|

市場調查報告書

商品編碼

1444702

藥品包裝 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

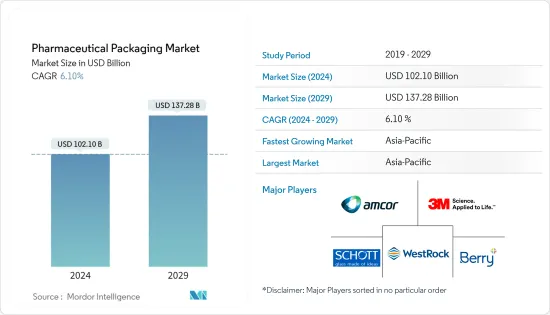

2024年藥品包裝市場規模預估為1,021.0億美元,預估至2029年將達到1,372.8億美元,在預測期間(2024-2029年)CAGR為6.10%。

主要亮點

- 全球製藥業不斷發展,對治療傳染性和非傳染性疾病的包裝產生了需求。因此,藥品製造中對包裝的需求不斷成長,因為它可以保護藥品免受損壞、生物污染和外部影響。

- 藥品需求的增加與產業技術進步有關,並直接創造了對瓶子、小瓶和其他包裝解決方案的需求。此外,對注射劑的需求不斷成長正在推動製藥業玻璃瓶的成長。對腫瘤藥物和其他高效藥物(例如抗體偶聯物和速效類固醇)的強勁需求以及人均藥品支出的增加預計將成為關鍵的成長動力。

- 全球醫藥產品的需求情勢支持了包裝產業的創收,並預計在預測期內將持續下去。總體而言,隨著藥品包裝的持續擴張和研發,預計藥品包裝市場將保持穩定成長。因此,預計需求在預測期內將出現巨大成長。

- 塑膠包裝產業面臨聚合物成本上漲,使得塑膠更加昂貴。此外,烏克蘭和俄羅斯之間的戰爭再次推高了價格。塑膠及塑膠製品的需求量逐年增加。供應跟不上需求的成長也是推動聚合物價格上漲的因素之一,預計將阻礙市場成長。

- 由於COVID-19的傳播,預計市場將大幅成長。受疫情影響,消費者轉向網上購物。 COVID-19 大流行對發展中國家和已開發國家的包裝材料擴張造成了沉重打擊。然而,對無菌藥品包裝的強勁需求鼓勵了對該領域的投資。此外,業內人士預計醫療保健產業對包裝技術將表現出強勁的需求。

藥品包裝市場趨勢

塑膠包裝佔有重要的市場佔有率

- 塑膠是最受歡迎的藥品包裝材料之一,因為它更適用、耐用、靈活且永續。藥品包裝採用由各種材料製成的塑膠瓶,包括聚氯乙烯、聚乙烯、聚丙烯和聚苯乙烯。該行業使用透明、耐用、輕質的塑膠來儲存和銷售。

- 塑膠用於包裝泡殼包裝、小袋、預填充注射器和吸入器、注射液袋和瓶子。藥品包裝中使用的材料需要具有化學惰性、水蒸氣滲透性低且易於處理。此外,包裝材料與藥品和生物製劑直接接觸,因此需要遵守監管機構的嚴格規定。塑膠和聚合物滿足這些要求;因此,它常用於藥品包裝。

- 藥品包裝瓶由防兒童開啟的瓶蓋和封口組成。美國FDA要求藥用塑膠製造商在產品標籤上突出顯示“兒童安全包裝”,以供消費者評估。對兒童安全包裝的需求不斷成長是預測期內推動醫藥塑膠包裝市場的因素之一。

- 作為利用藥品包裝的一部分,公司專注於擴大業務。例如,2022 年 6 月,Constantia Flexibles 推出了 Perpetua Alta,這是一種面向製藥市場的新型聚丙烯單一材料。這種單聚合物解決方案取代了化學成分產品(例如液體和凝膠藥物組合物)的多組分包裝。此外,德國實驗室 Cyclos-HTP 的獨立認證確認材料回收率高達 96%,具體取決於最終材料成分。這些創新推動了醫藥包裝市場中塑膠材料的發展。

- 此外,通常用作主要包裝材料的聚氯乙烯和 PVDC(聚偏二氯乙烯)可以保護藥品免受氧氣和異味、濕氣、水蒸氣穿透、污染和細菌的影響。這使得 PVC 和 PVDC 成為泡殼包裝的首選材料。它們卓越的感官品質確保包裝食品和藥物的風味不受影響。 PVC 單晶薄膜耐陽光和紫外線,可在預測期內阻止生產和分銷過程中細菌的傳播,從而起到防止污染的屏障作用。

