|

市場調查報告書

商品編碼

1414742

眼內給藥市場:按技術、按製劑類型、按疾病、按最終用戶:2023-2032 年全球機會分析和產業預測Ocular Drug Delivery Market By Technology, By Formulation Type, By Disease Indication, By End User : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

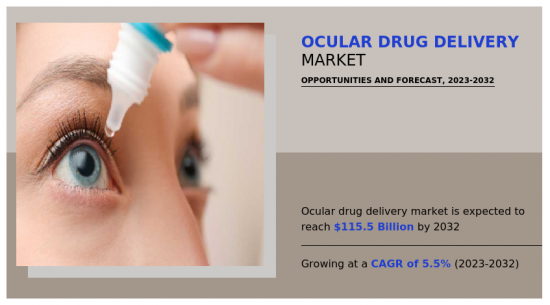

由於醫療保健產業的需求不斷增加,預計2023年至2032年眼內給藥市場將出現5.5%的顯著成長率。

眼內給藥市場的成長是由眼科疾病發生率的增加、人口老化的加劇以及眼內給藥新技術市場的快速開拓所推動的。人口快速老化和生活方式的改變是眼科疾病盛行率增加的主要風險因素,例如:

1 青光眼、老齡化黃斑部病變(AMD)等。發生老齡化黃斑部病變的風險隨著年齡的成長而增加。例如,根據美國生物技術資訊中心(NCBI)的數據,2022年估計約有2億人患有AMD,到2040年這數字預計將達到3億。因此,對能夠持續、集中地輸送藥物來治療這些疾病的高效藥物輸送系統的需求日益成長。

此外,改善眼內藥物發行策略的持續技術進步也推動了市場成長。這些進展旨在提高眼部給藥過程中的功效、準確性和患者體驗。例如,緩釋性眼內植入包括:

1 ILUVIEN 分別使用氟輕鬆和地塞米松,已被公認為一項突破性技術。這些植入透過穩定眼內的藥物濃度並在較長時間內逐漸釋放藥物,最大限度地減少了頻繁滴眼的需要。

目錄

第1章簡介

第 2 章執行摘要

第3章市場概況

- 市場定義和範圍

- 主要發現

- 影響因素

- 主要投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 眼內藥物傳輸技術進展

- 眼科疾病迅速增加

- 老年人口增加

- 抑制因素

- 嚴格的產品核可監理要求

- 機會

- 新產品核可快速增加,產品平臺強大

- 促進因素

第4章眼內給藥市場:依技術分類

- 概述

- 外用藥

- 眼內植入物

- 眼內植入

- 眼內凝膠

- 其他

第5章眼內給藥市場:依製劑類型

- 概述

- 解決方案

- 乳液

- 暫停

- 軟膏

- 其他

第6章眼內給藥市場:依疾病分類

- 概述

- 青光眼

- 糖尿病性視網膜病變

- 乾眼症

- 老齡化黃斑部病變

- 其他

第7章眼內給藥市場:依最終使用者分類

- 概述

- 醫院

- 眼科診所

- 其他

第8章眼內給藥市場:按地區

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 其他

- 拉丁美洲/中東/非洲

- 巴西

- 沙烏地阿拉伯

- 南非

- 其他

第9章 競爭形勢

- 介紹

- 關鍵成功策略

- 10家主要企業產品圖譜

- 競爭對手儀表板

- 競爭熱圖

- 2022年主要企業定位

第10章 公司簡介

- AbbVie Inc.

- Bausch Health Companies, Inc.

- Ocular Therapeutix, Inc.

- EyePoint Pharmaceuticals, Inc.

- Clearside Biomedical, Inc.

- Santen Pharmaceutical Co., Ltd.

- Novaliq GmbH

- Alimera Sciences, Inc.

- Nocox

- Kiora Pharmaceuticals, Inc.

The ocular drug delivery market is likely to experience a significant growth rate of 5.5% from 2023-2032 owing to rise in demand from healthcare industry- Allied Market Research

The ocular drug delivery market growth is driven by increase in the incidences of ocular diseases, rise in aging population, and surge in development of new technologies for ocular drug delivery. Surge in aging population and shift in lifestyles are the major risk factors that contribute to the increased prevalence of eye disorders such as

1) glaucoma, age-related macular degeneration (AMD), and others. The risk of getting age-related macular degeneration rises with the aging population. For instance, according to National Center for Biotechnology Information (NCBI) 2022, about 200 million people are estimated to have AMD and by 2040, this number is expected to reach 300 million. Thus, there is an increase in need for efficient drug delivery systems that can offer consistent and focused delivery of drugs to treat these illnesses.

