|

市場調查報告書

商品編碼

1404338

半導體代工:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Semiconductor Foundry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

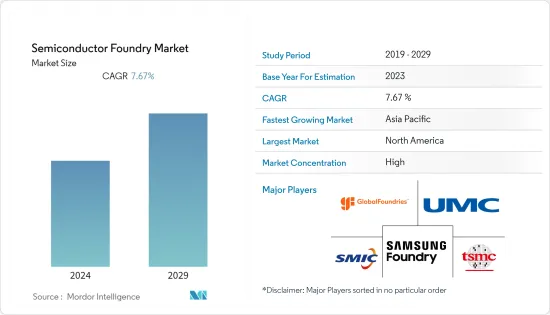

上年度半導體代工市場規模為1,277.9億美元,預計未來五年將達1,849.4億美元,複合年成長率為7.67%。

物聯網(IoT)、雲端運算和人工智慧(AI)等技術變革正在推動晶片產業的長期需求。例如,人工智慧正在為半導體產業創造新的機遇,因為許多人工智慧應用都依賴硬體作為創新核心,特別是在邏輯和儲存功能方面。與人工智慧快速擴大使用相關的晶片需求預計將對整體行業成長做出重大貢獻。

主要亮點

- 密切的跨境政府間合作夥伴關係預計將推動代工市場的成長,特別是在韓國和美國。此外,各國政府鼓勵企業在不洩露商業機密的情況下披露半導體生產資訊,以識別瓶頸並防止供應鏈中斷。美國政府要求三星和台積電等公司自願填寫此類資訊細節。

- 如果正確應用,進階分析可以顯著改善營運和報酬率,同時推動成長。然而,包括幾家半導體公司在內的許多公司在採用這些策略方面進展緩慢。

- 由於高速連接可用性的不斷提高、雲端採用的增加以及資料處理和分析的使用的增加,物聯網 (IoT) 的採用正在穩步成長。例如,根據愛立信的數據,2022年全球蜂巢式物聯網連接數量預計將達到19億,到2027年將成長到55億,在此期間複合年成長率為19%。

- 技術創新放緩可能導致採用該技術的新用戶減少,從而減少晶片製造商的新開發資金。這可能會形成一個自我強化的循環,穩步降低通用晶片的經濟吸引力並減緩技術進步。

- 儘管受到 COVID-19 大流行的影響,全球半導體市場在 2020 年下半年仍保持強勁成長,並持續到 2021 年。該行業一直受到高虧損和需求增加的困擾,導致供應鏈出現嚴重缺口,這主要是由於 COVID-19 大流行造成的。由於擔心汽車等關鍵產業對晶片的需求下降,病毒最初的傳播導致代工廠關閉並降低了運轉率。儘管半導體代工廠最初預測需求增加,但產量下降導致全球半導體短缺。

半導體代工市場趨勢

家用電子電器和通訊成為最大的終端用戶產業

- 消費性電子是半導體代工市場的關鍵應用領域之一。筆記型電腦、耳機、穿戴式裝置和智慧型手機等家用電子電器的日益普及正在推動該領域的成長。

- 半導體是家用電子電器的重要組成部分,可實現通訊、運算和各種其他應用等關鍵功能的進步。此外,家用電子電器技術和規模的快速發展也帶動了對先進半導體技術的需求。

- 根據美國科技協會(CTA)預測,2021年消費科技產業收益預計將與前一年同期比較%。對智慧型手機、健康設備、汽車技術和串流媒體服務的強勁需求將推動大部分預期收益。

- 2023 年 1 月,蘋果宣布計劃開發採用 3 奈米製程製造的 Apple M3 處理器的新款 MacBook Air 和 iMac。根據這些計劃,台積電於 2022 年 12 月開始批量生產用於下一代 Mac、iPhone 和其他蘋果設備的 3 奈米晶片製程。

- 此外,穿戴式裝置的成長也導致了新的、更小的晶片的採用,推動了大量生產這些晶片的半導體代工廠的成長。據Cisco稱,北美連網穿戴裝置數量將從 2021 年的 3.788 億台增至 2022 年的 4.39 億台。全球整體,連網穿戴裝置數量已超過10億。

北美佔有很大的市場佔有率

- 由於半導體技術在連網型設備和汽車領域的廣泛使用,北美的半導體製造市場正在顯著擴大。北美代工市場預計將由美國主導,因為該領域面臨國內外競爭的激烈競爭。

- 多年來,美國的地位面臨著無數挑戰,但由於其韌性和更快行動的能力,它始終能夠生存下來。據SIA稱,自1990年代以來,美國半導體產業的晶片銷售一直領先於全球,佔全球市場佔有率的近50%。此外,美國半導體企業在研發、設計和製造流程技術方面持續領先或具有高度競爭。

