|

市場調查報告書

商品編碼

1438548

噴墨印刷:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Inkjet Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

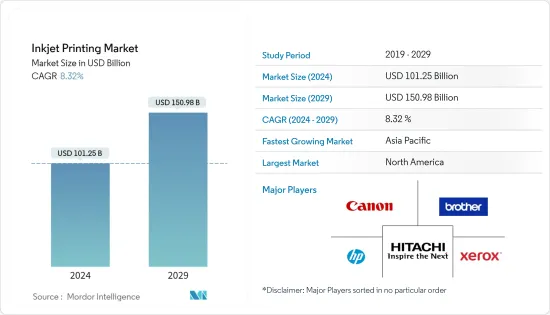

噴墨印刷市場規模預估2024年為1,012.5億美元,預估至2029年將達1,509.8億美元,在預測期間內(2024-2029年)年複合成長率為8.32%成長。

主要亮點

- 噴墨印刷涉及將微小的液體墨水液滴噴射到指定的表面(例如紙張)上,並幫助開發了數位印刷。這種方法產生的影像可與照片品質相媲美。噴墨列印是其他列印製程的一種經濟高效的替代方案,因為它具有完整的多功能性、較低的設定成本,並且允許小批量列印一份。

- 使用噴墨的主要優點是能夠有效地小批量生產獨特的產品。透過網路印刷技術進行的線上訂購和規格的興起正在推動商業印刷的發展。噴墨印表機的小批量和一次性生產能力鞏固了其作為此生態系統中關鍵推動者的地位。此外,智慧生產、速度、彈性和成本控制也將推動噴墨印刷的採用,推動噴墨印刷市場的成長,因為數位印刷的採用將使企業能夠更靈活地回應客戶的要求。儘管改用噴墨印表機具有潛在的好處,但也存在局限性,例如長期印刷的印刷成本較高,尤其是與模擬印刷相比。

- 隨著噴墨印刷產業創造對墨水的需求,墨水生態系統也有望發展。目前廣泛使用的是溶劑型、水性、UV型油墨。另一方面,LED墨水也在不斷發展。混合紫外線/水系統正在市場上興起。然而,墨水的高成本仍然是一個主要問題,導致供應商從類比到數位的轉換率較低。由於應用的增加和規模經濟,在預測期內墨水價格可能會下降。另一方面,與類似產品相比,墨水成本預計仍然較高。

- 近年來,數位廣告媒體越來越受歡迎,對印刷業的成長提出了挑戰。媒體播放機是數位廣告的關鍵組成部分,並且在技術、連接性和易用性方面正在經歷快速變化。例如,美國數位廣告媒體播放機供應商BrightSign LLC於2021年5月推出了BrightSign Mobile,這是將媒體播放機連接到雲端的新解決方案,這是傳統網路連線方式難以實現的。該解決方案包括一個 USB 區域數據機,並安裝了用於連接的 SIM 卡。這些發展和創新進一步限制了市場的成長。

- 由於食品和藥品包裝需求增加,包裝、標籤和印刷業在 COVID-19 期間保持相當穩定。然而,冠狀病毒感染疾病(COVID-19) 的爆發擾亂了食品和飲料、醫療保健和工業等各個最終用戶行業的供應鏈。雖然這場流行病對經濟產生了重大影響,但噴墨印刷公司正在透過使用網路印刷技術向符合條件的企業提供與冠狀病毒相關的印刷廣告來幫助滿足要求。這些資訊將用於傳達與 COVID-19感染疾病相關的所有企業客戶問題。

噴墨列印市場趨勢

廣告預計將佔據壓倒性的市場佔有率

- 廣告包括銷售點 (POS) 和展示,被認為是成長最快的領域之一。軟指示牌是一個常見的行業術語,用於描述數位印刷的布指示牌。軟標誌僅限於特定的油墨組,但通常印刷在聚酯基織物上,有時印刷在棉或棉混紡等天然纖維上。

- 橫幅因其多功能性和可用於多種應用程式的能力而在廣告媒體中佔據巨大佔有率。市場上有許多不同類型的材料,包括織物橫幅、乙烯基橫幅和網膜橫幅。

- 隨著對印花紡織品的需求和所需尺寸的不斷增加,數位印刷機供應商開始推出可處理3米寬或以上材料的數位紡織品印表機。雖然該領域歷來以傳統印刷方法為主,但 EFI、d.gen、Durst 和 Mimaki 等公司正透過大幅面數位紡織品印表機進入該領域。

