|

市場調查報告書

商品編碼

1403976

農業接種劑:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Agricultural Inoculants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

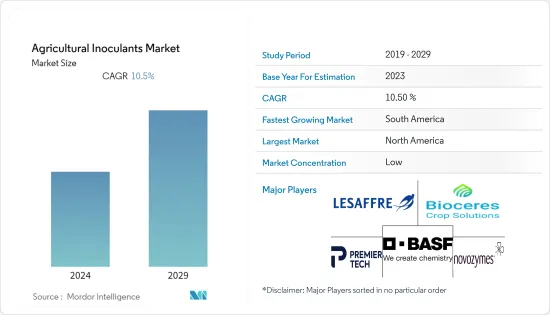

農業接種劑市場規模預計到2024年為101.5億美元,預計到2029年將達到167.6億美元,預測期內複合年成長率為10.5%。

主要亮點

- 目前的農業方法嚴重依賴化學肥料、農藥和除草劑等化學投入,這對農產品的營養價值以及農民和消費者的健康產生負面影響。過度和濫用這些化學物質導致了食品污染、雜草和抗病性以及對環境的負面影響,對人類健康產生了重大影響。這些化學輸入促進有毒化合物在土壤中的累積。

- 有些合成肥料含有酸根,如鹽酸根和硫酸根,會增加土壤的酸度,對土壤和植物的健康產生不利影響。此外,一些植物可能會吸收高度持久的化合物。持續食用此類作物會導致人類全身性疾病。

- 因此,隨著人們越來越認知到消費劣質作物帶來的健康挑戰,需要新的和改進的技術來提高農產品的數量和品質而不損害人類健康。

- 化學投入的可靠替代品是微生物接種劑,可用作生物肥料、生物除草劑、生物殺蟲劑和生物防治劑。它們是有益的微生物,應用於土壤和植物以提高生產力和作物健康。它也廣泛用於控制害蟲和改善地面和作物的品質。

- 此外,政府促進有機農業採用的舉措預計將在研究期間推動市場成長。例如,根據綠色交易的「從農場到餐桌」策略,歐盟委員會制定了到2030年將歐盟至少25%的農業用地涵蓋有機農業的目標,並大幅增加有機水產養殖。

農業接種劑市場趨勢

採用有機農業和環保耕作方法

- 耕作方式有從傳統耕作到有機耕作的趨勢。這種轉變是由於人們越來越認知到傳統耕作方法對人類健康和環境安全的負面影響。

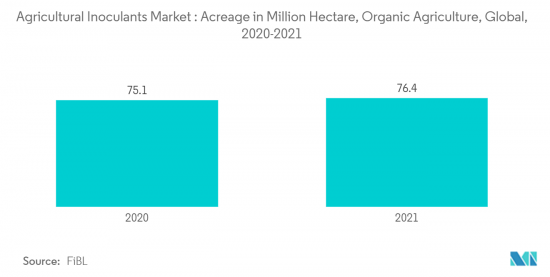

- 根據有機農業研究所(德語:Forschungsinstitut Fur biologischen Landbau (FiBL))預測,有機種植面積將從2018年的7090萬公頃增加到2021年的7640萬公頃,有187個國家實行有機農業。這導致對接種劑等有機解決方案的需求增加,並增加了對社區研究的公共和私人投資。

- 微生物接種劑可以改善土壤健康、增加養分利用率並預防疾病,為合成投入提供天然且永續的替代品。此外,微生物接種劑可以幫助減少合成投入物對環境的影響,並促進更永續的農業實踐。

- 因此,尋求減少環境足跡並生產更健康、更永續作物的農民對微生物接種劑的需求不斷增加。此外,在預測期內,農業用地面積的增加和消費者對有機產品需求的增加可能會對農業接種劑市場產生正面影響。

北美是最大市場

- 北美是農業接種劑最大的市場,其中美國佔大部分市場。美國農業部門高度發達,最近採用了自然和有機耕作方法。化學投入成本的增加、對土壤和環境的負面影響以及平衡植物營養意識的提高是推動該國市場的主要因素。

- 此外,某些公司和研究機構強調推出新產品以獲得競爭優勢。例如,由溫尼伯生物研究公司 XiteBio Technologies 開發的 XiteBio OptiPlus 是一種革命性的液體大豆接種劑,採用了經過市場驗證的 AGPT(先進促進生長技術)。

- 它結合了固氮細菌日本慢生根瘤菌(Bradyrhizobium japonicum)與2021年2月在加拿大註冊的取得專利的解磷植物促生根瘤菌(PGPR),專用大豆設計。預計此類新興市場的開拓將創造該地區對農業接種劑的需求,並在研究期間影響全球市場。

