|

市場調查報告書

商品編碼

1445419

生物基聚合物 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Bio-based Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

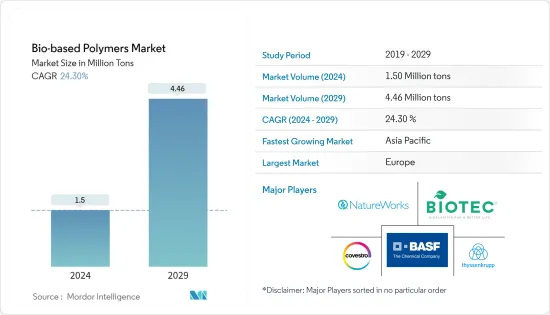

生物基聚合物市場規模預計到2024年為150萬噸,預計2029年將達到446萬噸,在預測期內(2024-2029年)CAGR為24.30%。

COVID-19 影響了生物基聚合物市場的成長。然而,疫情期間和疫情後對包裝食品和線上食品配送的需求增加推動了包裝塗料的消費,從而促使了生物基聚合物的消費。

短期內,對永續塑膠的需求不斷增加是推動市場需求的主要因素之一。

另一方面,生物塑膠的性能問題以及與石油基聚合物相比生物基聚合物的高價格預計將阻礙所研究市場的成長。

可生物分解塑膠的應用不斷增加可能會在未來帶來機會。

此外,包裝行業主導市場,預計在預測期內將成長。

歐洲主導了全球市場,最大的消費來自法國和英國等國家。

生物基聚合物市場趨勢

包裝產業需求不斷增加

- 包裝是生物基聚合物的最大市場之一。這些聚合物表現出優異的透明度和光澤度、耐食品脂肪和油性以及芳香屏障。此外,它們還為包裝提供剛性、扭曲保持力和適印性。

- 生物基聚合物主要用於超市的水果和蔬菜包裝、麵包袋和麵包盒、瓶子、信封、展示紙盒窗戶以及購物袋或手提袋等。例如,根據印度商務部的數據,2022會計年度印度新鮮蔬菜的出口額約為8.02億美元。加工蔬菜的出口額則接近4.25億美元。與2020年相比,新鮮蔬菜成長了10.87%,加工蔬菜成長了0.21%。因此,新鮮和加工蔬菜出口的增加預計將創造該國對生物基聚合物的需求。

- 歐洲和北美地區的生物基聚合物包裝市場正在快速成長。 FDA和相關組織在食品安全方面日益加強的干涉,很大程度上促進了可生物分解和食品級塑膠在飲料和零食消費中的使用。

- 連鎖餐廳和食品加工行業擴大採用可生物分解材料進行食品包裝。消費者在食品安全方面的意識也迅速提高,特別是在新興經濟體,因為一些塑膠被證明具有致癌性。

- 由於各個食品和安全組織不斷提高食品包裝標準,亞太地區、南美和中東等發展中地區的成長預計在不久的將來將會增加。

- 此外,可生物分解聚合物更易於處理,進一步增加了包裝行業對它們不斷成長的需求。

歐洲地區將主導市場

- 歐洲擁有最大的生物基聚合物佔有率並主導全球市場。

- 該地區的公眾意識和政府措施支持在購物袋、食品包裝、食品服務(餐具等)和有機廢物盒內襯等中使用可生物分解聚合物。

- 該地區的各個國家一直致力於提供更環保的包裝。這增加了包裝領域對聚乳酸的需求。

- 英國(UK)是歐洲領先的國家之一,對生物基聚合物包裝的需求一直在增加。對包裝產品永續性因素的更高認知,以及最近的政府舉措,正在為該國研究市場的成長創造有利的市場前景。

- 一次性塑膠的禁令是直接影響生物基聚合物包裝產品需求的主要因素之一。例如,2021年,英國政府宣布計劃在英格蘭禁止使用一次性塑膠餐具、盤子和聚苯乙烯杯子,以解決塑膠污染問題。