Furthermore, continuous technical advancements to improve ocular drug delivery strategies are also driving the market growth. These developments are intended to enhance the effectiveness, accuracy, and patient experience while administering drugs to the eyes. For instance, sustained-release intraocular implants, such as

1) the ILUVIEN, which deliver fluocinolone acetonide and dexamethasone, respectively, have become recognized as ground-breaking technologies. These implants ensure stable drug levels in the eye and minimize the need for frequent eye drops by releasing medication gradually over an extended period of time.

In addition, increase in R&D activities and reduced side effects of drugs due to use of advanced drug delivery technologies boost the market growth. However, stringent regulatory guidelines for the drug approvals limit the growth of the ocular drug delivery market. Furthermore, high cost associated with new drug development is financially challenging for pharmaceutical companies and limit their ability to invest in innovation and develop new ocular drug delivery formulation thereby impacting the market growth. Further, shift of patient preference towards the non-invasive treatments due to ease of administration and improved compliance also drives the demand for eye drops, eye ointments, and other formulations. For instance, according to National Centers for Biotechnology Information (NCBI), topical eye drop is the most convenient and highly preferred route of drug administration.

The ocular drug delivery market is segmented on the basis of technology, formulation type, disease indication, end user, and region. On the basis of technology, the market is classified into topical, ocular insert, intraocular implants, in-situ gels, and others. As per formulation type, the market is categorized into solution, emulsion, suspension, ointment, and others. On the basis of disease indication, the market is segmented into glaucoma, diabetic retinopathy, dry eye syndrome, age related macular degeneration, and others. On the basis of end use the market is divided into hospitals, ophthalmic clinics, and others.

Region wise, the market is analyzed across North America (the U.S., Canada, and Mexico), Europe (Germany, France, the UK, Italy, Spain, and rest of Europe), Asia-Pacific (China, Japan, Australia, India, South Korea, and rest of Asia-Pacific), and LAMEA (Brazil, South Africa, Saudi Arabia, and rest of LAMEA).

Major key players that operate in the global ocular drug delivery market are Ocular Therapeutix, Inc., EyePoint Pharmaceuticals, Inc., Clearside Biomedical, Santen Pharmaceutical Co., Ltd., Abbvie Inc., Novaliq GmbH, Bausch & Lomb, Alimera Sciences, Inc., Nicox, and Kiora Pharmaceuticals, Inc. Key players operating in the market have adopted product approval and collaboration as their key strategies to expand their market share and product portfolio.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the ocular drug delivery market analysis from 2022 to 2032 to identify the prevailing ocular drug delivery market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the ocular drug delivery market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global ocular drug delivery market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Regulatory Guidelines

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- SWOT Analysis

Key Market Segments

By Technology

- Topical

- Ocular Insert

- Intraocular Implants

- In-Situ Gel

- Others

By Formulation Type

- Ointment

- Others

- Solution

- Emulsion

- Suspension

By End User

- Others

- Hospitals

- Ophthalmic Clinics

By Disease Indication

- Glaucoma

- Diabetic Retinopathy

- Dry Eye Syndrome

- Age related macular degeneration

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- South Africa

- Rest of LAMEA

Key Market Players:

- Bausch Health Companies, Inc.

- Ocular Therapeutix, Inc.

- Clearside Biomedical, Inc.

- Alimera Sciences, Inc.

- EyePoint Pharmaceuticals, Inc.

- Kiora Pharmaceuticals, Inc.

- Nocox

- Santen Pharmaceutical Co., Ltd.

