|

市場調查報告書

商品編碼

1433868

即時支付 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Real-Time Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

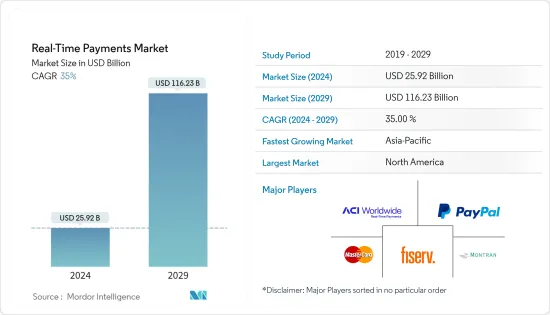

即時支付市場規模預計到2024年為 259.2 億美元,預計到2029年將達到 1162.3 億美元,在預測期內(2024-2029年)CAGR為 35%。

即時支付通常集中在低價值零售支付系統(RPS);它們不同於即時全額結算系統(RTGS)和分散式帳本支付系統。除了滿足需求和期望之外,即時支付還引起了監管機構、競爭主管機構和支付服務提供者的興趣。監管機構認為,即時支付將擴大銀行服務範圍、支持經濟成長、提供 Visa/Mastercard 網路的替代方案並減少現金和支票的使用。

主要亮點

- 全球即時支付(RTP)生態系統快速成長,企業和政府意識到實施更快、更有效率的支付系統的好處。根據ACI Worldwide2023年3月的報告,目前六大洲70多個國家支持即時支付,今年交易額達1,950億美元,較去年同期成長63%。

- 智慧型設備的日益普及和全球線上零售商務的蓬勃發展推動即時支付的快速採用。當需要向商家、帳單商、同業和其他人付款時,越來越多挑剔的消費者開始使用智慧型手機。

- 金融科技領域越來越注重使用先進技術和新業務模式,例如使用行動應用程式的開放 API 支援的即時支付系統,促進了市場成長。根據 Finastra 去年的一項研究,Baas(銀行即服務)預計在未來三年內成長 25%,為系統中嵌入的用戶提供各種功能,如即時支付、零售銀行業務等,市場上86%的參與者計劃採用開放API 來啟用可用的銀行功能。

- COVID-19 大流行導致全球數位支付的使用增加。根據2021年全球 Findex 資料庫,在中低收入經濟體(不包括中國),超過 40%使用銀行卡、電話或網路進行店內或線上支付的成年人是為了自 COVID-19 爆發以來首次。

- 然而,隨著即時支付的廣泛採用,詐欺風險顯著增加。對於大多數付款類型,客戶都可以在處理之前撤回錯誤的付款。然而,即時支付在幾秒鐘內完成,且不可撤銷,付款人無法取消交易。這些因素增加了打擊即時支付詐欺的挑戰。

即時支付市場趨勢

P2B細分市場是推動市場的關鍵

- P2B 支付是指企業與顧客之間(往來)的貨幣交易。行動交易和電子商務的強勁成長是推動該領域發展的關鍵因素。

- 線上購物和電子商務銷售的持續成長預計將推動該領域的發展。 P2B 支付使企業能夠提高客戶滿意度。 P2B結構隨著監管改革的變化而加快步伐。線上和店內帳單支付預計將帶來下一波大額支付,以保持即時成本比卡片更便宜。

- 此外,成本較低的 P2B 交易為企業提供了新水準的現金管理,這些企業可以從即時流動性中受益,因為即時結算以及與交易狀態即時通知相關的消費者服務水準的提高。

- 在零工經濟中,勞動市場的特徵是暫時的。構成(準時勞動力)的工作範例包括送餐服務、叫車服務(例如 Uber 或 Bolt)、家庭保母和遛狗者。即時支付使零工經濟工人受益匪淺,因為工人的工資很快就能得到,使他們能夠更佳規劃自己的財務,而不必擔心與現金相關的交易。

- 基於雲端的即時支付解決方案的成長趨勢可歸因於它們為零售商提供即時支付洞察的靈活性。全球大型零售商店擴大採用數位支付方式,預計將在預測期內推動市場發展。

亞太地區將成為成長最快的市場

- 對新興國家的即時交易成長預測將是將市場提升到新水準的關鍵,印度等國家將領先並超越已開發國家。世界各地啟用即時方案的政府透過為企業和消費者提供更快、更便宜、更有效率的支付方式來推動繁榮和經濟成長。

