|

市場調查報告書

商品編碼

1404371

分散式天線系統 -市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Distributed Antenna Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

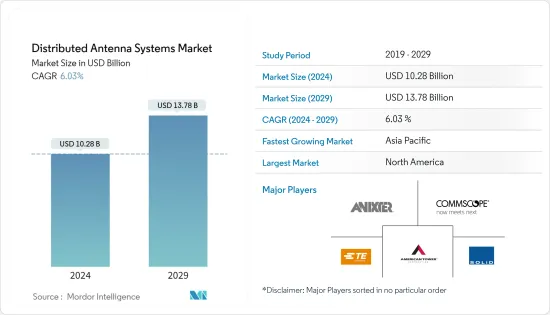

分散式天線系統市場規模預計到 2024 年為 102.8 億美元,預計到 2029 年將達到 137.8 億美元,在預測期內(2024-2029 年)複合年成長率為 6.03%。

由於通訊技術的進步,高速連接、更低功耗的網路設備以及更大的連接覆蓋範圍的進步正在推動分散式天線系統市場。此外,對穩定和不間斷連接的需求不斷成長以及連接設備數量的增加正在支持所研究市場的成長。

主要亮點

- 分散式天線系統的概念已經存在多年,無線網路在建築物中的使用迅速增加,在智慧家庭和連網型設備中具有潛在的應用,導致市場對分散式天線系統的引入進一步推動。與單天線系統相比,分散式天線系統具有多種優勢,使企業能夠獲得其應用所需的覆蓋範圍。

- 此外,雖然客戶期望無處不在的高品質語音覆蓋,但資料和視訊主導應用程式的使用正在迅速增加,從而重新定義了分散式天線系統的作用。

- 無線產業不斷努力透過整合 LTE 和 LTE-Advanced (LTE-A) 標準來滿足高速應用對更高頻寬和快速成長的資料使用不斷成長的需求。僅宏蜂窩蜂巢式網路無法有效滿足上一代應用的要求。這使得人們更加關注部署分散式天線系統網路以滿足用戶需求,例如辦公室、體育場館、家庭、機場和高層建築的服務。

- 此外,事實證明,在語音通話方面,分散式天線系統不僅僅是室內網路覆蓋解決方案。例如,在智慧城市中,分散式天線系統是幫助建立連網型系統所需的基礎設施的重要解決方案。智慧建築、購物中心、醫院和車輛交通管理等各種基礎設施需要持續通訊,預計將推動市場需求。

- 然而,由於分散式天線系統解決方案的價格是根據時間和範圍確定的,因此分散式天線系統的成本已成為阻礙所研究市場開拓的主要挑戰之一。例如,用於一致確定蜂窩通訊業者覆蓋範圍的被動分佈式天線系統價格低廉,可能僅花費幾百到幾千美元。相反,用於擴展一個或多個行動服務供應商網路的室內覆蓋範圍的有源分散式天線系統的成本較高。

- 此外,在 COVID-19 危機期間,科技在封鎖和隔離期間保持社會正常運作方面發揮了關鍵作用。除此之外,分散式天線系統和其他相關技術預計將產生長期影響。此外,在 COVID-19 危機之後,繼續監測可能出現的新世界秩序的不斷變化的徵兆對於有抱負的企業至關重要,而主要參與企業現在將關注不斷變化的分佈式天線,我期待著該系統取得成功。

分散式天線系統市場趨勢

體育和娛樂業佔主要市場佔有率

- 分散式天線系統主要透過天線系統為體育場館、體育場館等大型基礎設施提供無線服務,提供統一的連接,並允許緊急應變在緊急情況下留在建築結構內,並維持現場的無線通訊。

- 體育和娛樂愛好者現在期望不間斷的無線服務能夠在享受現場活動的同時快速輕鬆地與朋友和家人聯繫。此外,社群媒體更新、共用照片和影片、發送簡訊和撥打電話是體驗現場活動的重要且預期的部分。然而,體育場館和競技場因其大小、型態和資料使用的變化而給行動通訊帶來了獨特的挑戰。

- 室內無線解決方案解決了體育場館和競技場特有的這些挑戰,確保觀眾始終擁有可靠的連線。使用分散式天線系統,體育場館還可以為保全人員和公共初期應變人員配備支援蜂窩和公共頻寬的關鍵任務通訊資源。