- 數位化是印刷業的重大變革,其中包括與數位印刷能力的成長並進的產品個人化、創新和溝通。消費者希望產品具有互動性,並包含他們想了解的有關產品的所有資訊。這些設備配備了技術功能,例如帶有社交媒體連結的2D碼、虛擬實境等。

- 在注射印刷中實施物聯網將進一步減少物理干涉並提高自動化程度。定期監控和記錄設備的實際運作狀態和系統效能有助於分析預期的停機時間。隨著時間的推移,對這些資料進行分析,使公司能夠預測機器故障並識別需要更換的零件,以避免代價高昂的意外停機。

預計亞太地區在預測期內成長最快

- 在中國、印度和許多快速成長國家的推動下,亞太地區已成為全球最大的印刷油墨地區。另一方面,許多最大的跨國油墨製造商都位於該地區。 DIC、SAKATA INX CORPORATION、東洋油墨和 T&K TOKA 總部位於日本,其餘主要公司也在該地區擁有大規模業務。

- 此外,許多歐洲印刷公司依賴中國供應新化學品,例如油墨和溶劑成分,這些都是印刷程序中所需的投入。除此之外,智慧型手機公司增加對製造這些印表機的投資是推動該國銷售的關鍵因素。

- 就新冠肺炎 (COVID-19) 而言,亞太地區(尤其是印度)的冠狀病毒感染疾病數量史無前例地增加,導致工業噴墨印表機製造活動暫停。

- 然而,Etiquettes Pierre Foucher 和商業膠印公司 Imprimerie Coste &Films 推出了採用噴墨技術的基於碳粉的 AccurioLABel 230 印表機,以滿足客戶對短交付時間和周轉時間的需求。 Accurio 的新設計型號提供 76 英尺/分鐘的最大列印速度、縮短的預熱時間以及可選的套印套件。

- 亞太地區也主導著自訂服裝印花市場,例如自訂T 卹印花。預計該地區在未來幾年也將出現顯著的成長。因此,大尺寸噴墨印表機的需求預計將持續增加。

噴墨印刷業概況

根據行業分析,噴墨列印供應商之間存在著激烈的競爭。由於有大量參與者,市場高度分散。市場滲透率正在不斷提高,大型企業在成熟市場中擁有強大的影響力。鑑於市場產品的同質化,許多在市場上經營的企業進一步被迫進行價格競爭。公司採取許多成長和擴大策略來獲得競爭優勢。企業參與企業也遵循價值鏈價值鏈聯盟。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

- 產業價值鏈分析

- 評估新型冠狀病毒感染疾病(COVID-19)對市場的影響

第5章市場動態

- 市場促進因素

- 巨量資料、物聯網、印刷包裝數位化

- 智慧生產、速度、彈性和成本控制

- 市場挑戰

- 數位廣告媒體日益普及

- 高價以及投資和技術的限制

- 彈性凸版印刷和絲網印刷等成熟技術之間的激烈競爭

- 市場機會

- 向永續性的過渡可以推動市場成長

第6章市場區隔

- 按用途

- 書籍/出版

- 商業印刷

- 廣告

- 交易

- 標籤

- 包裝

- 其他用途

- 按地區

- 北美洲

- 歐洲

- 東歐洲

- 西歐

- 亞太地區

- 亞洲

- 澳洲

- 拉丁美洲

- 中東和非洲

第7章 競爭形勢

- 公司簡介

- HP Development Company LP

- Jet Inks Private Limited

- Brother Industries Ltd

- Xerox Corporation

- Canon Inc.

- Hitachi Industrial Equipment Systems Co. Ltd

- Lexmark International Inc.

- Videojet Technologies Inc.

- Inkjet Inc.

- Fujifilm Holdings Corporation

第8章投資分析

第9章市場的未來

The Inkjet Printing Market size is estimated at USD 101.25 billion in 2024, and is expected to reach USD 150.98 billion by 2029, growing at a CAGR of 8.32% during the forecast period (2024-2029).

Key Highlights

- Inkjet printing involves spraying tiny droplets of liquid ink onto designated surfaces, such as paper, which aided the development of digital printing. This method produces images that are photo-quality equivalents. Inkjet printing is a cost-effective alternative to other print processes since it offers full versatility and inexpensive set-up costs, allowing for low-volume printing of single copies.

