|

市場調查報告書

商品編碼

1351468

衛星 D2D(直接到設備)市場:第四版Satellite Direct to Device Markets, 4th Edition |

||||||

本報告調查了衛星D2D(直接到設備)市場,包括服務收入和流量趨勢和預測、按行業細分和地區進行的詳細分析、技術趨勢、市場影響因素和市場機會分析以及各種資訊。我們正在編制建議等

主要特點

本文檔的內容

- 進入衛星D2D生態系統的主要建議

- 服務收入預測:按地區/細分市場

- 流量預測:按地區/類別

- 目標市場的定義

- 衛星D2D能力的主要優點和限制回顧

- 技術演進的時機及其對市場發展的影響

- 關鍵策略選擇的評估和影響:頻率、標準和商業模式

本書中的分類

- 消費者

- 交通

- 服務收入

- 物聯網

- 交通

- 服務收入

- 政府/軍隊

- 交通

- 服務收入

本書中介紹的公司

- Airbus

- Apple

- AST SpaceMobile

- AT&T

- Bullitt

- Echostar

- Ericsson

- Globalstar

- Honor

- Huawei

- Inmarsat

- Iridium

- Lynk

- Mediatek

- Motorola

- Nokia

- Nothing

- OmniSpace

- Oppo

- PNCC

- Qualcomm

- Rakuten

- Sateliot

- SCT

- Skylo

- SMART

- Starlink

- Telefónica

- Thales Alenia Space

- T-Mobile

- vivo

- Vodafone

- Xiaomi

目錄

關於本書

執行摘要

調查概覽

- 挑戰:行動網路業者的收入流和社會影響受到其地面網路覆蓋範圍的限制。

- 解決方案:衛星 D2D 透過提高用戶參與度、支援新服務和降低農村網路部署成本來擴大 MNO 的機會

推薦

- 1. D2D:MNO差異化與成長的新泉源

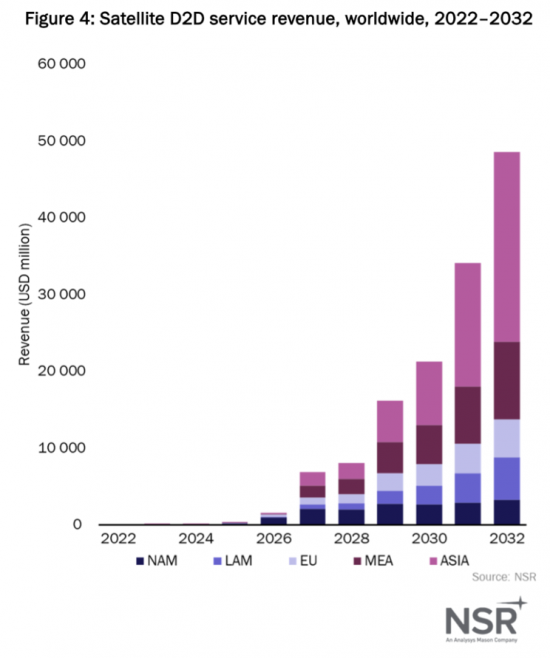

- 1、 2032年衛星D2D服務收入將飆升至486億美元

- 2. D2D 預計將吸引來自三個主要領域的市場興趣:消費者、物聯網和政府/軍事。

- 3.消費者領域在收入領域佔據主導地位,但物聯網和政府/軍隊提供了特殊機會

- 4.衛星 D2D 不會對行動網路營運商構成競爭風險,該技術應被視為能帶來新的收入來源

- 2.適應快節奏的技術與業務演進

- 1.新進的業者必須不斷適應技術和業務的快節奏演進。

- 2.供應時機對於平衡市場準備度和競爭優勢至關重要。頻寬是關鍵資源,需要大幅增加供應

- 3.價值鏈調整

- 1.建構正確的合作夥伴生態系統是提供複雜的 D2D 解決方案的關鍵

- 2.由於向後相容性,使用MNO頻寬可以實現快速啟動。MSS 透過監管確定性和績效改進獲得長期利益

- 3.儘管專有協定提供了更快的商業化途徑,但基於標準的解決方案是促進可擴展性的首選方法。

- 4.衛星服務需要關注對行動網路營運商有吸引力的批發模式

附錄:研究方法

關於作者和 Analysys Mason

Report Summary:

NSR's “Satellite Direct to Device Markets, 4th Edition (D2D4) ” report provides a comprehensive analysis of the satellite D2D (Direct-to-Device) market opportunity, including market drivers and restraints, key use cases, and strategic insights.

