|

市場調查報告書

商品編碼

1406090

導電有機矽膠-市場佔有率分析、產業趨勢、統計數據、成長預測 2024-2029Conductive Silicone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

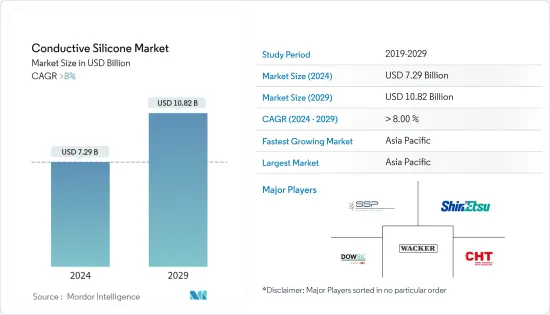

預計2024年導電矽膠市場規模為72.9億美元,預計2029年將達到108.2億美元,市場預估及預測期間(2024-2029年)複合年成長率為8%,預計將快速成長。

COVID-19 擾亂了導電有機矽膠供應鏈,但快速數位化以及遠距學習和遠距工作的採用導致電子產品需求激增。然而,隨著COVID-19病例的減少和業務恢復正常,導電性有機矽膠市場正恢復到疫情前的階段。

各行業電氣設備對導電矽膠的需求不斷成長,推動了市場的成長。

另一方面,導電矽膠橡膠所需原料的高成本預計將抑制預測期內的市場成長。

技術進步,特別是微流體裝置等導電矽膠橡膠的進步,正在為市場開闢新的可能性。

由於汽車、電子和通訊行業的需求不斷成長,亞太地區在導電有機矽膠市場佔據主導地位。

導電矽膠市場趨勢

市場區隔主導市場

- 導熱矽膠市場以導熱材料為主。導電矽膠的高導熱性使其成為多種應用的理想材料。

- 熱界面材料的需求不斷增加,因為它們擴大用於將微處理器、LED 陣列和其他發熱組件黏合到散熱器上,以提供熱傳遞途徑。

- 電子系統的小型化和不斷增加的電流密度正在推高動作溫度,從而推動用於散熱的高性能矽膠TIM(熱界面材料)的發展。因此,在預測期內,導電矽膠的需求可能會增加。

- 熱感界面材料主要用於填充熱源(如CPU和GPU)與散熱器之間的微觀間隙,改善從熱源到散熱器的熱傳遞,從而防止熱源過熱和內部系統損壞. 是可以預防的。 TIM 主要用於電腦、筆記型電腦、主機和其他電子設備(路由器、電源、放大器等)。

- 蘋果、戴爾、三星、小米等許多公司正在全球擴大智慧型手機和筆記型電腦的銷售,這對散熱膏和墊片等熱感界面材料的消耗產生了直接影響。

- 根據印度品牌股權基金會(IBEF)統計,上一年(2022年)印度通訊市場線下零售金額成長36%,2023年國內通訊市場將維持穩定的金額主導成長。那。

- 隨著政府推動Start-Ups生態系統進入熱界面材料和系統市場,熱界面材料市場規模將會擴大。自2018年以來,包括Thermulon、Rovilus、U-MAP在內的多家公司紛紛進入該市場,創新和拓展熱界面材料領域。

- 此外,由於其作為電子元件的抗靜電封裝被覆劑的作用,以及作為黏劑、密封劑和電線塗料的廣泛用途,電子/電氣領域預計將成為數量成長最快的應用領域和電纜。將會完成。

- 包括矽膠橡膠在內的導熱矽膠橡膠材料擴大應用於感測器、印刷基板、電子線路基板等電子元件中,並有望提供良好的效果。這是由於其具有適當的流動性、加工性和高熱穩定性等優點。

- 電子設備小型化的趨勢強調了保護這些組件免受電磁干擾 (EMI) 和靜電耗散 (ESD) 影響的重要性。用於 ESD 和 EMI 保護的導電矽膠橡膠的使用不斷增加,預計將在整個預測期內產生積極影響。

- 中國、印度和越南等亞太國家的消費性電子產品成長強勁,預計將在預測期內推動該地區導電矽膠的消費。

亞太地區主導市場

- 亞太地區是導電矽膠最大且成長最快的市場。電子、汽車和發電行業的使用不斷增加,推動了亞太地區對導電矽膠的需求。

- 中國、印度、日本、印尼和越南等亞太國家對發電工程的投資不斷增加,進一步推動了導電有機矽膠市場的發展。

- 抗靜電包裝也變得越來越重要,導電矽膠在電子設備中的使用預計將迅速增加,以防止充電過程中的灰塵並保持電氣和電子設備的功能和壽命。亞洲是最大的電氣和電子設備生產國,包括中國、日本、印度和東南亞國協。

- 中國是導電矽膠的重要消費國,導電有機矽用於各種行動電話組件,如小鍵盤、EMI屏蔽和溫度控管解決方案。中國是全球最大的行動電話製造國之一,2022年產量將佔全球產量的30%以上。根據Gizchina Media報道,2023年1月至8月,中國智慧型手機產量為6.79億支。

