|

市場調查報告書

商品編碼

1441570

海底佈線系統 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029 年)Submarine Cabling Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

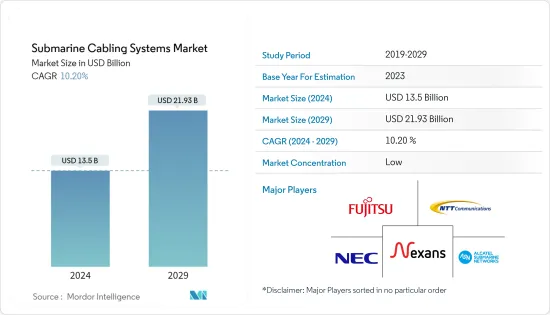

海底佈線系統市場規模預計到2024年為135億美元,預計2029年將達到219.3億美元,在預測期內(2024-2029年)CAGR為10.20%。

主要亮點

- 海底電纜系統通常利用光纖電纜來傳輸資料和電力。這些系統鋪設在海底,連接不同地點的電纜登陸站(CLS),在廣闊的海洋上傳輸電信和電力訊號。海底佈線系統在世界各國之間提供高度可靠、安全和高容量的電信連結。

- 推動海底佈線系統市場成長的主要因素之一是高速網路基礎設施投資的增加。此外,全球資料生成和傳輸的持續擴展預計將顯著促進市場成長。因此,預計許多網路骨幹業者將在整個預測期內投資海底佈線系統市場。

- 隨著發展中國家網路存取的擴展,下一階段的網路改進可能會集中在全球新興市場。因此,包括政府實體在內的許多企業都將海底佈線系統市場視為利潤豐厚的前景。此外,行動寬頻採用率的快速成長極大地促進了產業成長。

- 此外,由於多種因素,包括可支配收入的增加、5G的引入以及電信基礎設施的進步,全球對智慧型手機的需求一直在成長。愛立信報告稱,2021 年全球智慧型手機用戶數量為 62.6 億,預計到 2027 年將達到 76.9 億。預計這些趨勢仍將是研究市場成長的關鍵驅動力。

- 海底電纜對全球經濟和電信至關重要,其運作環境越來越容易受到地緣政治、物理和網路威脅,包括民族國家的破壞和間諜活動。據官方消息稱,海底通訊電纜日益成為網路威脅行為者的目標,其事件可能造成全球網路嚴重中斷,進一步影響研究市場的成長。

- 在新冠肺炎 (COVID-19) 疫情期間,由於封鎖,大量屋主開始使用自動機器人等先進電子設備,對老年家庭成員進行無接觸清潔和家庭護理,從而增加了網路消費。這場大流行也促使更廣泛人群的消費模式發生重大變化,使他們比以往任何時候都對新技術更加開放。這項轉變預計將推動後疫情時期海底電纜網路的投資。

海底佈線系統市場趨勢

乾燥植物產品推動市場成長

- 幹電站包括陸地上的海底電纜網路段,從海灘沙井延伸至電纜登陸站。這包括供電設備 (PFE)、海底線路終端設備、網路管理系統和陸地電纜段。

- 為了滿足客戶對寬頻服務和增強網路效能的需求,全球電信流量正在迅速成長。例如,根據國際電信聯盟的數據,2022 年歐洲每 100 名居民的固定寬頻用戶數為 35.4 人,美洲為 25.4 人。因此,對海底電信系統的需求正在穩步成長,不僅是為了建造新的電纜系統,而且是為了增加現有電纜系統的容量。多家公司正在開發利用光學技術的海底線路終端設備(SLTE),以滿足這種不斷成長的需求。

- 例如,2023 年 10 月,Google Equiano 電纜的聖赫勒拿分支啟用,代表該島首次透過高速海底光纜連接到網路。到2023年6月,此電纜海底線路終端設備的安裝和整合已經完成,促使當地陸地光纖網路的工作開始。

- 陸地電纜段將海底線路終端連接到電纜登陸站的供電設備和其他系統。網路管理系統作為統一平台管理海纜系統中的所有設備,在日常維護和運作期間監控濕廠、饋電設備(PFE)、開放式電纜接入設備(OCAE)和網路運作。

