|

市場調查報告書

商品編碼

1414957

熱量表市場:按類型、連結性別、應用分類:2023-2032 年全球機會分析與產業預測Heat Meters Market By Type (Mechanical, Static), By Connectivity (Wireless, Wired), By Application (Residential, Commercial, Industrial): Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

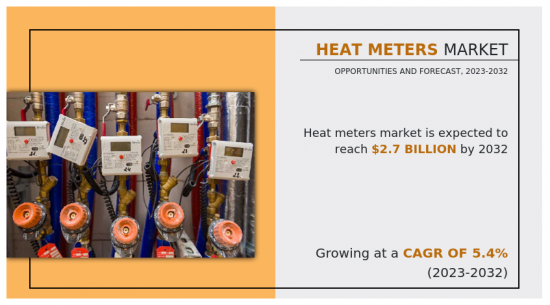

2022年熱量表市場規模為16億美元,預估2023年至2032年複合年成長率為5.4%,2032年達27億美元。

熱量表是一種測量系統中熱能的裝置。它通常在建築物中用於監測供暖消耗的熱能量。熱量表通常由測量進入或離開加熱系統的水或流體溫度的感測器和測量流經其的流體量的流量計組成。

對能源效率不斷成長的需求與更廣泛的永續性努力密切相關。熱量表允許用戶有效地追蹤和管理其能源使用情況,從而為永續性做出貢獻。熱量計鼓勵採用環保做法,減少碳排放並為更永續的未來做出貢獻。此外,熱量計是智慧型能源管理系統的重要組成部分。能源管理中智慧技術的日益普及取決於熱量計提供的準確資料。熱量計能夠實施智慧型、資料主導的解決方案,從而最佳化能源使用、減少浪費並提高效率。所有這些因素都推動了熱量表的需求。

然而,熱量表的初期成本較高,阻礙了其普及。這種初期成本阻礙了投資,特別是對於區域供熱或工業環境中的大規模安裝。對於個人用戶和小型企業來說,大量的初始投資可能會超過預期的收益並影響採用率。然而,儘管初期成本較高,熱量表透過節能、公平申請和合規性提供長期效益。

熱量計和智慧技術的整合代表了能源管理的重大進步。透過利用互連系統和資料分析,智慧熱量計可以即時洞察能源消耗。現在可以進行遠端監控和控制,使用戶能夠有效地管理他們的暖氣系統。預測性維護演算法有助於及早發現問題並確保系統可靠性。融入智慧電網可實現智慧型能源分配和最佳化使用,消除浪費。所有這些因素預計將為熱量計市場預測帶來新的成長機會。

熱量計市場按類型、連接性、應用和區域進行細分。依類型分類,市場分為機械型和固定型。到 2022 年,靜態式熱量表佔全球熱量表市場佔有率的四分之三,預計在預測期內將保持其主導地位。靜態熱量表能夠在沒有移動部件的情況下測量熱量。這種設計特性有助於提高可靠性和耐用性,因為易磨損的零件較少。

根據連接性,市場分為無線和有線。 2022 年,有線部分佔全球熱量計市場佔有率的近三分之二,預計在預測期內將保持其主導地位。隨著全球努力關注能源效率和永續性,人們正在部署有線熱量計來最佳化能源使用。有線熱量計在識別供暖系統效率低下方面發揮著重要作用,使消費者和企業能夠做出明智的決策以減少能源消耗和碳排放。它使之成為可能。所有這些因素都將增加預測期內對有線熱量表的需求。

根據應用,市場分為住宅、商業和工業。 2022 年,住宅領域佔全球熱量表市場佔有率的一半以下,預計在預測期內將保持其主導地位。在多用戶住宅和多戶住宅中,單獨的熱量表可以準確測量每個單位的消費量。這允許公平和透明的申請,這意味著居住者只需為他們使用的能源付費。此外,它還能促進居住者的公平感,鼓勵節能意識行為,並導致減少廢棄物和有效利用資源。

