|

市場調查報告書

商品編碼

1445519

硫酸:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Sulfuric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

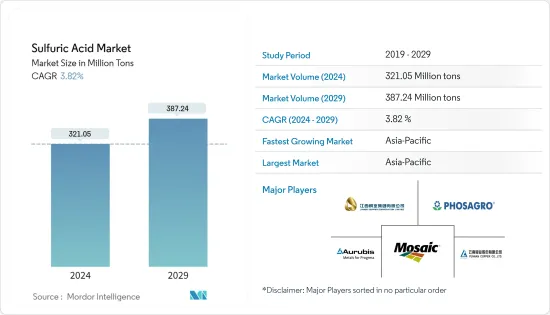

2024年硫酸市場規模預估為3,2,105萬噸,預估至2029年將達到3,8,724萬噸,在預測期內(2024-2029年)年複合成長率為3.82%。

COVID-19大流行對2020年硫酸市場產生了中等影響。各國實施的封鎖和供應中斷影響了化學工業。然而,由於硫酸是化學行業使用的主要化學品之一,因此預計在預測期內需求將會很高。

主要亮點

- 短期內,市場研究是由磷基肥料中硫酸的高需求以及全球化學和製藥行業不斷成長的需求所推動的。

- 另一方面,原物料價格的波動可能會減緩未來幾年硫酸市場的成長。

- 發煙硫酸在醫療和其他行業中的使用不斷增加,可以被視為一個巨大的市場機會。

- 亞太地區主導全球硫酸市場,其中中國、印度和日本等國家的消費量最大。

硫酸市場趨勢

化肥領域消費擴大

- 硫酸是由硫、氫和氧組成的強無機酸。它是一種透明油狀液體,有強烈氣味,具有強腐蝕性。即使是稀釋形式,也應始終小心處理。當用水稀釋時,陶瓷排氣反應會釋放熱量。它是肥料製造過程中使用的重要工業化學品。

- 世界上大約一半的硫酸供應用於農業和農業,特別是用作肥料。硫酸用於生產磷肥,例如過磷酸鈣和硫酸銨。硫酸可以提高作物產量,並透過生產更有營養的作物幫助農民賺更多的收益。

- 肥料替代作物從土壤中吸收的養分。如果沒有化肥,作物產量和農業生產力將會大幅下降。因此,礦物肥料用於補充土壤的養分,其中含有易於被作物吸收和利用的礦物質。

- 農業是全世界生計的主要來源。印度和美國的農業正在經歷積極成長。因此,未來幾年市場可能會受到化肥需求的推動。

- 例如,根據聯合國糧食及農業組織的數據,2021年全球氨、磷酸鹽和鉀肥產能為315,973噸,預計2022年將達到318,652噸,導致硫酸市場需求增加。預測期。

- 2021年,農產品及相關產品出口總額達412.5億美元。灌溉投資的增加擴大了灌溉面積,創造了化肥需求,並刺激了硫酸市場。

- 拉丁美洲和加勒比地區的農業部門過去經歷了顯著成長。根據經濟合作暨發展組織(OECD)和聯合國糧食及農業組織(FAO)的預測,2018年至2028年農業和漁業產量預計將增加17%。預計這一成長的約 53% 將歸因於作物產量的增加。因此,農業的發展增加了對化肥的需求。預計這將影響硫酸市場的成長。

- 根據國際肥料工業協會的數據,2021 年全球消耗了 199,884 噸農業肥料(氮、磷、鉀 (NPK))。在總消費量量中,2021年東亞、南亞、拉丁美洲、加勒比海和北美分別消費了61,936千噸、38,694千噸、28,817千噸和25,730千噸。

- 因此,未來幾年肥料中硫酸使用量的增加可能會推動市場的發展。

亞太地區主導市場

- 預計亞太地區在預測期內將主導硫酸市場。由於中國、印度和日本等化工、化肥和其他製造業的高需求,硫酸市場正在迅速擴張。

- 根據中國國家統計局數據,2021年中國硫酸產量為9,383萬噸,較2020年的9,238萬噸增加1.5%以上。我國硫酸產量持續增加,2022年產能達1.29億噸,年增1.59%。

- 在中國,企業計劃將硫酸產能提高至每年2,108萬噸。 2022年至2024年產能增加後,預計國內硫酸市場供應格局將發生重大變化,包括出口增加、進口減少、貨流變化等。

- 中國是世界上最大的化肥生產國。根據國家統計局數據,2021年我國氮磷鉀肥產量5,544萬噸,比2020年的5,496萬噸增加0.87%。

- 在印度,2021 年 7 月,奧里薩邦首席部長為肥料合作社 IFFCO 帕拉迪普分部的硫酸生產設施奠基。該計劃將耗資約 40 億印度盧比(約 4,836 萬美元),預計將於 2023 年投入營運。這個新生產廠將減少我們對化學品進口的依賴。這是 IFFCO 的第三座硫酸生產廠,產能約為每天 2,000 噸 (MT)。

- 此外,印度是高度依賴農業的經濟體之一。農業仍是55%以上人口的主要生計來源。根據印度2020-21年經濟調查報告,20會計年度印度糧食總產量為2.9665億噸,比2019會計年度的2.8521億噸增加1144萬噸。

