|

市場調查報告書

商品編碼

1365632

電動車塑膠市場:按材料、車輛和用途:2023-2032 年全球機會分析和產業預測Electric Vehicle Plastic Market By Material, By Vehicle, By Application : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

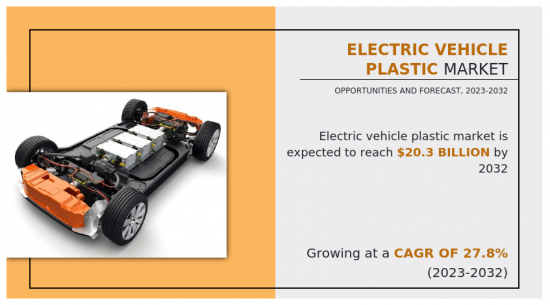

根據Allied Market Research最新報告《電動車塑膠市場》,2022年電動車塑膠市場價值為18億美元,2023年至2032年複合年複合成長率為27.8%,2032年將達203%。達到10億美元。

電動車(EV) 是汽車。電動車作為傳統內燃機汽車的綠色汽車品越來越受歡迎,因為它們具有零廢氣排放並且可以減少對石化燃料的依賴。塑膠在包括汽車製造在內的各個行業中具有廣泛的用途和應用。塑膠在汽車中用於製造保險桿、內裝、儀表板和各種其他零件,因為它們重量輕、耐用且設計高度彈性。

與傳統金屬相比,塑膠本質上是一種輕質材料。透過將輕質塑膠融入各種車輛零件中,製造商可以減輕電動車的整體重量。這種重量減輕有助於抵消電動車中使用的重型電池組的影響。更輕的車輛移動所需的能量更少,從而提高燃油效率並延長行駛距離。此外,塑膠具有廣泛的材料特性,使其適合電動車用途。塑膠可以設計成具有高強度重量比、良好的抗衝擊性和良好的隔熱性能。這些特性使塑膠成為車身面板、內裝、電池機殼等的理想選擇。這些材料的策略性使用使製造商能夠在不影響安全性或性能的情況下減輕重量。此外,塑膠比金屬提供更大的設計自由度。它可以模製成複雜的形狀,從而將多種功能整合到一個零件中。此外,塑膠可以輕鬆地根據特定的設計要求進行客製化,從而使製造商能夠製造出更輕、更有效率、更美觀的電動車。在電動車中使用輕質塑膠有助於提高燃油效率並延長續航里程。

然而,與傳統加油站的數量相比,目前充電站的數量相對有限。充電站的稀缺可能會阻礙潛在的電動車購買者,因為他們依賴現成的加油選項的便利性。有限的充電基礎設施為電動車的普及帶來了挑戰,並影響了對電動車製造中使用的電動車塑膠零件的需求。此外,電動車充電比傳統汽油或柴油車加油需要更長的時間。如此長的充電時間可能會加劇潛在電動車購買者的里程焦慮。里程焦慮是指擔心在到達充電站之前電池電量就會耗盡。這主要是出於對電動車續航里程短和充電時間的擔憂。續航里程焦慮可能會阻礙潛在買家選擇電動車,並對電動車塑膠零件的需求產生負面影響。

塑膠可用於建造充電站,包括外殼、內部零件和保護蓋。塑膠具有輕質結構、耐腐蝕和設計彈性優點,可打造美觀且耐用的充電站。此外,塑膠還可用於製造充電電纜和插頭的連接器外殼。這些外殼可保護電氣連接並確保安全可靠的充電。塑膠可以提供優異的電絕緣性、抗衝擊性以及防潮和防塵性能。此外,戶外充電站會暴露在各種天氣條件下,例如雨、雪和紫外線。耐候塑膠可以承受這些環境要素而不會劣化或喪失功能,從而確保充電基礎設施的使用壽命和可靠性。此外,塑膠易於客製化,並具有出色的設計彈性,使充電站和相關設備能夠融入各種特性和功能。這包括整合品牌元素、安全功能、電纜管理系統和方便用戶使用的介面。