- 聯合支付介面(UPI)改變了印度人的支付方式,使他們能夠快速地將資金從一個銀行帳戶即時轉移到另一個銀行帳戶:從客戶到企業或個人之間。根據萬事達卡2022年新支付指數,印度消費者是亞太地區消費者中最願意使用新興無現金支付方式的消費者,93%的人可能在前一年進行過此類支付。

- 根據 CEBR 的資料,印度在全球企業中即時支付量最高,去年全年所有此類支付中超過 40%源自該國。印度去年進行了 486 億筆即時支付,大約是中國的 2.6 倍,中國以 185 億筆即時交易位居第二。

- 根據CEBR的資料,中國即時支付為企業和消費者帶來的淨收益達到153.97億美元,即時交易佔全部交易的5.7%。根據中國目前的即時採用水準,即時支付透過縮短浮動時間,去年每天的交易總額達到1708.00億美元。該營運資金在同年促進了約 124.11 億美元的業務產出。

- 根據 CEBR 的資料,去年香港的即時支付佔有率為 7.3%,預計將增加兩倍(到2026年將達到 22.8%)。強烈預測即時支付將使消費者和企業收益在2026年達到 2.6 億美元。去年使用即時支付的宏觀經濟效益估計為經濟產出 3.4 億美元(佔正式 GDP 的 0.09%) ,相當於3,355名工人的產出。

即時支付行業概覽

即時支付市場的競爭程度較高,因為該市場由許多大型供應商組成,除了擁有完善的分銷網路外,這些供應商還佔據顯著的市場佔有率。隨著消費者偏好的快速變化,即時支付市場已成為利潤豐厚的選擇,因此吸引了巨額投資。服務提供者建立合作夥伴關係以促進產品創新。市場上一些知名的供應商包括 ACI Worldwide Inc.、Fiserv Inc.、Paypal Holdings Inc. 和 Mastercard Inc.。

2022年6月,ACI Worldwide 宣布推出全新行動互動平台ACI Smart Engage,使世界各地的商家能夠利用語音、位置和影像辨識技術直接向消費者的智慧型手機提供服務和商品庫存,將行動購物提升到新的水準。

此外,2022年 4月,Fiserv 為金融機構推出了 Appmarket,金融機構可以在其中存取一套精選的金融科技解決方案,幫助他們更有效率地運作、吸引新客戶並更有效地競爭。 AppMarket 將為 Fiserv 金融機構客戶提供支持,並解決新興的零工經濟銀行和加密金融機會、中小企業(SMB)貸款和其他優先事項。

額外的好處:

- Excel 格式的市場估算(ME)表

- 3 個月的分析師支持

目錄

第1章:簡介

- 研究假設和市場定義

- 研究範圍

第2章:研究方法

第3章:執行摘要

第4章:市場洞察

- 市場概況

- 價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭激烈程度

- 評估 COVID-19 對市場的影響

第5章:市場動態

- 市場促進因素

- 智慧型手機普及率提高

- 輕鬆便利

- 對傳統銀行業務的依賴下降

- 市場挑戰

- 付款詐欺

- 現有對現金的依賴

- 市場機會

- 鼓勵使用數位支付的政府政策預計將有助於即時支付方式的成長

- 數位支付產業的主要法規和標準

- 主要案例研究和用例分析

- 對實際支付交易占所有交易的佔有率進行分析,並按交易量對主要國家進行區域細分

- 實際支付交易占非現金交易的比例分析,並按交易量對主要國家進行區域細分

第6章:市場細分

- 按付款方式

- 對等

- 點對點

- 按地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 西班牙

- 瑞典

- 芬蘭

- 歐洲其他地區

- 亞太

- 中國

- 印度

- 韓國

- 泰國

- 日本

- 亞太其他地區

- 拉丁美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 中東和非洲其他地區

- 北美洲

第7章:競爭格局

- 公司簡介

- ACI Worldwide Inc.

- Fiserv Inc.

- Paypal Holdings Inc.

- Mastercard Inc.

- Montran Corporation

- Temenos AG

- Volante Technologies Inc.

- Wirecard AG

- FIS Global

- Visa Inc.

- Finastra

第8章:投資分析

第9章:市場的未來

The Real-Time Payments Market size is estimated at USD 25.92 billion in 2024, and is expected to reach USD 116.23 billion by 2029, growing at a CAGR of 35% during the forecast period (2024-2029).

Real-time payments typically focus on low-value retail payment systems (RPS); they differ from real-time gross settlement systems (RTGS) and distributed ledger payment systems. In addition to meeting the demands and expectations, real-time payments have generated interest from regulators, competition authorities, and payment service providers. Regulators believe that instant payments will expand access to banking services, support economic growth, provide alternatives to Visa/Mastercard networks and reduce the use of cash and cheques.

