|

市場調查報告書

商品編碼

1439881

硝酸:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Nitric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

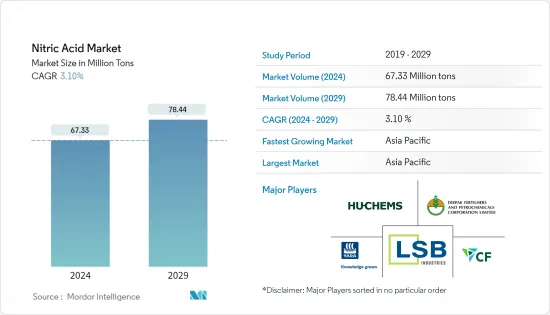

預計2024年硝酸市場規模為6,733萬噸,預計2029年將達到7,844萬噸,在預測期(2024-2029年)年複合成長率為3.10%。

由於新型冠狀病毒感染疾病(COVID-19)的爆發,世界各地實施了國家封鎖,製造活動和供應鏈中斷以及生產停頓對硝酸市場產生了負面影響。市場現已從疫情中恢復,並正在經歷顯著成長。

主要亮點

- 短期內,化肥和炸藥製造中對硝酸的需求不斷增加預計將推動市場成長。

- 然而,硝酸造成的健康危害可能會阻礙市場成長。

- 儘管如此,硝酸生產的技術發展和最近的政府激勵措施預計將在預測期內創造利潤豐厚的市場機會。

- 預計亞太地區將主導全球市場,最大消費來自中國、日本和印度等國家。

硝酸市場趨勢

化肥產業需求增加

- 80%以上的硝酸用於化學肥料生產。硝酸銨和硝酸銨鈣等肥料是由硝酸製成的。需要更多的耕地來滿足世界日益成長的糧食需求。因此,化肥需求不斷增加,預計全球化肥料產業在預測期內的年複合成長率將達到5%左右。

- 硝酸銨是一種常見的高效能氮基肥料,其總氮含量約為35%(以重量計)。此外,硝酸銨鈣 (CAN) 肥料的氮含量約為 25-28%。 CAN肥料用於提供氮以促進任何植物的生長。

- 硝酸銨鈣是透過在約 170°C 下混合熔融硝酸銨和碳酸鈣而生產的。它具有吸濕性,會吸收環境中的水分。因此,即使在沒有足夠水的土壤中,硝酸銨鈣也可以使用。

- 根據美國糧食及農業組織(FAO)預測,2022年全球化肥料需求預計將達到2,0092萬噸。

- 根據聯合國同業貿易地圖,2021年化肥出口額超過850億美元,與前一年同期比較成長約50%。 2021年,全球化肥出口達到十年來的最高水準。

- 據歐洲肥料協會稱,到2029/2030季節,歐盟氮肥的年消費量預計將達到1,060萬噸,而目前的平均消費量1,120萬噸。經過幾年的復甦,未來十年化肥年消費量預計將連續第四年下降,從而限制市場成長。

- 因此,上述因素可能在預測期內影響肥料應用硝酸市場。

亞太地區主導市場

- 亞太地區預計將成為硝酸生產的主要市場,因為包括中國、印度和韓國在內的亞太國家是最大的化肥生產國和消費國。

- 根據ITC貿易地圖,韓國是最大的硝酸出口國,2021年出口量為53.42萬噸。 2020年中國是第二大進口國,進口量為15.28萬噸,用於化肥、油墨、顏料、染料和化學製造業等各種最終用戶。

- 印度化肥協會數據顯示,2020-21年度化肥產品總產量為4,349萬噸,較2019-20年成長1.7%。 2020-2021年氮肥產量達1,374萬噸,2019-2020年小幅成長0.2%。

- 根據中國國家統計局數據,2021年糧食總合6.829億噸,比去年的6.5億噸增加2%。玉米種植面積較上年增加5%,產量增加4.6%。增加化肥的使用以提高生產力以滿足耕地面積的減少預計將推動該國的市場。

- 硝酸用作油墨、顏料和染料的原料,主要應用於紡織工業。根據工業和資訊化部(工信部)統計,2021年前9個月,中國紡織工業平穩成長,利潤總合達到1711億元人民幣(約合268億美元),與前一年同期比較% .我做到了。

- 硝酸用於生產三硝基甲苯 (TNT)、硝化纖維素和硝化甘油等炸藥,用於採礦應用。例如,2021年3月,印度煤炭有限公司(CIL)核准了32個新煤礦開採計劃,其中24個是現有計劃的擴建,其餘為待開發區。該計劃估計費用為 4,700 億印度盧比(約 56.7564 億美元),將擴大潛在市場。

- 因此,預計上述因素將在未來幾年對市場產生重大影響。

硝酸產業概況

硝酸市場本質上是分散的。研究的市場主要企業包括(排名不分先後)CF Industries Holdings Inc.、HUCHEMS、Yara、LSB INDUSTRIES 和 Deepak Fertilizers and Petrochemicals Corporation Ltd (DFPCL)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 擴大化肥領域的使用

