|

市場調查報告書

商品編碼

1431632

減壓柴油:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Vacuum Gas Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

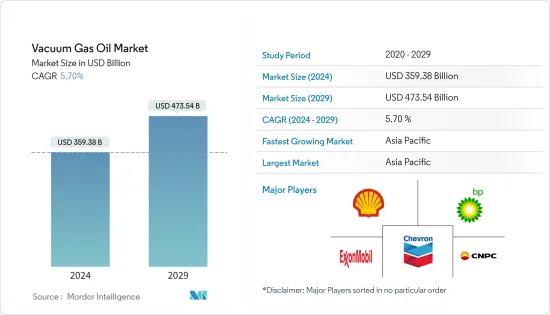

減壓柴油市場規模預計到2024年為3593.8億美元,預計到2029年將達到4735.4億美元,在預測期內(2024-2029年)複合年成長率為5.70%。

主要亮點

- 中期來看,全球汽油需求的增加和汽車工業的快速擴張是推動市場的主要因素。

- 另一方面,全球組織對VGO成分和排放氣體含量的嚴格要求將成為市場的主要限制因素。

- 儘管如此,海洋工業的成長預計將大幅增加深海貨船和其他船舶船用燃油中真空瓦斯油(VGO)的需求,這將在預測期內為市場帶來重大機會。大概。

- 由於石油和天然氣產量的增加,預計亞太地區將主導市場。

減壓柴油市場趨勢

全球汽油和柴油需求不斷成長推動市場

- 減壓瓦斯油主要用作煉油廠擴大汽油和柴油產量的中間原料。 VGO 是在真空蒸餾塔中採用加氫和裂解等製程生產的。

- 柴油一直是交通、農業和各工業部門的主要燃料。然而,有些國家禁止使用柴油。由於經濟發展和流動性增加,印度和中國等開發中國家的柴油消費量也大幅增加。各種需求的柴油消耗量的增加將成為近期VGO成長的驅動力。

- 汽油是美國消耗的主要燃料之一,也是精製生產的主要產品。 2022年,美國消耗了約1,345.5億加侖成品汽油(平均每天約3.69億加侖)。由於真空瓦斯油(VGA)是生產汽油的中間原料,汽油消費量的增加將推動市場成長。

- 此外,2022年全球整體石油消費量量約為9,730萬桶/日,相對高於2015年的9,270萬桶/日。全部區域石油消費量的增加可能會支持 VGO 的成長,因為 VGO 被用作柴油和汽油生產的原料。

- 2022年3月,霍尼韋爾國際公司宣布杜拜油田設備供應商SPEC Energy DMCC將利用該技術將低價值減壓瓦斯油(VGO)和減壓渣油轉化為汽油和烷基化物等高價值產品. 宣佈在其煉油廠中使用Honeywell的成套工藝技術。計劃的第一階段將安裝新的UOP 渣油流化催化裂解裝置,旨在提高汽油產量,以及安裝UOP/木材溶劑脫瀝青製程裝置(SDA),預計將提高RFCC 的供應品質。現已完成。

- 由於上述幾點和最近的發展,在柴油和汽油生產中減壓瓦斯油(VGO)的使用增加將在預測期內推動市場。

亞太地區預計將出現顯著成長

- 減壓瓦斯油是石油蒸餾留下的重油,可以在裂解裝置中進一步精製。這是一種中間原料,可以增加煉油廠柴油和汽油的產量。

- 中國、印度、日本和印尼等國家日益都市化和快速工業化正在推動石油需求,進而推動整個全部區域真空瓦斯油 (VGO) 的成長。此外,汽車需求的成長和石油領域支出的發展是推動該地區 VGO 需求成長的主要因素。

- 此外,2022年12月,雪佛龍公司Lummus Global LLC宣布,山東玉龍石化已為其位於中國山東省的渣油加氫裂解裝置選擇了CLG許可的EST。建成後,該工廠將生產柴油、石腦油和真空瓦斯油 (VGO),並將成為世界上最大的工廠之一,產能為 3.0 MMTA。

