|

市場調查報告書

商品編碼

1404391

應用傳遞控制器 (ADC) -市場佔有率分析、行業趨勢和統計、2024-2029 年成長預測Application Delivery Controllers (ADC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

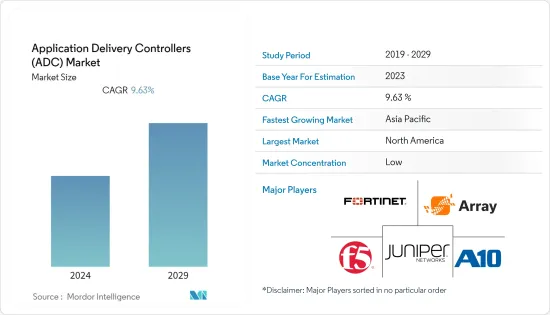

本會計年度應用傳遞控制器(ADC)市場規模預估為26.5億美元,複合年成長率為9.63%,預計五年內將達到46.1億美元。

由於對高效、安全的應用程式交付解決方案的需求不斷成長,該市場正在經歷顯著成長。

主要亮點

- ADC 市場的成長要素包括基於 Web 的應用程式的普及、雲端運算和虛擬的興起,以及企業快速、安全地向最終用戶交付應用程式的需求不斷成長。

- 應用程式交付控制器在過去幾年中獲得了廣泛的歡迎,這主要是由於對負載平衡、提高效能以及處理與應用傳輸相關的更高級要求的需求不斷成長。這些解決方案提供可用性、可擴展性、效能、安全性、自動化和控制,以保持應用程式和伺服器正常運作。這些功能還可以幫助想要或已經遷移到雲端環境的組織。

- 近年來,隨著網路攻擊的頻率和複雜性不斷增加,對應用傳遞控制器(ADC)的需求也隨之增加。 ADC 在加強應用程式和基礎設施的安全狀況方面發揮關鍵作用,使其成為防範各種網路威脅的重要組成部分。

- 透過向網路添加新服務來擴展應用程式(通常由不同供應商的解決方案組成)的需求日益成長,可能會增加網路複雜性並增加故障點。因此,向用戶提供服務變得更加複雜,並可能導致嚴重的延遲,從而導致收益流損失並降低用戶的體驗品質。

- 此外,COVID-19大流行進一步凸顯了應用程式視覺性和控制的重要性,因為遠距工作者迅速改變了工作環境,以保持員工在任何地方的工作效率。預計這將在預測期內擴大應用傳遞控制器市場。

應用傳遞控制器 (ADC) 市場趨勢

BFSI 最終用戶部分預計將佔據主要市場佔有率

- 由於各種改革和發展,BFSI 領域對應用傳遞控制器的需求正在不斷成長。科技普及的提高,加上網路銀行和手機銀行等數位管道,使銀行業務成為銀行服務的首選。利用先進的身份驗證和存取控制流程已成為銀行日益重要的要求。

- 圍繞銀行的數位生態系統正在迅速擴張。隨著消費者需求的不斷變化,銀行面臨著客製化產品以滿足消費者需求的壓力。此外,採用行動生活方式並在數位平台上互動的消費者希望銀行在同一平台上與他們建立聯繫。因此,BFSI 領域對應用傳遞控制器的需求不斷增加。

- 此外,隨著網路銀行、網路銀行和手機銀行數位流量的增加,BFSI部門也面臨因維護工作而停機的情況。為此,銀行需要實現負載均衡,支援輪詢分配,將領先優勢從伺服器1轉移到伺服器2、伺服器3等,但他們引入了ADC,這樣就沒有必要了。