- 乾燥植物產品通常經過精心設計,能夠承受惡劣的海岸環境條件,包括強風、鹽霧和極端溫度。他們的設計優先考慮高可靠性,因為乾電站的任何中斷都可能導致整個海底電纜系統的服務中斷。

跨太平洋航線將佔據重要市場佔有率

- 在跨太平洋地區,第一個跨太平洋海底電纜系統(TPC-1(Trans-Pacific Cable 1))於 1960 年代投入營運。它是一條海底同軸電纜,最初只有 128 條電話線路容量,透過夏威夷連接日本、關島、夏威夷和美國大陸。此後,大量跨太平洋海底電纜系統不斷建設,顯著擴大了該地區的容量。

- 海底電纜處理全球 97% 以上的網路流量,反映出日常任務普遍依賴網路。網路連結全球人們的能力促使國際流量持續成長。亞太地區貢獻了全球約一半的網路流量,推動了對海底通訊電纜的需求。該地區某些國家缺乏這些系統,刺激了跨太平洋地區對更快網際網路服務的需求,從而促使世界銀行和亞洲開發銀行等組織為新的電纜系統提供資金。

- 2022 年 7 月,NTT Ltd Japan Corporation、三井物產、PC Landing Corp. 和 JA Mitsui Leasing, Ltd. 宣布成立一家新公司 Seren Juno Network(“Seren”),旨在建設和營運“JUNO”連接日本和美國的最廣泛的跨太平洋海底電纜系統。

- 此外,2022年8月,NEC公司透露,Seren Juno Network已選擇他們建造跨太平洋海底光纜“JUNO電纜系統”,連接美國加州與日本千葉縣和三重縣。這條電纜全長超過 10,000 公里,預計將於 2024 年完工。

- 該地區的主要國家,包括日本和澳洲等,認為海底電纜系統對其經濟成長至關重要,並正在增加對海底電纜網路的投資,從而在所研究的市場中創造機會。例如,2023 年 7 月,日本政府宣布了擴大數位基礎設施發展基金的計劃,以擴大連接日本與世界其他地區的海底電纜網路。

海底佈線系統產業概述

海底電纜系統市場擁有眾多主要參與者,包括 NTT Communications Corporation、Nexans SA、Fujitsu Ltd、NEC Corporation 和 Alcatel Submarine Network。這些公司參與合資企業、長期合作夥伴關係以及併購等策略性舉措,以促進收入成長並擴大其全球影響力。

2023年10月,NEC公司標誌著印尼Patara-2海底電纜網路的竣工和啟用。該網路由該國最大的數位電信供應商 PT Telkom Indonesia 擁有,是推進印尼各島嶼數位化工作的關鍵一步。

同樣,谷歌有限責任公司在同月透露了南太平洋連接計劃的計劃。這項措施需要實施兩條新的跨太平洋海底電纜——Honomoana 和 Tabua。這些電纜旨在顯著提高整個太平洋地區數位連接的可靠性和彈性。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買家的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭程度

- 產業價值鏈分析

- 宏觀趨勢對產業的影響

第 5 章:市場動態

- 市場促進因素

- 內容供應商對網路頻寬的需求不斷增加

- 增加新興地區的海底電纜連接

- 離岸風電場投資不斷增加

- 市場限制

- 資料隱私和本地化計劃

- 地緣政治緊張局勢限制了項目

第 6 章:市場區隔

- 依類型

- 乾燥植物產品

- 濕植物產品

- 依所有權類型

- 多重所有製

- 單一所有權制度

- 多邊開發銀行

- 依地理

- 跨太平洋

- 跨大西洋

- 美國 - 拉丁美洲

- 亞洲內部

- 歐洲 - 亞洲

- 歐洲 - 撒哈拉以南非洲

第 7 章:競爭格局

- 公司簡介

- Alcatel Submarine Networks

- NEC Corporation

- Nexans SA

- Fujitsu Ltd

- NTT Communications Corporation

- Google LLC

- SubCom LLC

- Sumitomo Electronics Industries Ltd

- JDR Cable Systems LLC

- PT Communication Cable System Indonesia Tbk

第 8 章:投資分析

第 9 章:市場的未來前景

The Submarine Cabling Systems Market size is estimated at USD 13.5 billion in 2024, and is expected to reach USD 21.93 billion by 2029, growing at a CAGR of 10.20% during the forecast period (2024-2029).

