|

市場調查報告書

商品編碼

1437480

工業固定設備:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Industrial Static Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

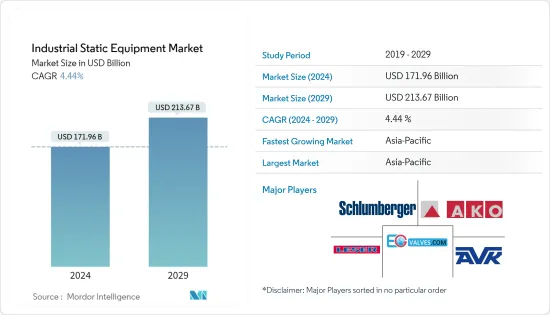

2024年工業固定設備市場規模估計為1719.6億美元,預計到2029年將達到2136.7億美元,在預測期間(2024-2029年)以4.44%的複合年增長率增長。

世界原油和其他碳氫化合物生產的顯著進步促使石油和天然氣探勘和精製的增加。隨著汽車、醫藥、通訊、製造等各行各業的革命,大規模工業化、都市化,石油已成為發展的重要因素。

主要亮點

- 本研究提供的市場數據代表了閥門、熔爐/鍋爐、熱交換器、壓力容器等類型的靜態工業設備的總體銷售。其他市場是最終用戶產業,代表多個產業中多種類型靜態工業設備的銷售,例如石油和天然氣、發電、化學和石化、水和廢水處理、其他製程工業以及其他離散製造業。也分為。行業。

- 食品飲料產業也是靜態設備需求預計進一步成長的重點產業之一。食品加工和食品消費量的增加是該行業成長的主要貢獻者之一。根據美國人口普查局的數據,2022年5月至2022年7月零售和食品服務總銷售額年增9.2%。

- 石油和天然氣產業對幾乎所有產業的成長做出了重大貢獻。這是因為任何工業設施的運作都需要電力,而在最近可再生資源的開發之前,電力主要由石油和天然氣提供。

- 石油和天然氣行業是鍋爐、熔爐、管道和閥門等靜態工業設備的主要消費者之一,因為整個石油探勘和生產活動涉及在不同地點進行的多個流程。

- 冠狀病毒感染疾病(COVID-19)的爆發對工業部門的成長產生了重大影響,進而影響了所研究市場的成長。根據歐盟統計局的數據,2020年歐盟工業生產下降了7%。生產活動的下降對關鍵工業固定設備的需求產生了負面影響,因為關鍵產業克制了進一步的擴張活動和對新設施的投資。

工業固定設備市場趨勢

快速工業化推動市場成長

- 自工業革命開始以來,工業部門一直是世界經濟繁榮的引擎。根據世界銀行預計,2021年製造業對全球經濟付加價值約為17.01%。工業部門預計將在增加工業產品需求方面發揮作用,並透過其產出刺激其他產業的成長。它將在預測期內推動工業部門的發展。

- 鍋爐、閥門、熱交換器、熔爐等靜態工業設備對於幫助實現工業設施內的營運目標發揮著至關重要的作用,因此這些設備也與工業設施有直接的聯繫。考慮到兩者之間的相關性,預期它們將遵循類似的成長模式。

- 工業部門一直是美國、中國、日本等主要經濟已開發國家的支柱。例如,根據聯合國統計司(UNSD)提供的資料,美國、日本、德國的付加分別為22720億美元、10336億美元和6973億美元。隨著這些國家為加強工業部門而增加投資和建立配套法規,預計在預測期內對靜態工業設備的需求也將進一步增加。

- 此外,亞太地區是工業領域的主要參與者,有利的政府法規、大量人口和低成本勞動力吸引了全球公司落腳該地區,預計將成為成長領頭羊。中國、台灣和印度等國家是跨國公司最喜歡的目的地之一。例如,根據產業內貿易促進部(DPIIT)的數據,2021-22會計年度印度收到的外國直接投資(FDI)總額為587.7億美元,其中汽車行業收到了相當數量的FDI .. 32.84,化學製造業完成194.5億美元。醫藥業實際吸收外資194.1億美元。