從區域來看,我們對北美、歐洲、亞太地區和拉丁美洲地區的市場進行了分析。到 2022 年,北美將佔熱量表全球市場佔有率的近五分之二,預計在預測期內將保持其主導地位。 LEED 認證和當地能源法規鼓勵在新建築和建築維修中安裝熱量表。熱量計透過提供準確的能源使用資料、促進透明的申請以及促進在建築物中實施節能技術和實踐來遵守這些標準。所有這些因素預計將在預測期內為北美熱量表提供新的成長機會。

目錄

第1章簡介

第 2 章執行摘要

第3章市場概況

- 市場定義和範圍

- 主要發現

- 影響因素

- 主要投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 增加區域供熱系統的引進

- 對能源效率的需求不斷成長

- 抑制因素

- 投資成本高

- 機會

- 與智慧科技融合

- 促進因素

- 價值鏈分析

- 關鍵監管分析

- 專利形勢

第4章熱量表市場:依類型

- 概述

- 機械的

- 靜電

第5章熱量表市場:連結性別

- 概述

- 無線的

- 有線

第6章熱量表市場:依應用分類

- 概述

- 住宅

- 商業的

- 工業的

第7章熱量表市場:按地區

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他

- 拉丁美洲/中東/非洲

- 巴西

- 南非

- 沙烏地阿拉伯

- 其他

第8章 競爭形勢

- 介紹

- 關鍵成功策略

- 10家主要企業產品圖譜

- 競爭對手儀表板

- 競爭熱圖

- 2022年主要企業定位

第9章 公司簡介

- Danfoss A/S

- Diehl Stiftung & Co. KG

- Honeywell International Inc.

- Ista Energy Solutions Limited

- Kamstrup

- Landis+Gyr Group AG

- QUNDIS GmbH

- Sensus

- Siemens AG

- Sontex SA

According to a new report published by Allied Market Research, titled, "Heat Meters Market," The heat meter market size was valued at $1.6 billion in 2022, and is estimated to reach $2.7 billion by 2032, growing at a CAGR of 5.4% from 2023 to 2032.

A heat meter is a device used to measure the amount of heat energy in a system. It is commonly employed in buildings to monitor the amount of thermal energy consumed for heating purposes. Heat meters typically consist of sensors to measure the temperature of the water or fluid entering and leaving a heating system, along with a flow meter to measure the volume of fluid passing through.

The rise in demand for energy efficiency is closely linked to broader efforts toward sustainability. Heat meters contribute to sustainability initiatives by enabling users to track and manage their energy usage effectively. They encourage the adoption of eco-friendly practices, reducing carbon footprints and contributing to a more sustainable future. In addition, heat meters are integral components of smart energy management systems. Increase in adoption of smart technologies in energy management relies on accurate data provided by heat meters. They enable the implementation of intelligent, data-driven solutions that optimize energy use, reduce waste, and promote efficiency. All these factors drive the demand for the heat meter.

However, the high upfront expense associated with heat meters impedes their widespread adoption. This initial cost deters investments, especially for large-scale implementations in district heating or industrial settings. For individual users or smaller businesses, the substantial initial investment might outweigh perceived benefits, impacting adoption rates. However, despite the upfront expense heat meters offer long-term benefits through energy savings, fair billing, and regulatory compliance.

The integration of heat meters with smart technologies marks a significant advancement in energy management. By leveraging interconnected systems and data analytics, smart heat meters offer real-time insights into energy consumption. They enable remote monitoring and control, empowering users to manage heating systems efficiently. Predictive maintenance algorithms help detect issues early, ensuring system reliability. Integration into smart grids allows for intelligent energy distribution and optimized usage, reducing waste. All these factors are anticipated to offer new growth opportunities in the heat meter market forecast.

The heat meter market is segmented on the basis of type, connectivity, application, and region. On the basis of type, the market is bifurcated into mechanical and static. The static type accounted for three-fourths of the global heat meter market share in 2022 and is expected to maintain its dominance during the forecast period. Static heat meters have the ability to measure heat without any moving parts. This design characteristic contributes to their reliability and durability, as there are fewer components prone to wear and tear.