- Novaliq GmbH

- AbbVie Inc.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Moderate bargaining power of suppliers

- 3.3.2. Low threat of new entrants

- 3.3.3. Moderate threat of substitutes

- 3.3.4. Moderate intensity of rivalry

- 3.3.5. Moderate bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Technological advancements in the ocular drug delivery

- 3.4.1.2. Surge in prevalence of eye disorders

- 3.4.1.3. Rise in geriatric population

- 3.4.2. Restraints

- 3.4.2.1. Stringent regulatory requirements for product approvals

- 3.4.3. Opportunities

- 3.4.3.1. Surge in new product approvals and strong product pipeline

- 3.4.1. Drivers

CHAPTER 4: OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Topical

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Ocular Insert

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Intraocular Implants

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. In-Situ Gel

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

- 4.6. Others

- 4.6.1. Key market trends, growth factors and opportunities

- 4.6.2. Market size and forecast, by region

- 4.6.3. Market share analysis by country

CHAPTER 5: OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Solution

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Emulsion

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Suspension

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Ointment

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

- 5.6. Others

- 5.6.1. Key market trends, growth factors and opportunities

- 5.6.2. Market size and forecast, by region

- 5.6.3. Market share analysis by country

CHAPTER 6: OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Glaucoma

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Diabetic Retinopathy

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Dry Eye Syndrome

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

- 6.5. Age related macular degeneration

- 6.5.1. Key market trends, growth factors and opportunities

- 6.5.2. Market size and forecast, by region

- 6.5.3. Market share analysis by country

- 6.6. Others

- 6.6.1. Key market trends, growth factors and opportunities

- 6.6.2. Market size and forecast, by region

- 6.6.3. Market share analysis by country

CHAPTER 7: OCULAR DRUG DELIVERY MARKET, BY END USER

- 7.1. Overview

- 7.1.1. Market size and forecast

- 7.2. Hospitals

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by region

- 7.2.3. Market share analysis by country

- 7.3. Ophthalmic Clinics

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by region

- 7.3.3. Market share analysis by country

- 7.4. Others

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by region

- 7.4.3. Market share analysis by country

CHAPTER 8: OCULAR DRUG DELIVERY MARKET, BY REGION

- 8.1. Overview

- 8.1.1. Market size and forecast By Region

- 8.2. North America

- 8.2.1. Key market trends, growth factors and opportunities

- 8.2.2. Market size and forecast, by Technology

- 8.2.3. Market size and forecast, by Formulation Type

- 8.2.4. Market size and forecast, by Disease Indication

- 8.2.5. Market size and forecast, by End User

- 8.2.6. Market size and forecast, by country

- 8.2.6.1. U.S.

