|

市場調查報告書

商品編碼

1430603

大豆殺菌劑種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029)Soybean Fungicide Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

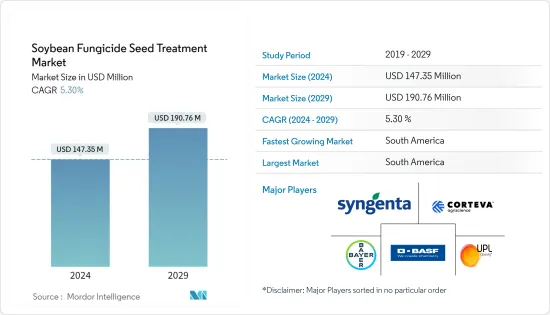

預計2024年大豆殺菌劑種子處理市場規模為1.4735億美元,預計2029年將達到1.9076億美元,在預測期內(2024-2029年)複合年成長率為5.30%。

由於 COVID-19 的影響,市場受到部分影響,世界各地的物流和供應都受到限制。據觀察,出貨限制以及空運、海運和陸運運費上漲是擾亂種子處理殺菌劑業務的關鍵因素。

從長遠來看,糧食需求的增加、作物保護技術創新的不斷增加、生物種子處理需求的增加以及政府支持的加強將推動全球大豆殺菌劑種子處理市場的發展。近年來,我們看到對生物種子處理產品的需求不斷增加。認知到這一需求,公司正在積極將新的生物種子處理產品推向市場。 2021 年,Ceradis BV 生產的一種新型生物種子處理劑 Ceramax 在 EPA 註冊,用於保護大豆作物免受猝死症候群 (SDS) 的影響。

此外,消費量的快速產量導致對高產量的需求不斷成長,推動了北美和南美種子處理劑市場的需求。然而,田間種植的大豆容易受到疫黴根腐病和莖腐病的影響,隨著人們對種子品質和安全性的認知不斷提高,以防止疾病入侵,亞太地區的種子處理實踐也在不斷增加,且進展迅速。

因此,處理種子的重要性,加上參與者採取的市場擴張和新技術創新等策略,可能會導致大豆殺菌劑種子處理市場的成長。

大豆殺菌劑種子處理市場趨勢

生物種子處理需求快速成長

日益嚴重的環境問題,特別是在許多新興市場,正在增加對生物種子處理的需求,從而推動預測期內的市場開拓。因此,越來越多的化學公司開始提供生物種子處理劑並試圖抓住市場需求。主要公司向美國生產商出售經過生物製藥和化學品組合處理的大豆種子。例如,在北美銷售的一些先鋒大豆種子產品經過生物種子處理,以提高生長、活力和產量。

生物種子處理使用活性成分,包括活微生物、發酵產物、植物抽取物、植物激素,甚至硬化學物質,對植物產生正面影響。生物種子處理劑的需求正在增加,因為它們能夠透過增強植物遺傳潛力來最佳化植物生長、最大限度地減少壓力並提高產量。

認知到潛力,越來越多的公司正在進入生物種子處理市場。 2021年,FMC與先正達作物保護公司簽訂了分銷協議,將Draco(一種玉米和大豆生物種子處理劑)在加拿大商業化。本產品具有獨特的作用方式,結合了地衣芽孢桿菌和枯草芽孢桿菌,為加拿大農民提供保護,防止根瘤菌和線蟲等奪取產量的根部害蟲的侵害。

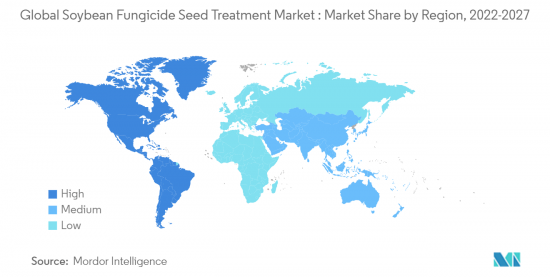

南美洲市場佔據主導地位

根據聯合國糧食及農業組織(FAO)的數據,巴西於2020年成為世界主要大豆生產國。再加上真菌病害的增加,導致種子處理殺菌劑的散佈增加,預計未來幾年還會增加。由豆薯層銹菌引起的大豆銹病是該國主要的真菌感染疾病。然而,與其他害蟲相比,大豆受到昆蟲的損害更大。

