|

市場調查報告書

商品編碼

1402979

輕度混合動力車:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029Mild Hybrid Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

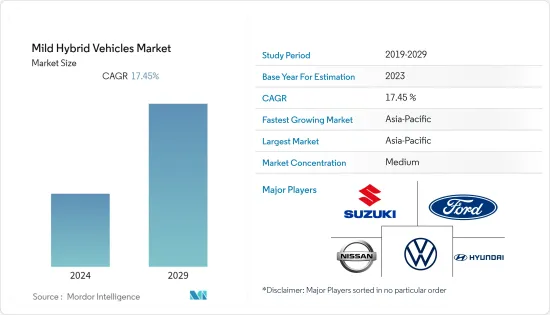

本會計年度輕度混合動力車市場規模預估為1003.5億美元。

預計未來五年將達2,242.7億美元,預測期內複合年成長率為17.45%。

嚴格的排放法規、燃油效率和政府激勵措施是推動汽車製造商和購買者從傳統汽車轉向混合汽車的主要因素。然而,純電動車的需求正在顯著成長,這可能會阻礙輕度混合動力車市場的成長。

預計亞太地區在預測期內將出現加速成長。然而,某些趨勢可能會阻礙印度等新興國家的混合汽車銷售成長,印度最近取消了 FAME 計畫對輕度混合汽車的補貼。由於北美和歐洲專注於純電動車和全混合汽車的成長,預計輕度混合動力車將顯著成長。

輕度混合動力車市場趨勢

48V 或更高電壓的輕度混合車繼續獲得主要市場佔有率

過去三年來,不少汽車製造商開始為新車標配48V輕度混合動力。世界各國對電壓低於 48V 的輕度混合動力的需求正在穩定成長。

48V 或更高電壓的輕度混合的主要優點之一是,它們以較低的成本提供全混合的許多優點,例如再生煞車和引擎啟動停止技術。特別是對於SUV和卡車等大型車輛來說,它是提高燃油效率和減少排放氣體的經濟高效的選擇。

包括梅賽德斯-奔馳、奧迪和寶馬在內的幾家主要汽車製造商都投資了48V輕度混合動力技術,目前該技術已應用於許多新車。例如,2022 年梅賽德斯-奔馳 S 級車採用 48V 輕度混合系統,可增加 22 馬力和高達 184 磅英尺的扭矩,同時提高燃油經濟性高達 10%。

世界各地的汽車製造商都在推出配備 48V 以下輕度混合系統的車輛,進一步增加了對 48V 以下細分市場的需求。

SUZUKI汽車公司、馬恆達汽車公司和現代汽車公司等主要汽車製造商過去都推出了 12V 輕度混合動力車。由於最終用戶的需求不斷增加,製造商目前正專注於開發配備48V輕度混合系統的車輛,預計這將在預測期內對市場成長構成挑戰。

亞太地區繼續佔據主要市場佔有率

亞太地區由於汽車銷量最高,佔據了最大的市場佔有率,主要是在中國。許多車企正計劃投資亞太市場,以滿足混合的強勁需求。

為了長遠發展和實現零排放,中國汽車製造商正在研究強大的混合動力汽車、插電式混合動力汽車、高效引擎等先進技術,同時引入48V輕度混合動力技術。例如,2022年9月,Volvo在印度推出了最新的汽油輕度混合動力系列。 2023年的產品陣容包括旗艦SUV XC90、中型SUV XC60、小型SUV XC40和豪華轎車S90的汽油輕度混合動力版本。

印度政府也實施了多項舉措,促進印度電動車的製造和普及,以減少排放氣體,並根據快速都市化的國際慣例發展電動交通。 NEMMP(國家電動車任務計畫)和 FAME I/II(印度混合動力和電動車的更快採用和製造)計畫有助於提高人們對電動車的初步興趣和關注。 FAME(印度混合動力車和電動車的更快採用和製造)計劃於 2015 年首次實施,並於 2019 年更新,為消費者和國內企業提供各種獎勵。例如,在FAME第二階段,政府宣佈2022年支出14億美元。本階段重點推動大眾交通工具及共享交通電動,津貼7,090輛電動公車、50萬輛電動三輪車、55萬輛電動小客車、100萬輛電動二輪車。

汽車製造商和政府的上述電動車計畫預計將在預測期內進一步推動亞太市場輕度混合的銷售。

輕度混合動力汽車產業概況

該市場的主要企業包括日產汽車有限公司、大眾汽車集團、SUZUKI汽車公司、現代汽車有限公司、福特汽車公司和豐田汽車公司。各汽車製造商推出的新產品也刺激了對輕度混合動力的需求。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 排放氣體消耗和減排