農業接種劑產業概況

農業接種劑市場分散,國際企業佔據主要市場佔有率。主要企業專注於研發活動、廣泛的產品系列、地理擴張、收購和積極的促銷策略,以維持其市場地位。領先公司包括 Novozymes、Lesaffre、BioceresCrop Solutions、Premier Tech 和BASF SE。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 採用有機農業和環保耕作方法

- 耕地面積減少,糧食安全擔憂加劇

- 市場抑制因素

- 對傳統產品和合成產品的高需求

- 缺乏認知和其他限制農業接種劑採用的因素

- 波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 功能

- 作物營養

- 作物保護

- 微生物

- 細菌

- 根瘤菌

- 固氮菌

- 磷細菌

- 其他細菌

- 菌類

- 木黴屬

- 菌根真菌

- 其他真菌

- 其他微生物

- 細菌

- 申請方法

- 種子接種

- 土壤接種

- 作物類型

- 糧食

- 豆類和油籽

- 經濟作物

- 水果和蔬菜

- 其他用途

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 其他非洲

- 北美洲

第6章競爭形勢

- 最採用的策略

- 市場佔有率分析

- 公司簡介

- BASF SE

- Premier Tech

- Lallemond Inc.

- Novozymes

- Mapleton Agri Biotec Pty Ltd

- New Edge Microbials Pty Ltd

- T.Stanes & Company Limited

- AEA Investors(Verdesian Life Sciences LLC)

- Lesaffre

- Bioceres Crop Solutions

第7章 市場機會及未來趨勢

The agricultural inoculants market size is estimated at USD 10.15 billion in 2024 and is expected to reach USD 16.76 billion by 2029, growing at a CAGR of 10.5% during the forecast period.

Key Highlights

- Current agricultural practices depend heavily on chemical inputs, such as fertilizers, pesticides, and herbicides, which cause a deleterious effect on the nutritional value of farm products and the health of farm workers and consumers. Excessive and indiscriminate use of these chemicals has resulted in food contamination, weed and disease resistance, and adverse environmental outcomes, significantly impacting human health. Applying these chemical inputs promotes the accumulation of toxic compounds in soils.

- Several synthetic fertilizers contain acid radicals, such as hydrochloride and sulfuric radicals, increasing soil acidity and adversely affecting soil and plant health. Highly recalcitrant compounds can also be absorbed by some plants. Continuous consumption of such crops can lead to systematic disorders in humans.

- Therefore, the increasing awareness of health challenges due to the consumption of poor-quality crops has led to a quest for new and improved technologies to improve the quantity and quality of produce without jeopardizing human health.

- A reliable alternative to chemical inputs is microbial inoculants that can act as biofertilizers, bioherbicides, biopesticides, and biocontrol agents. They are beneficiary microorganisms applied to the soil or the plant to improve productivity and crop health. They are also widely used to control pests and improve the quality of the ground and crops.

- Moreover, government initiatives to promote the adoption of organic farming are anticipated to fuel the market growth during the study period. For instance, under the Green Deal's Farm to Fork strategy, the European Commission set a target of at least 25% of the EU's agricultural land under organic farming and a significant increase in organic aquaculture by 2030.

Agricultural Inoculants Market Trends

Adoption of Organic and Eco-friendly Farming Practices

- Agricultural practices are witnessing a trend shift from conventional to organic farming. This shift can be attributed to growing awareness about the adverse impact of traditional farming methods on human health and environmental safety.

- According to the Research Institute of Organic Agriculture (German: Forschungsinstitut fur biologischen Landbau (FiBL)), the area under organic cultivation increased from 70.9 million ha in 2018 to 76.4 million ha in 2021, with 187 countries practicing organic agriculture. This increases the demand for organic solutions such as inoculants and investments in localized research by private and public sectors.

- Microbial inoculants offer a natural and sustainable alternative to synthetic inputs, as they can improve soil health, increase nutrient availability, and protect against diseases. Additionally, microbial inoculants help reduce the environmental impact of synthetic inputs and promote more sustainable farming practices.

- As a result, the demand for microbial inoculants is increasing among farmers looking for ways to reduce their environmental footprint and produce healthier, more sustainable crops. Moreover, rising acreage and growing consumer demand for organic products will positively influence the agricultural inoculants market during the forecast period.

North America is the Largest Market

- North America is the largest market for agricultural inoculants, with the United States holding the majority of the share. The United States, with its highly evolved agricultural sector, has been adopting the natural and organic way of farming lately. The increasing cost of chemical inputs, their adverse effect on soil mass and the environment, and increasing awareness regarding balanced plant nutrition are the major factors driving the market in the country.