- 8.2.6.1.1. Market size and forecast, by Technology

- 8.2.6.1.2. Market size and forecast, by Formulation Type

- 8.2.6.1.3. Market size and forecast, by Disease Indication

- 8.2.6.1.4. Market size and forecast, by End User

- 8.2.6.2. Canada

- 8.2.6.2.1. Market size and forecast, by Technology

- 8.2.6.2.2. Market size and forecast, by Formulation Type

- 8.2.6.2.3. Market size and forecast, by Disease Indication

- 8.2.6.2.4. Market size and forecast, by End User

- 8.2.6.3. Mexico

- 8.2.6.3.1. Market size and forecast, by Technology

- 8.2.6.3.2. Market size and forecast, by Formulation Type

- 8.2.6.3.3. Market size and forecast, by Disease Indication

- 8.2.6.3.4. Market size and forecast, by End User

- 8.3. Europe

- 8.3.1. Key market trends, growth factors and opportunities

- 8.3.2. Market size and forecast, by Technology

- 8.3.3. Market size and forecast, by Formulation Type

- 8.3.4. Market size and forecast, by Disease Indication

- 8.3.5. Market size and forecast, by End User

- 8.3.6. Market size and forecast, by country

- 8.3.6.1. Germany

- 8.3.6.1.1. Market size and forecast, by Technology

- 8.3.6.1.2. Market size and forecast, by Formulation Type

- 8.3.6.1.3. Market size and forecast, by Disease Indication

- 8.3.6.1.4. Market size and forecast, by End User

- 8.3.6.2. France

- 8.3.6.2.1. Market size and forecast, by Technology

- 8.3.6.2.2. Market size and forecast, by Formulation Type

- 8.3.6.2.3. Market size and forecast, by Disease Indication

- 8.3.6.2.4. Market size and forecast, by End User

- 8.3.6.3. UK

- 8.3.6.3.1. Market size and forecast, by Technology

- 8.3.6.3.2. Market size and forecast, by Formulation Type

- 8.3.6.3.3. Market size and forecast, by Disease Indication

- 8.3.6.3.4. Market size and forecast, by End User

- 8.3.6.4. Italy

- 8.3.6.4.1. Market size and forecast, by Technology

- 8.3.6.4.2. Market size and forecast, by Formulation Type

- 8.3.6.4.3. Market size and forecast, by Disease Indication

- 8.3.6.4.4. Market size and forecast, by End User

- 8.3.6.5. Spain

- 8.3.6.5.1. Market size and forecast, by Technology

- 8.3.6.5.2. Market size and forecast, by Formulation Type

- 8.3.6.5.3. Market size and forecast, by Disease Indication

- 8.3.6.5.4. Market size and forecast, by End User

- 8.3.6.6. Rest of Europe

- 8.3.6.6.1. Market size and forecast, by Technology

- 8.3.6.6.2. Market size and forecast, by Formulation Type

- 8.3.6.6.3. Market size and forecast, by Disease Indication

- 8.3.6.6.4. Market size and forecast, by End User

- 8.4. Asia-Pacific

- 8.4.1. Key market trends, growth factors and opportunities

- 8.4.2. Market size and forecast, by Technology

- 8.4.3. Market size and forecast, by Formulation Type

- 8.4.4. Market size and forecast, by Disease Indication

- 8.4.5. Market size and forecast, by End User

- 8.4.6. Market size and forecast, by country

- 8.4.6.1. Japan

- 8.4.6.1.1. Market size and forecast, by Technology

- 8.4.6.1.2. Market size and forecast, by Formulation Type

- 8.4.6.1.3. Market size and forecast, by Disease Indication

- 8.4.6.1.4. Market size and forecast, by End User

- 8.4.6.2. China

- 8.4.6.2.1. Market size and forecast, by Technology

- 8.4.6.2.2. Market size and forecast, by Formulation Type

- 8.4.6.2.3. Market size and forecast, by Disease Indication

- 8.4.6.2.4. Market size and forecast, by End User

- 8.4.6.3. India

- 8.4.6.3.1. Market size and forecast, by Technology

- 8.4.6.3.2. Market size and forecast, by Formulation Type

- 8.4.6.3.3. Market size and forecast, by Disease Indication

- 8.4.6.3.4. Market size and forecast, by End User

- 8.4.6.4. Australia

- 8.4.6.4.1. Market size and forecast, by Technology

- 8.4.6.4.2. Market size and forecast, by Formulation Type

- 8.4.6.4.3. Market size and forecast, by Disease Indication

- 8.4.6.4.4. Market size and forecast, by End User

- 8.4.6.5. South Korea

- 8.4.6.5.1. Market size and forecast, by Technology

- 8.4.6.5.2. Market size and forecast, by Formulation Type

- 8.4.6.5.3. Market size and forecast, by Disease Indication

- 8.4.6.5.4. Market size and forecast, by End User

- 8.4.6.6. Rest of Asia-Pacific

- 8.4.6.6.1. Market size and forecast, by Technology

- 8.4.6.6.2. Market size and forecast, by Formulation Type

- 8.4.6.6.3. Market size and forecast, by Disease Indication

- 8.4.6.6.4. Market size and forecast, by End User

- 8.5. LAMEA

- 8.5.1. Key market trends, growth factors and opportunities

- 8.5.2. Market size and forecast, by Technology

- 8.5.3. Market size and forecast, by Formulation Type

- 8.5.4. Market size and forecast, by Disease Indication

- 8.5.5. Market size and forecast, by End User