- 其他國家也觀察到類似的趨勢。例如,2022年9月,馬來西亞投資發展局(MIDA)宣布,2022年上半年政府在製造業、服務業和一級產業吸引了價值275億美元的投資核准。

亞太地區預計將成為成長最快的市場

- 預計,由於投資增加、政府採取更強力的措施加強基礎設施和促進液化天然氣探勘,以及在該地區包括中國和印度在內的成長中國家開展業務的重要公司的存在,亞太市場預計將快速發展。例如,2021 年 1 月,古爾岡大都會發展局 (GMDA) 在 Vasai 和 Dhanwapur 周圍的約 10 個地點啟動了水資源管理技術試點計劃。該計劃的目標是監測、控制和調節城市地下水箱的流量。地下儲槽將配備流量控制閥、超音波流體流量計和位准計。

- 中國在石油和天然氣探勘方面的支出使其成為亞太地區石油和天然氣生產的先驅。印度的石油鑽井平台數量最多,其次是印度,該國也在穩步改善。此外,許多研究機構正在多個國家進行研發工作,以提高設備性能並鼓勵對該行業的投資。例如,中國計劃在2022年3月投資815億元用於上游開發,特別是順北地區和大河地區的原油基地以及四川和內蒙古地區的天然氣資源。石油和天然氣探勘需求的增加將增加對靜態設備的需求,推動市場成長。

- 亞太地區是一些世界領先的止回閥製造商的所在地。對更安全應用的需求不斷增加,以及與自動閥門相關的研發力度不斷加大,是推動亞太地區工業發展的一些關鍵因素。此外,工業研究,特別是在中國,擴大了閥門在能源電力、化學等許多領域的應用範圍。止回閥應用於能源電力、石油天然氣、水和廢水處理等領域,調節整個網路中的介質流量,以啟動、停止或控制運動,以實現安全有效的製程自動化。

- 該地區人口集中、消費者收入高、工業規模大、都市化程度不斷提高,是該地區工業閥門擴張的重要驅動力。印度、中國和東南亞國家是該地區成長最快的經濟體。該地區不斷成長的大都會人口迫切需要現代化和強化的污水處理設施。

- 加強水和污水管理技術的需求不斷增加、政府對污水處理的措施不斷增加,以及對適當用水的需求不斷成長,正在推動亞太地區對靜態設備的需求。

工業固定設備產業概況

工業固定設備市場處於適度高位,預計在預測期內保持不變。斯倫貝謝有限公司、AKO Armaturen&Separationstechchink GMBH、AVK Group、EG Valves LeserGMBH &CO. KG 等領先公司也正在建立合作夥伴關係並推出新產品,以維持其市場地位。

- 2022 年 7 月 - 阿法拉伐與瑞典全球鋼鐵公司 SSAB 合作開發和商業化世界上第一個由無化石鋼製成的熱交換器。目標是到 2023 年建造第一座氫還原鋼裝置。此次合作也是阿法拉伐實現 2030 年碳中和目標的重要一步。

- 2022 年 3 月 - AVK 集團推出新系列優質 100 閘閥。 Premium 100 閘閥耐腐蝕、耐磨。非常適合無法進行挖掘或需要長使用壽命和最大安全性的安裝。這可能包括繁忙的道路、公共建築和旅遊景點、沿海地區以及受到石油或汽油污染的地區。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 科技趨勢

- 產業價值鏈分析

- COVID-19 對市場的影響

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場動態

- 市場促進因素

- 快速工業化

- 石油和天然氣探勘活動增加

- 市場限制因素

- 高投資成本和向可再生能源發電過渡

第6章市場區隔

- 依類型

- 閥門

- 門,手套,檢查

- 球閥

- 蝴蝶

- 插頭

- 消除壓力裝置

- 熔爐/鍋爐

- 熱交換器

- 壓力容器

- 閥門

- 依最終用戶產業

- 油和氣

- 發電

- 化學品和石化產品

- 水和污水

- 其他流程工業

- 其他離散製造業

- 依地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭形勢

- 公司簡介 - 閥門

- Schlumberger Limited

- AKO Armaturen &Separationstecchink GMBH

- AVK Group

- EG Valves

- Leser GMBH &CO. KG

- Baker Hughes Company

- Emerson Electric CO.