Market Opportunity and Overview:

- The report describes the satellite D2D market opportunity, which represents a significant growth area within the satellite industry.

- NSR was one of the first market research firms to identify this opportunity, and this report represents the 4th annual update with a high level of maturity and in-depth analysis.

Key Focus Areas:

- NSR's “D2D4” aims to build a complete picture of trends and strategic choices within the satellite D2D market.

- It provides forecasts for service revenues and traffic broken down by region and market segment.

- Recommendations are offered for satellite operators, mobile network operators (MNOs), and equipment and infrastructure vendors on how to capture a portion of this growing market.

Key Questions Addressed:

- What is the revenue opportunity for the emerging satellite D2D market?

- What use cases can MNOs target beyond their terrestrial coverage leveraging satellite D2D?

- What are the limitations and strength of satellite D2D?

- Which are the key technology developments that will shape the future of the market and how should players stay adaptive to this evolution?

- Who are the main players and which are the different strategies (spectrum, supply and capabilities, standards, business models, etc.)?

Target Audience

NSR's “Satellite Direct to Device Markets” report is intended for various stakeholders in the satellite and telecommunications industries, including:

- Satellite operators seeking to understand revenue potential, traffic forecasts, and market dynamics.

- MNOs and CSPs interested in satellite D2D as a source of growth and differentiation.

- Chipset and parts vendors, OEMs, and infrastructure vendors (both space and terrestrial) looking to assess strategic choices in terms of spectrum, standards, and business models.

- Regulators and industry agencies seeking to leverage D2D to foster innovation and bridge the digital divide.

Differentiating Factors:

- NSR's “Satellite Direct to Device Markets” stands out due to the unique combination of expertise from NSR in the satellite industry and Analysys Mason's knowledge of telecommunications trends.

- “D2D4” leverages NSR's understanding of the space industry and Analysys Mason's insights into telco trends and consumer needs.

- “Satellite Direct to Device 4” draws from extensive primary research, including interviews with key industry players, and is based on a solid foundation of secondary research.

- NSR's “D2D4” serves as a roadmap for future strategic decisions, helping readers navigate various market segments, regions, and strategic options in the dynamic satellite D2D landscape.

NSR's “Satellite Direct to Device Markets, 4th Edition” report offers valuable insights and recommendations for industry stakeholders interested in capitalizing on the emerging satellite D2D market opportunity. It leverages the expertise of NSR and Analysys Mason to provide a comprehensive and unbiased analysis of this evolving landscape.

Key Features:

Covered in this Report:

- Key recommendations for participating in the satellite D2D ecosystem

- Service revenues forecast by region and segment

- Traffic forecast by region and segment

- Addressable market definition

- Review of the key strength and limitations of the satellite D2D capabilities

- Timing of the technology evolution and implications for the development of the market

- Assessment and implications of key strategic choices: spectrum, standards and business models

Report Segmentation:

- Consumer

- Traffic

- Service Revenues

- IoT

- Traffic

- Service Revenues

- Government and Military

- Traffic

- Service Revenues

Companies included in this Report:

Airbus, Apple, AST SpaceMobile, AT&T, Bullitt, Echostar, Ericsson, Globalstar, Honor, Huawei, Inmarsat, Iridium, Lynk, Mediatek, Motorola, Nokia, Nothing, OmniSpace, Oppo, PNCC, Qualcomm, Rakuten, Sateliot, SCT, Skylo, SMART, Starlink, Telefónica, Thales Alenia Space, T-Mobile, vivo, Vodafone, Xiaomi.