- 此外,5G技術將影響人們生活的幾乎各個方面,包括所有體育和娛樂場所的球迷體驗。新體育場從一開始就考慮到了支援 5G 的技術,多個現有平台也融入了 5G,以滿足球迷的期望並透過創新解決方案簡化連接。

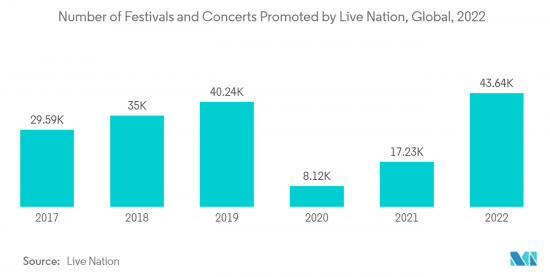

- 此外,全球舉辦的體育和娛樂賽事數量不斷增加,推動了新體育場館和體育娛樂綜合體建設的投資,預計將形成有利於市場成長的市場格局。例如,領先的活動組織 Live Nation 2021 年在全球舉辦了約 17,234 場活動。儘管這一數字主要由於 COVID-19 的影響而下降,但預計在預測期內將獲得牽引力。

亞太地區將經歷最高的成長

- 高層住宅和購物中心、商業園區等商業空間建設的快速成長,以及新加坡智慧國家和印度智慧城市使命等多項政府舉措、4G智慧型手機數量的不斷增加以及自帶設備趨勢這些因素正在推動該地區的分散式天線系統市場。

- 蜂窩技術的最新進展是該地區在預測期內實現強勁成長的關鍵因素之一。這是由於新興國家的LTE網路部署計畫不斷增加。此外,行動網路虛擬和開放 API 的快速採用也是推動市場成長的其他因素。

- 亞太地區是一個對比鮮明的地區。過去幾年,韓國和日本等已開發市場一直在進行 5G 網路緻密化計劃。高度都市化的中國香港、澳門和新加坡在小型基地台和分散式天線系統的廣泛使用方面具有可比性。另一方面,印度和印尼等新興市場依靠傳統的大型鐵塔來覆蓋其農村人口。馬爾地夫和其他太平洋島國也是這群人的一部分,它們完全取消了訊號塔,轉而採用更便宜的衛星行動網路。

- 因此,中國當地、韓國和日本是目前該地區最大的鐵塔市場。然而,由於這些市場的鐵塔覆蓋已經覆蓋了大多數人口,未來鐵塔的成長將在很大程度上取決於透過使用小型基地台和分散式天線系統來實現都市區網路的密集化,這將取決於您。

- 該地區還建立了多個聯盟和合作,為進一步的技術進步鋪平了道路。例如,諾基亞和中國移動聯合開發了這款5G低成本混合分散式室內系統來應對這些挑戰。此智慧室內覆蓋系統利用諾基亞 5G Pico 遠端無線電頭端系統以及被動分散式天線系統天線和藍牙低功耗 (BLE) 技術。與傳統的純被動式分散式天線系統相比,這種新解決方案還降低了安裝成本,同時提供了比分散式天線系統更高的容量。

分散式天線系統產業概況

分散式天線系統市場的競爭較為溫和,但該市場的推動因素包括行動資料流量的增加、物聯網(IoT) 帶來的連接設備的激增、對頻譜效率日益成長的需求以及尋求擴大網路覆蓋範圍和不間斷服務的消費者由於需求不斷增加,預計競爭將會加劇。目前,許多公司正在以不同的範圍進入該市場。主要參與企業包括 Anixter、CommScope、TE Connectivity、Corning Inc. 和 American Tower Corporation。最近的市場開拓包括:

2022 年 12 月,皇家貝蒂斯 Balompie 足球俱樂部宣布與無線通訊和廣播基礎設施供應商 Cellnex 合作,開發俱樂部的數位基礎設施,並為其球迷提供最佳的數位體驗。根據該契約,Cellnex 在貝尼托·維拉馬林體育場安裝了分散式天線系統。