- 政府法規和獎勵

- 市場抑制因素

- 競爭替代技術

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 容量類型

- 小於48V

- 48V以上

- 車輛類型

- 小客車

- 商用車

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 其他地區

- 巴西

- 南非

- 其他

- 北美洲

第6章競爭形勢

- 供應商市場佔有率

- 公司簡介

- Toyota Motor Corporation

- Nissan Motor Co. Ltd

- Honda Motor Company Ltd

- Hyundai Motor Company

- Kia Motors Corporation

- Suzuki Motor Corporation

- Daimler AG

- Volvo Group

- Volkswagen Group

- BMW AG

- Ford Motor Company

- Audi AG

- Mitsubishi Motors Corporation

- BYD Co. Ltd

第7章 市場機會及未來趨勢

- 消費者對混合技術的認知與偏好不斷增強

- ADAS(進階駕駛輔助系統)整合

The Mild Hybrid Vehicles Market size is estimated at USD 100.35 billion in the current year. It is expected to reach USD 224.27 billion within the next five years, registering a CAGR of 17.45% during the forecast period.

Stringent emission standards, fuel efficiency, and government incentives are the major factors driving automakers and buyers to shift toward hybrid vehicles from conventional vehicles. However, demand for battery-electric vehicles is growing significantly, which might hinder the growth of the mild hybrid vehicle market.

Asia-Pacific is expected to grow faster during the forecast period. However, certain trends in emerging countries, like India, may hinder the sales growth of hybrid vehicle types as the country recently removed the subsidy for mild hybrid vehicles under the FAME scheme. North America and Europe are expected to witness considerable growth for mild hybrid vehicles as these regions are focusing more on the growth of pure electric or full hybrid vehicles.

Mild Hybrid Vehicles Market Trends

48V and Above Mild Hybrid Vehicles Continue to Capture the Major Market Share

Over the past three years, many automakers started launching a 48V mild hybrid as a standard feature in their new vehicle models. The demand for mild hybrid vehicles equipped with less than 48V capacity steadily grew in various countries across the globe.

One of the key advantages of 48V and above mild hybrid vehicles is that they can offer many of the benefits of full hybrid vehicles, such as regenerative braking and engine start-stop technology, at a lower cost. It makes them a more cost-effective option for improving fuel efficiency and reducing emissions, especially for larger vehicles such as SUVs and trucks.

Several major automakers, such as Mercedes-Benz, Audi, and BMW, are investing in 48 V mild hybrid technology, and many of their new models now feature this technology. For example, the 2022 Mercedes-Benz S-Class offers a 48 V mild hybrid system that provides an additional 22 horsepower and up to 184 lb-ft of torque while also improving fuel efficiency by up to 10%.

Automobile manufacturers in various countries globally are launching vehicles with a mild hybrid system with less than 48 V capacity, which is further increasing demand for the less than 48 V capacity segment.

Leading vehicle manufacturers such as Suzuki Corporation, Mahindra, Hyundai, etc., launched vehicles with a 12 V mild hybrid in the past. With increasing demand from end users, manufacturers are now focusing on developing vehicles with a 48 V mild hybrid system, which is expected to challenge the growth of the market over the forecast period.

Asia-Pacific Continues to Capture the Major Market Share

Asia-Pacific is capturing the largest share of the market owing to the highest vehicle sales, majorly in China. Many automotive companies planned to invest in the Asia-Pacific market to cater to the strong demand for hybrid vehicles.

With an aim for long-term development and to realize the zero-emission goal, Chinese automakers are working on strong HEV, PHEV, high-efficiency engines, and other advanced technologies while introducing 48V mild hybrid technology. For instance,

- In September 2022, Volvo launched its latest range of petrol mild-hybrid cars in India. The company's 2023 line-up includes the petrol mild-hybrid version of its flagship SUV XC90, mid-size SUV XC60, compact SUV XC40, and its luxury sedan S90.

The Indian government also undertook multiple initiatives to promote the manufacturing and adoption of electric vehicles in India to reduce emissions as per international conventions and develop e-mobility in the wake of rapid urbanization.

