|

市場調查報告書

商品編碼

1408827

汽車貸款:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029Auto Loan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

本會計年度汽車貸款市場貸款餘額預計將達4.12兆美元,預測期內複合年成長率將超過5%。

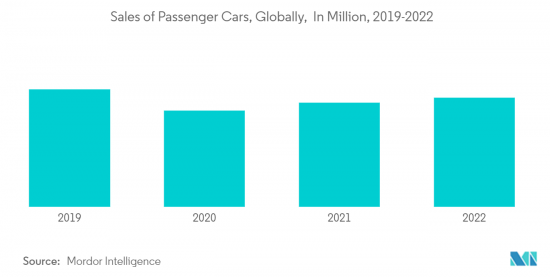

近年來,全球銷售的汽車數量穩步成長,隨著購買汽車數量的增加,用於為其資金籌措的汽車貸款數量也隨之增加。長期貸款涉及較高風險,因此貸款提供者會隨著時間的推移提高利率。已開發國家和發展中國家購買的汽車類型不同,因此汽車貸款銷售也不同。在印度等開發中國家,摩托車在汽車銷售中佔比較大,而在美國等已開發國家,四輪車(輕型卡車)在汽車銷售中佔比較大。小客車佔全球汽車銷售量的60%以上,商用車佔剩餘佔有率。自COVID-19以來,小客車價格基本上保持穩定,而商用車價格上漲了10-12%。

汽車貸款市場多種多樣,各國對其產品的需求也各不相同。貸款提供者不斷推出新的貸款產品,讓購車變得更輕鬆、更方便。在汽車貸款提供者中,銀行、專屬式金融和信用合作社佔據了 70% 左右的很大佔有率,利率根據國家/地區從 4% 到 10% 不等。

為了鼓勵電動車的普及,汽車貸款提供者為這些汽車貸款提供低長期利率。自 COVID-19 以來,中國、美國和印度已成為全球最大的汽車市場,為該地區的汽車貸款提供者帶來了更多的商機。

汽車貸款市場趨勢

小客車銷量增加

小客車市場包括兩輪車、四輪車和其他主要用於客運的車輛的銷售。 小客車的全球平均價格約為 28,000 美元,存在地區差異。 在四輪小客車的銷量中,SUV和中型車是最暢銷的市場區隔,全球銷量超過3000萬輛。 隨著銷量的同比增長,這兩個小客車市場區隔佔據了小客車銷量份額的50%以上,汽車貸款供應商正在將產品集中在特定的小客車市場區隔,以享受現有利潤並增加汽車貸款銷售。 在美國,小客車價格去年上漲,而汽車貸款價格上漲使購車者負債纍纍。 小客車價格的上漲正在擴大汽車貸款供應商的業務。 隨著收入和生活水準的提高,小客車正在成為汽車貸款的機會。

信用合作社增加汽車貸款

信用合作社是向其使用者提供傳統銀行服務的金融合作機構。隨著世界各國央行收緊貨幣政策,銀行機構利率持續上升。因此,在新冠肺炎 (COVID-19) 疫情之後,隨著人們儲蓄下降,信用合作社已成為高效的汽車貸款提供者。在美國汽車貸款的供應商分佈中,信用合作社的佔有率在冠狀病毒爆發後成長了 7% 以上。在購買二手車的貸款中,信用合作社的佔有率從 COVID-19 期間的 25% 增加到去年的 31%。由於汽車價格上漲和貸款利率上升,信用合作社正在成為對汽車購買者有吸引力的融資解決方案。

汽車貸款產業概況

目前汽車貸款市場較為型態,參與者眾多。尋求以最低手續費獲得低利率貸款的公司之間的競爭日益激烈,促使更具競爭力的公司進行投資以獲得更大的客戶佔有率。數位貸款和銀行應用程式的創新正在提高借款人的汽車貸款效率。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態與洞察

- 市場概況

- 市場促進因素

- 小客車需求增加

- 透過更快的貸款處理來增加汽車貸款銷售

- 市場抑制因素

- 銀行升息

- 汽車市場價格上漲

- 市場機會

- 新興電動車市場擴大汽車貸款市場

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 汽車貸款市場的技術創新

- COVID-19 對市場的影響

第5章市場區隔

- 依車型分類

- 小客車

- 商用車

- 依所有權

- 新車

- 二手車

- 依最終用戶

- 個人

- 公司

- 依貸款提供者

- 銀行

- OEM

- 信用合作社

- 其他

- 依地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 德國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 南美洲

- 巴西

- 秘魯

- 南美洲其他地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東地區

- 其他地區

- 北美洲

第6章 競爭形勢

- 市場集中度概覽

- 公司簡介

- Ally Financial

- Wells Fargo

- Chase

- Capital One

- Bank of America

- BNP Paribas Financial Service

- Credit Agricole

- HDFC Bank

- ICICI Bank

- Mashreq Bank

第7章 市場未來趨勢

第 8 章 免責聲明與出版商訊息

The auto loan market has a loan outstanding of USD 4.12 trillion in the current year and is poised to register a CAGR of more than 5% for the forecast period.

