|

市場調查報告書

商品編碼

1132080

華為重振努力:雲上成功固然重要,但確保芯片獨立性和建立強大的供應鍊是關鍵Huawei's Quest for Resurgence: Cloud Success is Vital, but Attaining Chip Independence and Grooming a Robust Supply Chain Holds Key |

||||||

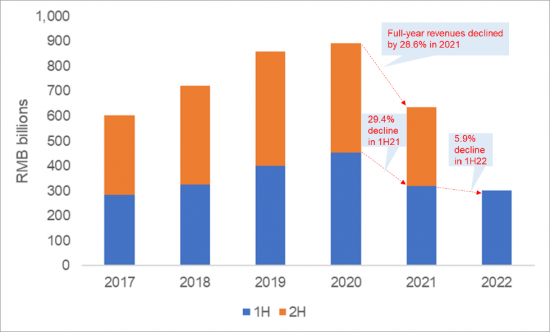

2018 年和 2020 年的美國製裁繼續困擾著華為。該公司被迫出售多個業務線,包括其低端智能手機部門榮耀和 x86 服務器業務,這對其“黃金寶石”電信設備業務的全球地位造成了影響。這些挫折讓華為陷入了動盪,2021年的年收入降幅最大,達到28.6%。 2022年上半年銷量下滑趨勢將持續,但下滑速度明顯放緩。然而,由於美國技術限制帶來的惡劣經濟環境,客戶需求下降了一半以上,這不足以遏制這一時期的淨收入下降。

圖表示例

受當前動蕩的影響,華為在雲計算和供應鏈獨立性上押注很大,以進一步降低風險。對雲的關注源於實體清單裁決對服務和軟件缺乏直接影響。該公司已經在雲領域取得了長足的進步,成為僅次於阿裡巴巴的中國第二大雲提供商。考慮到華為在與中國省級政府和國有企業打交道的經驗,強大的政府部門雲產品組合是一大優勢。另一個優勢是我們在不受美國製裁直接影響的市場中的海外雲數據中心的記錄。在中國宏偉的“一帶一路”倡議(BRI)下,華為也是全球數字擴張計劃——數字絲綢之路(DSR)的重要參與者。

為了重建供應鏈,華為致力於端到端的自主創新,以加強硬件和雲相關業務。公司旗下芯片子公司海思為數據中心服務器處理器和設備以及電信網絡設備設計芯片,同時也生產自己的芯片,與國內晶圓廠合作,投資國內芯片初創企業。我們的主要戰略。

華為的複興有兩個方面:

- 雲服務業務:基於硬件的消費行業受到了重創,因此您的工作是彌補一些差距。

- 獲得可以在競爭中脫穎而出的先進芯片

華為能夠提出獨特的建議,例如雲服務與電信設備業務之間的協同效應,通過其最近發布的電信運營商雲解決方案以及與電信運營商的靈活合作模式,方面似乎是可以實現的。

但第二點可能是華為的絆腳石。這是因為國產芯片製造所取得的技術能力落後於英特爾、台積電、三星很多年。在找到解決先進製造短板的方法之前,華為將繼續依賴能力較弱的國內晶圓廠,並在未來三到四年內處於生存模式。此外,華為目前嚴重依賴 ARM 在其華為雲產品中心的數據中心設計服務器芯片。美國還可以找到限制 ARM 與華為合作的方法,迫使中國供應商訴諸 RISC-V 替代方案。

在這份報告中,我們調查了華為近期的業績趨勢和主要問題,以及克服困難的措施——推進雲業務、加強供應鍊等——以及需要解決的問題。我們來了。

分析範圍

本報告分析的公司和組織:

|

|

內容

- 概覽

- 制裁動搖了華為的全球地位

- 華為全力以赴保護雲和足夠的芯片

- 華為要找回失去的魔力還有很長的路要走

The US sanctions imposed way back in 2018, and then again in 2020, continue to haunt Huawei. The company was forced to divest some business lines- including its mid- to low-end smartphone unit, Honor, and x86 server business - and its global standing in its "crown jewel" telecom equipment business has taken a hit. These setbacks have sent Huawei into a tizzy as it reported its biggest ever annual revenue drop of 28.6% in 2021. Though the revenue downtrend continued into 1H22, the pace of drop slowed down drastically. But that wasn't enough to contain net profit decline during the period, which more than halved as a difficult economy reduced demand from customers, intensifying woes brought by the US technology curbs.