- 所有上述因素預計將在預測期內增加亞太地區對硫酸的需求。

硫酸產業概況

全球硫酸市場高度分散。主導市場的前五名公司是 Mosaic、PhosAgro Group of Companies、江西銅業集團、雲南銅業和 Aurubis AG。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 磷基肥料對硫酸的需求量大

- 化學和製藥行業需求不斷成長

- 抑制因素

- 原物料價格波動

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

- 貿易分析

- 原料分析

- 區域產能

第5章市場區隔

- 原料類型

- 單質硫

- 黃鐵礦

- 其他類型原料

- 最終用戶產業

- 肥料

- 化學和製藥

- 車

- 石油精製

- 其他最終用戶產業(紙漿和造紙、金屬加工)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 合併、收購、合資、合作和協議

- 市場佔有率(%)分析

- 主要企業採取的策略

- 公司簡介

- Aarti Industries Limited

- Aurubis AG

- Bodal Chemicals Ltd

- Boliden Group

- Hindustan Zinc

- Jiangxi Copper Group Co. Ltd

- KANTO KAGAKU

- Nouryon

- Panoli Intermediates India Private Limited

- PhosAgro Group of Companies

- PVS

- Mosaic

- WeylChem International GmbH

- Yunnan Copper Co. Ltd

第7章市場機會與未來趨勢

- 發煙硫酸在醫療和其他行業的使用增加

The Sulfuric Acid Market size is estimated at 321.05 Million tons in 2024, and is expected to reach 387.24 Million tons by 2029, growing at a CAGR of 3.82% during the forecast period (2024-2029).

The COVID-19 pandemic moderately affected the sulfuric acid market in 2020. The imposition of lockdowns across various countries and disruptions in supply affected the chemical sector. However, since sulfuric acid is among the primary chemicals used in the chemical sector, high demand is anticipated in the forecast period.

Key Highlights

- In the short term, the market study is being driven by the high demand for sulfuric acid in phosphate-based fertilizers and the growing demand from the chemical and pharmaceutical industries around the world.

- On the other hand, changes in the prices of raw materials are likely to slow the growth of the sulfuric acid market in the coming years.

- The growing use of oleum in medical and other industries can be seen as a major opportunity for the market.

- The Asia-Pacific region dominated the sulfuric acid market globally, with the highest consumption coming from countries such as China, India, and Japan.

Sulfuric Acid Market Trends

Growing Consumption from Fertilizer Segment

- Sulfuric acid is a strong mineral acid made up of sulfur, hydrogen, and oxygen. It has a strong smell and is an extremely corrosive, oily, and clear liquid. It should always be handled with caution, even in its diluted form. When diluted with water, it releases heat in a ceramic exhaust reaction. It is an important industrial chemical used in fertilizer manufacturing processes.

- Around half of the global sulfuric acid supply is used in agriculture and farming, especially as fertilizer. Sulfuric acid is used to manufacture phosphate fertilizers, such as the superphosphate of lime and ammonium sulfate. Sulfuric acid increases crop yield, which helps farmers generate more revenue by producing highly nutritional crops.

- Fertilizers replace the nutrients that crops remove from the soil. Without fertilizers, crop yields and agricultural productivity would be significantly reduced. Due to this, mineral fertilizers are used to supplement the soil's nutrient stocks with minerals that may be quickly absorbed and used by crops.

- Agriculture is the major source of livelihood globally; India and the United States are witnessing positive growth in agriculture. So, the market is likely to be driven by the need for fertilizers over the next few years.

- For instance, according to the Food and Agriculture Organization, the global capacity for producing ammonia, phosphoric acid, and potash in 2021 was 315,973 metric tons, which is expected to reach 318,652 metric tons in 2022, thereby boosting the market demand for sulfuric acid in the forecast period.

- The total agricultural and allied products exports stood at USD 41.25 billion in 2021. The growing investments in irrigation enhanced the gross irrigated area, creating a demand for fertilizers and stimulating the sulfuric acid market.

- The agriculture sector in Latin America and the Caribbean has witnessed significant growth in the past. According to the Organization for Economic Co-operation and Development (OECD) and the Food and Agriculture Organization of the United Nations (FAO), agricultural and fisheries production is expected to grow by 17% during 2018-2028. Around 53% of this growth is expected to come from increased crop production. Hence, the growing agricultural industry boosted the demand for fertilizers. This is expected to impact the growth of the sulfuric acid market.

- According to the International Fertilizer Industry Association, the consumption of agricultural fertilizer (nitrogen, phosphorus, and potassium (NPK)) across the globe accounted for 199,884 kilotons in 2021. Out of the total consumption, East Asia, South Asia, Latin America and the Caribbean, and North America consumed 61,936 kilotons, 38,694 kilotons, 28,817 kilotons, and 25,730 kilotons, respectively, in 2021.

- So, the market is likely to be driven by the growing use of sulfuric acid in fertilizers over the next few years.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the sulfuric acid market during the forecast period. Due to the high demand from the chemical, fertilizer, and other manufacturing sectors in countries like China, India, and Japan, the sulfuric acid market has been rapidly increasing.