2022 年 11 月,分散式天線系統和中繼器的領先供應商 Advanced RF Technologies (ADRF) 宣布推出新的 ADXV 分散式天線系統 C 頻段解決方案和 SDRX C 頻段中繼器。 ADXV 分散式天線系統 C 頻段模組提供高功率遠端 (HPR) 和中功率遠端 (MPR) 選項,支援 3.7GHz 至 3.98GHz 的 C 頻段頻率,可供建築業主、行動電信業者、系統使用對於整合商來說,Neutral Host 可以為各種規模的建築物和場館提供無處不在的5G 覆蓋。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 支援多個通訊業者的分散式天線系統功能和最新技術

- 市場挑戰

- 高升級成本是市場成長的挑戰

第6章市場區隔

- 按類型

- 主動型

- 被動的

- 數位的

- 混合

- 按最終用戶

- 製造業

- 醫療保健

- 政府機關

- 運輸

- 體育/娛樂

- 通訊

- 其他最終用戶

- 按用途

- 對於企業

- 公共

- 其他用途

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章競爭形勢

- 公司簡介

- Anixter Inc.

- Cobham PLC

- Antenna Products Corporation

- CommScope Inc.

- Tower Bersama Group

- SOLiD Inc.

- TE Connectivity Ltd.

- Corning Inc.

- Comba Telecom Systems Holdings Ltd.

- Boingo Wireless Inc.

- American Tower Corporation

第8章投資分析

第9章 市場未來展望

The Distributed Antenna Systems Market size is estimated at USD 10.28 billion in 2024, and is expected to reach USD 13.78 billion by 2029, growing at a CAGR of 6.03% during the forecast period (2024-2029).

The developments in communication technology that have led to the evolution of high-speed connectivity, lesser power-consuming network devices, and more substantial connectivity coverage have boosted the market for DAS systems. Additionally, the rising demand for stable and uninterrupted connectivity and the growing number of connected devices support the studied market's growth.

Key Highlights

- The concept of distributed antenna systems has been there for many years, and the surged usage of wireless networks in buildings with potential applications in smart homes and connected devices has further promoted the implementation of DAS systems in the market as it facilitates several advantages over single-antenna systems, allowing businesses to get the coverage essential for applications.

- Moreover, while customers expect ubiquitous high-quality voice coverage, the rapidly growing use of data and video-driven applications redefine DAS systems' role.

- The wireless industry consistently strives to keep pace with the growing demand for higher bandwidth and surging data usage for high-speed applications by incorporating LTE standards and the LTE-Advanced (LTE-A) standards. Depending on macro cellular networks alone could not efficiently meet the requirements of the last generation of applications. This has further focused on the need to deploy DAS networks for accommodating user demands such as services in offices, stadiums, homes, airports, and high-rises.

- Furthermore, DAS has turned out to be more than an indoor network coverage solution in regard to voice calls. For instance, in smart cities, DAS has turned out to be a crucial solution in aiding to creation of the needed infrastructure for achieving connected systems. Various infrastructures such as smart buildings, shopping complexes, hospitals, and vehicular traffic management require continuous communication; thus, this is expected to propel market demand.

- However, the cost of distributed antenna systems is among the major factors challenging the studied market's development, as the price of a DAS solution is determined based on the time and range. For instance, passive DAS utilized for identifying the coverage of cellular carriers consistently is at the lower end and may cost only a couple of hundreds or thousands of dollars; on the contrary, active DAS utilized for increasing in-building coverage of one or more mobile service provider networks that is available at higher costs.

- Moreover, during the COVID-19 crisis, essential technologies played an essential role in keeping society functional during lockdowns and quarantines. In addition to this, DAS and other related technologies are expected to have a long-lasting impact. Furthermore, continuous monitoring for the evolving signs of a possible new world order post-COVID-19 crisis is essential for aspiring businesses, and the significant players are looking forward to finding success in the now-changing Distributed Antenna Systems (DAS), which is expected to propel investments, supporting the growth of the studied market during the forecast period.

Distributed Antenna Systems Market Trends

Sport and Entertainment Segment to Hold a Significant Market Share

- Distributed Antenna Systems (DAS) provide wireless service via an antenna system, mainly to large infrastructural establishments such as sports complexes, stadiums, etc., to provide even connectivity and to ensure that emergency responders maintain wireless communications within a building structure and on-the-job in emergencies, considering large gatherings at these places.

