|

市場調查報告書

商品編碼

1439841

多晶矽:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Polysilicon - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

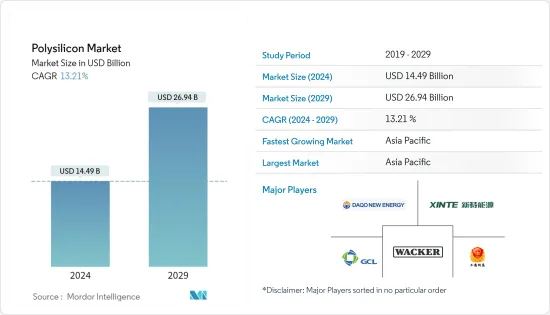

預計2024年多晶矽市場規模為144.9億美元,預計2029年將達269.4億美元,在預測期內(2024-2029年)年複合成長率為13.21%。

新型冠狀病毒感染症 COVID-19 對 2020 年研究的市場產生了負面影響。鑑於政府實施的封鎖,世界各地的太陽能發電工程在疫情期間暫時停止。然而,所研究市場的需求在 2021 年顯著復甦,預計未來幾年將顯著成長。

主要亮點

- 短期內,推動所研究市場的主要因素是光伏(PV)安裝數量的增加和半導體產業的成長。

- 然而,改進的冶金級矽(UMG-Si)太陽能電池和高資本支出等新競爭對手可能會阻礙市場發展。

- 在預測期內,生產過程中的技術進步可能代表全球多晶矽市場的重大機會。

- 亞太地區預計將主導全球多晶矽市場,並且由於中國和印度等國家消費量的成長,預計亞太地區也將成為預測期內成長最快的市場。

多晶矽市場趨勢

太陽能發電產業需求不斷成長

- 多晶矽是光電產業的關鍵材料,因為它是生產矽基太陽能電池的最重要原料之一。

- 多晶矽用於生產結晶和多晶太陽能板。結晶太陽能電池板是目前用於屋頂太陽能板安裝的最受歡迎的太陽能電池板之一。矽晶型太陽能電池採用柴可拉斯基法製造。在此方法中,將矽籽結晶置於高溫純矽熔池中。

- 該過程形成稱為矽錠的結晶,將其切成薄矽晶圓並用於太陽能模組。

- 多晶板有時也稱為多晶板。深受想要在預算內安裝太陽能板的住宅的歡迎。

- 與結晶板類似,多晶電池板由矽太陽能電池製成。然而,由於冷卻過程不同,形成的是多個結晶而不是一個。住宅中使用的多晶板通常包含 60 個太陽能電池。

- 太陽能產業是世界上成長最快的產業之一。根據國際能源總署(IEA)的數據,該產業幾乎佔全球淨發電量的三分之二。

- 使用太陽能為迷你電網供電是為居住在電線附近的人們提供電力的好方法,特別是在太陽能資源豐富的新興國家。

- 根據國際可再生能源機構 (IRENA) 的數據,太陽能仍然是世界上成長最快的可再生能源,2021 年全球可再生能源裝置容量為 3,064 吉瓦,其中一半來自太陽能。

- 根據國際可再生能源機構(IRENA)的數據,2021年全球整體太陽能產能擴張成長19%,新增裝置133吉瓦。此外,根據世界經濟論壇預測,2021年,太陽能和風電合計發電量將首次超過全球總發電量的10%,其中太陽能將佔約5%的佔有率。

- 2021 年,全球裝置容量約為 850 吉瓦,而 2020 年為 770 吉瓦。 IEA表示,2021年再生能源容量成長將由290吉瓦的太陽能光電新委託推動,佔3%。去年,太陽能發電佔所有再生能源擴張的一半以上。

- 因此,不斷成長的太陽能產業預計將在未來幾年增加對多晶矽的需求。

亞太地區主導市場

- 由於中國、韓國和印度等國家消費量的增加,亞太地區已成為多晶矽的主要消費地區。

- 中國省最近公佈了國內多晶矽產能,總合12.2萬噸。

- 該國新的多晶矽擴建項目仍在建設中,預計到 2023 年運作產量將超過 120 萬噸。全球大部分多晶矽生產(89%)預計將繼續在中國境內進行,儘管大部分擴張(72%)計劃在新疆以外進行。

- 韓國的太陽能發電裝置規模排名世界第九。該國約4%的電力也來自太陽能,自2021年11月以來,太陽能發電量一直在穩定成長。此外,根據國際貿易組織的數據,韓國是第 14 個到 2050 年實現碳中和的國家,其中期目標是到 2030 年排放40%。

- 韓國90%以上的能源依賴進口,支撐著因國內能源資源匱乏而被視為高能源集中產業。 2021年,韓國發電量為576,316吉瓦時,其中可再生能源發電量(43,085吉瓦時)增加了18%。

- 2021年,塔塔電力太陽能公司將從國營能源效率服務有限公司(EESL)獲得53.8億印度盧比(約6,577萬美元),用於在印度啟動多個約100兆瓦的分散式地面太陽能發電工程。)我們收集了訂單數量相當可觀。

