|

市場調查報告書

商品編碼

1403834

通訊塔:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測Telecom Towers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

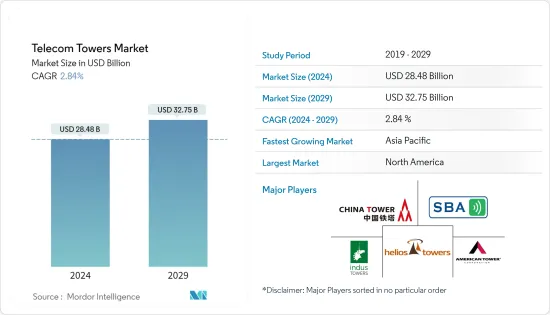

通訊塔市場規模預計到 2024 年為 284.8 億美元,預計到 2029 年將達到 327.5 億美元,在預測期內(2024-2029 年)複合年成長率為 2.84%。

鐵塔共享已成為通訊業的關鍵驅動力之一,因為它帶來了節省成本和更快的資料部署等好處。通訊塔產業作為獨立公司正在獲得大量關注,主要是在印度和美國。

主要亮點

- 5G技術的引進是通訊塔市場的主要推動要素。 5G 網路需要更密集的基礎設施,包括更多的基地台和小型基地台,以提供增強的覆蓋範圍和更快的資料通訊速度。根據代表全球行動網路營運商利益的非營利組織GSMA協會統計,截至去年終,全球86個國家已有252個商用5G網路,支援超過10億個5G連線。 此外,預計到預測期內,全球 5G 連線數將超過 50 億,帶來超過 1 兆美元的國內生產總值(GDP) 成長。同時,預計到預測期內,5G將在北美、歐洲、中國和海灣合作理事會國家達到成熟。許多低收入和中等收入國家(LMIC)可能會繼續成長。

- 隨著地理機會的減少,多樣化機會的擴大在很大程度上是由先進通訊基礎設施的出現所推動的。由於5G技術需要合適的地形,預計許多無線電塔將很快集中在重大建設項目中。然而,由於這些塔可能繼續擁有大量 5G 天線,組織可能能夠透過收購或租賃垂直房地產來開拓新路線。

- 去年,印度領先的通訊業者之一 Bharti Airtel 計劃與高通合作開發其 5G 網路技術堆疊。通訊業者計劃利用高通的5G無線接取網路技術在印度部署商用5G網路並建立虛擬5G網路和開放5G網路。

- 此外,對LTE(長期演進)先進技術的投資也正在增加。對 LTE-A 網路連接的需求激增是由多種因素推動的,包括價格實惠的智慧型手機的普及、對高速網際網路接入的需求不斷成長、對智慧城市計劃的投資不斷增加以及對物聯網設備的需求不斷成長。因素。因此,網路營運商正在積極投資LTE-A基礎設施的部署,LTE和LTE-A基地台的數量不斷增加。這些基地台將連接到通訊塔,並將能夠為最終用戶提供基本的無線電存取網路服務。由於 LTE-A 需求的增加,通訊塔市場正在經歷顯著成長。

- 據思科稱,在預測期內連接到網際網路協定(IP)網路的設備數量預計將達到 293 億。 M2M(機器對機器)連線的佔有率已從近年來的33%增加到明年的50%,今年M2M連線數可能達到147億。

- 通訊塔對環境的影響一直是一個主要問題。移動塔的輻射是一個重要問題,被認為是一種微妙的看不見的污染物,以多種方式影響生物體。

- 隨著 COVID-19 大流行的爆發,由於遠距工作條件和很大一部分人留在家裡,電訊業對網路服務的需求大幅增加。在家工作的人數增加,透過視訊會議、線上視訊觀看、下載以及增加的網路流量和資料使用增加了通訊需求。

通訊塔市場趨勢

營運商自有塔預計將錄得顯著成長

- 訊號塔的建造、運作和維護由多個行動通訊業者(MNO) 負責。這些服務擴大委託給新興國家的第三方公司。

- 再加上行動網路營運商分離和保留營運商主導的鐵塔公司的趨勢不斷增強,鐵塔公司正在超越其建設、購買和租賃垂直房地產的核心業務,以創造新的資產,並被迫考慮服務。事實上,正如許多鐵塔公司領導者所言,超過 50% 的內部成長來自傳統大型塔樓和屋頂之外的解決方案,包括街道照明和建築解決方案。