農業規模的擴大和作物輪作的減少以及生物農產品意識的增強是巴西種子產業持續發展的因素,從而導致高價值種子的快速普及。巴西的作物生產主要集中在大豆和玉米,因此幾乎所有種子都經過處理,通常在播種前經過多次處理。

近年來,農業中擴大採用先進技術和管理實踐,例如生物種子處理,可顯著改善植入並降低成本。對此,2018年,先正達在阿根廷市場推出了大豆種子處理劑Vibrance Maxx。因此,作為大豆的主要生產國和出口國,加上創新技術的不斷採用和參與企業的積極參與,大豆殺菌劑種子處理市場將在預測期內成長。

大豆殺菌劑種子處理產業概況

全球大豆殺菌劑種子處理市場由先正達國際公司、BASF、拜耳作物科學公司、科迪華農業科學公司、UPL、吳羽公司等主要企業高度整合。先正達國際股份公司擁有最大的市場佔有率,其次是BASF股份公司和拜耳作物科學股份公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 類型

- 化學

- 非化學/生物

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 泰國

- 越南

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 其他非洲

- 北美洲

第6章 競爭形勢

- 最採用的策略

- 市場佔有率分析

- 公司簡介

- Kureha Corporation

- Syngenta International AG

- Bayer CropScience AG

- BASF SE

- Bioworks Inc.

- UPL

- Corteva Agriscience

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Andermatt Group AG

第7章 市場機會及未來趨勢

第 8 章 COVID-19 市場影響評估

The Soybean Fungicide Seed Treatment Market size is estimated at USD 147.35 million in 2024, and is expected to reach USD 190.76 million by 2029, growing at a CAGR of 5.30% during the forecast period (2024-2029).

The market studied has been partially affected due to the COVID-19 pandemic, due to the logistics and supply constraints observed across the world. The restriction in movements of shipments and high air, sea, or land freight was observed to be a major factor disrupting the businesses, including seed treatment fungicides.

In the long run, increasing food demand, the rising innovation in crop protection technology, the increasing demand for biological seed treatments, and increasing government support would drive the global market of soybean fungicide seed treatment. Rising demand for biological seed treatment products has been observed in recent years. Recognizing this demand, the players are actively launching new biological seed treatment products in the market. In 2021, a new biological seed treatment, CeraMax, was registered under EPA to protect soybean crops from sudden death syndrome(SDS) produced by Ceradis BV.

Furthermore, the rising demand for higher yield due to the rapid increase in the consumption of crops has increased the demand for the seed treatment market in north America and South America. However, as as soybean plants grown in fields are highly prone to phytophthora root and stem rot and increasing awareness about the quality and safety of the seeds to protect from disease infestation, seed treatment practice in Asia-Pacific is also advancing at a faster rate.

Thus, the importance of treated seed, coupled with the strategies adopted by players, such as expanding market and innovating new technologies, is bound to lead to the growth of the soybean fungicide seed treatment market.

Soybean Fungicide Seed Treatment Market Trends

Rapidating Demand for Biological Seed Treatment

The rising environmental concerns, especially in many developed regions, the demand for biological seed treatment is rising, fueling the market's growth during the forecast period. Hence, more chemical companies are offering biological seed treatments to capture the market demand. Major players are selling soybean seeds treated with a combination of biologicals and chemicals to the growers in the United States. For instance, several pioneer soybean seed products sold in North America are treated with biological seed treatments to improve stand, plant vigor, and yield.

Biological seed treatments use active ingredients, including living microbes, fermentation products, plant extracts, phytohormones, and even hard chemistry, to have a favorable impact on plants. Owing to their ability to optimize plant growth, minimize stress, and boost overall yield by empowering the genetic potential of the plant, biological seed treatments are witnessing increasing demand.