Key Highlights

- Submarine cable systems typically utilize optical fiber cables for transmitting both data and power. These systems are laid on the seabed, connecting cable landing stations (CLS) at different locations to carry telecommunication and power signals across vast expanses of the ocean. Submarine cabling systems offer highly reliable, secure, and high-capacity telecommunication links between countries worldwide.

- One primary factor driving the growth of the submarine cabling system market is the increased investment in high-speed internet infrastructure. Additionally, the continuous expansion in data generation and transmission globally is anticipated to significantly boost market growth. Consequently, numerous internet backbone operators are expected to invest in the submarine cabling system market throughout the forecast period.

- As Internet access expands in developing countries, the next phase of network improvement may focus on emerging markets worldwide. Consequently, many businesses, including government entities, perceive the submarine cabling system market as a lucrative prospect. Moreover, the rapid increase in mobile broadband adoption significantly contributes to industry growth.

- Furthermore, the global demand for smartphones has been on the rise due to various factors, including increasing disposable income, the introduction of 5G, and telecom infrastructure advancements. Ericsson reports that the global number of smartphone subscribers was 6.26 billion in 2021, predicted to reach 7.69 billion in 2027. These trends are expected to remain key drivers of the studied market's growth.

- Submarine cables, crucial to the global economy and telecommunications, operate in an environment increasingly exposed to geopolitical, physical, and cyber threats, including nation-state sabotage and spying. According to official sources, submarine communication cables are a growing target for cyber-threat actors, with incidents capable of causing substantial global internet disruption, further impacting the studied market's growth.

- During the COVID-19 period, a significant number of homeowners began implementing advanced electronic devices, such as autonomous robots, for contact-free cleaning and home care of elderly family members due to lockdowns, subsequently increasing internet consumption. The pandemic also led to a significant change in consumption patterns among broader populations, making them more open than ever to new technologies. This shift is expected to drive investments in the subsea cable network in the post-COVID period.

Submarine Cabling Systems Market Trends

Dry Plant Products to Drive the Market's Growth

- The dry plant comprises the subsea cable network segment on land, extending from the beach manhole to the cable landing station. This encompasses power feeding equipment (PFE), submarine line terminal equipment, network management systems, and land cable segments.

- Global telecommunications traffic is rapidly expanding in response to customer demands for broadband services and enhanced network performance. For instance, according to ITU, the number of fixed broadband subscriptions per 100 inhabitants was 35.4 in Europe in 2022 and 25.4 in the Americas. Consequently, the demand for submarine telecommunication systems is steadily increasing, not only for constructing new cable systems but also for augmenting the capacity of existing ones. Several companies are developing Submarine Line Terminal Equipment (SLTE) utilizing optical technologies to meet this rising demand.

- For instance, in October 2023, the Saint Helena branch of the Google Equiano cable was activated, representing the island's inaugural connection to the internet through high-speed subsea fiber optic cables. By June 2023, the installation and integration of the cable's Submarine Line Terminal Equipment had concluded, prompting the commencement of work on the local terrestrial fiber optic network.

- The land cable segments link the submarine line terminals to the power-feeding equipment and other systems at the cable landing station. The Network Management System serves as the unified platform managing all equipment in the submarine cable system, overseeing the wet plant, Power Feeding Equipment (PFE), Open Cable Access Equipment (OCAE), and network operations during routine maintenance and operation.

- Dry plant products are typically engineered to withstand harsh coastal environmental conditions, including high winds, salt spray, and extreme temperatures. Their design prioritizes high reliability, as any disruption to the dry plant can result in a service outage for the entire submarine cable system.