Key Highlights

- There is rapid growth in the global Real-Time Payment (RTP) ecosystem, with businesses and governments realizing the benefits of implementing faster, more efficient payment systems. Currently, over 70 countries on six continents support real-time payments, with USD 195 billion in transaction volume this year, presenting a year-on-year growth of 63%, according to ACI Worldwide's March 2023 report.

- The growing penetration of smart devices and booming online retail commerce across the world are driving the rapid adoption of real-time payments. Increasingly, demanding consumers are turning to their smartphones when they need to pay merchants, billers, peers, and others.

- The increasing focus on using advanced technologies and new business models in the Fintech sector, like open API-enabled real-time payment systems using mobile applications, has contributed to market growth. As per a study by Finastra last year, Baas (Banking as a Service) is expected to grow by 25% over the next three years, providing various features to users embedded in the system like real-time payment, retail banking, etc., and 86% players in the market are planning to adopt open APIs to enable available banking capabilities.

- The COVID-19 pandemic resulted in increased use of digital payments across the world. According to the Global Findex Database 2021, in low and middle-income economies (excluding China), more than 40% of adults who made merchant in-store or online payments by using a card, phone, or through the internet did so for the first time since the start of COVID-19.

- However, with real-time payments gaining widespread adoption, there is a significant increase in the risk of fraud. With most payment types, a customer has the ability to recall a payment made in error before it is processed. However, an instant payment is completed in a few seconds, and as it is irrevocable, the payer cannot cancel the transaction. Such factors increase the challenges in combating fraud in the case of real-time payments.

Real Time Payments Market Trends

P2B Segment Holds the Key to Drive the Market

- P2B payments refer to monetary transactions between (to or from) businesses and customers. The unabated growth of mobile-based transactions and e-commerce is a key factor driving the development of the segment.

- The continuous growth of online shopping and e-commerce sales is expected to drive the development of the segment. P2B payments allow businesses to improve customer satisfaction. The P2B structure has been picking up the pace with the change in regulatory reforms. Online and in-store bill payments promise the next wave of huge volumes needed to keep real-time costs cheaper than cards.

- Also, lower-cost P2B transactions offer a new level of cash management to businesses that can benefit from real-time liquidity owing to instant settlement along with the added level of service to the consumer related to the instant notification of the status of the transaction.

- In the gig economy, the labor markets are characterized temporarily. Examples of jobs that comprise the (just-in-time workforce) include food delivery services, ride-hailing services (such as Uber or Bolt), house sitters, and dog walkers. Real-time payments make it big and beneficial to gig economy workers because workers are paid quickly, allowing them to better plan their finances without worrying about cash-related transactions.

- The increasing trends for cloud-based real-time payment solutions can be attributed to their flexibility in providing real-time payment insights to retailers. The growing adoption of digital payment methods in big retail stores across the globe is anticipated to drive the market in the forecasted period.

Asia Pacific will be the Fastest Growing Market

- Real-time transaction growth forecasts for emerging countries will be the key to taking the market to a new level, with countries like India leading and outpacing developed nations. Governments around the world that enable real-time schemes are driving prosperity and economic growth by providing businesses and consumers with faster, cheaper, and more efficient payment methods.

- United Payments Interface (UPI) has transformed how Indians make payments, allowing them to quickly transfer money instantly from one bank account to another: from a customer to a business or between individuals. According to Mastercard's 2022 New Payments Index, Indians are the most willing of any consumers in the Asia-Pacific region to use emerging cashless payment methods, with 93% likely to have made such a payment in the previous year.

- As per the CEBR, India accounted for the highest volume of real-time payments among businesses globally, with over 40% of all such payments made throughout last year originating in the country. India made 48.6 billion real-time payments last year, which was around 2.6 times higher than China, which was in second place with 18.5 billion real-time transactions.

- According to the CEBR, net benefits for businesses and consumers of real-time payments hit USD 15.397 billion in China, supported by real-time accounting for 5.7% of all transactions. Based on current real-time adoption levels in China, instant payments unlocked a total transaction value of USD 170.800 billion per day last year through a reduced float time. This working capital facilitated an estimated USD 12.411 billion in business output in the same year.