- 截至2021年6月,全球許多最大的太陽能發電設施位於印度和中國。在印度,位於拉賈斯坦邦焦特布爾地區的Bhadra太陽能發電廠總產能為2,245兆瓦。

- 因此,這種趨勢加上最終用戶的快速成長,預計將在預測期內推動亞太國家對多晶矽的需求。

多晶矽行業概況

全球多晶矽市場整合,前五名企業佔全球產量的較大佔有率。主要參與者包括(排名不分先後)四川永祥(通威)、協鑫科技、大全新能源、瓦克化學和新特能源。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 太陽能發電裝置數量增加

- 半導體產業的成長

- 抑制因素

- 新的競爭對手,例如昇級的冶金級矽 (UMG-Si) 太陽能電池

- 資金投入大

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

- 技術簡介

第5章市場區隔(以金額為準的市場規模)

- 最終用戶產業

- 太陽能

- 結晶太陽能板

- 多晶太陽能板

- 電子(半導體)

- 太陽能

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 合併、收購、合資、合作和協議

- 市場佔有率(%)分析

- 主要企業採取的策略

- 公司簡介

- Asia Silicon(Qinghai)Co. Ltd

- Daqo New Energy Co. Ltd

- GCL-TECH

- Hemlock Semiconductor Operations LLC And Hemlock Semiconductor LLC

- Mitsubishi Polycrystalline Silicon America Corporation

- OCI Company Ltd

- Qatar Solar Technologies

- REC Silicon ASA

- Sichuan Yongxiang Co. Ltd(Tongwei)

- Tokuyama Corporation

- Wacker Chemie AG

- Xinte Energy Co. Ltd

第7章市場機會與未來趨勢

- 生產過程中的技術進步

The Polysilicon Market size is estimated at USD 14.49 billion in 2024, and is expected to reach USD 26.94 billion by 2029, growing at a CAGR of 13.21% during the forecast period (2024-2029).

COVID-19 negatively affected the market studied in 2020. Considering the government-imposed lockdowns, solar projects across the world were temporarily halted during the pandemic. However, the demand for the market studied recovered significantly in 2021 and is expected to grow at a significant rate in the coming years.

Key Highlights

- Over the short term, the major factor driving the market studied are the increasing number of solar photovoltaic (PV) installations and growth in the semiconductor industry.

- However, emerging competitors, such as upgraded metallurgical-grade silicon (UMG-Si) solar cells and high capital expenditure, are likely to hinder the market.

- Technological advancement in the production process is likely to be a major opportunity in the global polysilicon market over the forecast period.

- Asia-Pacific is expected to dominate the global polysilicon market and is also expected to be the fastest-growing market during the forecast period owing to the increasing consumption of countries such as China and India.

Polysilicon Market Trends

Growing Demand from the Solar PV Industry

- Polysilicon is a key material in the solar PV industry as it is one of the most important feedstock materials used to manufacture silicon-based solar cells.

- Polysilicon is used to produce monocrystalline solar panels and multi-crystalline panels. Monocrystalline solar panels are one of the most popular solar panels used in rooftop solar panel installations today. Monocrystalline silicon solar cells are manufactured through the Czochralski method, in which a seed crystal of silicon is placed into a molten vat of pure silicon at a high temperature.

- This process forms a single silicon crystal, called an ingot, which is sliced into thin silicon wafers, which are then used in solar modules.

- Polycrystalline panels are sometimes referred to as multi-crystalline panels. They are popular among homeowners looking to install solar panels on a budget.

- Like monocrystalline panels, polycrystalline panels are made of silicon solar cells. However, the cooling process is different, which causes multiple crystals to form instead of one. Polycrystalline panels used in residential homes usually contain 60 solar cells.

- The solar PV industry is one of the fastest-growing industries in the world. According to the International Energy Agency (IEA), this industry accounts for almost two-thirds of the net power capacity across the world.

- Using solar PV to power mini-grids is an excellent way to bring electricity access to people who do not live near power transmission lines, particularly in developing countries with excellent solar energy resources.

- Solar power remains the fastest-growing renewable energy across the world, therefore representing over half of the 3,064 GW (gigawatt) of renewable capacity installed internationally in 2021, as per the International Renewable Energy Agency (IRENA).

- According to International Renewable Energy Agency (IRENA), the total global solar capacity expansion increased by 19% in 2021, recording 133 GW additional installations. Furthermore, as per World Economic Forum, in 2021, for the first time, solar and wind together generated over 10% of the total electricity across the world, with solar power accounting for around 5% of the share.

- In 2021, the total global installed solar energy capacity was around 850 GW, compared to 770 GW in 2020. As per IEA, the additions in renewable power capacity in 2021 were driven up by 290 GW of solar PV new commissions, representing a 3% hike from 2020. Solar PV accounted for more than half of the total renewable power expansions the previous year.

- Therefore, the growing solar PV industry is expected to boost the demand for polysilicon in the coming years.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific was found to be the major consumer of polysilicon, owing to increasing consumption from countries such as China, South Korea, and India.