COVID-19 大流行對電動車塑膠市場產生了重大影響。疫情嚴重擾亂了全球供應鏈,影響了包括汽車製造在內的各個產業。塑膠製造商面臨工廠關閉、勞動力短缺和物流中斷等挑戰。這些中斷導致電動車生產所需塑膠零件的採購出現延誤和困難。疫情的經濟影響減少了許多領域的消費者支出,包括汽車購買。儘管對電動車的需求依然強勁,但由於經濟不確定性,一些潛在買家推遲或推遲了購買決定。疫情導致原料價格波動,包括塑膠製造中使用的原料價格。供應鏈中斷和需求變化影響了石油產品和塑膠製造中使用的其他原料的定價。這項變化影響了電動車的整體製造成本,並影響了塑膠市場。

目錄

第1章 簡介

第2章 執行摘要

第3章 市場概況

- 市場定義和範圍

- 主要發現

- 影響要素

- 主要投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 抑制因素

- 機會

- COVID-19 市場影響分析

- 平均售價

- 市場佔有率分析

- 品牌佔有率分析

- 貿易資料分析

- 產品消費

- 價值鏈分析

- 法規指引

- 關鍵法規分析

- 專利形勢

第4章 電動車塑膠市場:依材料分類

- 概述

- 聚丙烯(PP)

- 聚氨酯(PUR)

- 丙烯腈丁二烯苯乙烯 (ABS)

- 聚氯乙烯(PVC)

- 聚甲醛 (POM)

- 聚苯乙烯(PS)

- 聚碳酸酯(PC)

- 聚醯胺 (PA)

- 壓克力(壓克力)

- 其他(聚乙烯)

第5章 電動車塑膠市場:依車輛分類

- 概述

- 混合電動車(HEV)

- 插電式混合(PHEV)

- 純電動車(BEV)

第6章 電動車塑膠市場:依用途

- 概述

- 內裝的

- 外裝的

- 其他

第7章 電動車塑膠市場:按地區

- 概述

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他

- 拉丁美洲/中東/非洲

- 巴西

- 南阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他

第8章 競爭形勢

- 介紹

- 關鍵成功策略

- 10家主要企業產品圖譜

- 競爭儀表板

- 競爭熱圖

- 2022年主要企業定位

第9章 公司簡介

- BASF SE

- SABIC

- LyondellBasell Industries Holdings BV

- Evonik Industries

- Covestro AG.

- DUPONT

- Sumitomo Chemicals Co. Ltd.

- LG Chem Ltd

- Asahi Kasei

- LANXESS

According to a new report published by Allied Market Research, titled, "Electric Vehicle Plastic Market," The electric vehicle plastic market was valued at $1.8 billion in 2022, and is estimated to reach $20.3 billion by 2032, growing at a CAGR of 27.8% from 2023 to 2032.

Electric vehicles (Evs) are automobiles that are powered by one or more electric motors, using electricity stored in rechargeable batteries or obtained from an external source such as a charging station. Evs are gaining popularity as a more environmentally friendly alternative to traditional internal combustion engine vehicles, as they produce zero tailpipe emissions and can reduce dependence on fossil fuels. Plastics have a wide range of uses and applications in various industries, including automotive manufacturing. Plastics are used in vehicles for components such as bumpers, interior trim, dashboards, and various other parts due to their lightweight, durability, and design flexibility.

Plastics are inherently lightweight materials compared to traditional metals. By incorporating lightweight plastics in various vehicle components, manufacturers can reduce the overall weight of the EV. This weight reduction helps offset the heavy battery packs used in Evs, which are necessary for storing and delivering electric power. A lighter vehicle requires less energy to move, leading to improved fuel efficiency and extended driving range. Moreover, plastics offer a wide range of material properties that make them suitable for EV applications. They can be engineered to have high strength-to-weight ratios, excellent impact resistance, and good thermal insulation properties. These characteristics make plastics ideal for use in body panels, interior trim, and battery enclosures. By utilizing these materials strategically, manufacturers can reduce weight without compromising safety or performance. Furthermore, plastics provide greater design flexibility compared to metals. They can be molded into complex shapes, allowing for the integration of multiple functionalities within a single component. This flexibility enables innovative designs that optimize aerodynamics and reduce drag, further enhancing the fuel efficiency of Evs. In addition, plastics can be easily customized to meet specific design requirements, allowing manufacturers to create lightweight, efficient, and aesthetically appealing Evs. The use of lightweight plastics in electric vehicles contributes to improved fuel efficiency and extended driving range.

