|

市場調查報告書

商品編碼

1270831

通訊業者的5G代價 - 2022年債務增加,較低利潤:COVID以後,投資劇增,部分通訊業者陷入困境- 隨著利率上升和新收入未能出現,需要管理債務增加Telcos Pay 5G Price - Higher Debt, Lower Margins in 2022: Investments Have Surged Since COVID, Putting Some Telcos in Tough Spot - Need to Manage Higher Debt as Interest Rates Rise and New Revenues Fail to Appear |

||||||

價格

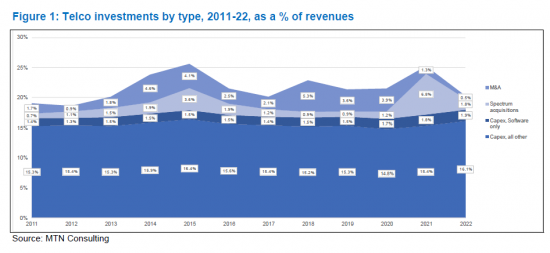

2022年第四季的通訊業者的負債總額為1兆1,400億美金,17%明年還款到期。銷售額中軟體設備投資佔的比例,2022年成為1.9%,從2021年的1.8%稍微上升。收購的支出2022年成為銷售額的0.5%,是2012年以後最低的數值。

視覺

本報告提供通訊業者為焦點,彙整到目前為止的設備投資趨勢,2022年第四季的負債,今後預測等相關資料。

目錄

- 摘要

- 通訊業者過去2年,在設備投資,頻帶,M&A花費了高額的費用

- 2022年第四季的電信業者負債總額是1兆1,400億美元,17%到明年還款到期

- 淨負債2022年減少了,不過,EBITDA比率與2015~19年相符

- 許多各個的通訊業者的債務等級限制支出

- 利益,負債,支出預測的影響

- 附錄

Product Code: GNI-03052023-1

This brief report presents data aimed at shedding light on the following question: can telcos afford to pay for their future investment needs? The report considers debt, cash, and margin metrics, for the industry overall and for specific key players. It also speculates how 2022 trends may impact 2023 and beyond, in a rising interest rate climate. A number of large telcos have high debt, low margins, and/or weak top line growth, and may have to curtail spending in 2023-4 in order to cope with this reality.

VISUALS

Key findings include:

- Total telco debt in 4Q22 was $1.14 trillion, 17% due in next year

- Software capex as a % of revenues was 1.9% in 2022, up a bit from 1.8% in 2021.

- Spending on acquisitions amounted to 0.5% of revenues in 2022, the lowest figure since 2012.

- At the industry level, the ratio of net debt to EBITDA in 2022 was 1.9, a bit up from 2021 but down from 2020.

- A number of large telcos face short-term debt levels over 30% of total debt

- Average margins for the industry in 2022 disappointed: free cash flow margin for the telco industry in 2022 was 11.4%, down from 12.6% in 2021; EBITDA margin was 33.7% (2021: 34.0%), and EBIT margin was 14.4% (2021: 14.9%).

Companies mentioned:

|

|

Table of Contents

- Summary

- Telcos have spent big on capex, spectrum and M&A in last 2 years

- Total telco debt in 4Q22 was $1.14 trillion, 17% due in next year

- Net debt declined in 2022 but ratio to EBITDA in line with 2015-19

- Many individual telcos have debt levels which will constrain their spending

- Margins, debt, and implications for spending outlook

- Appendix

List of Figures

- Figure 1: Telco investments by type, 2011-22, as a % of revenues

- Figure 2: Telco sector total debt in US$B, and short-term debt as % total

- Figure 3: Components of telco sector total debt at year-end 2022 (US$B)*

- Figure 4: Telco industry net debt ($M) and net debt to EBITDA ratio, 2011-22

- Figure 5: Telcos with net debt to EBITDA ratios above 3 (YE2022)**

02-2729-4219

+886-2-2729-4219

通訊營運管理:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

通訊營運管理:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 2024 年電信營運管理全球市場報告

2024 年電信營運管理全球市場報告 全球電信營運管理市場

全球電信營運管理市場 通信網絡能源效率將每年提高12%:每兆瓦時能源消耗的流量將從2020年的12.3TB增長到2022年的15.5TB,但進一步提高效率對於降低成本和排放至關重要

通信網絡能源效率將每年提高12%:每兆瓦時能源消耗的流量將從2020年的12.3TB增長到2022年的15.5TB,但進一步提高效率對於降低成本和排放至關重要 電信營運管理市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會及預測

電信營運管理市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會及預測 2016-2022 年電信運營費用 (OPEX) 分析:2022 年網絡運營費用和折舊成本驅動的網絡運營費用將佔電信公司總運營費用的一半

2016-2022 年電信運營費用 (OPEX) 分析:2022 年網絡運營費用和折舊成本驅動的網絡運營費用將佔電信公司總運營費用的一半 電信營運管理市場:依軟體類型、服務、部署類型分類 - 2023-2030 年全球預測

電信營運管理市場:依軟體類型、服務、部署類型分類 - 2023-2030 年全球預測 Web 3.0的通訊業者:駕馭不斷變化的服務和基礎設施格局

Web 3.0的通訊業者:駕馭不斷變化的服務和基礎設施格局 健康市場上通訊業者的策略

健康市場上通訊業者的策略 通訊運用管理的全球市場 2022-2026

通訊運用管理的全球市場 2022-2026

▼