Recognizing the potential, more companies are entering the biological seed treatment market space. In 2021, the FMC corporation entered into distribution agreements with Syngenta Crop Protection to commercialize Draco, a biological seed treatment for corn and soybean in Canada. The product has a unique mode of action that combines bacillus licheniformis and bacillus subtilis to offer Canadian farmers protection against yield-robbing root pests, such as rhizoctonia and nematodes.

South America Dominates the Market

In 2020, Brazil was the top producer of soybean in the world acoording to the Food and Agriculture Organization(FAO). This, coupled with increasing fungal diseases, leads to the hiher application of seed treatment fungicide and is anticipated to be increase in the coming years. Soybean rust, caused by Phakopsora pachyrhizi, is the major fungal infestation in the country. However, soybean is majorly affected by insects, compared to other pests.

Increasing farm size and decreasing crop rotation, coupled with rising awareness on Bio agribusiness are some of the factors contributing to the continuing strength of Brazil's seed sector which leads to the rapid adoption of high-value seeds. With Brazilian crop production narrowly focused on soybeans along with maize, virtually every seed gets treated, often more than once before it is planted.

In recent years, increased adoption of advanced technologies and management practices in agriculture can be witnessed, including biological seed treatments that significantly improve implantation and reduce costs. In this regard, in 2018, Syngenta launched Vibrance Maxx, a soybean seed treatment in the Argentine market. Therefore, being a major producer and exporter for soybeans, increased adoption of innovating technologies, coupled with the active participation of players, the soybean fungicide seed treatment market is anticipated to grow during the forecast period.

Soybean Fungicide Seed Treatment Industry Overview

The global market for soybean fungicide seed treatment is highly consolidated, with major players such as Syngenta International AG, BASF SE, Bayer Crop Science AG, Corteva Agriscience, UPL, and Kureha Corporation, among others. Syngenta International AG occupies the largest market share, followed by BASF SE and Bayer Crop Science AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Chemical

- 5.1.2 Non-Chemical/Biological

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Spain

- 5.2.2.5 Italy

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Thailand

- 5.2.3.5 Vietnam

- 5.2.3.6 Australia

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Africa

- 5.2.5.1 South Africa

- 5.2.5.2 Rest of Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Kureha Corporation

- 6.3.2 Syngenta International AG

- 6.3.3 Bayer CropScience AG

- 6.3.4 BASF SE

- 6.3.5 Bioworks Inc.

- 6.3.6 UPL

- 6.3.7 Corteva Agriscience

- 6.3.8 Nufarm Ltd

- 6.3.9 Sumitomo Chemical Co. Ltd

- 6.3.10 Andermatt Group AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 ASSESSMENT OF IMPACT OF COVID-19 ON THE MARKET

2024-2032 年按類型、應用技術、作物類型、功能和地區分類的種子處理市場報告

2024-2032 年按類型、應用技術、作物類型、功能和地區分類的種子處理市場報告 小麥種子處理:全球市場佔有率分析、產業趨勢、統計資料、成長預測(2024-2029)

小麥種子處理:全球市場佔有率分析、產業趨勢、統計資料、成長預測(2024-2029) 棉籽加工:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)

棉籽加工:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029) 玉米種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029)

玉米種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029) 稻米種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029)

稻米種子處理:市場佔有率分析、產業趨勢、成長預測(2024-2029) 2024 年種子處理全球市場報告

2024 年種子處理全球市場報告 種子處理市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、作物類型、按應用、地區和競爭細分

種子處理市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、功能、作物類型、按應用、地區和競爭細分 全球種子處理市場

全球種子處理市場 2030 年種子處理市場預測:按作物類型、劑型、功能、用途和地區進行的全球分析

2030 年種子處理市場預測:按作物類型、劑型、功能、用途和地區進行的全球分析 種子處理的全球市場 - 市場規模,佔有率,成長分析:各類型,各作物,各功能 - 產業預測(2023年~2030年)

種子處理的全球市場 - 市場規模,佔有率,成長分析:各類型,各作物,各功能 - 產業預測(2023年~2030年)