However, the current number of charging stations is relatively limited compared to the number of traditional fuel stations. This scarcity of charging stations can discourage potential EV buyers who rely on the convenience of readily available refueling options. The limited charging infrastructure poses a challenge for the widespread adoption of electric vehicles, thereby impacting the demand for EV plastic components used in their manufacturing. Moreover, charging an electric vehicle takes more time compared to refueling a traditional gasoline or diesel vehicle. This longer charging duration can contribute to range anxiety among potential EV buyers. Range anxiety refers to the fear of running out of battery power before reaching a charging station. It is primarily driven by concerns about the limited range of electric vehicles and the time required for recharging. Range anxiety can discourage potential buyers from choosing electric vehicles, negatively affecting the demand for EV plastic components.

Plastics can be used in the construction of charging stations, including their external casings, internal components, and protective covers. Plastics offer advantages such as lightweight construction, corrosion resistance, and design flexibility, allowing for the creation of aesthetically pleasing and durable charging stations. Moreover, plastics can be utilized in the manufacturing of connector housings for charging cables and plugs. These housings provide protection for electrical connections and ensure safe and reliable charging. Plastics can offer excellent electrical insulation properties, impact resistance, and resistance to moisture and dust ingress. Furthermore, outdoor charging stations are exposed to various weather conditions, such as rain, snow, and UV radiation. Plastics with excellent weather resistance properties can withstand these environmental factors without degradation or loss of functionality, ensuring the longevity and reliability of the charging infrastructure. In addition, plastics allow for easy customization and design flexibility, enabling the integration of different features and functionalities into charging stations and related equipment. This includes the incorporation of branding elements, safety features, cable management systems, and user-friendly interfaces.

The COVID-19 pandemic had significant impacts on the market for electric vehicle plastic market. The pandemic severely disrupted global supply chains, affecting various industries, including automotive manufacturing. Plastic manufacturers faced challenges such as factory shutdowns, labor shortages, and logistics disruptions. These disruptions resulted in delays and difficulties in sourcing plastic components required for EV production. The economic impact of the pandemic led to reduced consumer spending in many areas, including automotive purchases. While the demand for Evs remained strong, some potential buyers delayed or postponed their purchasing decisions due to economic uncertainty. This slowdown in consumer spending indirectly affected the demand for plastic components used in Evs. The pandemic has caused fluctuations in raw material prices, including those used in plastic manufacturing. Disruptions in supply chains and shifts in demand have influenced the pricing of petroleum-based products and other raw materials used in plastic production. This volatility impacted the overall cost of manufacturing electric vehicles and influenced the plastic market.

The key players profiled in this report include: BASF SE, SABIC, LyondellBasell Industries Holdings B.V., Evonik Industries, Covestro AG., DUPONT, Sumitomo Chemicals Co. Ltd., LG Chem Ltd, Asahi Kasei, and LANXESS. The market players are continuously striving to achieve a dominant position in this competitive market using strategies such as collaborations and acquisitions.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the electric vehicle plastic market analysis from 2022 to 2032 to identify the prevailing electric vehicle plastic market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the electric vehicle plastic market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global electric vehicle plastic market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 20% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline talk to the sales executive to know more)

- Product Benchmarking / Product specification and applications

- Technology Trend Analysis

- Distributor margin Analysis

- Patient/epidemiology data at country, region, global level

- Regulatory Guidelines

- Strategic Recommedations

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Brands Share Analysis

- Criss-cross segment analysis- market size and forecast

- Historic market data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- SWOT Analysis

Key Market Segments

By Material

- Polypropylene (PP)

- Polyurethane (PUR)

- Acrylonitrile Butadiene Styrene (ABS)

- Polyvinyl Chloride (PVC)

- Polyoxymethylene (POM)

- Polystyrene (PS)

- Polycarbonate (PC)

- Polyamide (PA)

- Acrylic (PMMA)

- Others (Polyethylene)

By Vehicle

- Hybrid Electric Vehicles (HEVs)

- Plug-In Hybrid Electric Vehicles (PHEVs)

- Battery Electric Vehicles (BEVs)

By Application

- Interior furnishing

- Exterior furnishing

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- South Arabia

- United Arab Emirates

- South Africa

- Rest of LAMEA

Key Market Players:

- BASF SE

- SABIC

- LyondellBasell Industries Holdings B.V.

- Evonik Industries

- Covestro AG.

- DUPONT

- Sumitomo Chemicals Co. Ltd.