亞太地區將佔據主要佔有率

- 中國醫藥產業的強勁成長為該國的醫藥包裝公司創造了龐大的商機。對於公司來說,尋找滿足藥品包裝市場新興需求的包裝概念現在變得至關重要。

- 中國政府加速醫學體制轉型的政策預計將促進醫藥包裝產業的發展。此外,中國正積極升級醫藥包裝設施與材料,以實現醫藥產品多元化,為醫藥包裝企業帶來新的機會。

- 在發展中經濟體製藥業的成長和醫療保健服務改善的推動下,日本藥品包裝市場的前景看好。在這個市場中,塑膠、玻璃、紙張和鋁箔是主要的材料類型。直接影響藥品包裝產業動態的新興趨勢包括對環保包裝的需求不斷成長、奈米包裝的使用增加以及吹灌封技術的採用增加。

- 印度的藥品包裝產業多年來一直在大幅成長。由於創新和新興治療方法,製藥業的這一領域還有進一步成長的空間。 COVID-19 大流行讓人們重新認知到高效包裝和分銷產品的必要性。人們期望更快地製造和分銷產品,甚至包括包裝。包裝公司將面臨新的壓力,需要開發解決方案,以加快速度並增加需求。

- 韓國是亞洲成長最快的製藥地區之一,正成為全球醫療保健創新的重要貢獻者。在過去幾年中,它極大地推進了新藥研究和開發。特別是在過去幾年中,韓國在全球製藥和生技領域的新藥研發能力不斷增強。

- 亞太其他地區的範圍包括印尼、澳洲、新加坡、泰國、馬來西亞等多個國家。該市場是由國際合作夥伴關係的激增、生物學名藥、成品製劑出口的擴大以及強勁的學名藥市場推動的。

醫藥包裝行業概況

藥品包裝市場現有參與者之間的競爭非常激烈。該市場因 Amcor PLC、Schott AG、WestRock Company、Berry Global、Aptar Group Inc. 等多家主要參與者的存在而變得分散。公司正在透過產品發布、合作和投資來擴展業務。

- 2023 年 2 月:肖特在美國開設了第一家工廠,以擴大其診斷和生命科學產品的能力和製造能力。投資數百萬美元在亞利桑那州鳳凰城建設新工廠,將致力於生產客製化 DNA 和蛋白質生物感測器以及玻璃、半導體和聚合物微流體消耗設備上的其他微陣列。

- 2022 年 5 月:CCL Industries Inc. 宣布計劃擴建德國萊比錫附近的 Innovia 業務部門。一條新的 8 m 寬多層共擠生產線將生產高度工程化的薄規格標籤薄膜,以滿足永續發展驅動的對減少樹脂含量材料不斷成長的需求。這項新技術是標籤薄膜獨有的,年產能為 36,000 噸,能源效率一流。生產將於 2024 年下半年開始,大部分資本將在明年投入。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- COVID-19 對市場影響的評估

第 5 章:市場動態

- 市場促進因素

- 包裝監管標準和假冒偽劣產品的嚴格規範

- 奈米技術對創新和新一代包裝解決方案的影響

- 市場課題

- 供應商議價能力導致原物料成本波動

第 6 章:市場區隔

- 依材質

- 塑膠

- 玻璃

- 其他材料

- 依產品類型

- 瓶子

- 注射器

- 小瓶和安瓿

- 管

- 瓶蓋和瓶蓋

- 標籤

- 其他產品類型

- 依地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 北美洲

第 7 章:競爭格局

- 公司簡介

- Amcor PLC

- 3M Company

- Schott AG

- WestRock Company

- Berry Global Group Inc.

- McKesson Corporation

- AptarGroup Inc.

- Klockner Pentaplast Group

- CCL Industries Inc.

- FlexiTuff International Ltd

- Gerresheimer AG

- West Pharmaceutical Services Inc.

- Becton, Dickinson and Company

- Vetter Pharma International GmbH

- Catalent Inc.

- WL Gore & Associates Inc.

- Nipro Corporation

第 8 章:投資分析

第 9 章:市場機會與未來趨勢

The Pharmaceutical Packaging Market size is estimated at USD 102.10 billion in 2024, and is expected to reach USD 137.28 billion by 2029, growing at a CAGR of 6.10% during the forecast period (2024-2029).

Key Highlights

- The pharmaceutical industry is increasing worldwide, creating a need for packaging to treat communicable and non-communicable diseases. Therefore, the demand for packaging in pharmaceutical manufacturing is growing as it protects pharmaceuticals from damage, biological contamination, and external influences.