- 根據半導體工業協會 (SIA) 的數據,全球銷售的晶片中約 47% 是在美國製造的。這種差異對美國經濟和國家安全構成嚴重威脅,這就是為什麼商界相關人員和政界人士最近開始呼籲在該國建立半導體工廠。為此,英特爾、三星、台積電均表示希望在美國投資新晶圓廠、擴大業務,將大大支持美國未來的半導體製造業。

- 例如,英特爾最初宣布打算在 2022 年 1 月投資超過 200 億美元在俄亥俄州開設兩家新的尖端晶片工廠。作為英特爾 IDM 2.0 計畫的一部分,這項投資將有助於提高產量,以滿足對先進半導體急劇上升的需求,並為該業務的新一代尖端產品提供動力。

- 此外,2022年11月,台積電宣布將於2024年開始在亞利桑那州工廠生產3奈米晶片,目前為蘋果供貨。台積電亞利桑那州工廠是拜登政府推動該國晶片製造計畫的一部分。

- 此外,加拿大因其經濟、金融和政治體系、訓練有素的勞動力以及對商業的開放性而享有很高的國際聲譽,使其成為未來半導體代工領域的一個重要地區。我們處於獨特的地位,我們準備好採取必要步驟位於魁北克的 IBM 微電子公司持續封裝先進的電腦晶片,並致力於開發 5G 所需的新型光學元件技術。

半導體代工產業概況

隨著市場整合,該行業中的代工廠正在激烈競爭,以獲得與無晶圓廠供應商的交易,以進一步擴大其影響力和市場佔有率。此外,這些參與企業正在增加產能擴張的投資。

現有排名前五名的廠商台積電、三星電子、聯華電子、格羅方德、中芯國際的市場滲透率都非常高,每年都在爭取高市場佔有率。近年來,5G 和物聯網已成為其生產設備的一些關鍵促進因素,預計這將成為代工廠未來幾年的戰略重點。創新水平、上市時間和性能是參與企業在市場中脫穎而出的關鍵條件。由於整合不斷增加、技術進步和地緣政治形勢,所研究的市場正在經歷波動。

2022年12月,台積電宣布將在美國亞利桑那州的投資計畫增加兩倍以上,從先前的120億美元增加至400億美元。亞利桑那州工廠將生產用於 iPhone 處理器的 3nm 和 4nm 晶片。

2022年12月,三星電子有限公司宣布計畫在2023年提高韓國最大半導體工廠的晶片產能。

2022 年 10 月,美國參議員帕特里克·萊希(Patrick Leahy) 和GlobalFoundries 獲得了3,000 美元的聯邦撥款,用於推進格芯佛蒙特州埃塞克斯交界處晶圓廠下一代矽基氮化鎵( GaN) 半導體的開發和生產。將獲得 1,000,000 美元的資助。這筆 3000 萬美元的聯邦資金將使 GF 能夠購買工具並擴大 200mm GaN 晶圓製造的開發和實施,用於高功率應用晶片的生產,包括電動車、工業馬達和能源應用。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 鑄造產能利用率趨勢

- 產業價值鏈分析

- COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 透過分析最佳化半導體工藝

- 汽車、物聯網、人工智慧領域驅動市場

- 市場挑戰

- 莫耳定律已達到其物理極限

- 主要產業夥伴

- 與半導體產品相關的晶圓代工趨勢

第6章市場區隔

- 依技術節點

- 10/7/5nm

- 16/14nm

- 20nm

- 28nm

- 45/40nm

- 65nm

- 其他技術節點

- 按用途

- 家電及通訊

- 車

- 工業的

- HPC

- 其他用途

- 按地區

- 北美洲

- 歐洲、中東/非洲

- 亞太地區

第7章競爭形勢

- 公司簡介

- TSMC Limited

- Globalfoundries Inc.

- United Microelectronics Corporation(UMC)

- Semiconductor Manufacturing International Corporation(SMIC)

- Samsung Electronics Co. Ltd(Samsung Foundry)

- Dongbu Hitek Co. Ltd

- Intel Corporation

- Hua Hong Semiconductor Limited

- Powerchip Technology Corporation

- STMicroelectronics NV

- Tower Semiconductor Ltd.