- LG Chem Ltd

- Asahi Kasei

- LANXESS

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Average Selling Price

- 3.7. Market Share Analysis

- 3.8. Brand Share Analysis

- 3.9. Trade Data Analysis

- 3.10. Product Consumption

- 3.11. Value Chain Analysis

- 3.12. Regulatory Guidelines

- 3.13. Key Regulation Analysis

- 3.14. Patent Landscape

CHAPTER 4: ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Polypropylene (PP)

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Polyurethane (PUR)

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Acrylonitrile Butadiene Styrene (ABS)

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Polyvinyl Chloride (PVC)

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

- 4.6. Polyoxymethylene (POM)

- 4.6.1. Key market trends, growth factors and opportunities

- 4.6.2. Market size and forecast, by region

- 4.6.3. Market share analysis by country

- 4.7. Polystyrene (PS)

- 4.7.1. Key market trends, growth factors and opportunities

- 4.7.2. Market size and forecast, by region

- 4.7.3. Market share analysis by country

- 4.8. Polycarbonate (PC)

- 4.8.1. Key market trends, growth factors and opportunities

- 4.8.2. Market size and forecast, by region

- 4.8.3. Market share analysis by country

- 4.9. Polyamide (PA)

- 4.9.1. Key market trends, growth factors and opportunities

- 4.9.2. Market size and forecast, by region

- 4.9.3. Market share analysis by country

- 4.10. Acrylic (PMMA)

- 4.10.1. Key market trends, growth factors and opportunities

- 4.10.2. Market size and forecast, by region

- 4.10.3. Market share analysis by country

- 4.11. Others (Polyethylene)

- 4.11.1. Key market trends, growth factors and opportunities

- 4.11.2. Market size and forecast, by region

- 4.11.3. Market share analysis by country

CHAPTER 5: ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Hybrid Electric Vehicles (HEVs)

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Plug-In Hybrid Electric Vehicles (PHEVs)

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Battery Electric Vehicles (BEVs)

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

CHAPTER 6: ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Interior furnishing

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Exterior furnishing

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Others

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: ELECTRIC VEHICLE PLASTIC MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key trends and opportunities

- 7.2.2. Market size and forecast, by Material

- 7.2.3. Market size and forecast, by Vehicle

- 7.2.4. Market size and forecast, by Application

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Key market trends, growth factors and opportunities

- 7.2.5.1.2. Market size and forecast, by Material

- 7.2.5.1.3. Market size and forecast, by Vehicle

- 7.2.5.1.4. Market size and forecast, by Application

- 7.2.5.2. Canada

- 7.2.5.2.1. Key market trends, growth factors and opportunities

- 7.2.5.2.2. Market size and forecast, by Material

- 7.2.5.2.3. Market size and forecast, by Vehicle

- 7.2.5.2.4. Market size and forecast, by Application

- 7.2.5.3. Mexico

- 7.2.5.3.1. Key market trends, growth factors and opportunities

- 7.2.5.3.2. Market size and forecast, by Material

- 7.2.5.3.3. Market size and forecast, by Vehicle

- 7.2.5.3.4. Market size and forecast, by Application

- 7.3. Europe

- 7.3.1. Key trends and opportunities

- 7.3.2. Market size and forecast, by Material

- 7.3.3. Market size and forecast, by Vehicle

- 7.3.4. Market size and forecast, by Application

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Key market trends, growth factors and opportunities

- 7.3.5.1.2. Market size and forecast, by Material

- 7.3.5.1.3. Market size and forecast, by Vehicle

- 7.3.5.1.4. Market size and forecast, by Application

- 7.3.5.2. UK

- 7.3.5.2.1. Key market trends, growth factors and opportunities

- 7.3.5.2.2. Market size and forecast, by Material

- 7.3.5.2.3. Market size and forecast, by Vehicle

- 7.3.5.2.4. Market size and forecast, by Application

- 7.3.5.3. France

- 7.3.5.3.1. Key market trends, growth factors and opportunities

- 7.3.5.3.2. Market size and forecast, by Material

- 7.3.5.3.3. Market size and forecast, by Vehicle

- 7.3.5.3.4. Market size and forecast, by Application

- 7.3.5.4. Spain

- 7.3.5.4.1. Key market trends, growth factors and opportunities

- 7.3.5.4.2. Market size and forecast, by Material

- 7.3.5.4.3. Market size and forecast, by Vehicle

- 7.3.5.4.4. Market size and forecast, by Application

- 7.3.5.5. Italy

- 7.3.5.5.1. Key market trends, growth factors and opportunities

- 7.3.5.5.2. Market size and forecast, by Material

- 7.3.5.5.3. Market size and forecast, by Vehicle

- 7.3.5.5.4. Market size and forecast, by Application

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Key market trends, growth factors and opportunities