- 通訊業者擁有超過 200 萬座通訊塔,其餘由第三方建造。此外,隨著Bharti Infratel(印度)等營運商所有公司的出現,營運商自有通訊塔領域的商機正在擴大,這些公司作為客戶向其他行動通訊業者提供通訊塔。

- 塔的型態因地區而異。亞太地區的通訊業者更願意將鐵塔視為關鍵的差異化因素。相比之下,美國鐵塔市場經歷了轉型,大多數鐵塔行動通訊業者(MNO)轉向獨立公司。

- 在印度等國家,行動通訊業者經常利用聯合夥伴關係或專屬式鐵塔公司來擁有鐵塔。在多個營運商共用所有權方面,營運商擁有的鐵塔業務模式已被證明比行動通訊業者擁有鐵塔子公司更有效。

北美預計將佔據很大佔有率

- 美國形勢競爭非常激烈,許多大型供應商都在爭奪霸主地位。這種激烈的競爭是由5G通訊服務的巨大需求推動的,許多公司都在集中精力拓展業務,以抓住這一機會。美國政府有幾家主要供應商致力於合作、收購、合併、推廣和聯盟。

- SBA Communications 是美國著名的無線電塔供應商,持有約 10,000 個無線電塔,專門從事無線通訊。這項戰略合作夥伴關係持有DISH 能夠使用 SBA 在美國各地的廣泛通訊陸地產品組合。

- 此外,去年,PG&E 也宣布與 SBA Communications Corporation 達成協議,出售其無線通訊業者許可協議。這項戰略舉措將使 SBA 能夠保持其在市場上的地位,並允許更多無線提供者透過分許可進入其塔樓和建築物。

- 行動無線服務是加拿大近年來最重要、成長最快的通訊業。隨著第五代5G網路等先進技術的引入以及物聯網(IoT)等創新應用的融合,預計這一上升趨勢將持續下去。

- Bell Mobility、TCI 和 RCCI(國家無線通訊業者)在整個北美地區營運,包括西北地區、育空地區和努納武特地區,但薩斯喀徹爾除外(薩斯喀徹溫省在那裡行使唯一的市場支配力)。它在提供行動服務方面行使市場支配力該州的無線零售服務。

- 此外,安大略省和東安大略區域網路去年宣布與加拿大政府建立合作關係。此外,這項措施將為東安大略省99%的居民和企業提供可靠的無線連接,有效縮小行動電話差距,顯著提高區域安全、生產力和整體生活品質,我們的目標就是做到這一點。這項措施反映了羅傑對服務擴展的持續承諾,從而改善了服務不足地區(包括偏遠和農村地區)的連結性。

通訊塔產業概況

通訊塔市場競爭適度,有幾個主要參與者進入該市場。目前,只有少數大公司在市場佔有率方面佔據主導地位。這些通訊塔市場主要企業正在透過策略聯盟和收購通訊塔新興企業來擴大基本客群。因此,市場集中度較高,少數主導企業受益於較大的市場佔有率和盈利。

2022年10月,美國鐵塔公司(American Tower)非洲業務(ATC Africa)和Airtel Africa PLC(Airtel Africa)聯合宣布計劃擴大在肯亞和尼日爾的業務,以支援Airtel Africa的網路部署。產品協議將利用ATC Africa 在奈及利亞和烏干達的龐大通訊土地組合來實現產品開發能力。兩家公司計劃透過合作,大幅改善非洲大陸的連通性,為邊緣化人群提供數位包容性,並實現通用的溫室氣體(GHG)排放目標。

2022 年 1 月,T-Mobile US 與 Crown Castle International Corporation 宣佈建立新的 12 年合作夥伴關係,T-Mobile 可使用 Crown Castle 的訊號塔和小型基地台基地台。此交易將使UnCarrier進一步擴大和擴大其5G網路的覆蓋範圍,並創造合併後的財務協同效應,為美國各地的客戶提供服務。此外,此次交易還將支持 Crown Castle 透過小型基地台和塔實現長期收益發展。

2022 年 1 月,美國鐵塔公司宣布,將其一家全資子公司與 Coresight 合併,正式收購 Coresight Realty Corporation。此次收購預計將利用 Core Site 的網路資料中心功能和雲端入口,透過未來的電腦將推動成長,並增加當前塔樓房地產的價值。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 連結/改善與農村地區的連結性

- 改進和回應不斷成長的資料需求

- 市場挑戰

- 有關塔樓供電系統的環境問題

- 電信業者之間共享鐵塔

第 6 章 技術概覽

- 電訊業的主要趨勢 - 基礎設施共用(主動和被動)