- Flowserve Corporation

- 公司簡介 - 熱交換器

- Alfa Laval AB

- API Heat Transfer

- Danfoss A/S

- General Electric Company

- Hisaka Works Ltd

- HRS Heat Exchangers

- Johnson Controls International PLC

- 公司簡介-壓力容器

- Doosan Mecatec(Doosan Corporation)

- IHI Power Services Corp.(IHI Corporation)

- Mitsubishi Heavy Industries Ltd

- Hitachi Zosen Corporation

- Japan Steel Works Ltd

- Shanghai Electric Group Company Limited

- CIMC Enric Holdings Limited

- 公司簡介-熔爐/鍋爐

- Viessmann Group

- Lennox International Inc.

- Baxi(BDR Thermea Group)

- The Fulton Companies

- Worcester Bosch Group(the Bosch Group)

- Ideal Boilers(ideal Heating)

- Burnham Commercial Boilers

第8章 市場未來展望

The Industrial Static Equipment Market size is estimated at USD 171.96 billion in 2024, and is expected to reach USD 213.67 billion by 2029, growing at a CAGR of 4.44% during the forecast period (2024-2029).

The exploration and refining of oil and gas have increased due to the remarkable progress made in the worldwide production of crude oil and other hydrocarbons. With the massive industrialization and urbanization that has resulted from the revolution in a variety of industries, including the automobile, pharmaceutical, telecommunication, and manufacturing, petroleum is now a crucial component of development.

Key Highlights

- The market numbers provided in the study indicate the overall sales of static industrial equipment across types, such as valves, furnaces/boilers, heat exchangers, and pressure vessels. The further market is also segmented into an end-user industry which indicates the sales of several types of static industrial equipment across several industries such as oil and gas, Power generation, Chemical & petrochemical, Water & Wastewater, Other Process industries, and other discrete industries.

- The food and beverage industry is also among the major industries wherein the demand for static equipment is expected to grow further. The increasing consumption of processed and packaged foods globally is one of the major contributors to the growth of the industry. According to the US Census Bureau, total sales for retail and food services from May 2022 through July 2022 were up by 9.2% from the same period last year.

- The oil and gas industry has been among the key contributors to the growth of almost all industries. This was due to the fact that power is required to run any industrial establishment, and until the recent developments in renewable sources, power was used to be fulfilled primarily by oil and gas.

- The oil and gas industry is among the major consumers of static industrial equipment, such as boilers, furnaces, piping, and valves, as the entire oil exploration and production activity involves several processes that are carried out at different places.

- The outbreak of COVID-19 has had a notable impact on the growth of the industrial sector, which in turn impacted the growth of the studied market. According to Eurostat, industrial production in the European Union declined by 7% in 2020. The decline in production activities has had an adverse impact on the demand for major industrial static equipment as major industries put a hold on future expansion activities and investment in establishing new facilities.

Industrial Static Equipment Market Trends

Rapid Industrialization Drives the Market Growth

- The industrial sector has been an engine for the world's economic prosperity since the onset of the industrial revolution. According to the World Bank, the estimated value added by the manufacturing sector to the global economy was around 17.01% in 2021. The growing demand for manufactured products and the role the industrial sector plays in stimulating the growth of other sectors through its outputs are expected to drive the development of the industrial sector during the forecast period.

- As static industrial equipment such as boilers, valves, heat exchangers, furnaces, etc. plays a pivotal role within the industrial establishments to help them achieve their operational targets, they are also expected to follow a similar growth pattern considering their direct co-relation with the industrial sector growth.