The National Electric Mobility Mission Plan (NEMMP) and Faster Adoption and Manufacturing of Hybrid & Electric Vehicles in India (FAME I and II) schemes helped create the initial interest and exposure to electric mobility. The Faster Adoption and Manufacturing of Hybrid & Electric Vehicles in India (FAME) program, first implemented in 2015 and updated in 2019, provides consumers and domestic companies with various incentives. For instance, in phase II of FAME, the government announced an outlay of USD 1.4 billion through 2022. This phase focused on the electrification of public and shared transportation through subsidizing 7090 e-buses, 500,000 electric three-wheelers, 550,000 electric passenger vehicles, and 1,000,000 electric two-wheelers.

The above plans by automakers and governments for electric mobility are anticipated to further boost mild hybrid vehicle sales in the Asia-Pacific market during the forecast period.

Mild Hybrid Vehicles Industry Overview

Some of the major players in the market include Nissan Motor Co. Ltd, Volkswagen Group, Suzuki Motor Corporation, Hyundai Motor Company, Ford Motor Company, and Toyota Motor Corporation, among others. New product launches by various automobile manufacturers are also boosting the demand for mild hybrid cars.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Fuel Efficiency and Emissions Reduction

- 4.1.2 Government Regulations and Incentives

- 4.2 Market Restraints

- 4.2.1 Competing Alternative Technologies

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Capacity Type

- 5.1.1 Less than 48V

- 5.1.2 48V and Above

- 5.2 Vehicle Type

- 5.2.1 Passenger Car

- 5.2.2 Commercial Vehicle

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 US

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 UK

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 South Africa

- 5.3.4.3 Other Countries

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles*

- 6.2.1 Toyota Motor Corporation

- 6.2.2 Nissan Motor Co. Ltd

- 6.2.3 Honda Motor Company Ltd

- 6.2.4 Hyundai Motor Company

- 6.2.5 Kia Motors Corporation

- 6.2.6 Suzuki Motor Corporation

- 6.2.7 Daimler AG

- 6.2.8 Volvo Group

- 6.2.9 Volkswagen Group

- 6.2.10 BMW AG

- 6.2.11 Ford Motor Company

- 6.2.12 Audi AG

- 6.2.13 Mitsubishi Motors Corporation

- 6.2.14 BYD Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Consumer Awareness and Preference for Hybrid Technology

- 7.2 Integration of Advanced Driver Assistance Systems (ADAS)

微混合動力汽車市場評估:依電池容量、電池類型、車型和地區劃分的機會和預測(2017-2031)

微混合動力汽車市場評估:依電池容量、電池類型、車型和地區劃分的機會和預測(2017-2031) 汽車市場中的混合動力系統,按類型、組件、按應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

汽車市場中的混合動力系統,按類型、組件、按應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 混合自行車市場規模 - 按技術、按產品、按應用、按最終用戶和預測,2024 年 - 2032 年

混合自行車市場規模 - 按技術、按產品、按應用、按最終用戶和預測,2024 年 - 2032 年 輕度混合動力汽車市場- 全球行業規模、佔有率、趨勢、機會和預測,按容量(小於48 V 和48 V 及以上)、按車輛類型(乘用車和商用車)、按地區、競爭情況細分2018- 2028年

輕度混合動力汽車市場- 全球行業規模、佔有率、趨勢、機會和預測,按容量(小於48 V 和48 V 及以上)、按車輛類型(乘用車和商用車)、按地區、競爭情況細分2018- 2028年 全球混合動力電動車市場:按動力傳動系統、混合程度和車輛類型分類:機會分析和產業預測(2023-2032)

全球混合動力電動車市場:按動力傳動系統、混合程度和車輛類型分類:機會分析和產業預測(2023-2032) 混合動力總成市場規模 - 按類型(全混合動力、輕度混合動力、插電式混合動力)、車輛類型、銷售管道、區域展望與預測,2023 年 - 2032 年

混合動力總成市場規模 - 按類型(全混合動力、輕度混合動力、插電式混合動力)、車輛類型、銷售管道、區域展望與預測,2023 年 - 2032 年 全球混合動力系統市場

全球混合動力系統市場 混合汽車市場:按車輛類型、零部件、混合程度、電動動力傳動系統類型、推進類型 - 俄羅斯-烏克蘭衝突、高累積的累積影響 - 2023-2030 年全球預測

混合汽車市場:按車輛類型、零部件、混合程度、電動動力傳動系統類型、推進類型 - 俄羅斯-烏克蘭衝突、高累積的累積影響 - 2023-2030 年全球預測 全球輕度混合動力汽車市場 (2022-2028)

全球輕度混合動力汽車市場 (2022-2028) 輕度混合動力車車的全球市場 2023-2027

輕度混合動力車車的全球市場 2023-2027