- 巨量資料和分析等新一代技術和服務的日益普及需要對傳統網路進行轉型。軟體定義網路為各種規模的企業提供更大的彈性、更低的成本和更輕鬆的管理。

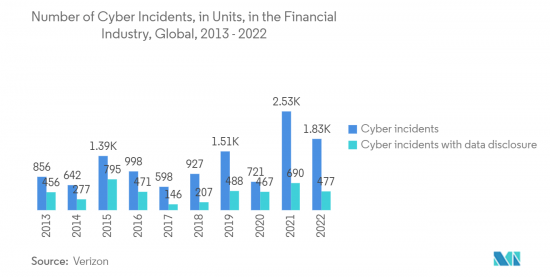

- 根據 Verizon 統計,2022 年全球金融業共通報了 1,829 起網路事件。金融業數以百萬計的敏感資料洩露給駭客,導致多家公司損失數百萬美元的資料外洩事件日益增多,引發了新興國家對強大安全性的關注。隨著全球業務的發展,DDoS 等威脅使關鍵資料面臨風險。這促使企業實施更好的解決方案來保護其端點和網路內的資料免受攻擊。

亞太地區預計將佔據主要市場佔有率

- 預計亞太地區在預測期內將呈現最高成長率。該地區雲端運算的快速成長預計將成為雲端基礎的應用程式交付控制器的關鍵驅動力。

- 此外,由於中小企業的投資,該地區預計將實現成長。中小型企業正在為其雲端基礎的應用程式投資經濟高效、雲端基礎且技術先進的解決方案。中國和印度等國家為該地區提供了巨大的成長機會。

- 由於技術進步,所研究的市場中連接設備的數量正在增加。此外,中國雲端處理產業的成長得到了政府的大力支持和私營部門的大量投資的支持。此外,5G和支援5G的設備將大大提高設備的互連性。其結果是連接設備的增加,這直接增加了對雲端基礎的應用程式的資料流量和安全性的控制需求。

- 此外,數位印度計劃旨在將舊有系統遷移到雲端基礎模式雲端基礎模式的模型或與基於雲端的模型整合,並透過雲端平台託管向公民提供電子服務。

- 此外,中國、印度和印尼等國家的網路用戶和資料流量正在增加,進一步推動了該地區 ADC 解決方案的成長。隨著數位時代的進步,市場供應商透過為最終用戶提供更多創新的網路解決方案和產品並確保最佳的技術體驗來引領細分市場。

應用傳遞控制器 (ADC) 產業概述

應用傳遞控制器 (ADC) 市場高度分散,主要參與者包括 F5 Networks Inc.、Fortinet Inc.、Juniper Networks Inc.、A10 Networks Inc. 和 Array Networks Inc.。市場參與企業正在採取聯盟和收購等策略來加強其產品陣容並獲得永續的競爭優勢。

2022 年 9 月,自動化機器身分管理 (MIM) 和應用程式基礎架構安全領域的領導者 AppViewX 宣布加入 F5 的技術聯盟計畫 (TAP)。透過此次合作,F5 和 AppViewX 將共同推動企業應用程式安全和交付解決方案,專注於管理和確保本地、雲端和邊緣應用程式的網路安全。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 可靠應用效能的需求不斷成長

- 網路攻擊增加

- 市場抑制因素

- 網路複雜度

- ADC 管理挑戰與成本上升

第6章市場區隔

- 按發展

- 雲

- 本地

- 按公司規模

- 中小企業 (SME)

- 主要企業

- 按行業分類

- 金融機構

- 零售

- 資訊科技/通訊

- 醫療保健

- 其他行業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區 中東/非洲

第7章競爭形勢

- 公司簡介

- F5 Networks Inc.

- Fortinet Inc.

- Juniper Networks Inc.

- A10 Networks Inc.

- Array Networks Inc.

- Citrix Systems Inc.

- Radware Corporation

- Akamai Technologies Inc.

- Barracuda Networks Inc.

- Piolink Inc.

- Sangfor Technologies Inc.

- HAProxy Technologies LLC

- Loadbalancer.org Inc.

- Kemp Technologies Inc.

第8章供應商市場佔有率分析

第9章投資分析

第10章投資分析市場的未來

The Application Delivery Controllers (ADC) Market was valued at USD 2.65 billion in the current year and is expected to register a CAGR of 9.63%, reaching USD 4.61 billion in five years. The market was experiencing significant growth due to the increasing demand for efficient and secure application delivery solutions.

Key Highlights

- Factors contributing to the ADC market's growth include the proliferation of web-based applications, the rise of cloud computing and virtualization, and the increasing need for businesses to deliver applications faster and securely to end-users.