- 炸藥製造需求增加

- 抑制因素

- 硝酸對健康造成的損害

- 環境法規政策

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭強度

- 貿易流量分析

- 成本分析

第5章市場區隔(市場規模、數量)

- 最終用戶產業

- 肥料

- 航太

- 油墨、顏料、染料

- 化學製造

- 霹靂

- 其他最終用戶產業(製藥、食品加工)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 墨西哥

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介

- BASF SE

- CF Fertilisers UK

- Deepak Fertilisers and Petrochemicals Corporation Ltd(DFPCL)

- Gujarat Narmada Valley Fertilizers &Chemicals Limited(GNFC)

- Hanwha Corporation

- HUCHEMS

- INEOS

- LSB INDUSTRIES

- MAXAMCORP HOLDING SL

- Mitsubishi Chemical Corporation

- Nutrien Ltd

- Sasol Ltd

- Sinopec Nanjing Chemical Industries Co. Ltd(China Petrochemical Corporation)

- Sumitomo Chemical Co. Ltd

- Yara

第7章市場機會與未來趨勢

- 硝酸生產的技術發展和政府近期激勵措施

The Nitric Acid Market size is estimated at 67.33 Million tons in 2024, and is expected to reach 78.44 Million tons by 2029, growing at a CAGR of 3.10% during the forecast period (2024-2029).

Due to the COVID-19 outbreak, nationwide lockdowns around the world, disruptions in manufacturing activities and supply chains, and production halts negatively impacted the nitric acid market. Currently, the market has recovered from the pandemic and is growing at a significant rate.

Key Highlights

- Over the short term, the increasing demand for nitric acid from fertilizer and explosives manufacturing is expected to drive the market's growth.

- However, health-related hazards caused by nitric acid are likely to hinder the growth of the market.

- Nevertheless, technological development in nitric acid manufacturing and recent government incentives are expected to create lucrative market opportunities over the forecast period.

- The Asia-Pacific region is expected to dominate the market, globally, with the largest consumption from countries such as China, Japan, and India.

Nitric Acid Market Trends

Increasing Demand from the Fertilizer Industry

- Over 80% of nitric acid is used in manufacturing fertilizers. Fertilizers, like ammonium nitrate and calcium ammonium nitrate, are produced from nitric acid. To meet the increasing global food demand, more arable land is required for cultivation. Hence, fertilizer demand is increasing, with the global fertilizer industry expected to witness a CAGR of about 5% during the forecast period.

- Ammonium nitrate is a popular, efficient nitrogen-based fertilizer with around 35% (by mass) of total nitrogen content. Moreover, calcium ammonium nitrate (CAN) fertilizer has a nitrogen content of ~25-28%. CAN fertilizer is used to supply nitrogen to advance the growth of any plant.

- Calcium ammonium nitrate is manufactured by mixing molten ammonium nitrate and calcium carbonate at a temperature of around 170°C. It is hygroscopic and can absorb moisture from the environment. Thus, calcium ammonium nitrate can be used in soil without sufficient water.

- According to the US Food and Agriculture Organization (FAO), the global demand for fertilizers was expected to reach 200.92 million tons in 2022.

- According to United Nations Comtrade and Trade Map, fertilizer exports were over USD 85 billion in 2021, representing a roughly 50% rise over the previous year's figures. In 2021, global fertilizer exports reached a decade high.

- According to the FERTILIZERS EUROPE, the annual nitrogen fertilizer consumption in the European Union is expected to reach 10.6 million tons by the 2029/2030 season, compared to the current average consumption of 11.2 million tons. After several years of recovery, annual fertilizer consumption over the next ten years is foreseen to decrease for the fourth consecutive year, thereby restricting the market growth.

- Thus, the above-mentioned factors are likely to affect the nitric acid market for fertilizer application during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to be the dominant market in nitric acid production, owing to the largest production and consumption of fertilizers in Asia-Pacific countries, including China, India, and South Korea.

- According to ITC Trade Map, South Korea is the largest exporter of nitric acid, with an exported quantity of 534.2 thousand ton in 2021. China is the second-largest importer in 2020, with an imported quantity of 152.8 thousand ton for various end-user industries like fertilizers, inks, pigments, dyes, and chemical manufacturing.

- According to the Fertilizer Association of India, the production of total fertilizer products stood at 43.49 million MT during 2020-21, which showed an increase of 1.7% over 2019-20. The production of nitrogen-based fertilizers stood at 13.74 million MT during 2020-21 and recorded a marginal increase of 0.2% over 2019-2020.

- According to the National Bureau of Statistics of China, in 2021, the grain production totaled 682.9 million ton, up from 650 million ton last year, registering an increase of 2%. Corn acreage rose by 5% from last year, and output rose by 4.6%. The growing use of fertilizers to increase productivity to keep up with the declining cultivated area is expected to drive the market in the country.