- 7.3.5.6.2. Market size and forecast, by Material

- 7.3.5.6.3. Market size and forecast, by Vehicle

- 7.3.5.6.4. Market size and forecast, by Application

- 7.4. Asia-Pacific

- 7.4.1. Key trends and opportunities

- 7.4.2. Market size and forecast, by Material

- 7.4.3. Market size and forecast, by Vehicle

- 7.4.4. Market size and forecast, by Application

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. China

- 7.4.5.1.1. Key market trends, growth factors and opportunities

- 7.4.5.1.2. Market size and forecast, by Material

- 7.4.5.1.3. Market size and forecast, by Vehicle

- 7.4.5.1.4. Market size and forecast, by Application

- 7.4.5.2. Japan

- 7.4.5.2.1. Key market trends, growth factors and opportunities

- 7.4.5.2.2. Market size and forecast, by Material

- 7.4.5.2.3. Market size and forecast, by Vehicle

- 7.4.5.2.4. Market size and forecast, by Application

- 7.4.5.3. India

- 7.4.5.3.1. Key market trends, growth factors and opportunities

- 7.4.5.3.2. Market size and forecast, by Material

- 7.4.5.3.3. Market size and forecast, by Vehicle

- 7.4.5.3.4. Market size and forecast, by Application

- 7.4.5.4. South Korea

- 7.4.5.4.1. Key market trends, growth factors and opportunities

- 7.4.5.4.2. Market size and forecast, by Material

- 7.4.5.4.3. Market size and forecast, by Vehicle

- 7.4.5.4.4. Market size and forecast, by Application

- 7.4.5.5. Australia

- 7.4.5.5.1. Key market trends, growth factors and opportunities

- 7.4.5.5.2. Market size and forecast, by Material

- 7.4.5.5.3. Market size and forecast, by Vehicle

- 7.4.5.5.4. Market size and forecast, by Application

- 7.4.5.6. Rest of Asia-Pacific

- 7.4.5.6.1. Key market trends, growth factors and opportunities

- 7.4.5.6.2. Market size and forecast, by Material

- 7.4.5.6.3. Market size and forecast, by Vehicle

- 7.4.5.6.4. Market size and forecast, by Application

- 7.5. LAMEA

- 7.5.1. Key trends and opportunities

- 7.5.2. Market size and forecast, by Material

- 7.5.3. Market size and forecast, by Vehicle

- 7.5.4. Market size and forecast, by Application

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Key market trends, growth factors and opportunities

- 7.5.5.1.2. Market size and forecast, by Material

- 7.5.5.1.3. Market size and forecast, by Vehicle

- 7.5.5.1.4. Market size and forecast, by Application

- 7.5.5.2. South Arabia

- 7.5.5.2.1. Key market trends, growth factors and opportunities

- 7.5.5.2.2. Market size and forecast, by Material

- 7.5.5.2.3. Market size and forecast, by Vehicle

- 7.5.5.2.4. Market size and forecast, by Application

- 7.5.5.3. United Arab Emirates

- 7.5.5.3.1. Key market trends, growth factors and opportunities

- 7.5.5.3.2. Market size and forecast, by Material

- 7.5.5.3.3. Market size and forecast, by Vehicle

- 7.5.5.3.4. Market size and forecast, by Application

- 7.5.5.4. South Africa

- 7.5.5.4.1. Key market trends, growth factors and opportunities

- 7.5.5.4.2. Market size and forecast, by Material

- 7.5.5.4.3. Market size and forecast, by Vehicle

- 7.5.5.4.4. Market size and forecast, by Application

- 7.5.5.5. Rest of LAMEA

- 7.5.5.5.1. Key market trends, growth factors and opportunities

- 7.5.5.5.2. Market size and forecast, by Material

- 7.5.5.5.3. Market size and forecast, by Vehicle

- 7.5.5.5.4. Market size and forecast, by Application

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product Mapping of Top 10 Player

- 8.4. Competitive Dashboard

- 8.5. Competitive Heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. BASF SE

- 9.1.1. Company overview

- 9.1.2. Key Executives

- 9.1.3. Company snapshot

- 9.2. SABIC

- 9.2.1. Company overview

- 9.2.2. Key Executives

- 9.2.3. Company snapshot

- 9.3. LyondellBasell Industries Holdings B.V.