- 電瓶採用矽膠保護,避免短路等電氣危險。此外,高熔點矽膠非常適合需要高溫的應用。此外,矽膠耐腐蝕、耐高溫,是製造鋰離子電池的理想材料。

- 導熱矽膠具有高導熱率,使其成為汽車行業各種應用的理想材料。亞洲地區汽車產量佔全球一半以上,其中中國、日本、印度、韓國和泰國貢獻主要。

- 其用途正在擴大到封裝、灌封化合物、保形塗料、緊固、黏合和印刷等應用,預計將推動導電矽膠市場的發展。

- 因此,預計此類市場趨勢將在預測期內推動該地區導電有機矽膠市場的需求。

導電矽膠產業概況

導電矽膠市場較為分散。主要公司(排名不分先後)包括 Wacker Chemie AG、DOWSIL(DOW Corning)、 工業、Specialty Silicone Products, Inc 和 ACC Silicones(CHT 集團)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究成果

- 研究場所

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 消費性電子領域對散熱的需求日益增加

- 汽車產業需求增加

- 矽膠橡膠需求增加

- 抑制因素

- 與替代產品的競爭

- 原料高成本

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模)

- 產品類別

- 合成橡膠

- 樹脂

- 凝膠

- 其他產品類型(糊劑、間隙填充劑、黏劑、潤滑脂)

- 目的

- 黏劑和密封劑

- 熱界面材料

- 封裝和灌封化合物

- 保形塗層

- 其他應用(生物醫學和光催化)

- 最終用戶產業

- 車

- 建築學

- 發電

- 電力/電子

- 其他最終用戶產業(工業機械和消費品)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Avantor, Inc.

- CHT Germany GmbH

- Dow

- Elkem ASA

- Evonik Industries AG

- Ferroglobe

- LegenDay

- Momentive

- Parker Hannifin Corporation

- Reiss Manufacturing, Inc.

- Shin-Etsu Chemical Co., Ltd

- Soliani Emc srl

- Specialty Silicone Products, Inc.

- Wacker Chemie AG

第7章 市場機會及未來趨勢

- 導電矽膠在醫療設備的應用研究與開發

- 矽膠橡膠技術進步的成長

The Conductive Silicone Market size is estimated at USD 7.29 billion in 2024, and is expected to reach USD 10.82 billion by 2029, growing at a CAGR of greater than 8% during the forecast period (2024-2029).

COVID-19 disrupted the conductive silicone supply chain, yet demand for electronics surged due to rapid digitization and the adoption of distance learning and remote work. However, the conductive silicone market is recovering to its pre-pandemic stage as COVID-19 cases declined and businesses returned to normal.

Increasing demand for conductive silicone from electrical devices in various industries fuels market growth.

On the flip side, the high cost of raw material required for conductive silicon rubber is anticipated to restrain the market's growth over the forecast period.

Advancements in technology, particularly in conductive silicone rubber, such as microfluidic devices, are opening up new possibilities within the market.

The Asia-Pacific region dominates the conductive silicone market, owing to rising demand from the automotive and electronics & telecommunications industry.

Conductive Silicone Market Trends

Thermal Interface Materials Segment to Dominate the Market

- The thermal interface materials segment is the dominating segment, offering adhesion to an extensive range of substrates. The high thermal conductivity of conductive silicones makes it an ideal material for various applications.

- Thermal interface material is witnessing increased demand due to their increasing application in bonding microprocessors, LED arrays, and other heat-generating components to heat sinks, ensuring an organized path for heat transfer.

- Increasing small electronic systems and rising current densities have resulted in higher operating temperatures, thereby driving the development of high-performance silicone-based TIM (Thermal Interface Materials) for heat dissipation. Thus, it will likely cause the demand for conductive silicone over the forecast period.

- Thermal Interface Materials are majorly used to fill the microscopic gaps between the heat source (such as a CPU or GPU) and the heat sink to improve the transfer of heat from the heat source to the heat sink, which can help to prevent the heat source from overheating and damaging the internals of a system. TIM is majorly used in computers, laptops, consoles, and other electronic devices (such as routers, power supplies, and amplifiers).

- The electronics segment is one of the major driving segments for the growth of the conductive silicone market, in which many companies like Apple, Dell, Samsung, and Xiaomi are expanding their smartphone and laptop sales across the globe, directly impacting the consumption of thermal interface materials like heat dissipating pastes and pads.

- According to the India Brand Equity Foundation (IBEF), the Indian telecom market experienced a 36% increase in value in offline retail during the previous year (2022) and is anticipated to maintain stable, value-driven growth in the domestic telecom market for the year 2023.

- The thermal interface materials market size rises with governments promoting start-up ecosystems as they enter the thermal interface materials and systems market. Since 2018, many companies have entered this market to innovate and expand the thermal interface materials segment, such as Thermulon, Rovilus, and U-MAP Co.,ltd.

