|

市場調查報告書

商品編碼

1432977

日本電動車充電設備:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Japan Electric Vehicle Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

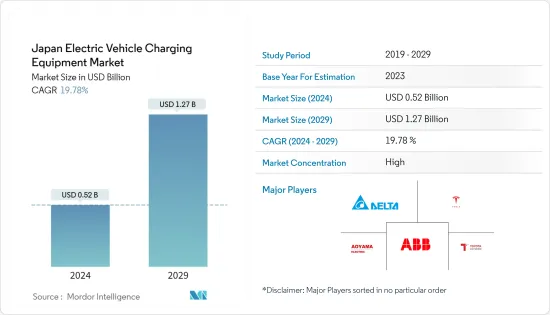

日本電動車充電設備市場規模預計到 2024 年為 5.2 億美元,預計到 2029 年將達到 12.7 億美元,預測期內(2024-2029 年)複合年成長率為 19.78%。

COVID-19 的爆發對市場產生了負面影響。該國電動車的銷售受到阻礙,而電動車的市場佔有率很低。今年銷售疲軟的主要原因是經濟活動長期暫停和實施嚴格的封鎖措施。 2020年3月,日本充電站數量減少約1,087個,至29,233個。充電站數量減少的原因是電動車僅佔日本銷售新車的1%,因此充電站的使用不多。有些看台很舊,有些已經拆除。

在日本,插電式混合動力汽車的大量使用以及純電動車及其使用需求的不斷成長,使得電動車充電站的需求大幅增加,擴大了該行業的市場機會。此外,自2010年以來,日本的車站數量一直在穩步增加。 2010年充電站數量約310個,到2021年將增加到3萬多個。

日本政府的目標是到 2050 年實現碳中和,為充電站提供補貼,以促進電動車的普及。日本政府正在促進綠色燃料汽車的銷售,雄心勃勃的計劃是到 2035 年所有銷售的新車都將採用電力動力來源,包括電動車和混合。這可能會在預測期內推動電動車充電設備的需求。

日本電動車充電站市場趨勢

政府促進電動車銷售的措施將對市場產生正面影響

日本政府透過鼓勵電動車(HEV、PHEV、BEV)的普及提高人們對環境問題的認知。同時,道路上的電動車數量不斷增加,這可能會推動對相關充電基礎設施的需求。

五個最大的小客車市場包括中國、美國、德國、印度和日本。 2020年12月,日本政府推出綠色成長策略,透過推廣電動車、燃料電池電動車、插電式混合和混合,到2050年實現日本碳中和。

透過這些實施,日本尋求減少運輸部門排放的影響,以實現《巴黎協定》下的溫室氣體減排目標。日本充電站的集中度遠低於其他已開發國家,顯示未來幾年的成長潛力巨大。例如,2021年,日本每100公里道路只有1.7個充電站,而韓國則約為75.2個。 2020年,日本總合29,855個充電站(21,916個普通充電器和7,939個快速充電器)。然而,與充電技術相關的專利申請數量超過1,310件,位居世界第二。

日本為其汽車產業制定了克服氣候變遷和盡量減少碳排放的長期目標和策略。在接下來的半個世紀裡,各國政府制定了三項主要行動來推廣電動車,包括創新、政策和基礎設施投資。促進創新,開發鋰離子電池,創造經濟的採購路線,並開發下一代技術。

政策重點是加強全球供應鏈、涵蓋國際電動政策、最大限度地提高燃料標準。在基礎設施發展方面,第一次調查將包括透過穩定電池零件的採購來建立電池網路、制定廢棄電池再利用和回收指南以及投資無線充電基礎設施的研發。 2021年11月,日本政府宣布將對電動車的獎勵加倍至每輛車80萬日元,並提供充電基礎設施補貼,以趕上北美、歐洲等成熟經濟體。

高安裝和維護成本預計將阻礙市場成長

安裝電動車充電站的成本相當高,並且根據安裝的充電器類型而有所不同。為了安裝電動車充電基礎設施,必須滿足最低基礎設施要求,找到合適的供應商和位置非常重要。充電基礎設施成本包括固定成本(安裝、公用事業服務、變壓器、設備)和變動成本(電費)。