- 不過,2022年11月,印度政府宣布將增加對美國、加拿大等各國的真空瓦斯油出口。因此,出口的增加預計將反過來推動全部區域真空瓦斯油市場的成長。

- 由於上述近期發展,亞太地區真空瓦斯油市場預計在預測期內將顯著成長。

減壓柴油產業概況

減壓瓦斯油市場處於半分散狀態。該市場的主要參與者(排名不分先後)包括殼牌公司、英國石油公司、雪佛龍公司、埃克森美孚和中國石油天然氣集團公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 2028年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 全球汽油和柴油需求不斷增加

- 汽車工業快速擴張

- 抑制因素

- 全球組織對 VGO 成分的嚴格規定

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

第5章市場區隔

- 產品

- 低硫含量

- 硫含量高

- 類型

- 輕質減壓瓦斯油

- 重減壓瓦斯油

- 按用途

- 汽油生產

- 輕質油生產

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美地區

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 卡達

- 科威特

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- BP PLC

- Chevron Corporation

- China National Petroleum Corporation

- Eni SpA

- Exxon Mobil Corporation

- Indian Oil Corp. Ltd.

- Kuwait Petroleum Corporation

- NK Rosneft'PAO

- Shell Plc

第7章 市場機會及未來趨勢

簡介目錄

Product Code: 50000865

The Vacuum Gas Oil Market size is estimated at USD 359.38 billion in 2024, and is expected to reach USD 473.54 billion by 2029, growing at a CAGR of 5.70% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, the increasing demand for gasoline globally and the rapidly expanding automotive industry are the major factors driving the market.

- On the other note, the strict mandates by global organizations on VGO composition and emission content will be a major restraint for the market.

- Nevertheless, the growing marine industry is set to surge vacuum gas oil (VGO) requirement in bunker fuels for deep-sea cargo ships and other vessels, which will be a vital opportunity for the market during the forecast period.

- Asia-Pacific is expected to dominate the market, owing to the increasing oil and gas production across the region.

Vacuum Gas Oil Market Trends

Increasing Demand for Gasoline and Diesel Across the Globe to Drive the Market

- Vacuum gas oil is predominantly used as an intermediate feedstock to escalate gasoline and diesel production from refineries. VGO is produced through a vacuum distillation column using processes such as hydrogenation and cracking.

- Diesel has been a primary fuel for transportation, agriculture, and various industrial sectors. However, the use of diesel is banned in some countries. Developing nations, such as India and China, have also experienced significant growth in diesel consumption due to economic development and increased mobility. The growing diesel consumption for various needs will, in turn, drive VGO growth in the near future.

- Gasoline is one of the major fuels consumed in the United States and is the main product that oil refineries produce. In 2022, around 134.55 billion gallons of finished motor gasoline were consumed in the United States, an average of about 369 million gallons per day. Since vacuum gas oil (VGA) is the intermediate feedstock for producing gasoline, the growing consumption of gasoline will, in turn, drive the market's growth.

- Moreover, oil consumption across the globe was around 97.30 million barrels per day in the year 2022, which is comparatively higher than 92.70 million barrels per day in 2015. The growing oil consumption across the region will support the growth of VGO since it is used as a feedstock in the production of gasoil and gasoline.

- In March 2022, Honeywell International Inc. announced that SPEC Energy DMCC, an Oil field equipment supplier in Dubai, was to use a range of Honeywell's process technologies at its refinery to convert low-value vacuum gas oil (VGO) and vacuum residue into high-value products such as gasoline and alkylate. Phase one of the project included the installation of a new UOP Residue Fluidized Catalytic Cracking unit that is tailored to improve gasoline yield, a UOP/Wood Solvent Deasphalting process Unit (SDA) which was expected to improve the feed quality to the RFCC.

- Owing to the above points and the recent developments, the growing usage of Vacuum Gas Oil (VGO) in the production of diesel and gasoline drives the market during the forecast period.