- The major advantage of using inkjets is due to its capability to produce short runs and unique products effectively. The rise of online ordering and specification via web-to-print technology is propelling commercial printing forward. Inkjet printers' capacity to produce small runs and one-off products solidified their position as a key enabler in such an ecosystem. Moreover, smart production, speed, flexibility, and cost control also drive the adoption of inkjet printing as the businesses can become more flexible and responsive to customer requirements through the adoption of digital print, thus fueling the growth of the Inkjet Printing Market. While switching to inkjet brings potential advantages, there are also restrictions - such as the higher cost of printing when it comes to long runs, particularly when compared to analog printing.

- Since the inkjet printing industry creates demand for inks, the ecosystem of inks is expected to evolve too. Currently, solvent, water-based, and UV-based inks are widely used. LED inks, on the other hand, are constantly evolving. Hybrid UV/water systems are making their way onto the market. High ink costs, on the other hand, remain a major problem, resulting in lower vendor conversion rates, from analog to digital. During the projection period, rising applications and economies of scale are likely to lower ink prices. Ink costs, on the other hand, are projected to remain higher than in analog.

- Digital advertising media has been gaining popularity lately, challenging the growth of the printing industry. The media player is the crucial component for digital advertising, experiencing a rapid transformation in technology, network connectivity, and ease of use. For instance, in May 2021, BrightSign LLC, a US provider of digital advertising media players, launched BrightSign Mobile, a new solution to connect media players to the cloud where traditional network connectivity methods are challenging to achieve. This solution includes a USB regional modem with an installed SIM card for connectivity. These developments and innovations further suppressed the market's growth.

- The packaging, labeling, and printing segments are considerably stable in the COVID-19 period, owing to the increasing demand for food and pharmaceutical packaging. However, the COVID-19 outbreak disrupted the supply chain across various end-user industries like food and beverage, healthcare, and industrial. Even though the pandemic had a massive impact on the economy, inkjet printing companies are supplying this requirement by offering those in requirement COVID-19-related printed advertisements with web-to-print technology. These are used for communicating all business-customer matters concerning the COVID-19 pandemic.

Inkjet Printing Market Trends

Advertisement is Anticipated to Hold a Dominant Share of the Market

- Advertising constitutes the point of sales (POS) and displays and is considered one of the fastest-growing segments. Soft signage is a common industry term that is used to describe digitally printed fabric signage. Although soft signs are limited to a particular ink set, they are typically printed on a polyester-based textile and, on occasion, natural fiber such as cotton or a cotton blend.

- Banners hold a significantly large share in advertising media due to their versatility and use across several applications. Various types of materials are available in the market, including fabric banners, vinyl banners, and mesh banners.

- As the demand for printed textiles and requested size continues to increase, digital press vendors are beginning to introduce digital textile printers that are capable of handling substrates up to and beyond 3 meters wide. Although this area has historically been dominated by traditional printing methods, companies like EFI, d.gen, Durst, and Mimaki are entering with grand format digital textile printers.

- Digitization has been a major game-changer in the printing industry, which includes product personalization, innovation, and communication that aligns closely with the growing capabilities of digital printing. As consumers want the products to be interactive and contain everything there is to know about them. The devices are equipped with technology features, such as QR codes with links to social media, virtual reality, etc.

- The implementation of IoT in inject printing further reduces physical intervention and increases automation. It helps to analyze the probable downtime by regularly monitoring and recording the actual operating conditions of the equipment and its system performance. This data is analyzed over a period of time, allowing companies to predict machine failure and identify parts that need replacement, avoiding costly unexpected downtime.

Asia-Pacific is Expected to Register the Fastest Growth During the Forecast Period

- Driven by China, India, and a host of fast-growing countries, the Asia-Pacific region has become the world's largest region for printing ink. On the other hand, The region is home to many of the largest multinational ink manufacturers. DIC, Sakata INX, Toyo Ink, and T&K Toka call Japan home, and the rest of the major leaders have large operations in the region.

- Also, numerous printing companies based in Europe are dependent on China for the supply of novel chemicals, such as constituents of inks and solvents, which are required in printing procedures as input materials. On top of that, increasing investment by smartphone companies in the manufacturing of these printers is a significant factor pushing sales in the country.

- In the case of COVID-19, the Asia-Pacific, especially India, witnessed an unprecedented rise in the number of coronavirus cases, which led to the discontinuation of industrial inkjet printer manufacturing activities.

- However, Etiquettes Pierre Foucher and commercial offset printer Imprimerie Coste & Films shifted from inkjet technology to install toner-based AccurioLAbel 230 printers to meet the demand for shorter runs and quick turnaround times from their customers. The new design model of Accurio offers a maximum print speed of 76ft/min, shorter warm-up times, and an optional over-print kit.