On the basis of connectivity, the market is divided into wireless and wired. Wired segment accounted for less than two-thirds of the global heat meter market share in 2022 and is expected to maintain its dominance during the forecast period. As global initiatives emphasize energy efficiency and sustainability, wired heat meters are being deployed to optimize energy usage. They play a crucial role in identifying inefficiencies in heating systems, enabling consumers and businesses to make informed decisions to reduce energy consumption and carbon footprint. All these factors increase the demand for the wired heat meter during the forecast period.

On the basis of application, the market is segmented into residential, commercial, and industrial. Residential segment accounted for less than half of global heat meter market share in 2022 and is expected to maintain its dominance during the forecast period. In residential complexes or multi-family dwellings, individual heat meters allow for accurate measurement of energy consumption in each unit. This enables fair and transparent billing, ensuring that residents only pay for the energy they use. In addition, it promotes a sense of fairness among occupants and encourages energy-conscious behaviors, leading to reduced waste and more efficient use of resources.

Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA. North America accounted for less than two-fifths of the global heat meter market share in 2022 and is expected to maintain its dominance during the forecast period. The stringent building efficiency standards and regulations, driven by initiatives such as LEED certification and regional energy codes, prompt the installation of heat meters in new constructions and building retrofits. Heat meters enable compliance with these standards by providing accurate data on energy usage, promoting transparent billing, and facilitating the implementation of energy-efficient technologies and practices in buildings. All these factors are anticipated to offer new growth opportunities for the heat meters in North America during the forecast period.

Key players in the heat meter industry include: Danfoss A/S, Diehl Stiftung & Co. KG, Honeywell International Inc., Ista Energy Solutions Limited, Kamstrup, Landis+Gyr Group AG, Qundis, Sensus, Siemens AG, and Sontex SA. Apart from these major players, there are other key players in the heat meter market growth. These include Apator Group, Krohne Messtechnik GmbH, Axioma Metering, Secure Meters, Zenner, Schlumberger Limited, Itron, Bmeters Srl, Micronics Ltd, and Diehl Stiftung & Co. KG.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the heat meter market analysis from 2022 to 2032 to identify the prevailing heat meter market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the heat meter market value and segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global heat meter market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Analysis of raw material in a product (by %)

- End user preferences and pain points

- Industry life cycle assessment, by region

- Investment Opportunities

- Product Benchmarking / Product specification and applications

- Product Life Cycles

- Technology Trend Analysis

- Go To Market Strategy

- Market share analysis of players by products/segments

- New Product Development/ Product Matrix of Key Players

- Regulatory Guidelines

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- List of customers/consumers/raw material suppliers- value chain analysis

- Market share analysis of players at global/region/country level

- SWOT Analysis

Key Market Segments

By Connectivity

- Wireless

- Wired

By Application

- Residential

- Commercial

- Industrial

By Type

- Mechanical

- Static

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- Italy

- Spain

- UK

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- South Africa

- Saudi Arabia

- Rest of LAMEA

Key Market Players:

- Honeywell International Inc.

- Landis+Gyr Group AG

- Kamstrup

- Sensus

- Ista Energy Solutions Limited

- QUNDIS GmbH

- Diehl Stiftung & Co. KG

- Siemens AG

- Sontex SA

- Danfoss A/S

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Moderate bargaining power of suppliers

- 3.3.2. High threat of new entrants

- 3.3.3. Moderate threat of substitutes

- 3.3.4. Moderate intensity of rivalry

- 3.3.5. Moderate bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Increase in adoption of district heating system

- 3.4.1.2. Rise in demand for energy efficiency

- 3.4.2. Restraints

- 3.4.2.1. High cost of investment

- 3.4.3. Opportunities

- 3.4.3.1. Integration with smart technologies

- 3.4.1. Drivers

- 3.5. Value Chain Analysis

- 3.6. Key Regulation Analysis

- 3.7. Patent Landscape

CHAPTER 4: HEAT METERS MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Mechanical