Asia-Pacific Region is Expected to Witness Significant Growth

- Vacuum gas oil refers to heavy oil left over from petroleum distillation, which can be further refined in a cracking unit. It is an intermediate feedstock that can increase the output of diesel and gasoline from refineries.

- The increasing urbanization and rapid industrialization in countries like China, India, Japan, and Indonesia are pushing up oil demand, which will, in turn, favor the growth of vacuum gas oil (VGO) across the region; in addition, the rise in need for automobiles and development in expenditure in the petroleum zone are the major factors responsible for the growth in demand for VGO in this region.

- Moreover, in December 2022, Chevron Corporation Lummus Global LLC announced Shandong Yulong Petrochemical Co., Ltd. had selected EST, which CLG licenses, for a slurry residue hydrocracking unit in Shandong Province, China. The unit will produce diesel, naphtha, and vacuum gas oil (VGO) once it is complete, and with a capacity of 3.0 MMTA, it will be one of the largest in the world.

- Moroever, in November 2022, The Government of India announced they were stepping up vacuum gas oil exports to various countries such as the United States and Canada. Therefore the increasing exports will, in turn, facilitate the growth of the Vacuum Gas Oil Market across the region.

- Owing to the above points and the recent developments, the Asia-Pacific region is expected to witness significant growth in the vacuum gas oil market during the forecast period.

Vacuum Gas Oil Industry Overview

The vacuum gas oil market is semi fragmented. Some of the major players operating in the market (in no particular order) include Shell Plc, BP Plc, Chevron Corporation, Exxon Mobil Corporation, and China National Petroleum Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Gasoline and Diesel Across the Globe

- 4.5.1.2 Rapid Expansion of Automotive Industry

- 4.5.2 Restraints

- 4.5.2.1 Strict Mandates by the Global Organizations on VGO Composition

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product

- 5.1.1 Low Sulfur Content

- 5.1.2 High Sulfur Content

- 5.2 Type

- 5.2.1 Light Vacuum Gas Oil

- 5.2.2 Heavy Vacuum Gas Oil

- 5.3 By Application

- 5.3.1 Gasoline Production

- 5.3.2 Diesel Oil Production

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Asia-Pacific

- 5.4.2.1 China

- 5.4.2.2 India

- 5.4.2.3 Japan

- 5.4.2.4 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Qatar

- 5.4.5.5 Kuwait

- 5.4.5.6 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BP PLC

- 6.3.2 Chevron Corporation

- 6.3.3 China National Petroleum Corporation

- 6.3.4 Eni SpA

- 6.3.5 Exxon Mobil Corporation

- 6.3.6 Indian Oil Corp. Ltd.

- 6.3.7 Kuwait Petroleum Corporation

- 6.3.8 NK Rosneft' PAO

- 6.3.9 Shell Plc

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Growth in Marine Industry

02-2729-4219

+886-2-2729-4219

工業固定設備:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

工業固定設備:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 全球上游生產與資本投資展望:2024-2028

全球上游生產與資本投資展望:2024-2028 2024 年石油和天然氣基礎設施全球市場報告

2024 年石油和天然氣基礎設施全球市場報告 2024 年減壓柴油全球市場報告

2024 年減壓柴油全球市場報告 2024年石油和天然氣中游設備全球市場報告

2024年石油和天然氣中游設備全球市場報告 石油和天然氣工程服務:市場佔有率分析、行業趨勢和統計、2024-2029 年成長預測

石油和天然氣工程服務:市場佔有率分析、行業趨勢和統計、2024-2029 年成長預測 全球油氣發現回顧(2023年)

全球油氣發現回顧(2023年) 石油和天然氣上游活動全球市場報告 2024年

石油和天然氣上游活動全球市場報告 2024年 石油和天然氣支持活動 2024 年世界市場報告

石油和天然氣支持活動 2024 年世界市場報告 中游石油和天然氣設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按應用、地區、競爭細分,2018-2028

中游石油和天然氣設備市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按應用、地區、競爭細分,2018-2028

▼