- 9.3.1. Company overview

- 9.3.2. Key Executives

- 9.3.3. Company snapshot

- 9.4. Evonik Industries

- 9.4.1. Company overview

- 9.4.2. Key Executives

- 9.4.3. Company snapshot

- 9.5. Covestro AG.

- 9.5.1. Company overview

- 9.5.2. Key Executives

- 9.5.3. Company snapshot

- 9.6. DUPONT

- 9.6.1. Company overview

- 9.6.2. Key Executives

- 9.6.3. Company snapshot

- 9.7. Sumitomo Chemicals Co. Ltd.

- 9.7.1. Company overview

- 9.7.2. Key Executives

- 9.7.3. Company snapshot

- 9.8. LG Chem Ltd

- 9.8.1. Company overview

- 9.8.2. Key Executives

- 9.8.3. Company snapshot

- 9.9. Asahi Kasei

- 9.9.1. Company overview

- 9.9.2. Key Executives

- 9.9.3. Company snapshot

- 9.10. LANXESS

- 9.10.1. Company overview

- 9.10.2. Key Executives

- 9.10.3. Company snapshot

LIST OF TABLES

- TABLE 01. GLOBAL ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 02. ELECTRIC VEHICLE PLASTIC MARKET FOR POLYPROPYLENE (PP), BY REGION, 2022-2032 ($MILLION)

- TABLE 03. ELECTRIC VEHICLE PLASTIC MARKET FOR POLYURETHANE (PUR), BY REGION, 2022-2032 ($MILLION)

- TABLE 04. ELECTRIC VEHICLE PLASTIC MARKET FOR ACRYLONITRILE BUTADIENE STYRENE (ABS), BY REGION, 2022-2032 ($MILLION)

- TABLE 05. ELECTRIC VEHICLE PLASTIC MARKET FOR POLYVINYL CHLORIDE (PVC), BY REGION, 2022-2032 ($MILLION)

- TABLE 06. ELECTRIC VEHICLE PLASTIC MARKET FOR POLYOXYMETHYLENE (POM), BY REGION, 2022-2032 ($MILLION)

- TABLE 07. ELECTRIC VEHICLE PLASTIC MARKET FOR POLYSTYRENE (PS), BY REGION, 2022-2032 ($MILLION)

- TABLE 08. ELECTRIC VEHICLE PLASTIC MARKET FOR POLYCARBONATE (PC), BY REGION, 2022-2032 ($MILLION)

- TABLE 09. ELECTRIC VEHICLE PLASTIC MARKET FOR POLYAMIDE (PA), BY REGION, 2022-2032 ($MILLION)

- TABLE 10. ELECTRIC VEHICLE PLASTIC MARKET FOR ACRYLIC (PMMA), BY REGION, 2022-2032 ($MILLION)

- TABLE 11. ELECTRIC VEHICLE PLASTIC MARKET FOR OTHERS (POLYETHYLENE), BY REGION, 2022-2032 ($MILLION)

- TABLE 12. GLOBAL ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 13. ELECTRIC VEHICLE PLASTIC MARKET FOR HYBRID ELECTRIC VEHICLES (HEVS), BY REGION, 2022-2032 ($MILLION)

- TABLE 14. ELECTRIC VEHICLE PLASTIC MARKET FOR PLUG-IN HYBRID ELECTRIC VEHICLES (PHEVS), BY REGION, 2022-2032 ($MILLION)

- TABLE 15. ELECTRIC VEHICLE PLASTIC MARKET FOR BATTERY ELECTRIC VEHICLES (BEVS), BY REGION, 2022-2032 ($MILLION)

- TABLE 16. GLOBAL ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 17. ELECTRIC VEHICLE PLASTIC MARKET FOR INTERIOR FURNISHING, BY REGION, 2022-2032 ($MILLION)

- TABLE 18. ELECTRIC VEHICLE PLASTIC MARKET FOR EXTERIOR FURNISHING, BY REGION, 2022-2032 ($MILLION)