- The Asia-Pacific region also dominates the custom apparel printing market, which includes custom t-shirt printing. Also, the region is expected to witness a significant growth rate over the coming years. Therefore, the demand for large format inkjet printers is expected to increase.

Inkjet Printing Industry Overview

Based on industry analysis, intense rivalry exists within the inkjet printing providers. The market is highly fragmented due to the presence of a large number of players. Market penetration is growing, with a strong presence of major players in established markets. Considering the homogenous nature of market products, many firms operating in the market are further driven to compete on price. The companies are involved in many growth and expansion strategies to get a competitive advantage. Business participants also follow the value chain alliance with business transactions in various steps of the value chain.

- February 2022 - Canon announced the expansion of its MAXIFY Ink Efficient GX Series lineup with a new ink tank business printer. The printer combines low color printing costs with speed, paper handling, and networking capabilities to give offices and businesses a boost in efficiency and productivity.

- October 2021 - Roland DG Corporation, a manufacturer of wide-format inkjet printers and printer/cutters, announced the launch of D-BRIDGE, a support website that provides a variety of helpful information about the benefits of digitalization and secrets of success for anyone engaged in creating, especially those involved in printing or manufacturing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Big Data, IoT, and Digitalization of Print Processing and Packaging

- 5.1.2 Smart Production, Speed, Flexibility, and Cost Control

- 5.2 Market Challenges

- 5.2.1 Growing Popularity of Digital Advertising Media

- 5.2.2 High Price and Investment and Technological Limitations

- 5.2.3 Cut-Throat Competition among Established Technologies, such as Flexographic Printing and Screen Printing

- 5.3 Market Opportunities

- 5.3.1 Shift Toward Sustainability can Increase the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Books/Publishing

- 6.1.2 Commercial Print

- 6.1.3 Advertising

- 6.1.4 Transaction

- 6.1.5 Labels

- 6.1.6 Packaging

- 6.1.7 Other Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.2.1 Eastern Europe

- 6.2.2.2 Western Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 Asia

- 6.2.3.2 Australia

- 6.2.4 Latin America

- 6.2.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 HP Development Company LP

- 7.1.2 Jet Inks Private Limited

- 7.1.3 Brother Industries Ltd

- 7.1.4 Xerox Corporation

- 7.1.5 Canon Inc.

- 7.1.6 Hitachi Industrial Equipment Systems Co. Ltd

- 7.1.7 Lexmark International Inc.

- 7.1.8 Videojet Technologies Inc.

- 7.1.9 Inkjet Inc.

- 7.1.10 Fujifilm Holdings Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球噴墨打碼機市場規模、佔有率、成長分析、依產品(連續噴墨打碼機、依需噴墨打碼機)、最終用戶、墨水 - 產業預測 2024-2031

全球噴墨打碼機市場規模、佔有率、成長分析、依產品(連續噴墨打碼機、依需噴墨打碼機)、最終用戶、墨水 - 產業預測 2024-2031 連續噴印 (CIJ) 機市場報告:2030 年趨勢、預測與競爭分析

連續噴印 (CIJ) 機市場報告:2030 年趨勢、預測與競爭分析 全球熱噴墨墨水市場 - 2023-2030

全球熱噴墨墨水市場 - 2023-2030 噴墨打碼機市場:按類型和應用分類 - 2023 年至 2030 年全球預測

噴墨打碼機市場:按類型和應用分類 - 2023 年至 2030 年全球預測 全球噴墨打碼機市場規模研究與預測,按類型、按應用和區域分析,2023-2030年

全球噴墨打碼機市場規模研究與預測,按類型、按應用和區域分析,2023-2030年 數位生產噴墨印刷市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、生產方法和應用

數位生產噴墨印刷市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按類型、生產方法和應用 噴墨打碼機的全球市場

噴墨打碼機的全球市場 噴墨印刷技術:各種用途、亞太地區市場

噴墨印刷技術:各種用途、亞太地區市場 噴墨打碼機市場:按類型、最終用戶劃分:2023-2032 年全球機會分析與產業預測

噴墨打碼機市場:按類型、最終用戶劃分:2023-2032 年全球機會分析與產業預測 MEMS噴墨印表機頭的全球市場的考察,預測(~2029年)

MEMS噴墨印表機頭的全球市場的考察,預測(~2029年)