Table of Contents

About this report

Executive summary

Research overview

- Challenge: MNOs' revenue sources and social impact are limited by the reach of terrestrial networks

- Solution: Satellite D2D extends MNOs' opportunities by boosting subscriber engagement, enabling new services and reducing rural network deployment costs

Recommendations

- 1. D2D as MNOs' new source of differentiation and growth

- 1. Satellite D2D service revenues to skyrocket to 48.6USD billion by 2032

- 2. D2D will attract market interest from 3 main segments: consumer, IoT and Gov/Mil

- 3. Consumer segment to dominate the revenue scene, but IoT and Gov/Mil present specialized opportunities

- 4. Satellite D2D does not represent a competitive risk for MNOs. The technology should be regarded as an enabler for new revenue streams

- 2. Fit for the fast-paced technology and business evolution

- 1. Actors in the field should stay adaptative to the extraordinarily fast evolution in technology and business

- 2. Timing of supply is critical to balance market readiness and competitive advantage. Spectrum is the key resource. Exponential supply growth needed

- 3. Aligning the value chain

- 1. Building the right ecosystem of partners is critical to deliver D2D's complex solution

- 2. Using MNOs' spectrum offers faster ramp-up thanks to backward compatibility. MSS long-term advantages due to regulatory certainty and enhanced performances

- 3. Standards-based solutions should be the preferred approach to facilitate scalability, albeit proprietary protocols offer a faster path to commercialization

- 4. Satellite offerings should focus on wholesale models that are attractive for MNOs

Appendix Methodology

About the authors and Analysys Mason

List of Exhibits

- Figure 1: Evolving Space enablers unlocking the opportunities in the satellite D2D market

- Figure 2: MNOs' limitations to create and capture value beyond their coverage

- Figure 3: Key segments enabled by satellite D2D

- Figure 4: Satellite D2D service revenues worldwide, 2022-2032

- Figure 5: share of service revenues per vertical worldwide

- Figure 6: satellite D2D cumulative service revenues (USD million) worldwide, 2022 to 2032

- Figure 7: Satellite D2D traffic with technology phases worldwide, 2022 to 2032

- Figure 8: generic legacy constellation supply case study

嵌入式衛星系統市場:2024-2034年

嵌入式衛星系統市場:2024-2034年 2024 年衛星全球市場報告

2024 年衛星全球市場報告 商業衛星組件市場:按組件、品質等級分類 - 2024-2030 年全球預測

商業衛星組件市場:按組件、品質等級分類 - 2024-2030 年全球預測 基於衛星的物聯網服務市場:按類型、頻寬、組織規模和服務分類 - 2024-2030 年全球預測

基於衛星的物聯網服務市場:按類型、頻寬、組織規模和服務分類 - 2024-2030 年全球預測 衛星對接系統市場:按服務類型、太空船類型、最終用戶分類 - 全球預測 2024-2030

衛星對接系統市場:按服務類型、太空船類型、最終用戶分類 - 全球預測 2024-2030 衛星指揮與控制系統市場:按組件、安裝類型、平台、頻寬、應用和最終用戶 - 2024-2030 年全球預測

衛星指揮與控制系統市場:按組件、安裝類型、平台、頻寬、應用和最終用戶 - 2024-2030 年全球預測 衛星 5G 新無線電市場:按服務、頻段和最終用戶分類 - 全球預測 2024-2030 年

衛星 5G 新無線電市場:按服務、頻段和最終用戶分類 - 全球預測 2024-2030 年 衛星在軌服務市場:按服務類型、衛星類型、軌道、最終用戶分類 - 全球預測 2024-2030

衛星在軌服務市場:按服務類型、衛星類型、軌道、最終用戶分類 - 全球預測 2024-2030 衛星指揮與控制 (C2) 系統:市場與技術預測(~2032 年)

衛星指揮與控制 (C2) 系統:市場與技術預測(~2032 年) 大型衛星推進和 AOCS 子系統的全球市場:按應用、最終用戶、子系統和地區進行分析和預測(2023-2033 年)

大型衛星推進和 AOCS 子系統的全球市場:按應用、最終用戶、子系統和地區進行分析和預測(2023-2033 年)