- In 2021, the sulfuric acid production in China was 93.83 million metric tons, compared to 92.38 million metric tons in 2020, registering a growth of over 1.5%, according to the National Bureau of Statistics of China. The sulfuric acid production output continued to rise in China, with a manufacturing capacity of 129 million tons in 2022, registering a growth of 1.59% from the same period in the previous year.

- In China, companies are planning to increase the manufacturing capacity of sulfuric acid to 21.08 million tons annually. After the capacity increase in 2022-2024, the supply pattern of the sulfuric acid market is expected to undergo significant changes in the country, including increasing exports, shrinking imports, and changes in goods flow.

- China is the largest fertilizer manufacturer in the world. According to the National Bureau of Statistics of China, the nitrogen, phosphate, and potash fertilizer production volume in China accounted for 55.44 million tons in 2021, compared to 54.96 million tons in 2020, registering a growth of 0.87%.

- In India, in July 2021, the Chief Minister of Odisha laid the foundation stone for a sulfuric acid manufacturing facility on the premises of the fertilizer cooperative IFFCO at its Paradip division. The project will cost around INR 400 crore (~USD 48.36 million), with operations estimated to start by 2023. This new production plant will reduce dependency on the import of chemicals. This is IFFCO's third sulfuric acid manufacturing plant, with a capacity of about 2,000 metric tons (MT) per day.

- Furthermore, India is one of the economies largely dependent on agriculture. Agriculture is still the primary source of livelihood for more than 55% of the population. According to The Economic Survey of India 2020-21 report, in FY20, the total food grain production in the country was recorded at 296.65 million tons, which increased by 11.44 million tons compared with 285.21 million tons in FY19.

- All the factors mentioned above are expected to boost the demand for sulfuric acid in the Asian-Pacific region over the forecast period.

Sulfuric Acid Industry Overview

The global sulfuric acid market is highly fragmented. The top five players dominating the market are Mosaic, PhosAgro Group of Companies, Jiangxi Copper Group Co. Ltd, Yunnan Copper Co. Ltd, and Aurubis AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 High Demand for Sulfuric Acid in Phosphate-based Fertilizers

- 4.1.2 Growing Demand from Chemical and Pharmaceutical Industries

- 4.2 Restraints

- 4.2.1 Volatility In Raw Material Pricing

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Trade Analysis

- 4.6 Feedstock Analysis

- 4.7 Regional Production Capacities

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Raw Material Type

- 5.1.1 Elemental Sulfur

- 5.1.2 Pyrite Ore

- 5.1.3 Other Raw Material Types

- 5.2 End-user Industry

- 5.2.1 Fertilizer

- 5.2.2 Chemical and Pharmaceutical

- 5.2.3 Automotive

- 5.2.4 Petroleum Refining

- 5.2.5 Other End-user Industries (Pulp and Paper, Metal Processing)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aarti Industries Limited

- 6.4.2 Aurubis AG

- 6.4.3 Bodal Chemicals Ltd

- 6.4.4 Boliden Group

- 6.4.5 Hindustan Zinc

- 6.4.6 Jiangxi Copper Group Co. Ltd

- 6.4.7 KANTO KAGAKU

- 6.4.8 Nouryon

- 6.4.9 Panoli Intermediates India Private Limited

- 6.4.10 PhosAgro Group of Companies

- 6.4.11 PVS

- 6.4.12 Mosaic

- 6.4.13 WeylChem International GmbH

- 6.4.14 Yunnan Copper Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Use of Oleum in Medical and Other Industries

電子級硫酸市場:依純度等級、依應用分類 - 2024-2030 年全球預測

電子級硫酸市場:依純度等級、依應用分類 - 2024-2030 年全球預測 2024年硫酸全球市場報告

2024年硫酸全球市場報告 全球硫酸市場預測(至2030年)

全球硫酸市場預測(至2030年) 硫酸全球市場分析:工廠產能、產量、運營效率、需求和供應、最終用戶行業、銷售渠道、區域需求、外貿、公司份額(2015-2030 年)

硫酸全球市場分析:工廠產能、產量、運營效率、需求和供應、最終用戶行業、銷售渠道、區域需求、外貿、公司份額(2015-2030 年) 全球硫酸市場規模、佔有率和行業趨勢分析報告:2023-2030年按原料、用途和地區分類的展望和預測

全球硫酸市場規模、佔有率和行業趨勢分析報告:2023-2030年按原料、用途和地區分類的展望和預測 全球超高純硫酸市場

全球超高純硫酸市場 全球硫酸市場

全球硫酸市場 硫酸的全球市場 2023-2027

硫酸的全球市場 2023-2027 硫酸市場:依等級(10%、29-32%、62-70%)、用途(化學肥料、纖維、氫氟酸)- 2023-2030 年全球預測

硫酸市場:依等級(10%、29-32%、62-70%)、用途(化學肥料、纖維、氫氟酸)- 2023-2030 年全球預測 硫酸的全球市場報告2023年

硫酸的全球市場報告2023年