- 幾家現有供應商以及包裝行業的新創公司也主動在該國推廣生物基聚合物包裝。例如,2022 年 6 月,英國公司 Magical Mushroom Company 為其基於植物的永續包裝獲得了 340 萬歐元(331 萬美元)的資金。

- 目前,英國包裝業年銷售額達110億英鎊,員工超過85,000人。

- 歐盟 (EU) 正在努力實現 2050 年淨零排放目標,並透過實施《歐洲綠色協議》來應對日益嚴重的環境和永續發展危機。對更永續發展的社會的傾向與歐洲經濟的塑膠生產、使用和處置交織在一起。

- 對小尺寸包裝不斷成長的需求以及與生活方式改變相關的不斷成長的消費習慣預計將在預測期內推動對生物基聚合物的需求。

生物基聚合物產業概況

生物基聚合物市場本質上是部分整合的。市場上的一些主要參與者(排名不分先後)包括 BASF SE、Covestro AG、BIOTEC Biologische Naturverpackungen GmbH & Co. KG.、thyssenkrupp AG 和 NatureWorks LLC 等。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 促進要素

- 偏好環保聚合物以保護環境

- 多國對不可分解聚合物的法規

- 提高已開發國家和發展中國家的消費者意識

- 可生物分解聚合物的無毒性

- 限制

- 與石油基聚合物相比價格較高

- 低收入國家的意識低下

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第 5 章:市場區隔

- 類型

- 澱粉基塑膠

- 聚乳酸 (PLA)

- 聚羥基鏈烷酸酯 (PHA)

- 聚酯(PBS、PBAT 和 PCL)

- 纖維素衍生物

- 應用

- 農業

- 紡織品

- 電子產品

- 包裝

- 衛生保健

- 其他應用

- 地理

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 世界其他地區

- 巴西

- 沙烏地阿拉伯

- 世界其他地區

- 亞太

第 6 章:競爭格局

- 併購、合資、合作與協議

- 市佔率(%)**/排名分析

- 領先企業採取的策略

- 公司簡介

- BASF SE

- Biologische Naturverpackungen GmbH & Co. KG.

- Cardia Bioplastics

- Covestro AG

- Corbion

- Cortec Group Management Services, LLC

- DuPont de Nemours, Inc.

- FKuR

- FP International

- Innovia Films

- Merck KGaA

- YIELD10 BIOSCIENCE, INC. (Metabolix Inc.)

- NatureWorks LLC

- Novamont SpA

- Rodenburg Biopolymers

- SHOWA DENKO KK

- thyssenkrupp AG

第 7 章:市場機會與未來趨勢

- 生物分解塑膠的應用不斷增加

- 加強藥物傳輸研究

- 新興國家不斷加強的法規

The Bio-based Polymers Market size is estimated at 1.5 Million tons in 2024, and is expected to reach 4.46 Million tons by 2029, growing at a CAGR of 24.30% during the forecast period (2024-2029).

COVID-19 impacted the bio-based polymer market's growth. However, the increased demand for packaged food and online food deliveries during the pandemic and post-pandemic propelled the consumption of packaging coatings, which resulted in the consumption of bio-based polymers.

Over the short term, increasing demand for sustainable plastics is one of the major factors driving market demand.

On the flip side, the performance issue with bioplastics and the high prices associated with bio-based polymers compared to petroleum-based polymers are expected to hinder the growth of the market studied.

The increasing applications of biodegradable plastics are likely to present an opportunity in the future.

Moreover, the packaging industry dominates the market and is expected to grow during the forecast period.

Europe dominated the market across the world, with the largest consumption coming from countries such as France and the United Kingdom.

Bio-based Polymers Market Trends

Increasing Demand from Packaging Industry

- Packaging is one of the largest markets for bio-based polymers. These polymers exhibit excellent clarity and gloss, resistance to food fats and oils, and an aroma barrier. Additionally, they also provide stiffness, twist retention, and printability to the packaging.

