住宅/商業設施)/組件(電器/控制)

全球智慧照明市場(2023-2030):規模、佔有率、成長分析和用途預測(住宅/商業設施)/組件(電器/控制)