|

市場調查報告書

商品編碼

1437912

人造板:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Wood-based Panel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

預計2024年人造板市場規模為40575萬立方米,預計到2029年將達到47427萬立方米,預測期內(2024-2029年)複合年成長率為3.17%。

2020年,市場受到COVID-19感染疾病的負面影響。一些國家對家具中使用的某些類型的進口纖維板徵收反傾銷稅,以支持國內生產商。為了遏制病毒的傳播,所有建築工程和其他活動都被停止,這對市場產生了負面影響。然而,由於建設活動的增加,預計 2021 年市場將穩定成長。

主要亮點

- 短期內,住宅和商業建築的看漲成長趨勢以及家具產業需求的增加是推動所研究市場成長的關鍵因素。

- 然而,人造板的甲醛排放量是預計在預測期內抑制目標產業成長的關鍵因素。

- 儘管如此,OSB 在結構絕緣板 (SIPS) 中的應用不斷增加可能很快就會為全球市場創造利潤豐厚的成長機會。

- 在亞太地區,由於人造板在家具、建築、包裝等最終用途領域的廣泛使用,因此預計人造板市場在評估期間將出現健康成長。特性。

人造板市場趨勢

家具業需求增加

- 人造板由於多種優點而廣泛應用於住宅家具。儘管木製家具的替代品有多種,但木製家具的需求仍處於高峰期。人造板經久耐用、經濟、易於清潔且用途廣泛。

- 全球家具市場佔國內家用家具的65%,其次是商業(包括辦公室、飯店等)。亞太地區是全球最大的家俱生產國,其中中國、印度和日本是主要生產國。

- 中國是世界家居產業的主要生產國。隨著都市化的推進,中國家具產業不斷湧現新的品牌。最忠實的客戶是年輕人,他們更有可能接受新趨勢並擁有巨大的購買力。此外,由於國家技術的不斷進步,家具業正在湧現新一代。宜家於2020年與中國電子商務巨頭阿里巴巴合作,在阿里巴巴網站上開設了一家虛擬商店。這是一個非常明智的市場舉措,因為虛擬商店使這家瑞典家具公司能夠接觸到更多的消費者,並嘗試新的方式來推廣其產品。

- 印度家具業最大的部分是家居用品。臥室家具在印度家居市場的佔有率最高,其次是客廳家具。然而,衣櫃和廚房是最昂貴的採購項目,顧客在廚房家具上的花費約為 7,000 至 10,000 美元。

- 歐洲家居產業嚴重依賴亞洲國家的進口產品,最近的供應鏈中斷使籌資策略變得複雜。因此,與亞洲國家相比,零售商正在增加從鄰國進口的比例,以降低運輸成本和交貨時間。

- 2022 年 10 月,MoKo Home+Living 在 B 輪債務股權資金籌措中籌集了 65 億美元,由美國投資基金 Taranton 和瑞士投資者 Alphamundi Group主導。目的是增加家用家具的產量並保持良好的品質。這項措施促進了該國家居產業的成長。

- 在家工作工作等工作型態的延續增加了對緊湊、耐用且易於操作的家用家具的需求。從辦公空間到住宅環境的轉變增加了對功能性更強、更靈活的家用家具的需求。一些製造商開始提供使用人造板的高效家具。從符合人體工學的椅子到辦公桌和學習桌,在家工作重新引起了人們對家居裝飾的關注,促使家具市場的成長。

- 所有上述因素預計將在未來幾年推動人造板市場。

亞太地區主導市場

- 亞太地區主導了全球市場佔有率。隨著中國、印度和日本等國家建設活動的增加和家具需求的增加,該地區對人造板的需求不斷增加。

- 根據中國木材及木製品流通協會的數據,中國是最大的人造板生產國,去年的年產量約為3.15億立方公尺。其中,合板產量佔全國人造板總產量的最大佔有率,產值2.01億立方公尺。此外,去年纖維板和塑合板的產量分別為6,300萬立方公尺和3,300萬立方公尺。

- 中國人造板生產集中在山東、江蘇、廣西三省,約佔總產量的60%。根據中國木材與木製品流通協會統計,去年中國約44%的人造板用於家具製造、裝飾和維修。

- 中國正處於建設熱潮之中。根據中國國家統計局的數據,中國建築業產值從2020年的23.27兆元(3.16兆美元)增加至2021年的25.92兆元(4.2兆美元)。此外,到2030年,中國將在建築方面投資近13兆美元,人造板前景光明。

- 此外,根據印度商務部的數據,2021會計年度印度膠合板及其產品的出口額為11.5204億美元,而2020會計年度為10.8688億美元。

- 此外,資訊科技 (IT) 持續推動辦公空間需求,佔去年總租金的 49.2%。銀行、金融服務和保險業(BFSI)佔辦公空間市場總量的 15.2%,與 2020 年相比成長率約為 3%。