- 8.5.6. Market size and forecast, by country

- 8.5.6.1. Brazil

- 8.5.6.1.1. Market size and forecast, by Technology

- 8.5.6.1.2. Market size and forecast, by Formulation Type

- 8.5.6.1.3. Market size and forecast, by Disease Indication

- 8.5.6.1.4. Market size and forecast, by End User

- 8.5.6.2. Saudi Arabia

- 8.5.6.2.1. Market size and forecast, by Technology

- 8.5.6.2.2. Market size and forecast, by Formulation Type

- 8.5.6.2.3. Market size and forecast, by Disease Indication

- 8.5.6.2.4. Market size and forecast, by End User

- 8.5.6.3. South Africa

- 8.5.6.3.1. Market size and forecast, by Technology

- 8.5.6.3.2. Market size and forecast, by Formulation Type

- 8.5.6.3.3. Market size and forecast, by Disease Indication

- 8.5.6.3.4. Market size and forecast, by End User

- 8.5.6.4. Rest of LAMEA

- 8.5.6.4.1. Market size and forecast, by Technology

- 8.5.6.4.2. Market size and forecast, by Formulation Type

- 8.5.6.4.3. Market size and forecast, by Disease Indication

- 8.5.6.4.4. Market size and forecast, by End User

CHAPTER 9: COMPETITIVE LANDSCAPE

- 9.1. Introduction

- 9.2. Top winning strategies

- 9.3. Product mapping of top 10 player

- 9.4. Competitive dashboard

- 9.5. Competitive heatmap

- 9.6. Top player positioning, 2022

CHAPTER 10: COMPANY PROFILES

- 10.1. AbbVie Inc.

- 10.1.1. Company overview

- 10.1.2. Key executives

- 10.1.3. Company snapshot

- 10.1.4. Operating business segments

- 10.1.5. Product portfolio

- 10.1.6. Business performance

- 10.1.7. Key strategic moves and developments

- 10.2. Bausch Health Companies, Inc.

- 10.2.1. Company overview

- 10.2.2. Key executives

- 10.2.3. Company snapshot

- 10.2.4. Operating business segments

- 10.2.5. Product portfolio

- 10.2.6. Business performance

- 10.3. Ocular Therapeutix, Inc.

- 10.3.1. Company overview

- 10.3.2. Key executives

- 10.3.3. Company snapshot

- 10.3.4. Operating business segments

- 10.3.5. Product portfolio

- 10.4. EyePoint Pharmaceuticals, Inc.

- 10.4.1. Company overview

- 10.4.2. Key executives

- 10.4.3. Company snapshot

- 10.4.4. Operating business segments

- 10.4.5. Product portfolio

- 10.4.6. Business performance

- 10.5. Clearside Biomedical, Inc.

- 10.5.1. Company overview

- 10.5.2. Key executives

- 10.5.3. Company snapshot

- 10.5.4. Operating business segments

- 10.5.5. Product portfolio

- 10.5.6. Key strategic moves and developments

- 10.6. Santen Pharmaceutical Co., Ltd.

- 10.6.1. Company overview

- 10.6.2. Key executives

- 10.6.3. Company snapshot

- 10.6.4. Operating business segments

- 10.6.5. Product portfolio

- 10.6.6. Business performance

- 10.7. Novaliq GmbH

- 10.7.1. Company overview

- 10.7.2. Key executives

- 10.7.3. Company snapshot

- 10.7.4. Operating business segments

- 10.7.5. Product portfolio

- 10.8. Alimera Sciences, Inc.

- 10.8.1. Company overview

- 10.8.2. Key executives

- 10.8.3. Company snapshot

- 10.8.4. Operating business segments

- 10.8.5. Product portfolio

- 10.8.6. Business performance

- 10.9. Nocox

- 10.9.1. Company overview

- 10.9.2. Key executives

- 10.9.3. Company snapshot

- 10.9.4. Operating business segments

- 10.9.5. Product portfolio

- 10.10. Kiora Pharmaceuticals, Inc.

- 10.10.1. Company overview

- 10.10.2. Key executives

- 10.10.3. Company snapshot

- 10.10.4. Operating business segments

- 10.10.5. Product portfolio

LIST OF TABLES

- TABLE 01. GLOBAL OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 02. OCULAR DRUG DELIVERY MARKET FOR TOPICAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. OCULAR DRUG DELIVERY MARKET FOR OCULAR INSERT, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. OCULAR DRUG DELIVERY MARKET FOR INTRAOCULAR IMPLANTS, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. OCULAR DRUG DELIVERY MARKET FOR IN-SITU GEL, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. GLOBAL OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 08. OCULAR DRUG DELIVERY MARKET FOR SOLUTION, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. OCULAR DRUG DELIVERY MARKET FOR EMULSION, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. OCULAR DRUG DELIVERY MARKET FOR SUSPENSION, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. OCULAR DRUG DELIVERY MARKET FOR OINTMENT, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. GLOBAL OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 14. OCULAR DRUG DELIVERY MARKET FOR GLAUCOMA, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. OCULAR DRUG DELIVERY MARKET FOR DIABETIC RETINOPATHY, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. OCULAR DRUG DELIVERY MARKET FOR DRY EYE SYNDROME, BY REGION, 2022-2032 ($MILLION)