對於公用電費充電器來說,按需收費可佔營業成本的大部分。因此,快速充電站的總電力成本高於住宅充電器,除非前者達到足夠高的運轉率。

在目前的利用水準下,商業充電器通常在經濟上不可行。為了使商業充電基礎設施實現經濟盈利並與 IC 引擎競爭,需要顯著且持續的需求成長。

在高峰時段集中對電動車進行家庭充電可能會使當地變壓器過載。公用事業公司可能必須購買額外的高峰容量,除非它們能夠將需求轉移到非尖峰時段時段。

電動車充電器分為三種。電器產品常用的標準 120V 插頭充電速度較慢,但約 8 至 12 小時即可將電池充滿。 240V 2 級充電器通常可在一小時內充電 20-25 英里,將充電時間縮短至不到八小時。在典型的家庭中,2 級充電器可以使用服裝類機或電烤箱所需的相同類型的插座。 3 級直流 (DC) 快速充電器可在 30 分鐘內將電池充電至 80%。

汽車製造商使用三種類型的直流快速充電器。大多數製造商使用SAE組合充電系統(CCS),CHAdeMO由日產和三菱使用,而Tesla Supercharger僅由特斯拉汽車使用。車輛相容性的缺乏可能會限制車輛普遍使用充電站並阻礙市場成長。

必須謹慎部署高功率充電樁,以確保電站的高使用率。在目前的情況下,充電站的盈利相當低。只有當電動車足夠普及並且基礎設施能夠保持高運轉率時,盈利才可能增加。例如,2020年純電動車銷量為14,604輛,而同期混合動力汽車銷量超過1,324,800輛。

日本電動車充電站產業概況

電動車充電站市場較為集中,主要市場佔有率由少數企業佔據。主要參與企業包括ABB、Delta電子和豐田。該國的主要企業已與其他參與者成立合資企業,以開發尖端技術。此外,各種汽車製造商正在向其客戶提供家庭充電解決方案以及電動車。例如,

- 2021 年 11 月,Subaru宣布推出首款電動車 (EV) Solterra。使用住宅充電器將 Solterra 從零充滿到 100% 需要近 13 小時。不過,使用 Level 3 直流快速充電器,Solterra 可以在不到一小時的時間內充電至 80%,續航里程預計超過 320 公里。

- 2021年10月,豐田汽車公司公佈了新型BEV(電池電動車)「bZ4X」的詳細資料。 bZ4X是中型SUV,也是豐田bZ系列的首款車型。採用與Subaru公司共同開發的BEV專用平台。隨附的家用壁式充電器可在 10 小時內充滿電。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 最終用途

- 家庭充電

- 公共充電

- 充電站

- 交流充電站

- 直流充電站

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- ABB Ltd

- Delta Electronics Inc.

- e-Mobility Power Inc.

- Toyota Connected Corporation

- Tesla Inc.

- Aoyama Elevator Global Ltd

- Tritium Charging

- NEC Telecommunication and Information Technology Ltd

第7章 市場機會及未來趨勢

The Japan Electric Vehicle Charging Equipment Market size is estimated at USD 0.52 billion in 2024, and is expected to reach USD 1.27 billion by 2029, growing at a CAGR of 19.78% during the forecast period (2024-2029).

The outbreak of COVID-19 has negatively impacted the market. The sales of electric vehicles in the country were hampered, and the market share of electric vehicles is very low. The major reason for the low sales during the year was the strict lockdown measures as economic activities were stopped for a long time. In March 2020, it was recorded that the number of charging stations in the country reduced by around 1,087 to 29,233 charging stations. The reason for the reduction in charging stations is that electric vehicles account for only one percent of the new cars sold in Japan because the charging stands are not being used very much. Some of them are outdated, and others have been removed.

The high number of plug-in hybrids and the growing demand for battery electric vehicles and their usage in the country significantly boosted the demand for electric vehicle charging stations and increased market opportunities for the industry. Further, number of stations has been growing steadily in Japan since fiscal 2010. In 2010, there were around 310 charging stations in the country, which increased to more than 30,000 stations in 2021.