- Application delivery controllers have gained significant traction in the past few years, primarily owing to the rising need for load balancing, improving performance, and handling much more advanced requirements associated with application delivery. These solutions provide availability, scalability, performance, security, automation, and control to keep the applications and servers running in their power band. These capabilities also aid organizations that want to or have already migrated to the cloud environments.

- The increasing frequency and sophistication of cyber attacks have driven the demand for application delivery controllers (ADCs) in recent years. ADCs play a crucial role in enhancing the security posture of applications and infrastructure, making them a vital component in defending against various cyber threats.

- The increasing need to scale out applications, which in various cases consists of solutions from different vendors along with the addition of new services to the network, can result in increased complexities and increased points of failure in the network. As a result, delivering these services to the consumers becomes more complex and can result in significant delays, leading to loss of revenue streams and lowered subscriber quality of experience.

- Additionally, with the COVID-19 pandemic, application visibility and management took on even more importance as remote workers quickly changed their working environments to maintain staff productivity from any place. This is expected to boost the market for application delivery controllers over the forecast period.

Application Delivery Controllers (ADC) Market Trends

BFSI By End-user Vertical Segment is Expected to Hold Significant Market Share

- The demand for application delivery controllers in the BFSI sector gained traction owing to various reforms and developments. The growing technological penetration, combined with digital channels, such as Internet banking, mobile banking, etc., is becoming a preferred choice for banking services. There is a more significant requirement for banks to leverage advanced authentication and access control processes.

- The digital ecosystem surrounding a bank is increasing at a rapid pace. With the constant change in consumer demand, banks have been pressured to customize their product offerings according to their demands. Moreover, consumers embracing a mobile lifestyle and socializing on digital platforms expect banks to connect with them on the same platforms. This is increasing the demand for application delivery controllers in the BFSI sector.

- Further, with increased digital traffic toward net banking, online banking, and mobile banking, the BFSI sector also faces downtime due to maintenance work. This requires the banks to implement load balancing where the banks would have to support round-robin distribution that is shifting lead from server 1 to server 2, followed by server 3, and so on, which is now eliminated with ADC.

- The rising popularity of next-generation technologies and services, such as Big Data and analytics, requires the transformation of legacy networks. Software-defined networks offer greater flexibility, lower cost, and easier management for businesses of all sizes.

- According to Verizon, in 2022, there were 1,829 reported cyber incidents in the financial industry worldwide. The instances of data breaches across financial industries that have leaked millions of crucial data to hackers and the loss of millions of dollars for multiple companies have increased the focus on robust security across emerging economies. As businesses worldwide grow, threats like DDoS have exposed critical data to risk. This has encouraged organizations to deploy better solutions to safeguard their data within endpoints and networks against attacks.

Asia Pacific is Expected to Hold Significant Market Share

- Asia Pacific is expected to witness the highest growth rate over the forecast period. The rapid increase in cloud computing in this region is expected to be a significant driver for cloud-based application delivery controllers.

- Additionally, the region is expected to witness growth, owing to the investments of small and medium organizations. SMEs are investing in cost-effective cloud-based and technologically advanced solutions for cloud-based applications. Countries such as China and India provide significant growth opportunities in the region.

- Owing to technological advancements, there is an increase in the number of connected devices in the studied market. Moreover, Strong government backing and substantial private sector investment are behind the growth of China's cloud computing industry. Furthermore, 5G and 5 G-enabled devices will exponentially increase the devices' interconnectivity. As a result, it increases connected devices, thereby directly augmenting the need for controlling the data traffic and security of cloud-based applications.

- Additionally, the Digital India initiative aims to move legacy and on-premise systems to a cloud-based model or integrate with it, and the cloud platform is expected to host the delivery of e-services to citizens.

- In addition, the increasing internet users and data traffic in countries like China, India, and Indonesia further augment the growth of ADC solutions in the region. With the evolving digital era, market vendors offer more innovative network solutions and products for end users, ensuring they have the best technology experience and driving the market segment.