第7章市場區隔

- 按燃料類型

- 可再生

- 不可可再生

- 依塔型分類

- 格子塔

- 引導塔

- 單極塔

- 隱形塔

- 透過安裝

- 屋頂

- 地上

- 按所有權

- 企業擁有

- 合資企業

- 個人擁有

- 行動網路業者 (MNO)專屬式

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 瑞士

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 越南

- 馬來西亞

- 菲律賓

- 澳洲/紐西蘭

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中美洲

- 哥倫比亞

- 其他拉丁美洲

- 中東/非洲

- 沙烏地阿拉伯

- 埃及

- 阿爾及利亞

- 奈及利亞

- 南非

- 坦尚尼亞

- 摩洛哥

- 其他中東和非洲

- 北美洲

第8章競爭形勢

- 公司簡介

- American Tower Corporation

- Helios Towers Africa

- Indus Towers Limited(Bharti Infratel)

- China Tower Corporation

- SBA Communications Corporation

- AT&T Inc.

- Crown Castle International Corporation

- T-Mobile USA Inc.

- GTL Infrastructure Limited

- IHS Towers(IHS Holding Limited)

- Tawal Com SA

- CellnexTelecom

- Deutsche Funkturm

- First Tower Company

- Orange

- Telenor ASA

- Zong Pakistan

- Telkom Indonesia

- Telxius Telecom SA

- Telesites SAB de CV

- Grup TorreSur

第9章投資分析

第10章投資分析市場的未來

The Telecom Towers Market size is estimated at USD 28.48 billion in 2024, and is expected to reach USD 32.75 billion by 2029, growing at a CAGR of 2.84% during the forecast period (2024-2029).

Tower-sharing is one of the significant growth drivers for the telecom industry, as it presents benefits, such as cost reduction and faster data rollout. The telecom tower industry has obtained high prominence as an independent, mainly in India and the United States.

Key Highlights

- Implementing 5G technology has been a major driving factor for the telecom tower market. 5G networks require denser infrastructure, including more cell towers and small cells, to deliver enhanced coverage and higher data speeds. According to the GSMA Association, a non-profit organization representing the interests of mobile network operators worldwide, there were already 252 commercial 5G networks in 86 countries worldwide at the end of the previous year, serving more than 1 billion 5G connections. Further, more than 5 billion 5G connections are expected globally by the forecast period, producing over USD 1 trillion in Gross Domestic Product (GDP) growth. At the same time, 5G is expected to reach maturity in North America, Europe, China, and the GCC countries by the forecast period. It will continue to grow in many low-and middle-income countries (LMICs).

- With the decline in geographical opportunities, the expansion of diversification opportunities has been significantly propelled by the emergence of advanced communication infrastructure. 5G technology demands appropriate terrain; therefore, many towers are expected to focus on their primary building business soon. However, firms and organizations may be able to explore additional routes by acquiring or leasing vertical real estate, as these towers may continue to see a significant number of 5G antennas installed on them.

- In the previous year, Bharti Airtel, one of India's major telecom operators, planned to develop its 5G network technology stack in partnership with Qualcomm. The telco plans to utilize Qualcomm 5G Radio Access Network Technologies to roll out its commercial 5G network, enabling the establishment of virtual and open 5G networks across India.

- Moreover, the increasing investment in Long Term Evolution (LTE) - Advanced technology. This surge in demand for LTE-A network connectivity results from several factors, including wider availability of affordable smartphones, a growing need for high-speed internet access, expanding investments in smart city initiatives, and a rising demand for IoT devices. Consequently, network operators are proactively investing in the deployment of LTE-A infrastructure, leading to more LTE and LTE-A base stations. These stations are connected to telecom towers, enabling them to offer essential radio access network services to end-users. As a result of the escalating demand for LTE-A, the telecom tower market is experiencing substantial growth.

- According to Cisco, the number of devices connected to the Internet Protocol (IP) network in the forecast period is expected to be 29.3 billion networked devices. The share of Machine-To-Machine (M2M) connections may grow from 33% in recent years to 50% by the following year, with 14.7 billion M2M connections by the current year.

- The environmental impacts of telecom towers have consistently been a major concern. Radiation from mobile towers has been an important issue, recognized as an unseen and subtle pollutant affecting life forms in multiple ways.

- With the outbreak of the COVID-19 pandemic, the telecom industry witnessed a significant increase in demand for internet services due to remote working conditions and a significant chunk of the population staying at home. The increase in people working from home has increased the demand for communication through video conferencing, online video viewing, downloading, and increased network traffic and data usage.