- Moreover, certain companies and research institutions emphasize introducing new products to gain a competitive advantage. For instance, developed by the Winnipeg bioresearch company XiteBio Technologies, XiteBio OptiPlus is a revolutionary proprietary liquid inoculant for soybeans powered by market-proven AGPT (Advanced Growth Promoting Technology).

- It combines the nitrogen-fixing bacteria Bradyrhizobium japonicum with patented phosphate-solubilizing plant growth-promoting rhizobacteria (PGPR), registered in Canada in February 2021, designed explicitly for soybeans. Such developments are anticipated to create demand for agricultural inoculants in the region and influence the global market during the study period.

Agricultural Inoculants Industry Overview

The agricultural inoculants market is fragmented, with international players occupying a major market share. The major players focus on R&D activities, extensive product portfolios, geographical expansions, acquisitions, and aggressive promotional strategies to uphold their position in the market. Some of the leading players are Novozymes, Lesaffre, BioceresCrop Solutions, Premier Tech, and BASF SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption of Organic and Eco-friendly Farming Practices

- 4.2.2 Declining Area of Arable Land and Rising Food Security Concerns

- 4.3 Market Restraints

- 4.3.1 High Demand for Conventional and Synthetic Products

- 4.3.2 Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Function

- 5.1.1 Crop Nutrition

- 5.1.2 Crop Protection

- 5.2 Microorganism

- 5.2.1 Bacteria

- 5.2.1.1 Rhizobacteria

- 5.2.1.2 Azotobacter

- 5.2.1.3 Phosphobacteria

- 5.2.1.4 Other Bacteria

- 5.2.2 Fungi

- 5.2.2.1 Trichoderma

- 5.2.2.2 Mycorrhiza

- 5.2.2.3 Other Fungi

- 5.2.3 Other Microorganisms

- 5.2.1 Bacteria

- 5.3 Mode of Application

- 5.3.1 Seed Inoculation

- 5.3.2 Soil Inoculation

- 5.4 Crop Type

- 5.4.1 Grains and Cereals

- 5.4.2 Pulses and Oilseeds

- 5.4.3 Commercial Crops

- 5.4.4 Fruits and Vegetables

- 5.4.5 Other Applications

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Russia

- 5.5.2.6 Italy

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Premier Tech

- 6.3.3 Lallemond Inc.

- 6.3.4 Novozymes

- 6.3.5 Mapleton Agri Biotec Pty Ltd

- 6.3.6 New Edge Microbials Pty Ltd

- 6.3.7 T.Stanes & Company Limited

- 6.3.8 AEA Investors (Verdesian Life Sciences LLC)

- 6.3.9 Lesaffre

- 6.3.10 Bioceres Crop Solutions

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024-2032 年按類型、微生物、施用方式、形式、作物類型和地區分類的農業接種劑市場報告

2024-2032 年按類型、微生物、施用方式、形式、作物類型和地區分類的農業接種劑市場報告 2024-2032 年按類型、配方、應用方法、功能、作物類型和地區分類的農業微生物市場報告

2024-2032 年按類型、配方、應用方法、功能、作物類型和地區分類的農業微生物市場報告 全球農業接種劑市場規模、佔有率、成長分析(按應用模式、按類型)-產業預測,2023-2030 年

全球農業接種劑市場規模、佔有率、成長分析(按應用模式、按類型)-產業預測,2023-2030 年 全球農業接種劑市場 - 2023-2030

全球農業接種劑市場 - 2023-2030 2030 年農業微生物市場預測:按類型、作物類型、功能、配方、應用和地區進行的全球分析

2030 年農業微生物市場預測:按類型、作物類型、功能、配方、應用和地區進行的全球分析 農業微生物學市場報告:2030 年趨勢、預測與競爭分析

農業微生物學市場報告:2030 年趨勢、預測與競爭分析 2024年基於細菌的農業微生物全球市場報告

2024年基於細菌的農業微生物全球市場報告 農業微生物市場:作物、配方、特徵、類型和應用分類 - 全球預測 2024-2030

農業微生物市場:作物、配方、特徵、類型和應用分類 - 全球預測 2024-2030 農業接種劑市場:按來源、類型和應用分類 - 2024-2030 年全球預測

農業接種劑市場:按來源、類型和應用分類 - 2024-2030 年全球預測 農業微生物市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、配方、應用模式、作物類型、地區和競爭細分

農業微生物市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、配方、應用模式、作物類型、地區和競爭細分