- 印度政府的「印度製造」計畫吸引了多家跨國公司在該國投資,這將在預計時間內增加對新辦公大樓的需求,並生產各種產品,例如塑合板。生產可能會支持對木材的需求。為基礎的面板。

- 印度龐大的建築業預計到2022年將成為世界第三大建築市場。印度政府實施的各種政策,例如智慧城市計劃和到 2022 年實現全民住宅,預計將為放緩的建設產業提供所需的刺激。行業。

- 上述因素促使預測期內該地區人造板消費需求的增加。

人造板產業概況

人造板市場本質上高度分散。主要公司包括 Kronoplus Limited、West Frazer、ARAUCO、EGGER Group 和 Kastamonu Entegre。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 住宅和商業建築的穩健成長趨勢

- 家具業需求增加

- 抑制因素

- 木質板材的甲醛排放量

- 其他限制

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔

- 產品類別

- 中密度纖維板(MDF)/高密度纖維板(HDF)

- 定向塑合板(OSB)

- 塑合板

- 硬板

- 合板

- 其他產品類型

- 應用

- 家具

- 住宅

- 商業的

- 建造

- 地板和屋頂

- 牆

- 門

- 其他結構

- 包裝

- 其他用途

- 家具

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業採取的策略

- 公司簡介

- ARAUCO

- CenturyPly

- Dongwha Group

- Dexco SA

- Egger Group

- Georgia-Pacific

- Green panel Industries Ltd

- Kastamonu Entegre

- Kronoplus Limited

- Langboard Inc.

- Louisiana-Pacific Corporation

- Pfleiderer

- Roseburg Forest Products

- Swiss Krono Group

- West Fraser

- Weyerhaeuser Company

第7章市場機會與未來趨勢

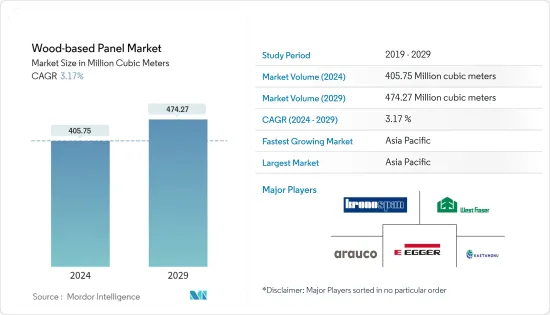

The Wood-based Panel Market size is estimated at 405.75 Million cubic meters in 2024, and is expected to reach 474.27 Million cubic meters by 2029, growing at a CAGR of 3.17% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. Several countries imposed anti-dumping duty on the import of a certain variety of fiberboard used in furniture in order to aid domestic producers. All the construction work and other activities were put on hold to curb the spreading of the virus, thereby negatively affecting the market. However, the market is projected to grow steadily, owing to increased building and construction activities in 2021.

Key Highlights

- Over the short term, bullish growth trends in residential and commercial construction, coupled with increasing demand from the furniture industry, are major factors driving the growth of the market studied.

- However, formaldehyde emission from wood-based panels is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the increasing application of OSB in structural insulated panels (SIPS) is likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific is estimated to witness healthy growth over the assessment period in the wood-based panel market due to the wide usage of wood-based panels in end-use application segments, such as furniture, construction, and packaging, due to their desirable properties.

Wood Based Panel Market Trends

Increasing Demand from the Furniture Industry

- Due to their several benefits, wood-based panels are extensively used in residential furniture. There are various alternatives to wooden furniture, but the demand for it is still at its peak. Wooden panels are long-lasting, economically friendly, easy-to-clean, and highly versatile.

- The global furniture market comprises 65% of domestic home furniture, followed by commercials (including offices, hotels, and others). Asia-Pacific is the world's largest home furniture producer, among which China, India, Japan, and others are the leading producers.

- China is the leading producer of the home furniture segment globally. As a result of urbanization, new brands have emerged in the Chinese furniture industry. Their most dedicated customers are younger people, who are more likely to adopt new trends and have tremendous purchasing power. Moreover, the growing technological advancement in the country has bought up a new generation in the furniture industry. In 2020, IKEA partnered with the Chinese e-commerce giant Alibaba to open up virtual stores on Alibaba's website. This is an extremely smart market move because the virtual store allows the Swedish furniture company to reach more consumers and experiment with a new manner of promoting their products.

- The Indian furniture industry's largest segment is the home furniture. Bedroom furniture has the highest share of the Indian home furniture market, followed by living room furniture. However, wardrobes and kitchens are the most expensive purchases, with customers spending around USD 7,000-10,000 on kitchen furniture.