- TABLE 17. OCULAR DRUG DELIVERY MARKET FOR AGE RELATED MACULAR DEGENERATION, BY REGION, 2022-2032 ($MILLION)

- TABLE 18. OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 19. GLOBAL OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 20. OCULAR DRUG DELIVERY MARKET FOR HOSPITALS, BY REGION, 2022-2032 ($MILLION)

- TABLE 21. OCULAR DRUG DELIVERY MARKET FOR OPHTHALMIC CLINICS, BY REGION, 2022-2032 ($MILLION)

- TABLE 22. OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 23. OCULAR DRUG DELIVERY MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 24. NORTH AMERICA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 25. NORTH AMERICA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 26. NORTH AMERICA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 27. NORTH AMERICA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 28. NORTH AMERICA OCULAR DRUG DELIVERY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 29. U.S. OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 30. U.S. OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 31. U.S. OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 32. U.S. OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 33. CANADA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 34. CANADA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 35. CANADA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 36. CANADA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 37. MEXICO OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 38. MEXICO OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 39. MEXICO OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 40. MEXICO OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 41. EUROPE OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 42. EUROPE OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 43. EUROPE OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 44. EUROPE OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 45. EUROPE OCULAR DRUG DELIVERY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 46. GERMANY OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 47. GERMANY OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 48. GERMANY OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 49. GERMANY OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 50. FRANCE OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 51. FRANCE OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 52. FRANCE OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 53. FRANCE OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 54. UK OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 55. UK OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 56. UK OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 57. UK OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 58. ITALY OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 59. ITALY OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 60. ITALY OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 61. ITALY OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 62. SPAIN OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 63. SPAIN OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 64. SPAIN OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 65. SPAIN OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 66. REST OF EUROPE OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 67. REST OF EUROPE OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 68. REST OF EUROPE OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 69. REST OF EUROPE OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 70. ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 71. ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 72. ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 73. ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 74. ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 75. JAPAN OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 76. JAPAN OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 77. JAPAN OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 78. JAPAN OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 79. CHINA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 80. CHINA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 81. CHINA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 82. CHINA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 83. INDIA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 84. INDIA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 85. INDIA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 86. INDIA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 87. AUSTRALIA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 88. AUSTRALIA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 89. AUSTRALIA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 90. AUSTRALIA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 91. SOUTH KOREA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 92. SOUTH KOREA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 93. SOUTH KOREA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 94. SOUTH KOREA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 95. REST OF ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 96. REST OF ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 97. REST OF ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 98. REST OF ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 99. LAMEA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 100. LAMEA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 101. LAMEA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 102. LAMEA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 103. LAMEA OCULAR DRUG DELIVERY MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 104. BRAZIL OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 105. BRAZIL OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 106. BRAZIL OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 107. BRAZIL OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 108. SAUDI ARABIA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 109. SAUDI ARABIA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 110. SAUDI ARABIA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 111. SAUDI ARABIA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 112. SOUTH AFRICA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 113. SOUTH AFRICA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 114. SOUTH AFRICA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 115. SOUTH AFRICA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 116. REST OF LAMEA OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022-2032 ($MILLION)

- TABLE 117. REST OF LAMEA OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022-2032 ($MILLION)

- TABLE 118. REST OF LAMEA OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022-2032 ($MILLION)

- TABLE 119. REST OF LAMEA OCULAR DRUG DELIVERY MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 120. ABBVIE INC.: KEY EXECUTIVES