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Static

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

CHAPTER 5: HEAT METERS MARKET, BY CONNECTIVITY

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Wireless

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Wired

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

CHAPTER 6: HEAT METERS MARKET, BY APPLICATION

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Residential

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Commercial

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Industrial

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: HEAT METERS MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by Type

- 7.2.3. Market size and forecast, by Connectivity

- 7.2.4. Market size and forecast, by Application

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Market size and forecast, by Type

- 7.2.5.1.2. Market size and forecast, by Connectivity

- 7.2.5.1.3. Market size and forecast, by Application

- 7.2.5.2. Canada

- 7.2.5.2.1. Market size and forecast, by Type

- 7.2.5.2.2. Market size and forecast, by Connectivity

- 7.2.5.2.3. Market size and forecast, by Application

- 7.2.5.3. Mexico

- 7.2.5.3.1. Market size and forecast, by Type

- 7.2.5.3.2. Market size and forecast, by Connectivity

- 7.2.5.3.3. Market size and forecast, by Application

- 7.3. Europe

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by Type

- 7.3.3. Market size and forecast, by Connectivity

- 7.3.4. Market size and forecast, by Application

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Market size and forecast, by Type

- 7.3.5.1.2. Market size and forecast, by Connectivity

- 7.3.5.1.3. Market size and forecast, by Application

- 7.3.5.2. France

- 7.3.5.2.1. Market size and forecast, by Type

- 7.3.5.2.2. Market size and forecast, by Connectivity

- 7.3.5.2.3. Market size and forecast, by Application

- 7.3.5.3. Italy

- 7.3.5.3.1. Market size and forecast, by Type

- 7.3.5.3.2. Market size and forecast, by Connectivity

- 7.3.5.3.3. Market size and forecast, by Application

- 7.3.5.4. Spain

- 7.3.5.4.1. Market size and forecast, by Type

- 7.3.5.4.2. Market size and forecast, by Connectivity

- 7.3.5.4.3. Market size and forecast, by Application

- 7.3.5.5. UK

- 7.3.5.5.1. Market size and forecast, by Type

- 7.3.5.5.2. Market size and forecast, by Connectivity

- 7.3.5.5.3. Market size and forecast, by Application

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Market size and forecast, by Type

- 7.3.5.6.2. Market size and forecast, by Connectivity

- 7.3.5.6.3. Market size and forecast, by Application

- 7.4. Asia-Pacific

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by Type

- 7.4.3. Market size and forecast, by Connectivity

- 7.4.4. Market size and forecast, by Application

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. China

- 7.4.5.1.1. Market size and forecast, by Type

- 7.4.5.1.2. Market size and forecast, by Connectivity

- 7.4.5.1.3. Market size and forecast, by Application

- 7.4.5.2. Japan

- 7.4.5.2.1. Market size and forecast, by Type

- 7.4.5.2.2. Market size and forecast, by Connectivity

- 7.4.5.2.3. Market size and forecast, by Application

- 7.4.5.3. India

- 7.4.5.3.1. Market size and forecast, by Type

- 7.4.5.3.2. Market size and forecast, by Connectivity

- 7.4.5.3.3. Market size and forecast, by Application

- 7.4.5.4. South Korea

- 7.4.5.4.1. Market size and forecast, by Type

- 7.4.5.4.2. Market size and forecast, by Connectivity

- 7.4.5.4.3. Market size and forecast, by Application

- 7.4.5.5. Australia

- 7.4.5.5.1. Market size and forecast, by Type

- 7.4.5.5.2. Market size and forecast, by Connectivity

- 7.4.5.5.3. Market size and forecast, by Application

- 7.4.5.6. Rest of Asia-Pacific

- 7.4.5.6.1. Market size and forecast, by Type

- 7.4.5.6.2. Market size and forecast, by Connectivity

- 7.4.5.6.3. Market size and forecast, by Application

- 7.5. LAMEA

- 7.5.1. Key market trends, growth factors and opportunities

- 7.5.2. Market size and forecast, by Type

- 7.5.3. Market size and forecast, by Connectivity

- 7.5.4. Market size and forecast, by Application

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Market size and forecast, by Type