- The industrial sector has been the backbone of major economically developed countries such as the United States, China, Japan, etc. For instance, according to the data provided by the United Nations Statistics Division (UNSD), the value added by the manufacturing industry to the GDP of the United States, Japan, and Germany amounted to USD 2,272 billion, USD 1.033.6 billion, and USD 697.3 billion, respectively. As these countries are increasingly investing and framing supportive regulations to bolster the industrial sector, the demand for static industrial equipment is also expected to grow further during the forecast period.

- Additionally, the Asia-Pacific region is expected to be the leader in industrial sector growth, as the favorable government regulations, large populations, and the availability of low-cost labor attract global players to set up their base in the region. Countries like China, Taiwan, India, etc., have been among the favorite destinations of global companies. For instance, According to the Department for Promotion of Industry and Internal Trade (DPIIT), the total foreign direct investment (FDI) received by India in the financial years 2021-22 stood at USD 58.77 billion, of which the automotive industry received FDI worth USD 32.84, chemical manufacturing sector received USD 19.45 billion. The FDI received by the drug and pharmaceutical industry amounted to USD 19.41 billion.

- A similar trend has been observed across other countries as well. For instance, in September 2022, The Malaysian Investment Development Authority (MIDA) announced that the government has attracted approved investment worth USD 27.5 billion in its manufacturing, services, and primary sectors in the first half of 2022.

Asia Pacific is Expected to be the Fastest Growing Market

- The Asia Pacific market is predicted to develop rapidly due to increased investment, increased government measures to enhance infrastructures and promote LNG exploration, and the existence of important firms operating in growing countries, including China and India, in this area. For instance, in January 2021, the Gurugram Metropolitan Development Authority (GMDA) began a trial project for its water management technology in around ten places around Basai and Dhanwapur. The project's goal is to monitor, control, and regulate the flow of the city's underground water tanks. In the subterranean tanks, a flow control valve, an ultrasonic fluid flow meter, and a level meter will be installed as part of the project.

- China is the pioneer in oil & gas production in Asia-Pacific because of its oil & gas exploration expenditure. The nation has the most oil rigs, followed by India, which has also made steady improvements. Furthermore, numerous institutes are conducting research and development initiatives in several nations to increase equipment performance and encourage investment in the industry. For instance, in March 2022, China intends to invest CNY 81.5 billion in upstream exploitation, particularly in the crude oil foundations in the Shunbei and Tahe areas and natural gas resources in Sichuan province and the Interior Mongolia region. Increasing demand for oil & gas exploration will increase the demand for static equipment, boosting the market growth.

- The Asia Pacific area is home to several of the world's major check valve manufacturers. Increasing demand for safer applications and increased R&D efforts linked to automatic valves are some significant factors fueling industry development in the Asia Pacific. Furthermore, industrial research has widened the applicability of valves in many sectors, including energy & power, and chemicals, notably in China. Check valves are employed in the energy & power, oil & gas, and water & wastewater treatment sectors to regulate medium flow throughout the network, commence, stop, or control the movement, and provide secure and effective processing automation.

- The region's concentrated populace, significant consumer income, large-scale industry, and increasing urbanization are important drivers driving the region's industrial valve expansion. India, China, and Southeast Asian countries are among the region's fast-growing economies. Because of the region's growing metropolitan population, there is a strong need for modern and enhanced wastewater treatment facilities.

- The increasing demand for enhanced water and wastewater management techniques, rising government initiatives for treating wastewater, and the growing necessity for appropriate water usage are driving the need for static equipment in the Asia-Pacific region.

Industrial Static Equipment Industry Overview

Industrial Static Equipment Market is expected to be moderately high and remains the same over the forecast period. Major companies like Schlumberger Limited, AKO Armaturen& Separationstecchink GMBH, AVK Group, EG Valves LeserGMBH & CO. KG are also making partnerships and launching new products to retain their market position.

- July 2022 - Alfa Laval collaborated with SSAB, the global Swedish steel company, on developing and commercializing the world's first heat exchanger made of fossil-free steel. The goal is to have the first hydrogen-reduced steel unit ready by 2023. The collaboration is also a significant step toward Alfa Laval's goal of becoming carbon neutral by 2030.