- Vanguard International Semiconductor Corporation

- X-FAB Silicon Foundries

- NXP Semiconductors NV

- Renesas Electronics Corporation

- Microchip Technologies Inc.

- Texas Instruments Inc.

第 8 章 研究期間 IDMS 影響半導體(OSD 和 IC)銷售和成長的主要趨勢和動態

第9章 研究期間IDMS的代工銷售情況

第10章 研究期間前5名半導體銷售公司的供應商市場佔有率以及按類別(OSD和IC)的佔有率

第 11 章供應商市場佔有率分析 - 純粹的公司

第12章投資分析

第13章投資分析市場的未來

The semiconductor foundry market was valued at USD 127.79 billion the previous year and is expected to register a CAGR of 7.67%, reaching USD 184.94 billion by the next five years. Technology inflections such as the Internet of Things (IoT), cloud computing, and artificial intelligence (AI) are driving up the long-term demand for the chip industry. For instance, AI is creating new opportunities for the semiconductor industry as many AI applications rely on hardware as a core enabler of innovation, especially for logic and memory functions. The demand for chips related to the rapidly growing use of AI is expected to contribute significantly to the industry's overall growth.

Key Highlights

- Close partnerships between governments across borders, especially in South Korea and the United States, are anticipated to help the growth of the foundry market. Further, governments are encouraging companies to disclose semiconductor production information without revealing trade secrets to identify bottlenecks and prevent supply chain disruptions. The United States government asked firms like Samsung and Taiwan Semiconductor Manufacturing to voluntarily fill out a form detailing such information.

- Advanced analytics, when applied correctly, can drastically enhance operations and margins while simultaneously spurring growth. Despite this, many companies, including several semiconductor companies, have been slow to adopt these strategies.

- Owing to the increasing availability of high-speed connectivity, rising cloud adoption, and increasing use of data processing and analytics, the adoption of the Internet of Things (IoT) is growing steadily. For instance, as per Ericsson, there were 1.9 billion cellular IoT connections in the world in 2022, which is expected to grow to 5.5 billion in 2027, registering a CAGR of 19% over the period.

- Slowing innovation may lead to fewer new users adopting the technology, reducing the money chipmakers have for funding new developments. This may create a self-reinforcing cycle that steadily makes the economics of universal chips less attractive, slowing down technical progress.

- Despite the effects of the COVID-19 pandemic, the global semiconductor market observed robust growth in the latter half of 2020, which continued in 2021 as well. The industry was riddled with a high deficit and increasing demand, leading to a significant supply chain gap primarily attributed to the COVID-19 pandemic. The initial spread of the virus led to the shutting down or the reduction of foundry capacity utilization, fearing the decreasing demand for the chips across major sectors, like automotive. The diminished output led to a global shortage of semiconductors as the demand increased despite the initial estimates by semiconductor foundries.

Semiconductor Foundry Market Trends

Consumer Electronics and Communication to be the Largest End-user Industry

- Consumer electronics is one of the prominent application segments for the semiconductor foundry market. The growing adoption of consumer electronics devices, such as laptops, earphones, wearables, and smartphones, has propelled the segment's growth.

- Semiconductors are essential components of consumer electronics, enabling key features, such as advances in different applications like communication, computing, and others. In addition, the rapid development in the technology and size of consumer electronics has also been leading to the demand for advanced semiconductor technology.

- According to the Consumer Technology Association (CTA), in the United States, consumer technology industry revenue is projected to grow by 2.8% from 2021's impressive 9.6% growth over the year before. Strong demand for smartphones, health devices, automotive technologies, and streaming services would help the market to propel much of the projected revenue.

- In January 2023, Apple announced its plan to develop its new MacBook Air and iMac with the Apple M3 processor, built on a 3-nanometer process. In line with these plans, in December 2022, TSMC began mass production of its 3-nanometer chip process for the next generations of Mac, iPhone, and other Apple devices.

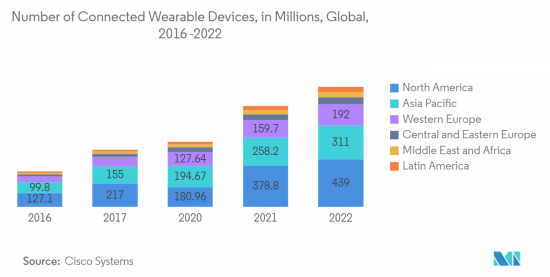

- Furthermore, the growth in wearables has also been leading to the adoption of new miniaturized chips, which propels the growth of semiconductor foundries that manufacture such chips in bulk. According to Cisco Systems, the number of connected wearable devices in North America reached 439 million in 2022 from 378.8 million in 2021. Globally, the number of connected wearable devices crossed 1 billion.