- Currently, sports and entertainment fans expect uninterrupted wireless service that can enable them to quickly and easily stay connected with their friends and family while enjoying any live event. Moreover, updating social media, sharing photos and videos, sending texts, and placing calls are integral and expected parts of experiencing a live event. However, stadiums and arenas have presented unique challenges for mobile communications due to their size, shape, and variation in data use.

- The in-building wireless solutions have solved these unique challenges of stadiums and arenas to ensure that spectators always have reliable connectivity. Using DAS systems, stadiums can also equip their security personnel and public safety first responders with mission-critical communication resources supporting both cellular and public safety bands.

- Moreover, 5G technology impacts almost every aspect of people's lives, including fans' experience at any sports and entertainment venue. New stadiums are being built with 5G-ready technologies taken into consideration from the beginning, while multiple existing platforms are also incorporating them to keep up with fans' expectations and streamline connectivity through innovative solutions.

- Furthermore, the increasing number of sporting and entertainment events being organized globally, driving investment in the construction of new stadiums and sports and entertainment complexes, are expected to create a favorable market scenario for the studied market growth. For instance, Live Nation, a leading event organization, organized about 17,234 events worldwide in 2021. Although the number has declined primarily due to COVID-19, it is expected to gain traction during the forecast period.

Asia-Pacific to Witness Highest Growth

- Owing to the rapidly increasing construction of high-rise residential buildings and commercial spaces, such as malls and business parks, coupled with the multiple government initiatives, such as Smart Nation Singapore and Smart Cities Mission India, among others, with a growing volume of 4G enabled smartphones, the rising popularity of Bring Your Own Device trends have been some of the other factors that are driving the region's DAS market.

- The recent advancements in cellular technology are one of the major factors for the region's excellent growth over the forecast period. This can be attributed to the growing number of planned deployments of LTE networks in emerging economies. Also, the virtualization of mobile networks and the rapid adoption of open APIs are other factors contributing to the market's growth.

- Asia-Pacific has been a region of contrasts. Advanced markets such as South Korea and Japan have had network densification projects for 5G for the past few years. The highly urbanized Chinese administrative regions of Hong Kong and Macau and the city-state of Singapore are comparable in their extensive usage of small cells and DAS. On the other hand, the development curve in emerging markets such as India and Indonesia which are still relying on the traditional macro-towers in order to cover their large rural populations. The Maldives and the Pacific island nations are also an example of this group, eschewing towers altogether in favor of even less expensive satellite-based mobile networks.

- Hence, Mainland China, South Korea, and Japan are currently the largest tower markets in the region. However, tower coverage in these markets has already reached the majority of the population, which implies that future tower growth would significantly rely on network densification in urban areas through the usage of small cells and DAS.

- The region is also witnessing several partnerships and collaborations, paving the way for further technological evolution. For instance, Nokia and China Mobile have jointly developed this 5G low-cost hybrid distributed indoor system in order to meet these challenges. The smart indoor coverage system leverages the Nokia 5G Pico Remote Radio Head system together with the passive DAS antennas and Bluetooth Low Energy (BLE) technology. This new solution also reduces deployment costs as compared to the traditional passive-only DAS systems while delivering greater capacity than DAS.

Distributed Antenna Systems Industry Overview

The distributed antenna systems market is moderately competitive; however, the competition is expected to grow owing to the increasing mobile data traffic, the proliferation of connected devices due to the Internet of Things (IoT), the rising need for spectrum efficiency, and the growing consumer demand for extended network coverage and uninterrupted connectivity. Many companies are now entering the market with an array of scopes. Some of the key players in the market are Anixter, CommScope, TE Connectivity, Corning Inc., and American Tower Corporation. Some recent developments in the market include:

In December 2022, Real Betis Balompie football club announced a partnership with Cellnex, a wireless telecommunication and broadcasting infrastructure provider, to develop the club's digital infrastructure and provide the best digital experience for its fans. As per this agreement, Cellnex installed a distributed antenna system (DAS) at the Benito Villamarin Stadium.