- In addition, the electronics & electrical segment is expected to be the fastest growing application segment in terms of volume owing to their widespread application as adhesives, sealants, and in coatings of wires & cables, along with acting as an anti-static packaging agent for electronic components.

- The heightened utilization of thermally conductive silicone rubber materials, including fluoro silicone rubber, in electronic components like sensors and printed and electronic circuit boards is expected to bring positive outcomes. This is attributed to their advantages of adequate flow, processing capabilities, and elevated thermal stability.

- The increasing trend toward miniaturization in electronic devices has underscored the importance of shielding these components from electromagnetic interference (EMI) and electrostatic dissipation (ESD). As the use of conductive silicone rubber for ESD and EMI protection continues to rise, it is expected to have a positive impact throughout the forecast period.

- Asia-Pacific countries like China, India, and Vietnam have been registering strong growth in consumer electronics, which is expected to drive the consumption of conductive silicone in the region over the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region stands to be the largest and fastest-growing market for conductive silicone. Factors such as rising utilization in electronics, automotive, and power generation industries have been driving the conductive silicone requirements in Asia-Pacific.

- Asia-Pacific countries like China, India, Japan, Indonesia, and Vietnam are witnessing increasing investment in power generation projects, further providing thrust to the conductive silicone market.

- Increased significance of anti-static packaging for dust control during electric charge and sustaining functionality and longevity of the electrical and electronic devices is anticipated to surge utilization of conductive silicone in electronics. Asia is the largest producer of electrical & electronic devices, with countries like China, Japan, India, And ASEAN Countries.

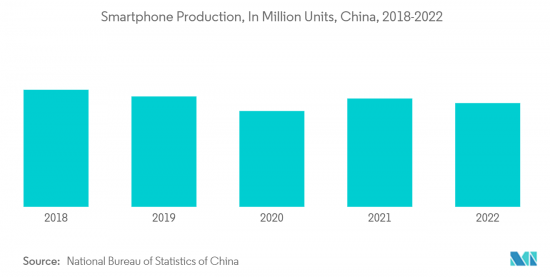

- China is a significant consumer of conductive silicone, used in various mobile phone components, such as keypads, EMI shielding, and thermal management solutions. China is one of the world's largest mobile manufacturing countries, accounting for over 30% of global production in 2022. As per Gizchina Media, the country manufactured 679 million smartphones from January 2023 to August 2023.

- The battery is shielded by silicone against short circuits and other electrical dangers. Additionally, with a high melting point, silicone is perfect for applications requiring high temperatures. In addition, silicone resists corrosion and can sustain high temperatures, making it an ideal material for producing lithium-ion batteries.

- Thermal interface materials dominate the application segment, as they offer adhesion to an extensive range of substrates, and the high thermal conductivity of conductive silicones makes them an ideal material for various applications in the automotive industry. Asian region accounts for more than half of the production of automobiles globally, with significant contributions from China, Japan, India, South Korea, and Thailand.

- Growing utilization in applications such as encapsulants & potting compounds, conformal coatings, fastening, bonding, and printing is expected to thrust the conductive silicone market.

- Hence, all such market trends are expected to drive the demand for the conductive silicone market in the region during the forecast period.

Conductive Silicone Industry Overview

The conductive silicone market is fragmented in nature. The major players (not in any particular order) include Wacker Chemie AG, DOWSIL (DOW Corning), Shin-Etsu Chemical Co., Ltd, Specialty Silicone Products, Inc., and ACC Silicones (CHT Group), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Consumption from Consumer Electronics Segment for Heat Dissipation

- 4.1.2 Growing Demand from Automotive Industry

- 4.1.3 Rising Demand for Silicon Rubber

- 4.2 Restraints

- 4.2.1 Competition from Substitutes

- 4.2.2 High Cost of Raw Material

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Product Type

- 5.1.1 Elastomers

- 5.1.2 Resins

- 5.1.3 Gels

- 5.1.4 Other Product Types (Pastes, Gap Fillers, Adhesives, and Greases)

- 5.2 Applications

- 5.2.1 Adhesives and Sealants

- 5.2.2 Thermal Interface Material

- 5.2.3 Encapsulant and Potting Compound

- 5.2.4 Conformal Coating

- 5.2.5 Other Applications (Biomedical and Photocatalysis)

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Power Generation

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user Industries (Industrial Machinery and Consumer Goods)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Avantor, Inc.

- 6.4.2 CHT Germany GmbH

- 6.4.3 Dow

- 6.4.4 Elkem ASA

- 6.4.5 Evonik Industries AG

- 6.4.6 Ferroglobe

- 6.4.7 LegenDay

- 6.4.8 Momentive

- 6.4.9 Parker Hannifin Corporation

- 6.4.10 Reiss Manufacturing, Inc.

- 6.4.11 Shin-Etsu Chemical Co., Ltd

- 6.4.12 Soliani Emc s.r.l.

- 6.4.13 Specialty Silicone Products, Inc.

- 6.4.14 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Reasearch and Development on Use of Conductive Silicone in Medical Device

- 7.2 Growth in Technological Advancements in Silicon Rubber