North America to Hold Significant Market Share

- The market for semiconductor manufacturing in North America is expanding significantly due to the growing use of semiconductor technology in connected devices and the automotive sector. The North American foundry market is predicted to be dominated by the United States because of the sector's intense competition from international and local competitors.

- Although America's position has faced numerous challenges throughout the years, it has always survived, owing to its resilience and capacity to move more quickly. Since the 1990s, the U.S. semiconductor sector has led the world in chip sales, holding close to 50% of the annual global market share, according to SIA. Additionally, American semiconductor companies continue to lead or be very competitive in research and development, design, and manufacturing process technology.

- Approximately 47% of the chips sold worldwide are created in the United States, according to the Semiconductor Industry Association (SIA). This discrepancy creates severe threats to the economy and national security of the United States, which is why both business insiders and politicians have recently started to demand the construction of semiconductor fabs in the country. Due to this, with capital investments for new fabs, Intel, Samsung, and TSMC have all expressed a willingness to grow their businesses in the United States, which will significantly support the country's future semiconductor manufacturing sector.

- For instance, Intel initially declared intentions to invest more than USD 20 billion in creating two new cutting-edge chip facilities in Ohio in January 2022. As part of Intel's IDM 2.0 plan, the investment will assist increase production in meeting the soaring demand for advanced semiconductors, powering a new generation of cutting-edge products from the business.

- In addition, TSMC declared in November 2022 that it will start producing 3-nanometer chips at its Arizona factory, where it now supplies Apple, in 2024. The Arizona factory of TSMC is a component of the Biden administration's plan to promote chip manufacturing in the country.

- Moreover, Canada is in a unique position, with economic, financial, and political systems, a highly-trained workforce, and a significant reputation internationally as a country that is open for business and is poised to take essential steps to emerge as a prominent region in the future semiconductor foundry landscape. IBM Microelectronics in Quebec still packages advanced computer chips and is now taking on new optical component technologies required for 5G.

Semiconductor Foundry Industry Overview

Owing to the consolidated nature of the market, foundries in the industry are competing intensely to gain access to fabless vendor deals to expand their presence and market share further. In addition, these players are increasingly investing in increasing their production capabilities.

The levels of market penetration for the existing top 5 vendors, TSMC, Samsung Electronics, UMC, GlobalFoundries, and SMIC, are significantly high, and these vendors are competing to gain a higher market share each year. In recent times, 5G and IoT have emerged as some of the significant drivers for units to be produced, and this is expected to be a strategic focus for foundries over the coming years. The level of innovation, time-to-market, and performance are the key terms by which the players differentiate themselves in the market. With growing consolidation, technological advancement, and geopolitical scenarios, the market studied is witnessing fluctuations.

In December 2022, Taiwan Semiconductor Manufacturing Co (TSMC) announced that it would more than triple its planned investment in Arizona, United States, to USD 40 billion from a previously announced USD 12 billion. The Arizona plants would produce 3-nm and 4-nm chips used for iPhone processors.

In December 2022, Samsung Electronics Ltd. announced plans to step up chip production capacity at its largest semiconductor fabrication plant in South Korea in 2023.

In October 2022, US Senator Patrick Leahy and GlobalFoundries announced the award of USD 30 million in federal funding to advance the development and production of next-generation gallium nitride (GaN) on silicon semiconductors at GF's Fab facility in Essex Junction, Vermont. The USD 30 million federal funding will enable GF to purchase tools and extend the development and implementation of 200 mm GaN wafer manufacturing in making chips for high-power applications, including electric vehicles, industrial motors, and energy applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Foundry Capacity Utilization Trends

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Optimization of Semiconductor Processes through Analytics

- 5.1.2 Automotive, IoT, and AI Sectors are Driving the Market

- 5.2 Market Challenges

- 5.2.1 Moores Law is about Reaching its Physical Limitation

- 5.3 Major Industry Partnerships

- 5.4 Foundry Trends Related to Semiconductor Products

6 MARKET SEGMENTATION

- 6.1 By Technology Node

- 6.1.1 10/7/5 nm

- 6.1.2 16/14 nm

- 6.1.3 20 nm

- 6.1.4 28 nm

- 6.1.5 45/40 nm

- 6.1.6 65 nm

- 6.1.7 Other Technology Nodes

- 6.2 By Application

- 6.2.1 Consumer Electronics and Communication

- 6.2.2 Automotive

- 6.2.3 Industrial

- 6.2.4 HPC

- 6.2.5 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe, Middle East and Africa

- 6.3.3 Asia Pacific

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 TSMC Limited

- 7.1.2 Globalfoundries Inc.