- TABLE 19. ELECTRIC VEHICLE PLASTIC MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 20. ELECTRIC VEHICLE PLASTIC MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 21. NORTH AMERICA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 22. NORTH AMERICA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 23. NORTH AMERICA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 24. NORTH AMERICA ELECTRIC VEHICLE PLASTIC MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 25. U.S. ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 26. U.S. ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 27. U.S. ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 28. CANADA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 29. CANADA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 30. CANADA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 31. MEXICO ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 32. MEXICO ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 33. MEXICO ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 34. EUROPE ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 35. EUROPE ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 36. EUROPE ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 37. EUROPE ELECTRIC VEHICLE PLASTIC MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 38. GERMANY ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 39. GERMANY ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 40. GERMANY ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 41. UK ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 42. UK ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 43. UK ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 44. FRANCE ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 45. FRANCE ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 46. FRANCE ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 47. SPAIN ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 48. SPAIN ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 49. SPAIN ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 50. ITALY ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 51. ITALY ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 52. ITALY ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 53. REST OF EUROPE ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 54. REST OF EUROPE ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 55. REST OF EUROPE ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 56. ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 57. ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 58. ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 59. ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 60. CHINA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 61. CHINA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 62. CHINA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 63. JAPAN ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 64. JAPAN ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 65. JAPAN ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 66. INDIA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 67. INDIA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 68. INDIA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 69. SOUTH KOREA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 70. SOUTH KOREA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 71. SOUTH KOREA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 72. AUSTRALIA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 73. AUSTRALIA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 74. AUSTRALIA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 75. REST OF ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 76. REST OF ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 77. REST OF ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 78. LAMEA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 79. LAMEA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 80. LAMEA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 81. LAMEA ELECTRIC VEHICLE PLASTIC MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 82. BRAZIL ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 83. BRAZIL ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 84. BRAZIL ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 85. SOUTH ARABIA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 86. SOUTH ARABIA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 87. SOUTH ARABIA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 88. UNITED ARAB EMIRATES ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 89. UNITED ARAB EMIRATES ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 90. UNITED ARAB EMIRATES ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 91. SOUTH AFRICA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 92. SOUTH AFRICA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 93. SOUTH AFRICA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 94. REST OF LAMEA ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022-2032 ($MILLION)

- TABLE 95. REST OF LAMEA ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022-2032 ($MILLION)

- TABLE 96. REST OF LAMEA ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 97. BASF SE: KEY EXECUTIVES

- TABLE 98. BASF SE: COMPANY SNAPSHOT

- TABLE 99. SABIC: KEY EXECUTIVES

- TABLE 100. SABIC: COMPANY SNAPSHOT

- TABLE 101. LYONDELLBASELL INDUSTRIES HOLDINGS B.V.: KEY EXECUTIVES

- TABLE 102. LYONDELLBASELL INDUSTRIES HOLDINGS B.V.: COMPANY SNAPSHOT

- TABLE 103. EVONIK INDUSTRIES: KEY EXECUTIVES

- TABLE 104. EVONIK INDUSTRIES: COMPANY SNAPSHOT

- TABLE 105. COVESTRO AG.: KEY EXECUTIVES

- TABLE 106. COVESTRO AG.: COMPANY SNAPSHOT

- TABLE 107. DUPONT: KEY EXECUTIVES

- TABLE 108. DUPONT: COMPANY SNAPSHOT

- TABLE 109. SUMITOMO CHEMICALS CO. LTD.: KEY EXECUTIVES

- TABLE 110. SUMITOMO CHEMICALS CO. LTD.: COMPANY SNAPSHOT

- TABLE 111. LG CHEM LTD: KEY EXECUTIVES

- TABLE 112. LG CHEM LTD: COMPANY SNAPSHOT

- TABLE 113. ASAHI KASEI: KEY EXECUTIVES

- TABLE 114. ASAHI KASEI: COMPANY SNAPSHOT

- TABLE 115. LANXESS: KEY EXECUTIVES

- TABLE 116. LANXESS: COMPANY SNAPSHOT

LIST OF FIGURES

- FIGURE 01. ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF ELECTRIC VEHICLE PLASTIC MARKET,2022-2032

- FIGURE 03. TOP INVESTMENT POCKETS IN ELECTRIC VEHICLE PLASTIC MARKET (2023-2032)

- FIGURE 04. BARGAINING POWER OF SUPPLIERS

- FIGURE 05. BARGAINING POWER OF BUYERS

- FIGURE 06. THREAT OF SUBSTITUTION

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. COMPETITIVE RIVALRY

- FIGURE 09. GLOBAL ELECTRIC VEHICLE PLASTIC MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 10. REGULATORY GUIDELINES: ELECTRIC VEHICLE PLASTIC MARKET