Major subsidies offered by the country's government to promote the use of electric vehicles, as an effort to become carbon neutral by 2050, led to subsidizing the charging stations in the country. This is likely to drive the market's growth during the forecast period.The Japanese government is boosting the sales of green fuel vehicles and has an ambitious plan that all the new vehicles sold by 2035 will be powered by electricity, both electric and hybrid electric vehicles. This will enhance electric vehicle charging equipment demand during the forecast period.

Japan EV Charging Stations Market Trends

Government Initiatives to Boost Electric Vehicle Sales to Have Positive Impact on the Market

Surging carbon emission by the transportation sector has propelled the environmental concern across Japan, which is scrutinized by Japan government by encouraging the adoption of electric vehicles, i.e., HEVs, PHEVs, and BEVs. With this, the number of electric vehicles on the road is constantly increasing, which is likely to drive the demand for associated charging infrastructure.

The five largest passenger car market includes China, the United States, Germany, India, and Japan. Along with several other countries across the world, Japan has committed to net zero-emission passenger car sales.In December 2020, Japan government introduced a green growth strategy to make Japan carbon neutral by 2050 by promoting electric vehicles, fuel cell electric vehicles, plug-in hybrid vehicles, and hybrid vehicles.

With these implementations, Japan seeks to reduce the emission impact from the transportation sector to achieve the GHG (Green House Gas) reduction goals under the Paris agreement.The concentration of charging stations in Japan is quite less compared to other developed countries, indicating massive growth potential in the coming years. For instance, in 2021, Japan had only 1.7 charging stations per 100 km of roadways, whereas South Korea had around 75.2. In 2020, Japan had a total of 29,855 charging stations (21,916 sallow chargers and 7,939 fast chargers). Although, Japan accounts for the second position in charging technology patents across the world, with more than 1,310 patent filings.

Japan has long-term goals and strategies for the automotive industry to beat climate change and minimize carbon emissions. For the next half-decade, the government has set three key actions to promote the electric vehicle, including innovations, Policies, and investment in infrastructure.Promotion for innovation, developing lithium-ion batteries, building economic procurement channels, and developing next-generation technologies.

Through policies, the country is focusing on robust the global supply chain, incorporating international electrification policies, and maximizing the fuel standards. In Infrastructural development, the primary focus would be building a battery network by stabilizing the battery components procurement, establishing a guideline for used batteries to reuse/recycle, and investing in research and development of wireless charging infrastructures. In November 2021, Japan government announced to double their incentives for electric vehicles to 800,000 Yen per vehicle and subsidizes charging infrastructure to catch up with matured economies, including North America and Europe.

High Cost of Installation and Maintenance Expected to Hinder Market growth

The cost of setting up an EV charging station is quite high and varies according to the type of chargers being installed. In order to set up the EV charging infrastructure, minimum infrastructure requirements need to be fulfilled, and finding the right vendor and location is important. The charging infrastructure costs include fixed (installation, utility service, transformers, and equipment) and variable (electricity charges) components.

For chargers on commercial electricity tariffs, demand charges can dominate operating costs. As a result, the total cost of power from fast-charging stations is higher than slower residential chargers unless the former can achieve sufficiently high utilization rates.

At current levels of utilization, commercial chargers are almost universally not economically profitable. A significant, sustained increase in demand will be needed for commercial charging infrastructure to deliver financial returns and compete with IC engines.

The high concentration of EV home charging during peak periods can overload local transformers. Utilities may have to procure additional peak capacities unless they are able to shift demand to off-peak periods.

There are three types of chargers available for EVs. The standard 120V plug, often used for home appliances, charges slowly but can fill a battery to near-full capacity in about 8 to 12 hours. The 240V level-2 chargers generally provide 20 to 25 miles of charge in an hour, which shortens charging time to eight hours or less. In homes, level-2 chargers can use the same outlet type required for clothes dryers or electric ovens. Level-3 direct current (DC) fast chargers can charge a battery up to 80% in 30 minutes.

Different auto manufacturers use three different varieties of DC fast chargers. Most manufacturers use the SAE Combined Charging System (CCS), the CHAdeMO variant is used by Nissan and Mitsubishi, and the Tesla Supercharger is used by only Tesla cars. This lack of vehicle compatibility restricts universal vehicle access to charging stations and could hinder market growth.