- 7.5.5.1.2. Market size and forecast, by Connectivity

- 7.5.5.1.3. Market size and forecast, by Application

- 7.5.5.2. South Africa

- 7.5.5.2.1. Market size and forecast, by Type

- 7.5.5.2.2. Market size and forecast, by Connectivity

- 7.5.5.2.3. Market size and forecast, by Application

- 7.5.5.3. Saudi Arabia

- 7.5.5.3.1. Market size and forecast, by Type

- 7.5.5.3.2. Market size and forecast, by Connectivity

- 7.5.5.3.3. Market size and forecast, by Application

- 7.5.5.4. Rest of LAMEA

- 7.5.5.4.1. Market size and forecast, by Type

- 7.5.5.4.2. Market size and forecast, by Connectivity

- 7.5.5.4.3. Market size and forecast, by Application

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product mapping of top 10 player

- 8.4. Competitive dashboard

- 8.5. Competitive heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. Danfoss A/S

- 9.1.1. Company overview

- 9.1.2. Key executives

- 9.1.3. Company snapshot

- 9.1.4. Operating business segments

- 9.1.5. Product portfolio

- 9.1.6. Business performance

- 9.2. Diehl Stiftung & Co. KG

- 9.2.1. Company overview

- 9.2.2. Key executives

- 9.2.3. Company snapshot

- 9.2.4. Operating business segments

- 9.2.5. Product portfolio

- 9.2.6. Business performance

- 9.2.7. Key strategic moves and developments

- 9.3. Honeywell International Inc.