- Increased demand for pharmaceuticals is associated with technological advancements in the industry and directly creates demand for bottles, vials, and other packaging solutions. Additionally, the growing demand for injectables is driving the growth of glass vials in the pharmaceutical industry. Strong demand for oncology and other high-potency drugs (such as antibody conjugates and fast-acting steroids) and increasing per capita spending on pharmaceuticals are expected to be key growth drivers.

- The global demand scenario for pharmaceutical products has supported revenue generation in the packaging sector and is expected to continue during the forecast period. Overall, the pharmaceutical packaging market is projected to register a steady growth rate coupled with ongoing expansion and research and development to improve pharmaceutical packaging. Thus, demand is anticipated to witness enormous growth over the forecast period.

- The plastic packaging industry faces rising polymer costs, making plastics more expensive. Additionally, the war between Ukraine and Russia has pushed prices up again. The demand for plastics and plastic products is increasing year by year. The lack of supply keeping up with the increase in demand is also one factor driving higher polymer prices, expected to hinder the market growth.

- Owing to the spread of COVID-19, the market is expected to grow significantly. Due to the pandemic, customers shifted toward online purchasing. The COVID-19 pandemic hit hard on expanding packaging materials in developing and developed countries. However, strong demand for sterilized pharmaceutical packaging encouraged investment in the landscape. Moreover, industry players expect the healthcare industry to show strong demand for packaging technology.

Pharmaceutical Packaging Market Trends

Plastic Packaging Holds a Significant Market Share

- Plastic is one of the most popular materials for pharmaceutical packaging as it is more applicable, durable, flexible, and sustainable. Pharmaceutical packaging utilizes plastic bottles constructed from various materials, including polyvinyl chloride, polyethylene, polypropylene, and polystyrene. The industry uses transparent, durable, lightweight plastic to store and market.

- Plastics are used for packaging blister packs, sachets, prefilled syringes and inhalers, parenteral solution pouches, and bottles. Materials used in pharmaceutical packaging need to be chemically inert, have low permeability to water vapor, and are easy to handle. In addition, packaging materials come in direct contact with pharmaceuticals and biological agents and hence need to comply with strict regulations from regulatory authorities. Plastics and polymers meet these requirements; therefore, it is often used for pharmaceutical packaging.

- Bottles for pharmaceutical packaging consist of child-resistant caps and closures. The US FDA requires pharmaceutical plastic manufacturers to highlight "child-resistant packaging" on product labels for consumer evaluation. Rising demand for child-safe packaging is one of the factors driving the pharmaceutical plastic packaging market during the forecast period.

- Companies are focused on expanding their business as part of leveraging pharmaceutical packaging. For instance, in June 2022, Constantia Flexibles introduced Perpetua Alta, a new polypropylene-based mono-material for the pharmaceutical market. This mono-polymer solution replaces multi-component packaging for chemically assertive products, such as liquid and gel pharmaceutical compositions. In addition, independent certification by the German laboratory Cyclos-HTP confirms up to 96% material recovery, depending on the final material composition. Such innovations drive the plastic materials in the pharmaceutical packaging market.

- Moreover, polyvinyl chloride and PVDC (polyvinylidene chloride), commonly used as principal packaging materials, protect pharmaceutical items from oxygen and odor, moisture, water vapor transmission, contamination, and bacteria. This makes PVC and PVDC the preferred materials for blister packing. Their superior organoleptic qualities ensure that the flavor of packaged food and medications remains unaffected. PVC mono films are sunlight and UV-ray-resistant and serve as a barrier against contamination by halting the spread of germs during production and distribution over the forecast period.

Asia-Pacific to Occupy Major Share

- The robust growth of the Chinese pharmaceutical sector creates significant business opportunities for the country's pharmaceutical packaging companies. It is now becoming critical for companies to look for packaging concepts that meet emerging needs in the pharmaceutical packaging market.

- The Chinese government's policies to accelerate the transformation of the country's medical regime are expected to promote the development of the pharmaceutical packaging sector. Furthermore, China is actively upgrading its pharmaceutical packaging facilities and materials and diversifying its pharmaceutical products, bringing new opportunities to pharmaceutical packaging firms.

- The future of the pharmaceutical packaging market in Japan looks good, driven by the pharmaceutical industry's growth and improving healthcare services in developing economies. In this market, plastic, glass, paper, and aluminum foil are the main material types. Emerging trends directly impacting the dynamics of the pharmaceutical packaging industry include rising demand for eco-friendly packaging, increasing use of nano-enabled packaging, and increasing adoption of blow-fill-seal technology.

- The pharmaceutical packaging industry in India has been experiencing substantial growth for several years. Due to innovations and emerging treatments, there is room for further growth in this section of the pharma industry. The COVID-19 pandemic has brought a new awareness of the need to package and distribute products efficiently. There will be expectations to manufacture and distribute products quicker, right down to the packaging. Packaging companies will face new pressures to develop solutions to get things moving faster and increase demand.