Deploying high-powered energy chargers must be done carefully to ensure stations have high utilization. The profit potential of charging stations is quite low in the current scenario. The profitability may only increase when there are enough electric cars on the road, so the infrastructure could have a high utilization rate. Consumer preference is more leaned toward hybrid vehicles, which significantly restraints the sales of BEVs; for instance, the sales of BEVs in 2020 was 14,604 units, whereas hybrid vehicles have surpassed the sales volume of 1,324,800 units during the same tenure.

Japan EV Charging Stations Industry Overview

The Electric vehicle charging station market is relatively consolidated, with a major market share being covered by a few companies. Some major players in the market are ABB, Delta Electronics Inc., Toyota, and others. The major players in the country are entering into joint ventures with other players to develop the latest technology. Various automakers are also providing home charging solutions to their customers along with electric vehicles. For instance,

- In November 2021, Subaru Corp unveiled its first all-electric vehicle (EV), the Solterra which takes almost 13 hours to fully charge from zero to 100 percent with the residential charger. However, Solterra also get an 80% charge in under an hour from a Level 3 DC fast charger giving out an estimated range to be greater than 320 km.

- In October 2021, Toyota Motor Corporation announced the details of bZ4X, its all-new model BEV (Battery Electric Vehicle). The bZ4X, a medium-segment SUV-type BEV, is the first model in the Toyota bZ series. The model adopts a BEV-dedicated platform jointly developed with Subaru Corporation. With provided home wall mount charger, car can reach full recharge in 10 hours.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End Use

- 5.1.1 Home Charging

- 5.1.2 Public Charging

- 5.2 Charging Station

- 5.2.1 AC Charging Station

- 5.2.2 DC Charging Station

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 ABB Ltd

- 6.2.2 Delta Electronics Inc.

- 6.2.3 e-Mobility Power Inc.

- 6.2.4 Toyota Connected Corporation

- 6.2.5 Tesla Inc.

- 6.2.6 Aoyama Elevator Global Ltd

- 6.2.7 Tritium Charging

- 6.2.8 NEC Telecommunication and Information Technology Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

電動車 (EV) 快速充電系統的全球市場:按應用、連接器類型、輸出、安裝類型和國家進行分析和預測(2023-2033 年)

電動車 (EV) 快速充電系統的全球市場:按應用、連接器類型、輸出、安裝類型和國家進行分析和預測(2023-2033 年) EVCI 硬體全球市場分析:電動車充電基礎設施

EVCI 硬體全球市場分析:電動車充電基礎設施 全球電動車充電基礎設施(EVCI)服務市場分析

全球電動車充電基礎設施(EVCI)服務市場分析 面向公共、商業和住宅領域的 EVCI(電動車充電基礎設施)軟體功能的全球市場

面向公共、商業和住宅領域的 EVCI(電動車充電基礎設施)軟體功能的全球市場 電動車充電適配器市場報告:2030 年趨勢、預測與競爭分析

電動車充電適配器市場報告:2030 年趨勢、預測與競爭分析 電動車 (EV) 充電基礎設施全球市場規模、佔有率和趨勢分析報告:按充電器類型、連接器、充電等級、連接性別、應用、地區和細分市場進行預測 (2024-2030)

電動車 (EV) 充電基礎設施全球市場規模、佔有率和趨勢分析報告:按充電器類型、連接器、充電等級、連接性別、應用、地區和細分市場進行預測 (2024-2030) 電動車充電適配器市場:按產品、產量、應用、最終用戶分類 - 2024-2030 年全球預測

電動車充電適配器市場:按產品、產量、應用、最終用戶分類 - 2024-2030 年全球預測 電動車快速充電系統市場:按充電模式、充電等級和最終應用分類 - 2024-2030 年全球預測

電動車快速充電系統市場:按充電模式、充電等級和最終應用分類 - 2024-2030 年全球預測 電動車充電管理軟體平台市場,按模組類型、充電等級、充電器類型、按應用、國家和地區 - 2023-2030 年產業分析、市場規模、市場佔有率和預測

電動車充電管理軟體平台市場,按模組類型、充電等級、充電器類型、按應用、國家和地區 - 2023-2030 年產業分析、市場規模、市場佔有率和預測 2024 年電動車充電器全球市場報告

2024 年電動車充電器全球市場報告