VISUALS

Hard-pressed by the current turmoil, Huawei is betting big on cloud and supply chain independence to alleviate any further risks. The cloud focus emerges from the fact that there is no direct impact from the Entity List ruling on services and software. The company is already making notable strides in the cloud space, with its emergence as the second-biggest cloud provider after Alibaba in China. Its strong cloud portfolio for the government sector is a big advantage, considering Huawei's experience working with provincial governments and state-owned enterprises in China. The other advantage is its overseas cloud data center footprint, which are in markets less directly impacted by US sanctions. Huawei is also an essential player engaged in China's global digital expansion initiative, "Digital Silk Road" (DSR), under its grand Belt and Road Initiative (BRI).

To rebuild its supply chain, Huawei is aspiring to end-to-end home-grown innovation to power both its hardware- and cloud-related businesses. While its chip subsidiary, HiSilicon, designs data center server processors and chips for devices and telecom network equipment, it is seeking to ramp up production capabilities through a three-pronged strategy: build in-house chips, partner with domestic fabs, and invest in domestic chip startups.

Huawei's efforts to stage a comeback will depend on two aspects:

- Cloud services business, which will be tasked to somewhat address the gap left by the severely hit hardware-based consumer division

- Access to advanced chips that can take on the competition

The first aspect looks achievable as Huawei will be able to offer distinctive propositions such as synergies between its cloud offering and telecom equipment business, through its recently launched telco cloud solutions, coupled with a flexible collaboration model with the telcos.

The second aspect, though, could prove to be a stumbling block for Huawei, as technological capabilities achieved through homegrown chip manufacturing are years behind the capabilities possessed by Intel, TSMC, and Samsung. Until a solution to its advanced manufacturing shortcoming is figured out, Huawei will continue to rely on less-capable domestic fabs, which will put the company in survival mode for the next 3-4 years. Further, Huawei is currently relying heavily on ARM for design of its data center server chips, which are central to the Huawei Cloud offering. There is some chance that the US will find a way to restrict ARM from working with Huawei, forcing the Chinese vendor to lean on RISC-V alternatives.

Coverage:

Companies and organizations mentioned in this report include:

|

|

Table of Contents

- Summary

- Sanctions roil Huawei's global standing

- Huawei goes full throttle on cloud, and chip sufficiency

- Huawei's journey to regain its lost mojo will be a long one

List of Figures

- Figure 1: Huawei's annualized share of telco network infrastructure market

- Figure 2: Huawei total revenues: Half-yearly basis, 2017-22

- Figure 3: Huawei's R&D and R&D/revenues: 2017-21

超大規模雲端市場預測至 2030 年 - 各服務類型(基礎設施即服務、軟體即服務和平台即服務)、企業類型、應用程式、最終用戶和地理位置全球分析

超大規模雲端市場預測至 2030 年 - 各服務類型(基礎設施即服務、軟體即服務和平台即服務)、企業類型、應用程式、最終用戶和地理位置全球分析 雲端基礎的資料管理服務市場至2030年的預測:按服務類型、服務模型、部署模式、最終用戶和地區進行的全球分析

雲端基礎的資料管理服務市場至2030年的預測:按服務類型、服務模型、部署模式、最終用戶和地區進行的全球分析 2024 年石油和天然氣雲端應用全球市場報告

2024 年石油和天然氣雲端應用全球市場報告 2024 年雲端專業服務全球市場報告

2024 年雲端專業服務全球市場報告 雲端的現況:透過雲端運算、人工智慧和資料在拉丁美洲最大限度地實現業務成功

雲端的現況:透過雲端運算、人工智慧和資料在拉丁美洲最大限度地實現業務成功 雲端聽寫解決方案市場報告:至2030年的趨勢、預測與競爭分析

雲端聽寫解決方案市場報告:至2030年的趨勢、預測與競爭分析 雲端成長機會:10 個關鍵項目(2024 年)

雲端成長機會:10 個關鍵項目(2024 年) 雲端基礎的資料管理服務的全球市場:按服務類型、按服務模型、按部署模式、按行業、按地區 - 預測到 2028 年

雲端基礎的資料管理服務的全球市場:按服務類型、按服務模型、按部署模式、按行業、按地區 - 預測到 2028 年 雲端的現況:利用雲端運算、人工智慧和資料實現業務成功

雲端的現況:利用雲端運算、人工智慧和資料實現業務成功 2023-2028 年按服務(平台即服務、軟體即服務、基礎設施即服務)、組織規模、部署模型、最終用途產業和地區分類的雲端專業服務市場報告

2023-2028 年按服務(平台即服務、軟體即服務、基礎設施即服務)、組織規模、部署模型、最終用途產業和地區分類的雲端專業服務市場報告