In November 2022, Advanced RF Technologies (ADRF), a leading pure-play distributed antenna system (DAS) and repeater provider, launched its new ADXV DAS C-band solution and the SDRX C-band repeater. The ADXV DAS C-band modules include high-power remote (HPR) and mid-power remote (MPR) options supporting C-band frequencies ranging from 3.7 GHz to 3.98 GHz and allow building owners, mobile carriers, system integrators, and neutral hosts to bring ubiquitous 5G coverage for buildings and venues of every size.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 DAS Ability to Support Multiple Telecom Carriers and Upcoming Technologies

- 5.2 Market Challenges

- 5.2.1 High Cost to Upgrade challenges the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Active

- 6.1.2 Passive

- 6.1.3 Digital

- 6.1.4 Hybrid

- 6.2 By End-User

- 6.2.1 Manufacturing

- 6.2.2 Healthcare

- 6.2.3 Government

- 6.2.4 Transportation

- 6.2.5 Sports and Entertainment

- 6.2.6 Telecommunications

- 6.2.7 Other End-Users

- 6.3 By Application

- 6.3.1 Enterprise DAS

- 6.3.2 Public Safety DAS

- 6.3.3 Other Applications

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Anixter Inc.

- 7.1.2 Cobham PLC

- 7.1.3 Antenna Products Corporation

- 7.1.4 CommScope Inc.

- 7.1.5 Tower Bersama Group

- 7.1.6 SOLiD Inc.

- 7.1.7 TE Connectivity Ltd.

- 7.1.8 Corning Inc.

- 7.1.9 Comba Telecom Systems Holdings Ltd.

- 7.1.10 Boingo Wireless Inc.

- 7.1.11 American Tower Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

分散式天線系統 (DAS)

分散式天線系統 (DAS) 全球室內分散式天線系統市場:按產品供應、按所有權模式、按用戶設施區域、按頻率協議、按網路類型、按最終應用 - 預測 2024-2030

全球室內分散式天線系統市場:按產品供應、按所有權模式、按用戶設施區域、按頻率協議、按網路類型、按最終應用 - 預測 2024-2030 分散式天線系統市場:按報價、覆蓋範圍、所有者、用戶設施、頻率通訊協定、訊號源、產業 - 2024-2030 年全球預測

分散式天線系統市場:按報價、覆蓋範圍、所有者、用戶設施、頻率通訊協定、訊號源、產業 - 2024-2030 年全球預測 分散式天線系統市場規模、佔有率、趨勢分析報告:按技術、按所有權、按應用、按地區、細分市場預測,2023-2030 年

分散式天線系統市場規模、佔有率、趨勢分析報告:按技術、按所有權、按應用、按地區、細分市場預測,2023-2030 年 全球中立託管市場:按技術、頻段、無線電類型、解決方案、部署方法和產業劃分(2023-2028)

全球中立託管市場:按技術、頻段、無線電類型、解決方案、部署方法和產業劃分(2023-2028) 室內分散式天線系統市場規模、佔有率、趨勢分析報告:按組件、按類型、按所有權、按應用、按地區、細分市場趨勢,2023-2030 年

室內分散式天線系統市場規模、佔有率、趨勢分析報告:按組件、按類型、按所有權、按應用、按地區、細分市場趨勢,2023-2030 年 2023-2028 年分散式天線系統市場報告(依產品、系統類型、覆蓋範圍、技術、最終用途和地區)

2023-2028 年分散式天線系統市場報告(依產品、系統類型、覆蓋範圍、技術、最終用途和地區) 分佈式天線系統 (DAS) 市場:2019-2029 年全球市場規模、佔有率、趨勢分析、機遇和預測報告

分佈式天線系統 (DAS) 市場:2019-2029 年全球市場規模、佔有率、趨勢分析、機遇和預測報告 全球分佈式天線系統 (DAS) 市場:未來按產品/服務產品、範圍、所有權模式、行業、用戶設施區域、頻率協議、網絡類型、信號源、區域預測(至 2028 年)

全球分佈式天線系統 (DAS) 市場:未來按產品/服務產品、範圍、所有權模式、行業、用戶設施區域、頻率協議、網絡類型、信號源、區域預測(至 2028 年) 分散天線系統 (DAS) 的全球市場 (2023年~2028年):各技術、類型 (主動式、被動式、混合)、覆蓋範圍 (室外、室內)、業者 (電信業者、企業、中立主機)、產業

分散天線系統 (DAS) 的全球市場 (2023年~2028年):各技術、類型 (主動式、被動式、混合)、覆蓋範圍 (室外、室內)、業者 (電信業者、企業、中立主機)、產業