- The European home furniture industry is heavily dependent on products imported from Asian countries, and recent supply chain interruptions complicate their sourcing strategies. As a result, retailers have increased their share of imports from neighboring countries compared to Asian countries to reduce transportation costs and delivery times.

- In October 2022, MoKo Home + Living raised USD 6.5 billion Series B debt-equity funding round, co-led by US-based investment fund Talanton and Swiss investor AlphaMundi Group. The aim is to increase home furniture production and maintain good quality. This initiative has driven the growth of the home furniture segment in the country.

- The ongoing working pattern, such as working from home, has increased the demand for compact, durable, and easy-to-handle home furniture. The shift from office workspaces to house settings has increased the demand for more functional and flexible home furniture. Several manufacturers have started offering efficient furniture using wood panels. Whether it is an ergonomic chair, office desk, and study table, working from home is putting the focus back on home decor, resulting in an increase in the furniture segment.

- All the above factors are expected to drive the market for wood-based panels in the coming years.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominated the global market share. With growing construction activities and the increasing demand for furniture in countries such as China, India, and Japan, the demand for wood-based panels is increasing in the region.

- According to the China Timber and Wood Products Distribution Association, China was the largest wood-based panel producer, with annual production accounting for around 315 million cubic meters last year. Out of the total, plywood production accounted for the largest share of the country's total wood-based panel production, with a production value of 201 million cubic meters. Furthermore, last year, fiberboard and particleboard production accounted for 63 million cubic meters and 33 million cubic meters, respectively.

- China's wood-based paneling production is concentrated in the Shandong, Jiangsu, and Guangxi provinces, which account for about 60% of the total production. According to the China Timber and Wood Products Distribution Association, around 44% of China's wood-based panels were used for furniture manufacturing, decoration, or renovation last year.

- China is amid a construction mega-boom. According to the National Bureau of Statistics of China, the construction works output value in the country increased from CNY 23.27 trillion (USD 3.16 trillion) in 2020 to CNY 25.92 trillion (USD 4.02 trillion) in 2021. Furthermore, China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for wood-based panels.

- Furthermore, according to the Department of Commerce (India), the export value of plywood and its products from India accounted for USD 1,152.04 million in FY 2021, compared to USD 1,086.88 million in FY 2020.

- Moreover, information technology (IT) continues to drive the demand for office spaces, with a 49.2% share of total leasing last year. Banking, financial services, and insurance (BFSI) accounted for a 15.2% share of the overall office space market, witnessing a growth rate of about 3% compared to 2020.

- The Make in India initiative by the government attracted several multinational companies to invest in the country, which is likely to increase the demand for new office buildings in the estimated time, supporting the demand for various wood-based panels, such as particle boards for furniture production.

- India's huge construction sector is expected to become the world's third-largest construction market by 2022. Various policies implemented by the Indian government, such as the Smart Cities project and Housing For All by 2022, are expected to bring the needed impetus to the slowing construction industry.

- The aforementioned factors are contributing to the increasing demand for wood-based panel consumption in the region during the forecast period.

Wood Based Panel Industry Overview

The wood-based panel market is highly fragmented in nature. The major players include Kronoplus Limited, West Frazer, ARAUCO, EGGER Group, and Kastamonu Entegre.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Bullish Growth Trends in Residential and Commercial Construction

- 4.1.2 Increasing Demand from the Furniture Industry

- 4.2 Restraints

- 4.2.1 Formaldehyde Emission from Wood-based Panels

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Medium-Density Fiberboard (MDF)/High-Density Fiberboard (HDF)

- 5.1.2 Oriented Strand Board (OSB)

- 5.1.3 Particleboard

- 5.1.4 Hardboard

- 5.1.5 Plywood

- 5.1.6 Other Product Types

- 5.2 Application

- 5.2.1 Furniture

- 5.2.1.1 Residential

- 5.2.1.2 Commercial

- 5.2.2 Construction

- 5.2.2.1 Floor and Roof

- 5.2.2.2 Wall

- 5.2.2.3 Door

- 5.2.2.4 Other Constructions

- 5.2.3 Packaging

- 5.2.4 Other Applications

- 5.2.1 Furniture

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ARAUCO

- 6.4.2 CenturyPly

- 6.4.3 Dongwha Group

- 6.4.4 Dexco SA

- 6.4.5 Egger Group

- 6.4.6 Georgia-Pacific

- 6.4.7 Green panel Industries Ltd

- 6.4.8 Kastamonu Entegre

- 6.4.9 Kronoplus Limited

- 6.4.10 Langboard Inc.

- 6.4.11 Louisiana-Pacific Corporation

- 6.4.12 Pfleiderer

- 6.4.13 Roseburg Forest Products

- 6.4.14 Swiss Krono Group

- 6.4.15 West Fraser

- 6.4.16 Weyerhaeuser Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Application of OSB in Structural Insulated Panels (SIPS)