Trans-Pacific to Hold a Significant Market Share

- In the transpacific region, the first Trans-Pacific submarine cable system (TPC-1 (Trans-Pacific Cable 1)) operated during the 1960s. It was a submarine coaxial cable that began with a modest 128-phone line capacity, linking Japan, Guam, Hawaii, and the mainland United States via Hawaii. Since then, numerous transpacific submarine cable systems have continuously been constructed, significantly expanding the region's capacity.

- Submarine cables handle over 97% of global Internet traffic, reflecting the widespread reliance on the Internet for daily tasks. The Internet's capability to connect people globally has led to a continuous rise in international traffic. The Asia Pacific region contributes approximately half of the world's internet traffic, driving the demand for submarine communication cables. The lack of these systems in certain countries within this region has spurred the need for faster internet services in the Transpacific region, prompting funding from organizations like the World Bank and the Asia Development Bank for new cable systems.

- In July 2022, NTT Ltd Japan Corporation, Mitsui & Co. Ltd, PC Landing Corp., and JA Mitsui Leasing, Ltd. announced the formation of a new company, Seren Juno Network Co., Ltd. ("Seren"), established to construct and operate "JUNO," the most extensive trans-Pacific submarine cable system linking Japan and the United States.

- Moreover, in August 2022, NEC Corporation revealed that Seren Juno Network had selected them to build the trans-Pacific subsea fiber-optic cable, the "JUNO Cable System," connecting California in the United States with Chiba and Mie prefectures in Japan. This cable, spanning over 10,000 km, is projected to be completed by 2024.

- Key countries in the region, including Japan and Australia, among others, consider submarine cabling systems vital for their economic growth and are intensifying their investments in submarine cable networks, creating opportunities in the studied market. For instance, in July 2023, the Japanese government unveiled plans to augment the Digital Infrastructure Development Fund to expand the submarine cable networks linking Japan with the rest of the world.

Submarine Cabling Systems Industry Overview

The submarine cable systems market features various key players, including NTT Communications Corporation, Nexans SA, Fujitsu Ltd, NEC Corporation, and Alcatel Submarine Networks. These companies engage in collaborative ventures, long-term partnerships, and strategic initiatives like mergers and acquisitions to bolster revenue growth and expand their global presence.

In October 2023, NEC Corporation marked the completion and activation of the Patara-2 submarine cable network in Indonesia. This network, owned by PT Telkom Indonesia, the country's largest digital telecommunications provider, stands as a pivotal step in advancing digitization efforts across Indonesia's diverse islands.

Similarly, Google LLC revealed plans for the South Pacific Connect initiative during the same month. This initiative entails the implementation of two new transpacific subsea cables-Honomoana and Tabua. These cables aim to significantly enhance the reliability and resilience of digital connectivity across the Pacific region.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro-trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Internet Bandwidth from Content Providers

- 5.1.2 Increasing Submarine Cable Connectivity in Emerging Regions

- 5.1.3 Growing Investments in Offshore Wind Farms

- 5.2 Market Restraints

- 5.2.1 Data Privacy and Localization Initiatives

- 5.2.2 Geopolitical Tensions Limiting Projects

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Dry Plant Products

- 6.1.2 Wet Plant Products

- 6.2 By Ownership Type

- 6.2.1 Multiple Ownership System

- 6.2.2 Single Ownership System

- 6.2.3 Multilateral Development Banks

- 6.3 By Geography

- 6.3.1 Trans - Pacific

- 6.3.2 Trans - Atlantic

- 6.3.3 US - Latin America

- 6.3.4 Intra Asia

- 6.3.5 Europe - Asia

- 6.3.6 Europe - Sub-Saharan Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Alcatel Submarine Networks

- 7.1.2 NEC Corporation

- 7.1.3 Nexans SA

- 7.1.4 Fujitsu Ltd

- 7.1.5 NTT Communications Corporation

- 7.1.6 Google LLC

- 7.1.7 SubCom LLC

- 7.1.8 Sumitomo Electronics Industries Ltd

- 7.1.9 JDR Cable Systems LLC

- 7.1.10 PT Communication Cable System Indonesia Tbk