- In Hong Kong, real-time payments share was recorded at 7.3% last year, which is estimated to triple (22.8% by 2026), as per CEBR. The strongly predicted real-time uptake will result in consumer and business benefits reaching USD .26 billion in 2026. The macroeconomic benefits of using real-time payments were an estimated USD .34 billion of economic output (0.09% of formal GDP) last year, equivalent to the output of 3,355 workers.

Real Time Payments Industry Overview

The competitive rivalry in the Real-Time Payments Market is moderately high, as the market comprises many large vendors that command a prominent market share besides having access to well-established distribution networks. With consumer preferences changing rapidly, the Real-Time Payments Market has become a lucrative option and, thus, has attracted huge investments. The service providers are engaging in partnerships to promote product innovation. Some of the prominent vendors in the market include ACI Worldwide Inc., Fiserv Inc., Paypal Holdings Inc., and Mastercard Inc.

In June 2022, ACI Worldwide announced its new mobile engagement platform ACI Smart Engage, enabling merchants worldwide to serve up their inventory of services and goods directly to consumers' smartphones using voice, location, and image recognition technology, taking shopping-on-the-go to a new level.

Furthermore, in April 2022, Fiserv launched Appmarket for financial institutions, where they can access a curated set of fintech solutions to help them operate more efficiently, reach new customers, and compete more effectively. AppMarket would empower Fiserv financial institution clients and address emerging gig economy banking and crypto finance opportunities, small and mid-size business (SMB) lending and other priorities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Smartphone Penetration

- 5.1.2 Ease of Convenience

- 5.1.3 Falling Reliance on Traditional Banking

- 5.2 Market Challenges

- 5.2.1 Payment Fraud

- 5.2.2 Existing Dependence on Cash

- 5.3 Market Opportunities

- 5.3.1 Government Policies Encouraging the Usage of Digital Payment is Expected to Aid the Growth of Real-Time Payment Methods

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of Major Case Studies and Use-cases

- 5.6 Analysis of Real Payments Transactions as a Share of all Transactions with a Regional Breakdown of Key Countries by Transaction Volume

- 5.7 Analysis of Real Payments Transactions as a Share of Non-Cash Transactions with a Regional Breakdown of Key Countries by Transaction Volume

6 MARKET SEGMENTATION

- 6.1 By Type of Payment

- 6.1.1 P2P

- 6.1.2 P2B

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 Spain

- 6.2.2.4 Sweden

- 6.2.2.5 Finland

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 South Korea

- 6.2.3.4 Thailand

- 6.2.3.5 Japan

- 6.2.3.6 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Argentina

- 6.2.4.3 Colombia

- 6.2.4.4 Mexico

- 6.2.4.5 Rest of Latin America

- 6.2.5 Middle-East and Africa

- 6.2.5.1 United Arab Emirates

- 6.2.5.2 South Africa

- 6.2.5.3 Nigeria

- 6.2.5.4 Rest of Middle-East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ACI Worldwide Inc.

- 7.1.2 Fiserv Inc.

- 7.1.3 Paypal Holdings Inc.

- 7.1.4 Mastercard Inc.

- 7.1.5 Montran Corporation

- 7.1.6 Temenos AG

- 7.1.7 Volante Technologies Inc.

- 7.1.8 Wirecard AG

- 7.1.9 FIS Global

- 7.1.10 Visa Inc.

- 7.1.11 Finastra

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

即時付款市場:按組成部分、付款性質、產業 - 2024-2030 年全球預測

即時付款市場:按組成部分、付款性質、產業 - 2024-2030 年全球預測 日本即時支付 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)

日本即時支付 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029) 2024 年即時支付 (RTP) 全球市場報告

2024 年即時支付 (RTP) 全球市場報告 即時支付市場規模-按組件(解決方案、服務)、部署模型(本地、雲端)、支付類型(個人對個人、個人對企業、企業對消費者、企業對-業務),組織規模、最終用戶和預測,2023-2032 年

即時支付市場規模-按組件(解決方案、服務)、部署模型(本地、雲端)、支付類型(個人對個人、個人對企業、企業對消費者、企業對-業務),組織規模、最終用戶和預測,2023-2032 年 即時付款市場報告:至2030年的趨勢、預測與競爭分析

即時付款市場報告:至2030年的趨勢、預測與競爭分析 亞太地區即時支付成長機會

亞太地區即時支付成長機會 全球實時支付市場:2023 年

全球實時支付市場:2023 年 亞太實時支付市場:2023 年

亞太實時支付市場:2023 年 即時付款:全球市場

即時付款:全球市場 即時付款的全球市場 2023-2027

即時付款的全球市場 2023-2027