- March 2022 - AVK Group launched a new line of premium 100 gate valves. Premium 100 gate valves offer corrosion and wear resistance. They are ideal for installation in locations where excavation is not feasible and where long life and maximum safety are required. This could include busy roads, public and tourist attractions, coastal areas, or areas contaminated with oil or gasoline.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on The Market

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Industrialization

- 5.1.2 Increasing Oil and Gas Exploration Activities

- 5.2 Market Restraints

- 5.2.1 High Investment Cost and Shift Toward Renewable Energy Generation Sources

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Valves

- 6.1.1.1 Gate, Globe, and Check

- 6.1.1.2 Ball Valves

- 6.1.1.3 Butterfly

- 6.1.1.4 Plug

- 6.1.1.5 Pressure Relief

- 6.1.2 Furnaces/Boilers

- 6.1.3 Heat Exchangers

- 6.1.4 Pressure Vessels

- 6.1.1 Valves

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Power Generation

- 6.2.3 Chemicals and Petrochemicals

- 6.2.4 Water and Wastewater

- 6.2.5 Other Process Industries

- 6.2.6 Other Discrete Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles - Valves

- 7.1.1 Schlumberger Limited

- 7.1.2 AKO Armaturen & Separationstecchink GMBH

- 7.1.3 AVK Group

- 7.1.4 EG Valves

- 7.1.5 Leser GMBH & CO. KG

- 7.1.6 Baker Hughes Company

- 7.1.7 Emerson Electric CO.

- 7.1.8 Flowserve Corporation

- 7.2 Company Profiles - Heat Exchangers

- 7.2.1 Alfa Laval AB

- 7.2.2 API Heat Transfer

- 7.2.3 Danfoss A/S

- 7.2.4 General Electric Company

- 7.2.5 Hisaka Works Ltd

- 7.2.6 HRS Heat Exchangers

- 7.2.7 Johnson Controls International PLC

- 7.3 Company Profiles - Pressure Vessels

- 7.3.1 Doosan Mecatec (Doosan Corporation)

- 7.3.2 IHI Power Services Corp. (IHI Corporation)

- 7.3.3 Mitsubishi Heavy Industries Ltd

- 7.3.4 Hitachi Zosen Corporation

- 7.3.5 Japan Steel Works Ltd

- 7.3.6 Shanghai Electric Group Company Limited

- 7.3.7 CIMC Enric Holdings Limited

- 7.4 Company Profiles - Furnaces/Boilers

- 7.4.1 Viessmann Group

- 7.4.2 Lennox International Inc.

- 7.4.3 Baxi (BDR Thermea Group)

- 7.4.4 The Fulton Companies

- 7.4.5 Worcester Bosch Group (the Bosch Group)

- 7.4.6 Ideal Boilers (ideal Heating)

- 7.4.7 Burnham Commercial Boilers

8 FUTURE OUTLOOK OF THE MARKET

減壓柴油:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

減壓柴油:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 全球上游生產與資本投資展望:2024-2028

全球上游生產與資本投資展望:2024-2028 2024 年石油和天然氣基礎設施全球市場報告

2024 年石油和天然氣基礎設施全球市場報告 2024 年減壓柴油全球市場報告

2024 年減壓柴油全球市場報告 2024年石油和天然氣中游設備全球市場報告

2024年石油和天然氣中游設備全球市場報告 石油和天然氣工程服務:市場佔有率分析、行業趨勢和統計、2024-2029 年成長預測

石油和天然氣工程服務:市場佔有率分析、行業趨勢和統計、2024-2029 年成長預測 全球油氣發現回顧(2023年)

全球油氣發現回顧(2023年) 石油和天然氣上游活動全球市場報告 2024年

石油和天然氣上游活動全球市場報告 2024年 石油和天然氣支持活動 2024 年世界市場報告

石油和天然氣支持活動 2024 年世界市場報告 中游石油和天然氣設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按應用、地區、競爭細分,2018-2028

中游石油和天然氣設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按應用、地區、競爭細分,2018-2028