- FIGURE 11. IMPACT OF KEY REGULATION: ELECTRIC VEHICLE PLASTIC MARKET

- FIGURE 12. PATENT ANALYSIS BY COMPANY

- FIGURE 13. PATENT ANALYSIS BY COUNTRY

- FIGURE 14. ELECTRIC VEHICLE PLASTIC MARKET, BY MATERIAL, 2022(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR POLYPROPYLENE (PP), BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR POLYURETHANE (PUR), BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR ACRYLONITRILE BUTADIENE STYRENE (ABS), BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR POLYVINYL CHLORIDE (PVC), BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR POLYOXYMETHYLENE (POM), BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR POLYSTYRENE (PS), BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR POLYCARBONATE (PC), BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR POLYAMIDE (PA), BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR ACRYLIC (PMMA), BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR OTHERS (POLYETHYLENE), BY COUNTRY 2022 AND 2032(%)

- FIGURE 25. ELECTRIC VEHICLE PLASTIC MARKET, BY VEHICLE, 2022(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR HYBRID ELECTRIC VEHICLES (HEVS), BY COUNTRY 2022 AND 2032(%)

- FIGURE 27. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR PLUG-IN HYBRID ELECTRIC VEHICLES (PHEVS), BY COUNTRY 2022 AND 2032(%)

- FIGURE 28. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR BATTERY ELECTRIC VEHICLES (BEVS), BY COUNTRY 2022 AND 2032(%)

- FIGURE 29. ELECTRIC VEHICLE PLASTIC MARKET, BY APPLICATION, 2022(%)

- FIGURE 30. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR INTERIOR FURNISHING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 31. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR EXTERIOR FURNISHING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 32. COMPARATIVE SHARE ANALYSIS OF ELECTRIC VEHICLE PLASTIC MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 33. ELECTRIC VEHICLE PLASTIC MARKET BY REGION, 2022(%)

- FIGURE 34. U.S. ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 35. CANADA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 36. MEXICO ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 37. GERMANY ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 38. UK ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 39. FRANCE ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 40. SPAIN ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 41. ITALY ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 42. REST OF EUROPE ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 43. CHINA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 44. JAPAN ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 45. INDIA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 46. SOUTH KOREA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 47. AUSTRALIA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 48. REST OF ASIA-PACIFIC ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 49. BRAZIL ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 50. SOUTH ARABIA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 51. UNITED ARAB EMIRATES ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 52. SOUTH AFRICA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 53. REST OF LAMEA ELECTRIC VEHICLE PLASTIC MARKET, 2022-2032 ($MILLION)

- FIGURE 54. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 55. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 56. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 57. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 58. COMPETITIVE DASHBOARD

- FIGURE 59. COMPETITIVE HEATMAP: ELECTRIC VEHICLE PLASTIC MARKET

- FIGURE 60. TOP PLAYER POSITIONING, 2022

電動車塑膠市場:依樹脂、成分、應用分類 - 2024-2030 年全球預測

電動車塑膠市場:依樹脂、成分、應用分類 - 2024-2030 年全球預測 電動車塑膠市場規模、佔有率、趨勢分析報告:按樹脂、按應用、按車輛類型、按部件、細分市場預測,2024-2030

電動車塑膠市場規模、佔有率、趨勢分析報告:按樹脂、按應用、按車輛類型、按部件、細分市場預測,2024-2030 全球電動汽車塑膠市場報告

全球電動汽車塑膠市場報告 全球電動汽車塑膠市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測

全球電動汽車塑膠市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測 電動車用塑膠的全球市場

電動車用塑膠的全球市場 電動車用塑膠的全球市場:2016-2032年

電動車用塑膠的全球市場:2016-2032年 電動車用塑膠的全球市場 (2023-2030年):規模·佔有率·預測 (樹脂·零組件·用途·車輛類型·各地區)·COVID-19影響分析

電動車用塑膠的全球市場 (2023-2030年):規模·佔有率·預測 (樹脂·零組件·用途·車輛類型·各地區)·COVID-19影響分析 全球電動汽車塑料市場:按類型、應用、組件、電池類型、材料、車輛類型和地區劃分的未來預測(到 2027 年)

全球電動汽車塑料市場:按類型、應用、組件、電池類型、材料、車輛類型和地區劃分的未來預測(到 2027 年) 電動車用塑膠的全球市場的預測:2022年~2030年

電動車用塑膠的全球市場的預測:2022年~2030年