- 9.3.1. Company overview

- 9.3.2. Key executives

- 9.3.3. Company snapshot

- 9.3.4. Operating business segments

- 9.3.5. Product portfolio

- 9.3.6. Business performance

- 9.4. Ista Energy Solutions Limited

- 9.4.1. Company overview

- 9.4.2. Key executives

- 9.4.3. Company snapshot

- 9.4.4. Operating business segments

- 9.4.5. Product portfolio

- 9.5. Kamstrup

- 9.5.1. Company overview

- 9.5.2. Key executives

- 9.5.3. Company snapshot

- 9.5.4. Operating business segments

- 9.5.5. Product portfolio

- 9.6. Landis+Gyr Group AG

- 9.6.1. Company overview

- 9.6.2. Key executives

- 9.6.3. Company snapshot

- 9.6.4. Operating business segments

- 9.6.5. Product portfolio

- 9.6.6. Business performance

- 9.6.7. Key strategic moves and developments

- 9.7. QUNDIS GmbH

- 9.7.1. Company overview

- 9.7.2. Key executives

- 9.7.3. Company snapshot

- 9.7.4. Operating business segments

- 9.7.5. Product portfolio

- 9.8. Sensus

- 9.8.1. Company overview

- 9.8.2. Key executives

- 9.8.3. Company snapshot

- 9.8.4. Operating business segments

- 9.8.5. Product portfolio

- 9.8.6. Key strategic moves and developments

- 9.9. Siemens AG

- 9.9.1. Company overview

- 9.9.2. Key executives

- 9.9.3. Company snapshot

- 9.9.4. Operating business segments

- 9.9.5. Product portfolio

- 9.9.6. Business performance

- 9.10. Sontex SA

- 9.10.1. Company overview

- 9.10.2. Key executives

- 9.10.3. Company snapshot

- 9.10.4. Operating business segments

- 9.10.5. Product portfolio

LIST OF TABLES

- TABLE 01. GLOBAL HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 02. HEAT METERS MARKET FOR MECHANICAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. HEAT METERS MARKET FOR STATIC, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. GLOBAL HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 05. HEAT METERS MARKET FOR WIRELESS, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. HEAT METERS MARKET FOR WIRED, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. GLOBAL HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 08. HEAT METERS MARKET FOR RESIDENTIAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. HEAT METERS MARKET FOR COMMERCIAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. HEAT METERS MARKET FOR INDUSTRIAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. HEAT METERS MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. NORTH AMERICA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 13. NORTH AMERICA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 14. NORTH AMERICA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 15. NORTH AMERICA HEAT METERS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 16. U.S. HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 17. U.S. HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 18. U.S. HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 19. CANADA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 20. CANADA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 21. CANADA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 22. MEXICO HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 23. MEXICO HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 24. MEXICO HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 25. EUROPE HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 26. EUROPE HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 27. EUROPE HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 28. EUROPE HEAT METERS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 29. GERMANY HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 30. GERMANY HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 31. GERMANY HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 32. FRANCE HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 33. FRANCE HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 34. FRANCE HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 35. ITALY HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 36. ITALY HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 37. ITALY HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 38. SPAIN HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 39. SPAIN HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 40. SPAIN HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 41. UK HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 42. UK HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 43. UK HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 44. REST OF EUROPE HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 45. REST OF EUROPE HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 46. REST OF EUROPE HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 47. ASIA-PACIFIC HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 48. ASIA-PACIFIC HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 49. ASIA-PACIFIC HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 50. ASIA-PACIFIC HEAT METERS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 51. CHINA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 52. CHINA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 53. CHINA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 54. JAPAN HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 55. JAPAN HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 56. JAPAN HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 57. INDIA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 58. INDIA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 59. INDIA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 60. SOUTH KOREA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 61. SOUTH KOREA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 62. SOUTH KOREA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 63. AUSTRALIA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 64. AUSTRALIA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 65. AUSTRALIA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 66. REST OF ASIA-PACIFIC HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 67. REST OF ASIA-PACIFIC HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 68. REST OF ASIA-PACIFIC HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 69. LAMEA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 70. LAMEA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 71. LAMEA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 72. LAMEA HEAT METERS MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 73. BRAZIL HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 74. BRAZIL HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 75. BRAZIL HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 76. SOUTH AFRICA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 77. SOUTH AFRICA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 78. SOUTH AFRICA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 79. SAUDI ARABIA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 80. SAUDI ARABIA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 81. SAUDI ARABIA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 82. REST OF LAMEA HEAT METERS MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 83. REST OF LAMEA HEAT METERS MARKET, BY CONNECTIVITY, 2022-2032 ($MILLION)

- TABLE 84. REST OF LAMEA HEAT METERS MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 85. DANFOSS A/S: KEY EXECUTIVES