- TABLE 121. ABBVIE INC.: COMPANY SNAPSHOT

- TABLE 122. ABBVIE INC.: PRODUCT SEGMENTS

- TABLE 123. ABBVIE INC.: PRODUCT PORTFOLIO

- TABLE 124. ABBVIE INC.: KEY STRATERGIES

- TABLE 125. BAUSCH HEALTH COMPANIES, INC.: KEY EXECUTIVES

- TABLE 126. BAUSCH HEALTH COMPANIES, INC.: COMPANY SNAPSHOT

- TABLE 127. BAUSCH HEALTH COMPANIES, INC.: PRODUCT SEGMENTS

- TABLE 128. BAUSCH HEALTH COMPANIES, INC.: PRODUCT PORTFOLIO

- TABLE 129. OCULAR THERAPEUTIX, INC.: KEY EXECUTIVES

- TABLE 130. OCULAR THERAPEUTIX, INC.: COMPANY SNAPSHOT

- TABLE 131. OCULAR THERAPEUTIX, INC.: PRODUCT SEGMENTS

- TABLE 132. OCULAR THERAPEUTIX, INC.: PRODUCT PORTFOLIO

- TABLE 133. EYEPOINT PHARMACEUTICALS, INC.: KEY EXECUTIVES

- TABLE 134. EYEPOINT PHARMACEUTICALS, INC.: COMPANY SNAPSHOT

- TABLE 135. EYEPOINT PHARMACEUTICALS, INC.: PRODUCT SEGMENTS

- TABLE 136. EYEPOINT PHARMACEUTICALS, INC.: PRODUCT PORTFOLIO

- TABLE 137. CLEARSIDE BIOMEDICAL, INC.: KEY EXECUTIVES

- TABLE 138. CLEARSIDE BIOMEDICAL, INC.: COMPANY SNAPSHOT

- TABLE 139. CLEARSIDE BIOMEDICAL, INC.: PRODUCT SEGMENTS

- TABLE 140. CLEARSIDE BIOMEDICAL, INC.: SERVICE SEGMENTS

- TABLE 141. CLEARSIDE BIOMEDICAL, INC.: PRODUCT PORTFOLIO

- TABLE 142. CLEARSIDE BIOMEDICAL, INC.: KEY STRATERGIES

- TABLE 143. SANTEN PHARMACEUTICAL CO., LTD.: KEY EXECUTIVES

- TABLE 144. SANTEN PHARMACEUTICAL CO., LTD.: COMPANY SNAPSHOT

- TABLE 145. SANTEN PHARMACEUTICAL CO., LTD.: PRODUCT SEGMENTS

- TABLE 146. SANTEN PHARMACEUTICAL CO., LTD.: PRODUCT PORTFOLIO

- TABLE 147. NOVALIQ GMBH: KEY EXECUTIVES

- TABLE 148. NOVALIQ GMBH: COMPANY SNAPSHOT

- TABLE 149. NOVALIQ GMBH: PRODUCT SEGMENTS

- TABLE 150. NOVALIQ GMBH: PRODUCT PORTFOLIO

- TABLE 151. ALIMERA SCIENCES, INC.: KEY EXECUTIVES

- TABLE 152. ALIMERA SCIENCES, INC.: COMPANY SNAPSHOT

- TABLE 153. ALIMERA SCIENCES, INC.: PRODUCT SEGMENTS

- TABLE 154. ALIMERA SCIENCES, INC.: PRODUCT PORTFOLIO

- TABLE 155. NOCOX: KEY EXECUTIVES

- TABLE 156. NOCOX: COMPANY SNAPSHOT

- TABLE 157. NOCOX: PRODUCT SEGMENTS

- TABLE 158. NOCOX: PRODUCT PORTFOLIO

- TABLE 159. KIORA PHARMACEUTICALS, INC.: KEY EXECUTIVES

- TABLE 160. KIORA PHARMACEUTICALS, INC.: COMPANY SNAPSHOT

- TABLE 161. KIORA PHARMACEUTICALS, INC.: PRODUCT SEGMENTS

- TABLE 162. KIORA PHARMACEUTICALS, INC.: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. OCULAR DRUG DELIVERY MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF OCULAR DRUG DELIVERY MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN OCULAR DRUG DELIVERY MARKET (2022 TO 2032)

- FIGURE 04. TOP INVESTMENT POCKETS IN OCULAR DRUG DELIVERY MARKET (2023-2032)

- FIGURE 05. MODERATE BARGAINING POWER OF SUPPLIERS

- FIGURE 06. LOW THREAT OF NEW ENTRANTS

- FIGURE 07. MODERATE THREAT OF SUBSTITUTES

- FIGURE 08. MODERATE INTENSITY OF RIVALRY

- FIGURE 09. MODERATE BARGAINING POWER OF BUYERS

- FIGURE 10. GLOBAL OCULAR DRUG DELIVERY MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. OCULAR DRUG DELIVERY MARKET, BY TECHNOLOGY, 2022 AND 2032(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR TOPICAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR OCULAR INSERT, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR INTRAOCULAR IMPLANTS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR IN-SITU GEL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. OCULAR DRUG DELIVERY MARKET, BY FORMULATION TYPE, 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR SOLUTION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR EMULSION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR SUSPENSION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR OINTMENT, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. OCULAR DRUG DELIVERY MARKET, BY DISEASE INDICATION, 2022 AND 2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR GLAUCOMA, BY COUNTRY 2022 AND 2032(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR DIABETIC RETINOPATHY, BY COUNTRY 2022 AND 2032(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR DRY EYE SYNDROME, BY COUNTRY 2022 AND 2032(%)