- Bio-based polymers are mostly used in fruit and vegetable packaging in supermarkets, for bread bags and bakery boxes, bottles, envelopes, display carton windows, and shopping or carrier bags, among others. For instance, according to the Department of Commerce (India), the export value of fresh vegetables from India amounted to about USD 802 million in the fiscal year 2022. For processed vegetables, the value stood at nearly USD 425 million in the same year, which shows an increase of 10.87% from the fresh vegetable segment and 0.21% from processed vegetables compared with 2020. Therefore, an increase in the exports of fresh and processed vegetables is expected to create demand for bio-based polymers in the country.

- The bio-based polymer market for packaging is growing rapidly in the European and North American regions. The increasing intervention of the FDA and related organizations in terms of food safety is largely promoting the usage of biodegradable and food-grade plastics for beverage and snack consumption.

- The restaurant chains and food processing industries are increasingly adapting biodegradable materials for food packaging. Consumer awareness is also rising rapidly, especially in emerging economies, in terms of food safety, as some plastics are proven carcinogenic.

- The growth in developing regions, like Asia-Pacific, South America, and the Middle East, is expected to increase in the near future due to the improving food packaging standards of various food and safety organizations.

- Moreover, the higher ease of disposing of biodegradable polymers has further added to their growing demand from the packaging industry.

Europe Region to Dominate the Market

- Europe holds the largest share of bio-based polymers and dominates the global market.

- Public awareness and government initiatives in the region have supported the use of biodegradable polymers in carrier bags, food packaging, food services (cutlery, etc.), and organic waste caddy liners, among others.

- Various countries in the region have been focusing on offering more eco-friendly packaging. This has increased the demand for polylactic acid in the packaging sector.

- The United Kingdom (UK) is among the leading countries in Europe, where the demand for bio-based polymer packaging has been increasing. The higher awareness about the sustainability factors of packaging products, along with recent government initiatives, are creating a favorable market scenario for the growth of the studied market in the country.

- The ban on single-use plastics is among the primary factors that will directly impact the demand for bio-based polymer packaging products. For instance, in 2021, the UK government announced plans to ban single-use plastic cutlery, plates, and polystyrene cups in England to tackle plastic pollution.

- Several existing vendors, as well as startups operating in the packaging industry, are also taking the initiative to promote bio-based polymer packaging in the country. For instance, in June 2022, Magical Mushroom Company, a UK-based company, secured funding of EUR 3.4 million (USD 3.31 million) for its plant-based sustainable packaging.

- Currently, the packaging sector in the United Kingdom has annual sales of GBP 11 billion, and it employs more than 85,000 people.

- The European Union (EU) is working towards the 2050 net-zero emissions goal and tackling the increasing environmental and sustainability crises by implementing the European Green Deal. The inclination towards a more sustainable society is intertwined with the European economy's production, use, and disposal of plastic.

- The growing need for small-size packaging and the growing consumption habits associated with the change in lifestyles are anticipated to propel the demand for bio-based polymers over the forecast period.

Bio-based Polymers Industry Overview

The bio-based polymer market is partially consolidated by nature. Some of the major players in the market (not in any particular order) include BASF SE, Covestro AG, BIOTEC Biologische Naturverpackungen GmbH & Co. KG., thyssenkrupp AG, and NatureWorks LLC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Preference toward Eco-friendly Polymers to Preserve Environment

- 4.1.2 Regulation on Non-degradable Polymers in Many Countries

- 4.1.3 Increasing Consumer Awareness in Developed and Developing Nations

- 4.1.4 Non-toxic Nature of Biodegradable Polymers

- 4.2 Restraints

- 4.2.1 Higher Price Compared to Petroleum-based polymers

- 4.2.2 Low Awareness in Low Income Countries

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Starch-based Plastics

- 5.1.2 Poly Lactic Acid (PLA)