- South Korea is one of the fastest-growing pharma regions in Asia, emerging as a critical contributor to global healthcare innovation. It has tremendously advanced new drug research and development in the last few years. Especially during the past few years, Korea has developed new drug R&D capabilities in the global pharmaceutical and biotech landscape.

- The scope of the Rest of the Asia-Pacific region includes multiple countries, such as Indonesia, Australia, Singapore, Thailand, and Malaysia. The market is driven by the surge of international partnerships, biosimilars, an expansion in the export of finished formulations, and a robust generics market.

Pharmaceutical Packaging Industry Overview

The rivalry among the existing players is intense in the pharmaceutical packaging market. The market is fragmented with the presence of various major players, such as Amcor PLC, Schott AG, WestRock Company, Berry Global, Aptar Group Inc., and more. Companies are expanding their business through product launches, collaborations, and investments.

- February 2023: Schott opened its first facility in the United States to expand its capabilities and manufacturing capacity for diagnostics and life sciences products. The construction of a new facility in Phoenix, Arizona, with a multimillion-dollar investment, will be dedicated to producing custom DNA and protein biosensors and other microarrays on glass, semiconductors, and polymer microfluidic consumable devices.

- May 2022: CCL Industries Inc. announced plans for an expansion at its Innovia business unit near Leipzig in Germany. A new 8 m wide multi-layer co-extrusion line will manufacture highly engineered thin gauge label films to meet the rising, sustainability-driven demand for materials with reduced resin contents. With a capacity of 36,000 ton annually and best-in-class energy efficiency, the new technology is exclusive to label films. Production will begin in the second half of 2024, with most of the capital invested in the next year.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Assessment of Impact of the COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Regulatory Standards on Packaging and Stringent Norms against Counterfeit Products

- 5.1.2 Impact of Nanotechnology due to Innovative and New- generation Packaging Solutions

- 5.2 Market Challenges

- 5.2.1 Fluctuations in Raw Material Cost Due to Suppliers Bargaining Power

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastics

- 6.1.2 Glass

- 6.1.3 Other Materials

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Syringes

- 6.2.3 Vials and Ampoules

- 6.2.4 Tubes

- 6.2.5 Caps and Closures

- 6.2.6 Labels

- 6.2.7 Other Product Types

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East & Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 3M Company

- 7.1.3 Schott AG

- 7.1.4 WestRock Company

- 7.1.5 Berry Global Group Inc.

- 7.1.6 McKesson Corporation

- 7.1.7 AptarGroup Inc.

- 7.1.8 Klockner Pentaplast Group

- 7.1.9 CCL Industries Inc.

- 7.1.10 FlexiTuff International Ltd

- 7.1.11 Gerresheimer AG

- 7.1.12 West Pharmaceutical Services Inc.

- 7.1.13 Becton, Dickinson and Company

- 7.1.14 Vetter Pharma International GmbH

- 7.1.15 Catalent Inc.

- 7.1.16 W. L. Gore & Associates Inc.

- 7.1.17 Nipro Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

藥品包裝設備市場評估:依水平、自動化、配方和地區劃分的機會和預測(2017-2031)

藥品包裝設備市場評估:依水平、自動化、配方和地區劃分的機會和預測(2017-2031) 全球藥品包裝市場規模、佔有率和成長分析:按產品和材料 - 產業預測(2024-2031)

全球藥品包裝市場規模、佔有率和成長分析:按產品和材料 - 產業預測(2024-2031) 2024 年益生菌包裝全球市場報告

2024 年益生菌包裝全球市場報告 全球藥品活性與智慧包裝市場 2024-2028

全球藥品活性與智慧包裝市場 2024-2028 2024年藥品包裝設備全球市場報告

2024年藥品包裝設備全球市場報告 配藥製藥包裝機世界市場報告 2024

配藥製藥包裝機世界市場報告 2024 全球藥品包裝市場:依原料、類型、藥物輸送、地區 - 預測(至 2028 年)

全球藥品包裝市場:依原料、類型、藥物輸送、地區 - 預測(至 2028 年) 全球藥品包裝市場 - 2024年至2029年預測

全球藥品包裝市場 - 2024年至2029年預測 益生菌包裝市場預測至 2030 年:按包裝類型、材料類型、型態、分銷管道、最終用戶和地區進行的全球分析

益生菌包裝市場預測至 2030 年:按包裝類型、材料類型、型態、分銷管道、最終用戶和地區進行的全球分析 永續藥品包裝市場報告:2030 年趨勢、預測與競爭分析

永續藥品包裝市場報告:2030 年趨勢、預測與競爭分析