- Nitric acid is used as a raw material for inks, pigments, and dyes, which find major applications in the textile industry. The textile industry of China grew steadily during the first nine months of 2021, with profits collectively worth CNY 171.1 billion (approximately USD 26.80 billion), a 31.7% increase Y-o-Y, according to the Ministry of Industry and Information Technology (MIIT).

- Nitric acid is used to produce explosives such as trinitrotoluene (TNT), nitrocellulose, nitroglycerin, and others, which are being used in mining applications. For instance, in March 2021, Coal India Ltd (CIL) approved 32 new coal mining projects, of which 24 are the expansion of the existing projects, and the remaining are greenfield. The project's estimated cost is INR 47,000 crores (~USD 5,675.64 million), thereby augmenting the market studied.

- Therefore, the factors mentioned above are expected to have a significant impact on the market in the coming years.

Nitric Acid Industry Overview

The nitric acid market is fragmented in nature. The major companies in the market studied (not in any particular order) include CF Industries Holdings Inc., HUCHEMS, Yara, LSB INDUSTRIES, and Deepak Fertilisers and Petrochemicals Corporation Ltd (DFPCL).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Usage from the Fertilizers Segment

- 4.1.2 Increasing Demand from Explosives Manufacturing

- 4.2 Restraints

- 4.2.1 Health Hazards Caused by Nitric Acid

- 4.2.2 Environmental Regulations and Policies

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive RiIvalry

- 4.5 Trade Flow Analysis

- 4.6 Cost Analysis

5 Market Segmentation (Market Size in Volume)

- 5.1 End-user Industry

- 5.1.1 Fertilizers

- 5.1.2 Aerospace

- 5.1.3 Inks, Pigments, and Dyes

- 5.1.4 Chemical Manufacturing

- 5.1.5 Explosives

- 5.1.6 Other End-user Industries (Pharmaceuticals, Food Processing)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Mexico

- 5.2.2.3 Canada

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Merger and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)** / Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 CF Fertilisers UK

- 6.4.3 Deepak Fertilisers and Petrochemicals Corporation Ltd (DFPCL)

- 6.4.4 Gujarat Narmada Valley Fertilizers & Chemicals Limited (GNFC)

- 6.4.5 Hanwha Corporation

- 6.4.6 HUCHEMS

- 6.4.7 INEOS

- 6.4.8 LSB INDUSTRIES

- 6.4.9 MAXAMCORP HOLDING SL

- 6.4.10 Mitsubishi Chemical Corporation

- 6.4.11 Nutrien Ltd

- 6.4.12 Sasol Ltd

- 6.4.13 Sinopec Nanjing Chemical Industries Co. Ltd (China Petrochemical Corporation)

- 6.4.14 Sumitomo Chemical Co. Ltd

- 6.4.15 Yara

7 Market Opportunities and Future Trends

- 7.1 Technological Developments in Nitric Acid Manufacturing and Recent Government Incentives

濃硝酸市場:按類型、等級、濃度、應用和最終用途 – 2024-2030 年全球預測

濃硝酸市場:按類型、等級、濃度、應用和最終用途 – 2024-2030 年全球預測 2024年硝酸全球市場報告

2024年硝酸全球市場報告 2024 年濃硝酸全球市場報告

2024 年濃硝酸全球市場報告 濃硝酸市場報告:2030 年趨勢、預測與競爭分析

濃硝酸市場報告:2030 年趨勢、預測與競爭分析 全球硝酸市場預測(截至 2030 年)

全球硝酸市場預測(截至 2030 年) 硝酸的全球市場 (2015-2032年):工廠生產能力、生產量、運作效率、供需數量、產品類型、終端用戶產業、銷售管道、地區需求、海外貿易、企業佔有率

硝酸的全球市場 (2015-2032年):工廠生產能力、生產量、運作效率、供需數量、產品類型、終端用戶產業、銷售管道、地區需求、海外貿易、企業佔有率 硝酸市場-2018-2028年全球產業規模、佔有率、趨勢、機會與預測,依工廠類型、銷售通路、最終用途、地區、競爭

硝酸市場-2018-2028年全球產業規模、佔有率、趨勢、機會與預測,依工廠類型、銷售通路、最終用途、地區、競爭 全球硝酸市場

全球硝酸市場 硝酸的全球市場(2016年~2032年)

硝酸的全球市場(2016年~2032年) 全球硝酸市場 - 按應用(肥料、硝基苯)、最終用途(農業、爆炸物)劃分的市場規模、份額和增長分析 - 行業預測 (2023-2030)

全球硝酸市場 - 按應用(肥料、硝基苯)、最終用途(農業、爆炸物)劃分的市場規模、份額和增長分析 - 行業預測 (2023-2030)