- 5.1.3 PolyHydroxy Alkanoates (PHA)

- 5.1.4 Polyesters (PBS, PBAT, and PCL)

- 5.1.5 Cellulose Derivatives

- 5.2 Application

- 5.2.1 Agriculture

- 5.2.2 Textile

- 5.2.3 Electronics

- 5.2.4 Packaging

- 5.2.5 Healthcare

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of World

- 5.3.4.1 Brazil

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 Rest of the World

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.3 Cardia Bioplastics

- 6.4.4 Covestro AG

- 6.4.5 Corbion

- 6.4.6 Cortec Group Management Services, LLC

- 6.4.7 DuPont de Nemours, Inc.

- 6.4.8 FKuR

- 6.4.9 FP International

- 6.4.10 Innovia Films

- 6.4.11 Merck KGaA

- 6.4.12 YIELD10 BIOSCIENCE, INC. (Metabolix Inc.)

- 6.4.13 NatureWorks LLC

- 6.4.14 Novamont SpA

- 6.4.15 Rodenburg Biopolymers

- 6.4.16 SHOWA DENKO K.K.

- 6.4.17 thyssenkrupp AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Applications of Bio-degradable Plastics

- 7.2 Increasing Research in Drug Delivery

- 7.3 Rising Regulations in Emerging Countries

按類型(聚乙烯(PE)、聚醯胺(PA)、聚乳酸(PLA)、聚對苯二甲酸乙二酯(PET)等)、應用(包裝、紡織、汽車、工業、農業等)的生物基聚合物市場報告,以及地區 2024-2032

按類型(聚乙烯(PE)、聚醯胺(PA)、聚乳酸(PLA)、聚對苯二甲酸乙二酯(PET)等)、應用(包裝、紡織、汽車、工業、農業等)的生物基聚合物市場報告,以及地區 2024-2032 電氣和電子市場中的生物聚合物,按類型、按應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

電氣和電子市場中的生物聚合物,按類型、按應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 生物聚合物全球市場規模、佔有率和趨勢分析報告:按最終用途、產品和地區分類的展望和預測,2023-2030年

生物聚合物全球市場規模、佔有率和趨勢分析報告:按最終用途、產品和地區分類的展望和預測,2023-2030年 可氧分解生物聚合物市場:按生物聚合物類型、製程和應用分類 - 2024-2030 年全球預測

可氧分解生物聚合物市場:按生物聚合物類型、製程和應用分類 - 2024-2030 年全球預測 蓖麻油基生物聚合物市場:按聚合物類型、型態和最終用戶分類 - 2024-2030 年全球預測

蓖麻油基生物聚合物市場:按聚合物類型、型態和最終用戶分類 - 2024-2030 年全球預測 醫用生物聚合物市場:按類型、來源、應用分類 - 2023-2030 年全球預測

醫用生物聚合物市場:按類型、來源、應用分類 - 2023-2030 年全球預測 生物聚合物市場規模、佔有率和趨勢分析報告:2024-2030 年按產品、最終用途、應用、地區和細分市場進行的預測

生物聚合物市場規模、佔有率和趨勢分析報告:2024-2030 年按產品、最終用途、應用、地區和細分市場進行的預測 亞太地區蓖麻油基生物聚合物市場:2022-2031

亞太地區蓖麻油基生物聚合物市場:2022-2031 電氣和電子市場中的生物聚合物 - 2018-2028 年全球行業規模、佔有率、趨勢、機會和預測(按類型、按應用、按地區、競爭)

電氣和電子市場中的生物聚合物 - 2018-2028 年全球行業規模、佔有率、趨勢、機會和預測(按類型、按應用、按地區、競爭) 生物聚合物薄膜市場:按原料、產品、技術和最終用戶分類 - 全球預測 2023-2030

生物聚合物薄膜市場:按原料、產品、技術和最終用戶分類 - 全球預測 2023-2030