- TABLE 86. DANFOSS A/S: COMPANY SNAPSHOT

- TABLE 87. DANFOSS A/S: PRODUCT SEGMENTS

- TABLE 88. DANFOSS A/S: PRODUCT PORTFOLIO

- TABLE 89. DIEHL STIFTUNG & CO. KG: KEY EXECUTIVES

- TABLE 90. DIEHL STIFTUNG & CO. KG: COMPANY SNAPSHOT

- TABLE 91. DIEHL STIFTUNG & CO. KG: PRODUCT SEGMENTS

- TABLE 92. DIEHL STIFTUNG & CO. KG: PRODUCT PORTFOLIO

- TABLE 93. DIEHL STIFTUNG & CO. KG: KEY STRATERGIES

- TABLE 94. HONEYWELL INTERNATIONAL INC.: KEY EXECUTIVES

- TABLE 95. HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

- TABLE 96. HONEYWELL INTERNATIONAL INC.: PRODUCT SEGMENTS

- TABLE 97. HONEYWELL INTERNATIONAL INC.: PRODUCT PORTFOLIO

- TABLE 98. ISTA ENERGY SOLUTIONS LIMITED: KEY EXECUTIVES

- TABLE 99. ISTA ENERGY SOLUTIONS LIMITED: COMPANY SNAPSHOT

- TABLE 100. ISTA ENERGY SOLUTIONS LIMITED: PRODUCT SEGMENTS

- TABLE 101. ISTA ENERGY SOLUTIONS LIMITED: PRODUCT PORTFOLIO

- TABLE 102. KAMSTRUP: KEY EXECUTIVES

- TABLE 103. KAMSTRUP: COMPANY SNAPSHOT

- TABLE 104. KAMSTRUP: PRODUCT SEGMENTS

- TABLE 105. KAMSTRUP: PRODUCT PORTFOLIO

- TABLE 106. LANDIS+GYR GROUP AG: KEY EXECUTIVES

- TABLE 107. LANDIS+GYR GROUP AG: COMPANY SNAPSHOT

- TABLE 108. LANDIS+GYR GROUP AG: PRODUCT SEGMENTS

- TABLE 109. LANDIS+GYR GROUP AG: PRODUCT PORTFOLIO

- TABLE 110. LANDIS+GYR GROUP AG: KEY STRATERGIES

- TABLE 111. QUNDIS GMBH: KEY EXECUTIVES

- TABLE 112. QUNDIS GMBH: COMPANY SNAPSHOT

- TABLE 113. QUNDIS GMBH: PRODUCT SEGMENTS

- TABLE 114. QUNDIS GMBH: PRODUCT PORTFOLIO

- TABLE 115. SENSUS: KEY EXECUTIVES

- TABLE 116. SENSUS: COMPANY SNAPSHOT

- TABLE 117. SENSUS: PRODUCT SEGMENTS

- TABLE 118. SENSUS: PRODUCT PORTFOLIO

- TABLE 119. SENSUS: KEY STRATERGIES

- TABLE 120. SIEMENS AG: KEY EXECUTIVES

- TABLE 121. SIEMENS AG: COMPANY SNAPSHOT

- TABLE 122. SIEMENS AG: PRODUCT SEGMENTS

- TABLE 123. SIEMENS AG: PRODUCT PORTFOLIO

- TABLE 124. SONTEX SA: KEY EXECUTIVES

- TABLE 125. SONTEX SA: COMPANY SNAPSHOT

- TABLE 126. SONTEX SA: PRODUCT SEGMENTS

- TABLE 127. SONTEX SA: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. HEAT METERS MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF HEAT METERS MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN HEAT METERS MARKET (2022 TO 2032)

- FIGURE 04. TOP INVESTMENT POCKETS IN HEAT METERS MARKET (2023-2032)

- FIGURE 05. MODERATE BARGAINING POWER OF SUPPLIERS

- FIGURE 06. HIGH THREAT OF NEW ENTRANTS

- FIGURE 07. MODERATE THREAT OF SUBSTITUTES

- FIGURE 08. MODERATE INTENSITY OF RIVALRY

- FIGURE 09. MODERATE BARGAINING POWER OF BUYERS

- FIGURE 10. GLOBAL HEAT METERS MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. IMPACT OF KEY REGULATION: HEAT METERS MARKET

- FIGURE 12. PATENT ANALYSIS BY COMPANY

- FIGURE 13. PATENT ANALYSIS BY COUNTRY

- FIGURE 14. HEAT METERS MARKET, BY TYPE, 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF HEAT METERS MARKET FOR MECHANICAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF HEAT METERS MARKET FOR STATIC, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. HEAT METERS MARKET, BY CONNECTIVITY, 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF HEAT METERS MARKET FOR WIRELESS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF HEAT METERS MARKET FOR WIRED, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. HEAT METERS MARKET, BY APPLICATION, 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF HEAT METERS MARKET FOR RESIDENTIAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF HEAT METERS MARKET FOR COMMERCIAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF HEAT METERS MARKET FOR INDUSTRIAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. HEAT METERS MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 25. U.S. HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 26. CANADA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 27. MEXICO HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 28. GERMANY HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 29. FRANCE HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 30. ITALY HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 31. SPAIN HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 32. UK HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 33. REST OF EUROPE HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 34. CHINA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 35. JAPAN HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 36. INDIA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 37. SOUTH KOREA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 38. AUSTRALIA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 39. REST OF ASIA-PACIFIC HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 40. BRAZIL HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 41. SOUTH AFRICA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 42. SAUDI ARABIA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 43. REST OF LAMEA HEAT METERS MARKET, 2022-2032 ($MILLION)

- FIGURE 44. TOP WINNING STRATEGIES, BY YEAR (2020-2022)