- The Chinese ministry recently released the polysilicon production capacity in the country, which totaled 122,000 tons.

- Sizeable pipelines for new polysilicon expansions in the country continue to be built, with over 1.2 million tons expected to be online by 2023. Although most expansions (72%) are planned outside of Xinjiang, the vast majority (89%) of global polysilicon production is still expected to take place within China.

- South Korea has the world's ninth-largest solar installation. The country also generates about 4% of its electricity from solar energy, and since November 2021, the amount of solar power has been steadily increasing. Furthermore, according to the International Trade Organization, South Korea is the 14th country to become carbon neutral by 2050, with an interim target of reducing emissions by 40% by 2030.

- South Korea imports more than 90% of its energy resources, sustaining industries deemed highly energy-intensive due to its lack of domestic energy resources. In 2021, South Korea generated 576,316 GWh of electricity, with an 18% increase in renewable energy (43,085 GWh).

- In 2021, Tata Power Solar bagged orders worth INR 538 crore (~USD 65.77 million) from state-run Energy Efficiency Services Ltd (EESL) to set up multiple distributed ground-mounted solar projects of approximately 100MW in India.

- As of June 2021, many of the world's largest solar power facilities were located in India and China. In India, Bhadla solar farm, located in Jodhpur district, Rajasthan, has a total production capacity of 2,245 megawatts.

- Hence, such trends, coupled with rapidly growing end users, are expected to boost the demand for polysilicon in countries of the Asia-Pacific region during the forecast period.

Polysilicon Industry Overview

The global polysilicon market is consolidated, with the top five players accounting for a significant share of global production. Some of the major players (not in any particular order) include Sichuan Yongxiang Co. Ltd (Tongwei Co. Ltd), GCL-TECH, DaqoNew Energy Co. Ltd, Wacker Chemie AG, and XinteEnergy Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Number of Solar PV Installation

- 4.1.2 Growth in the Semiconductor Industry

- 4.2 Restraints

- 4.2.1 Emerging Competitors, such as Upgraded Metallurgical-grade Silicon (UMG-Si) Solar Cell

- 4.2.2 High Capital Expenditure

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 End-user Industry

- 5.1.1 Solar PV

- 5.1.1.1 Monocrystalline Solar Panel

- 5.1.1.2 Multicrystalline Solar Panel

- 5.1.2 Electronics (Semiconductor)

- 5.1.1 Solar PV

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Asia Silicon (Qinghai) Co. Ltd

- 6.4.2 Daqo New Energy Co. Ltd

- 6.4.3 GCL-TECH

- 6.4.4 Hemlock Semiconductor Operations LLC And Hemlock Semiconductor LLC

- 6.4.5 Mitsubishi Polycrystalline Silicon America Corporation

- 6.4.6 OCI Company Ltd

- 6.4.7 Qatar Solar Technologies

- 6.4.8 REC Silicon ASA

- 6.4.9 Sichuan Yongxiang Co. Ltd (Tongwei)

- 6.4.10 Tokuyama Corporation

- 6.4.11 Wacker Chemie AG

- 6.4.12 Xinte Energy Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancement in Production Process

多晶矽全球市場規模、佔有率和趨勢分析報告(按應用、電子和地區分類的展望和預測,2023-2030年)

多晶矽全球市場規模、佔有率和趨勢分析報告(按應用、電子和地區分類的展望和預測,2023-2030年) 多晶矽塊市場報告:2030 年趨勢、預測與競爭分析

多晶矽塊市場報告:2030 年趨勢、預測與競爭分析 多晶矽市場:按型態、最終用途行業分類 - 2024-2030 年全球預測

多晶矽市場:按型態、最終用途行業分類 - 2024-2030 年全球預測 多晶矽市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場預測,2024-2030

多晶矽市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場預測,2024-2030 多晶矽市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按最終用戶產業(太陽能光電{單晶太陽能板和多晶太陽能板}、電子{半導體})、按地區、競爭

多晶矽市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按最終用戶產業(太陽能光電{單晶太陽能板和多晶太陽能板}、電子{半導體})、按地區、競爭 2023-2028年按製造技術(西門子製程、流體化床反應器製程、升級冶金級矽製程)、形式、應用和地區分類的多晶矽市場報告

2023-2028年按製造技術(西門子製程、流體化床反應器製程、升級冶金級矽製程)、形式、應用和地區分類的多晶矽市場報告 多晶矽市場,按形式類型、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測

多晶矽市場,按形式類型、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測 全球多晶矽市場 2023-2027

全球多晶矽市場 2023-2027 全球多晶矽市場

全球多晶矽市場 全球多晶矽市場:到 2028 年的預測 - 按等級(電子級、太陽能級)、形式(顆粒、塊、棒)、產品類型、技術、應用和地區分析

全球多晶矽市場:到 2028 年的預測 - 按等級(電子級、太陽能級)、形式(顆粒、塊、棒)、產品類型、技術、應用和地區分析