- FIGURE 27. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR AGE RELATED MACULAR DEGENERATION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 28. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 29. OCULAR DRUG DELIVERY MARKET, BY END USER, 2022 AND 2032(%)

- FIGURE 30. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR HOSPITALS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 31. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR OPHTHALMIC CLINICS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 32. COMPARATIVE SHARE ANALYSIS OF OCULAR DRUG DELIVERY MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 33. OCULAR DRUG DELIVERY MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 34. U.S. OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 35. CANADA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 36. MEXICO OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 37. GERMANY OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 38. FRANCE OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 39. UK OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 40. ITALY OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 41. SPAIN OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 42. REST OF EUROPE OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 43. JAPAN OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 44. CHINA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 45. INDIA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 46. AUSTRALIA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 47. SOUTH KOREA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 48. REST OF ASIA-PACIFIC OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 49. BRAZIL OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 50. SAUDI ARABIA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 51. SOUTH AFRICA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 52. REST OF LAMEA OCULAR DRUG DELIVERY MARKET, 2022-2032 ($MILLION)

- FIGURE 53. TOP WINNING STRATEGIES, BY YEAR (2020-2021)

- FIGURE 54. TOP WINNING STRATEGIES, BY DEVELOPMENT (2020-2021)

- FIGURE 55. TOP WINNING STRATEGIES, BY COMPANY (2020-2021)

- FIGURE 56. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 57. COMPETITIVE DASHBOARD

- FIGURE 58. COMPETITIVE HEATMAP: OCULAR DRUG DELIVERY MARKET

- FIGURE 59. TOP PLAYER POSITIONING, 2022

- FIGURE 60. ABBVIE INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 61. ABBVIE INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 62. ABBVIE INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 63. BAUSCH HEALTH COMPANIES, INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 64. BAUSCH HEALTH COMPANIES, INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 65. BAUSCH HEALTH COMPANIES, INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 66. SANTEN PHARMACEUTICAL CO., LTD.: NET REVENUE, 2021-2023 ($MILLION)

口服給藥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按配方、類型、治療領域、最終用戶、地區和競爭細分,2019-2029F

口服給藥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按配方、類型、治療領域、最終用戶、地區和競爭細分,2019-2029F 藥品給藥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按給藥途徑、應用、地區和競爭細分,2019-2029F

藥品給藥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按給藥途徑、應用、地區和競爭細分,2019-2029F MRI引導給藥的全球市場的洞察與預測(~2030年)

MRI引導給藥的全球市場的洞察與預測(~2030年) 藥物混懸劑市場:按類型、按適應症、按最終用戶、按分銷管道:2023-2032 年全球機會分析和行業預測

藥物混懸劑市場:按類型、按適應症、按最終用戶、按分銷管道:2023-2032 年全球機會分析和行業預測 全球呼吸藥物傳輸市場:2024-2034

全球呼吸藥物傳輸市場:2024-2034 高級皮膚科給藥市場:按產品、銷售管道、應用和最終用戶 - 全球預測 2024-2030

高級皮膚科給藥市場:按產品、銷售管道、應用和最終用戶 - 全球預測 2024-2030 基於人工智慧的藥物傳遞的全球市場:預測(2023-2028)

基於人工智慧的藥物傳遞的全球市場:預測(2023-2028) 長效給藥技術和服務市場:全球和區域分析(2023-2033)

長效給藥技術和服務市場:全球和區域分析(2023-2033) 到 2030 年藥物傳輸奈米藥物的市場預測:按產品類型、模式、適應症、給藥途徑、最終用戶和地區進行全球分析

到 2030 年藥物傳輸奈米藥物的市場預測:按產品類型、模式、適應症、給藥途徑、最終用戶和地區進行全球分析 藥物傳輸市場到2030年的預測:按類型、容量、配銷通路、應用和區域進行的全球分析

藥物傳輸市場到2030年的預測:按類型、容量、配銷通路、應用和區域進行的全球分析