Application Delivery Controllers (ADC) Industry Overview

The Application Delivery Controllers (ADC) Market is highly fragmented, with the presence of major players like F5 Networks Inc., Fortinet Inc., Juniper Networks Inc., A10 Networks Inc., and Array Networks Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In September 2022, AppViewX, the leader in automated machine identity management (MIM) and application infrastructure security, announced that the company joined F5's Technology Alliance Program (TAP). Through the partnership, F5 and AppViewX will jointly promote enterprise application security and delivery solutions focused on managing applications and ensuring cybersecurity across on-premises, cloud, and edge locations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Reliable Application Performance

- 5.1.2 Increasing Cyberattacks

- 5.2 Market Restraints

- 5.2.1 Increasing Network Complexity

- 5.2.2 Management Challenges and Higher Costs of ADCs

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 Cloud

- 6.1.2 On-premise

- 6.2 By Enterprise Size

- 6.2.1 Small and Medium Enterprises (SMEs)

- 6.2.2 Large Enterprises

- 6.3 By End-user Vertical

- 6.3.1 BFSI

- 6.3.2 Retail

- 6.3.3 IT and Telecom

- 6.3.4 Healthcare

- 6.3.5 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 F5 Networks Inc.

- 7.1.2 Fortinet Inc.

- 7.1.3 Juniper Networks Inc.

- 7.1.4 A10 Networks Inc.

- 7.1.5 Array Networks Inc.

- 7.1.6 Citrix Systems Inc.

- 7.1.7 Radware Corporation

- 7.1.8 Akamai Technologies Inc.

- 7.1.9 Barracuda Networks Inc.

- 7.1.10 Piolink Inc.

- 7.1.11 Sangfor Technologies Inc.

- 7.1.12 HAProxy Technologies LLC

- 7.1.13 Loadbalancer.org Inc.

- 7.1.14 Kemp Technologies Inc.

8 VENDOR MARKET SHARE ANALYSIS

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

應用傳遞控制器市場:按類型、組織規模、部署和最終用戶 - 2024-2030 年全球預測

應用傳遞控制器市場:按類型、組織規模、部署和最終用戶 - 2024-2030 年全球預測 2024-2032 年按類型、組件、組織規模(大型企業、中小企業)、垂直行業和地區分類的應用傳遞控制器市場報告

2024-2032 年按類型、組件、組織規模(大型企業、中小企業)、垂直行業和地區分類的應用傳遞控制器市場報告 2024 年應用傳遞控制器 (ADC) 全球市場報告

2024 年應用傳遞控制器 (ADC) 全球市場報告 應用程式交付控制器的全球市場:份額、規模、趨勢、行業分析報告 - 按部署、按公司規模、按最終用途、按地區、細分市場預測,2023-2032 年

應用程式交付控制器的全球市場:份額、規模、趨勢、行業分析報告 - 按部署、按公司規模、按最終用途、按地區、細分市場預測,2023-2032 年 應用程式交付控制器市場報告:2030 年趨勢、預測與競爭分析

應用程式交付控制器市場報告:2030 年趨勢、預測與競爭分析 交付控制器市場報告:2030 年趨勢、預測與競爭分析

交付控制器市場報告:2030 年趨勢、預測與競爭分析 應用程式交付控制器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署、企業規模、最終用戶垂直領域、地區、競爭細分,2018-2028 年。

應用程式交付控制器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按部署、企業規模、最終用戶垂直領域、地區、競爭細分,2018-2028 年。 應用傳遞控制器市場規模 - 按組件、企業規模、類型、最終用戶垂直領域和預測,2023 年至 2032 年

應用傳遞控制器市場規模 - 按組件、企業規模、類型、最終用戶垂直領域和預測,2023 年至 2032 年 應用傳遞控制器的全球市場:按類型(基於硬體、虛擬)、按服務(整合和實施、培訓、支援、維護)、按組織規模(中小企業、大型企業)、按行業、按地區- 2028 年預測到

應用傳遞控制器的全球市場:按類型(基於硬體、虛擬)、按服務(整合和實施、培訓、支援、維護)、按組織規模(中小企業、大型企業)、按行業、按地區- 2028 年預測到 全球應用傳遞控制器市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測

全球應用傳遞控制器市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測