Telecom Towers Market Trends

Operator-owned Tower is Expected to Register a Significant Growth

- In the operator-owned telecom tower segment of the market studied, multiple mobile network operators (MNOs) are responsible for towers' construction, functioning, and maintenance. These services are being increasingly outsourced to third-party companies in emerging economies.

- Between TowerCos nearing saturation of addressable markets and investible portfolios globally, combined with the growing tendency of MNOs to carve out and keep operator-led TowerCo, TowerCos are compelled to look beyond their core business of building, purchasing, and leasing vertical real estate to consider new assets and new services. Indeed, as per numerous TowerCo leaders, more than 50% of organic growth now originates from solutions beyond traditional macro towers and rooftops, encompassing lamp posts and building solutions.

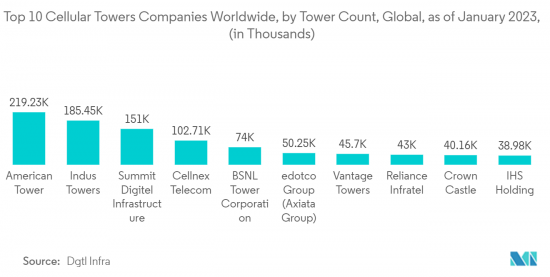

- Operators own over two million telecom towers, while third parties have constructed the rest. Furthermore, the emergence of operator-owned companies like Bharti Infratel (India), which offer telecom towers to other mobile network operators as their clients, has expanded the opportunities within the operator-owned telecom tower segment.

- Tower ownership patterns vary from region to region. The operators in the Asia Pacific region prefer to value their towers as a key differentiator. In contrast, the United States tower market has witnessed a transformation in which most towers moved from mobile network operators (MNOs) to independent enterprises.

- Mobile operators in countries like India frequently use joint partnerships or captive tower companies to own their towers. Regarding shared ownership among several operators, the operator-owned tower business model proved more effective than the mobile provider owning their tower subsidiary.

North America is Expected to Hold Major Share

- The United States landscape is highly competitive, with numerous significant vendors vying for dominance. This intense competition is driven by the country's substantial demand for 5G telecommunications services, leading many companies to focus on expanding their operations to capitalize on this opportunity. The United States government has multiple major vendors engaging in partnerships, acquisitions, mergers, rollouts, and coalitions.

- SBA Communications, a prominent tower provider in the United States, possesses approximately 10,000 towers and specializes in wireless communications. Additionally, the company has recently announced a significant long-term master lease agreement with DISH-this strategic partnership grants DISH access to SBA's extensive portfolio of wireless communications sites nationwide.

- Moreover, the previous year, PG&E made a significant announcement concerning its agreement with SBA Communications Corporation to divest its license agreements with wireless providers. This strategic move allows SBA to retain its market presence and further grant access to the towers and structures to more wireless providers through sub-licensing.

- Mobile wireless services are Canada's most significant and fastest-growing telecommunications industry in recent years. The upward trajectory is anticipated to persist as it witnesses the implementation of advanced technologies like the fifth-generation 5G network and the integration of innovative applications like the Internet of Things(IoT).

- Bell Mobility, TCI, and RCCI (collectively, the national wireless carriers) exercise market power to offer retail mobile wireless services in all provinces of North America, such as Northwest Territories, Yukon, and Nunavut, except Saskatchewan, where SaskTel exercises individual market power.

- Furthermore, the Province of Ontario and the Eastern Ontario Regional Network announced a partnership with the Government of Canada the previous year. Further, the initiatives aim to provide dependable wireless connectivity to 99% of residents and businesses in Eastern Ontario, effectively closing the cellular gap and significantly enhancing the region's safety, productivity, and overall quality of life. This effort reflects Roger's ongoing commitment to expanding its services and has resulted in improved connectivity for underserved communities, including remote and rural areas.

Telecom Towers Industry Overview

The telecom tower market's intensity of competition is moderately high and consists of several major players. Only some significant players currently dominate the market in terms of market share. These major players in the telecom tower market are expanding their customer base internationally through strategic collaborations and acquisitions of telecom tower startups. This has led to a moderately high market concentration, with a few dominant players benefiting from significant market share and profitability.

In October 2022, the American Tower Corporation's (American Tower) African operations (ATC Africa) and Airtel Africa PLC (Airtel Africa) together announced a multi-year, multi-product agreement in support of Airtel Africa's network rollout for leveraging ATC Africa's vast portfolio of communication sites across its footprint in Kenya, Niger, Nigeria, and Uganda for product development capabilities. The companies plan to significantly increase connectivity on the continent, provide digital inclusion to marginalized populations, and achieve their shared greenhouse gas (GHG) emission reduction goals through collaborative efforts.