- 7.1.3 United Microelectronics Corporation (UMC)

- 7.1.4 Semiconductor Manufacturing International Corporation (SMIC)

- 7.1.5 Samsung Electronics Co. Ltd (Samsung Foundry)

- 7.1.6 Dongbu Hitek Co. Ltd

- 7.1.7 Intel Corporation

- 7.1.8 Hua Hong Semiconductor Limited

- 7.1.9 Powerchip Technology Corporation

- 7.1.10 STMicroelectronics NV

- 7.1.11 Tower Semiconductor Ltd.

- 7.1.12 Vanguard International Semiconductor Corporation

- 7.1.13 X-FAB Silicon Foundries

- 7.1.14 NXP Semiconductors NV

- 7.1.15 Renesas Electronics Corporation

- 7.1.16 Microchip Technologies Inc.

- 7.1.17 Texas Instruments Inc.

8 OVERALL SEMICONDUCTOR (O-S-D AND IC) SALES BY IDMS DURING THE STUDY PERIOD AND KEY TRENDS AND DYNAMICS INFLUENCING THE GROWTH

9 FOUNDRY SALES BY IDMS DURING THE STUDY PERIOD

10 VENDOR MARKET SHARES BY TOP 5 IDMS BASED ON SEMICONDUCTOR SALES AND AN INDICATION OF THE PERCENTAGE SHARES BY CATEGORY (O-S-D VS IC) DURING THE STUDY PERIOD

11 VENDOR MARKET SHARE ANALYSIS - PUREPLAY COMPANIES

12 INVESTMENT ANALYSIS

13 FUTURE OF THE MARKET

按技術節點(10/7/5nm、16/14nm、20nm、45/40nm 等)、代工類型(純代工、IDM)、應用(通訊、消費性電子、電腦、汽車和其他)分類的半導體代工市場報告其他)和地區 2024-2032

按技術節點(10/7/5nm、16/14nm、20nm、45/40nm 等)、代工類型(純代工、IDM)、應用(通訊、消費性電子、電腦、汽車和其他)分類的半導體代工市場報告其他)和地區 2024-2032 鑄造服務市場:按技術節點、材料類型、工藝類型和最終用戶分類 - 2024-2030 年全球預測

鑄造服務市場:按技術節點、材料類型、工藝類型和最終用戶分類 - 2024-2030 年全球預測 鑄造服務市場:依材料類型、依製程類型、依最終用途產業、按地區

鑄造服務市場:依材料類型、依製程類型、依最終用途產業、按地區 全球半導體代工市場(2016-2030):按技術節點、代工模式、應用和地區劃分的機會和預測

全球半導體代工市場(2016-2030):按技術節點、代工模式、應用和地區劃分的機會和預測 半導體代工全球市場規模、佔有率、產業趨勢分析報告:依節點規模、應用、地區分類的展望與預測,2023-2030年

半導體代工全球市場規模、佔有率、產業趨勢分析報告:依節點規模、應用、地區分類的展望與預測,2023-2030年 2023-2030年全球半導體代工市場規模研究與預測,依技術節點、應用與區域分析

2023-2030年全球半導體代工市場規模研究與預測,依技術節點、應用與區域分析 半導體代工市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按技術節點、按應用、地區、競爭細分

半導體代工市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按技術節點、按應用、地區、競爭細分 晶圓代工廠服務市場:越來越多的無晶圓廠公司將芯片製造外包,推動晶圓代工服務需求

晶圓代工廠服務市場:越來越多的無晶圓廠公司將芯片製造外包,推動晶圓代工服務需求 半導體晶圓代工廠的全球市場:市場規模 - 各技術,各晶圓代工廠類型,各用途,各地區展望,競爭策略,各市場區隔預測(~2032年)

半導體晶圓代工廠的全球市場:市場規模 - 各技術,各晶圓代工廠類型,各用途,各地區展望,競爭策略,各市場區隔預測(~2032年) 半導體晶圓代工廠的全球市場:市場規模,趨勢,成長分析

半導體晶圓代工廠的全球市場:市場規模,趨勢,成長分析