- FIGURE 45. TOP WINNING STRATEGIES, BY DEVELOPMENT (2020-2022)

- FIGURE 46. TOP WINNING STRATEGIES, BY COMPANY (2020-2022)

- FIGURE 47. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 48. COMPETITIVE DASHBOARD

- FIGURE 49. COMPETITIVE HEATMAP: HEAT METERS MARKET

- FIGURE 50. TOP PLAYER POSITIONING, 2022

- FIGURE 51. DANFOSS A/S: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 52. DANFOSS A/S: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 53. DANFOSS A/S: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 54. DANFOSS A/S: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 55. DIEHL STIFTUNG & CO. KG: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 56. DIEHL STIFTUNG & CO. KG: NET SALES, 2020-2022 ($MILLION)

- FIGURE 57. DIEHL STIFTUNG & CO. KG: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 58. DIEHL STIFTUNG & CO. KG: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 59. HONEYWELL INTERNATIONAL INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 60. HONEYWELL INTERNATIONAL INC.: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 61. HONEYWELL INTERNATIONAL INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 62. HONEYWELL INTERNATIONAL INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 63. LANDIS+GYR: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 64. LANDIS+GYR: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 65. SIEMENS AG: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 66. SIEMENS AG: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 67. SIEMENS AG: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 68. SIEMENS AG: REVENUE SHARE BY REGION, 2022 (%)

熱量計市場:按類型、按應用、按組件、按通訊方法、按安裝方法、按地區

熱量計市場:按類型、按應用、按組件、按通訊方法、按安裝方法、按地區 熱量指數表市場報告:2030 年趨勢、預測與競爭分析

熱量指數表市場報告:2030 年趨勢、預測與競爭分析 渦街熱量表市場規模 - 按技術(機械、靜態)、按應用(住宅、商業、工業)和預測,2024 年至 2032 年

渦街熱量表市場規模 - 按技術(機械、靜態)、按應用(住宅、商業、工業)和預測,2024 年至 2032 年 熱量表市場、份額、規模、趨勢、產業分析報告:按類型、連結性別、最終用途、地區、細分市場預測,2023-2032 年

熱量表市場、份額、規模、趨勢、產業分析報告:按類型、連結性別、最終用途、地區、細分市場預測,2023-2032 年 熱量表市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(機械、靜態)、連接性(有線、無線)、最終用戶(住宅、工業、商業)、地區、競爭情況細分 2018 - 2028。

熱量表市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(機械、靜態)、連接性(有線、無線)、最終用戶(住宅、工業、商業)、地區、競爭情況細分 2018 - 2028。 熱量表市場規模、佔有率、趨勢分析報告:按類型、連結性別、最終用途、地區、細分市場趨勢,2023-2030

熱量表市場規模、佔有率、趨勢分析報告:按類型、連結性別、最終用途、地區、細分市場趨勢,2023-2030![熱量表市場規模 - 按產品(超音波、渦流)、按技術(機械、靜態)、按應用(住宅、商業[學院/大學、辦公大樓、政府建築]、工業)和預測,2023 - 2032](/sample/img/cover/42/1396580.png) 熱量表市場規模 - 按產品(超音波、渦流)、按技術(機械、靜態)、按應用(住宅、商業[學院/大學、辦公大樓、政府建築]、工業)和預測,2023 - 2032

熱量表市場規模 - 按產品(超音波、渦流)、按技術(機械、靜態)、按應用(住宅、商業[學院/大學、辦公大樓、政府建築]、工業)和預測,2023 - 2032 超音波熱量計市場報告:至2030年的趨勢、預測與競爭分析

超音波熱量計市場報告:至2030年的趨勢、預測與競爭分析 全球熱量表市場

全球熱量表市場 熱量計市場:按類型(機械、靜電)、連接性(有線連接、無線連接)、最終用戶 - 俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響 - 2023-2030 年全球預測

熱量計市場:按類型(機械、靜電)、連接性(有線連接、無線連接)、最終用戶 - 俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響 - 2023-2030 年全球預測