In January 2022, The announcement of a new 12-year collaboration between T-Mobile US, Inc. and Crown Castle International Corp. would allow T-Mobile more access to Crown Castle's towers and small cell sites as the company expands its national 5G network. With the help of the deal, the Un-carrier may serve customers across the United States by further extending and broadening the coverage of the company's 5G network and generating financial synergies after its merger. Additionally, the deal assists Crown Castle in developing long-term income development from small cells and towers.

In January 2022, American Tower Corporation announced that it had officially acquired CoreSite Realty Corporation by merging one of its wholly-owned subsidiaries with CoreSite. In facilitating growth and raising the value of current tower real estate through upcoming computing opportunities, this acquisition is anticipated to use CoreSite's networked data center capabilities and cloud on-ramps.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Connecting/Improving Connectivity to Rural Areas

- 5.1.2 Improving and Catering to Increasing Data Needs

- 5.2 Market Challenges

- 5.2.1 Environmental Concerns about Power Supply Systems to Towers

- 5.2.2 Tower-sharing between Telecom Companies

6 TECHNOLOGY SNAPSHOT

- 6.1 Discussed Key Trends In Telecom Industry - Infrastructure Sharing (Active And Passive)

7 MARKET SEGMENTATION

- 7.1 By Fuel Type

- 7.1.1 Renewable

- 7.1.2 Non-renewable

- 7.2 By Type of Tower

- 7.2.1 Lattice Tower

- 7.2.2 Guyed Tower

- 7.2.3 Monopole Towers

- 7.2.4 Stealth Towers

- 7.3 By Installation

- 7.3.1 Rooftop

- 7.3.2 Ground-based

- 7.4 By Ownership

- 7.4.1 Operator-owned

- 7.4.2 Joint Venture

- 7.4.3 Private-owned

- 7.4.4 MNO Captive

- 7.5 By Geography

- 7.5.1 North America

- 7.5.1.1 United States

- 7.5.1.2 Canada

- 7.5.2 Europe

- 7.5.2.1 United Kingdom

- 7.5.2.2 Germany

- 7.5.2.3 France

- 7.5.2.4 Italy

- 7.5.2.5 Spain

- 7.5.2.6 Netherlands

- 7.5.2.7 Sweden

- 7.5.2.8 Switzerland

- 7.5.2.9 Rest of Europe

- 7.5.3 Asia-Pacific

- 7.5.3.1 China

- 7.5.3.2 India

- 7.5.3.3 Japan

- 7.5.3.4 South Korea

- 7.5.3.5 Indonesia

- 7.5.3.6 Vietnam

- 7.5.3.7 Malaysia

- 7.5.3.8 Philippines

- 7.5.3.9 Australia & New Zealand

- 7.5.3.10 Rest of Asia-Pacific

- 7.5.4 Latin America

- 7.5.4.1 Brazil

- 7.5.4.2 Mexico

- 7.5.4.3 Argentina

- 7.5.4.4 Central America

- 7.5.4.5 Columbia

- 7.5.4.6 Rest of Latin America

- 7.5.5 Middle East and Africa

- 7.5.5.1 Saudi Arabia

- 7.5.5.2 Egypt

- 7.5.5.3 Algeria

- 7.5.5.4 Nigeria

- 7.5.5.5 South Africa

- 7.5.5.6 Tanzania

- 7.5.5.7 Morocco

- 7.5.5.8 Rest of Middle East and Africa

- 7.5.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 American Tower Corporation

- 8.1.2 Helios Towers Africa

- 8.1.3 Indus Towers Limited (Bharti Infratel)

- 8.1.4 China Tower Corporation

- 8.1.5 SBA Communications Corporation

- 8.1.6 AT&T Inc.

- 8.1.7 Crown Castle International Corporation

- 8.1.8 T-Mobile USA Inc.

- 8.1.9 GTL Infrastructure Limited

- 8.1.10 IHS Towers (IHS Holding Limited)

- 8.1.11 Tawal Com SA

- 8.1.12 CellnexTelecom

- 8.1.13 Deutsche Funkturm

- 8.1.14 First Tower Company

- 8.1.15 Orange

- 8.1.16 Telenor ASA

- 8.1.17 Zong Pakistan

- 8.1.18 Telkom Indonesia

- 8.1.19 Telxius Telecom SA

- 8.1.20 Telesites SAB de CV

- 8.1.21 Grup TorreSur