Automobile sales globally have observed a continuous increase over the years, increasing the number of vehicles purchased with a rise in rise in number of auto loans taken by people for financing them. Based on the duration, loan providers globally are increasing their rate of interest as long-term loans are associated with higher risk. With differences in the types of vehicles purchased between developed and developing countries, sales of auto loans category also vary. As developing countries such as India exist with a major share of two-wheelers in automobile sales, developed countries such as the United States exist with a major share of four vehicles (Light Truck) in their automobile sales. In terms of global motor vehicle sales, passenger cars have emerged with a share of more than 60%, and the remaining share is occupied by commercial vehicles. Post-COVID-19 price of passenger vehicles has almost stabilized, with commercial vehicles observing a price rise of 10-12%, resulting in a decline in their sales and their associated loan business.

The Auto loan market exists with a varied demand for its products, having intra-country differences. Loan providers are continuously emerging with new loan products for making the purchase of automobiles easy and more convenient. Among the Automobile loan providers, Banks, Captive finance, and credit unions exist with a major share of around 70%, with the rate of interest varying between 4% to 10% in different countries.

To promote the adoption of Electric vehicles, Auto loan providers are coming with low and long-term interest rates on these vehicle loans. Post-COVID-19, China, the United States, and India have emerged as the world's largest auto market, resulting in rising opportunities for Auto loan providers in the regions.

Auto Loan Market Trends

Rising Sales Of Passenger Vehicles

The passenger vehicles market includes sales of two-wheeler, four-wheeler vehicles, and other vehicles mostly used for passenger transportation. Globally average passenger vehicle price is around USD 28,000, with regional variation. Among the sales of four-wheeler passenger vehicles, SUVs and medium cars are among the segments with the largest sales of more than 30 Million vehicles globally. With an increase in y-o-y sales, these two segments of passenger vehicles are occupying more than 50% of the passenger vehicle sales share and leading Automobile loan providers to focus their products on specific segments of passenger vehicles to reap the existing benefits and increase their automobile loan sales. Last year United States observed an increase in the price of passenger vehicles, with rising vehicle loan prices leading to more automobile buyers entering into debt. The rise in price of passenger vehicles is increasing the business of Automobile loan providers. With the increase in income and standard of living, passenger vehicles are becoming an opportunistic segment of Auto loans.

Increasing Vehicle Loan By Credit Union

Credit Unions are financial cooperative institutions providing users with traditional banking services. With the global tightening of monetary policy by central banks, interest rate by banking institutions is observing a continuous increase, making their loan products more expensive to the borrowers. Credit unions exist with comparatively lower interest rates and processing fees than banks for borrowing loans, as a result of which, post-COVID-19, with a decline in the savings of people, credit unions have emerged as an efficient automobile loan provider. In terms of the distribution of vehicle loans by sources in the United States, Credit unions have observed an increase in the share of more than 7% post coronavirus. For loans in the used vehicles market purchase, the share of credit unions observed an increase to 31% last year from a level of 25% during COVID-19. As a result of the rising price of automobiles with increasing interest rates on loans, credit unions are emerging as an attractive financing solution for automobile buyers.

Auto Loan Industry Overview

The auto loan market currently exists in a fragmented form, with the existence of a large number of players. Rising competition among firms for lower interest rates on loans with minimization of processing fees is leading to more competitive firms investing to occupy a large share of the customers. The technological innovation of digital loans and banking apps is further making Auto loans more efficient for borrowers. Some of the existing players in the Auto Loan Industry are Ally Financial, Wells Fargo, Chase, Capital One, and Bank of America.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in Demand for Passenger Vehicles

- 4.2.2 Quick Processing of Loan Increasing Automobile Loan Sales

- 4.3 Market Restraints

- 4.3.1 Rising of Interest Rates by Banks

- 4.3.2 Rising Price in Automobile Market

- 4.4 Market Opportunities

- 4.4.1 Emerging Market of Electric Vehicles Expanding the Auto Loan Market

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technological Innovations in Auto Loan Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicle

- 5.1.2 Commercial Vehicle

- 5.2 By Ownership

- 5.2.1 New Vehicle

- 5.2.2 Used Vehicle

- 5.3 By End-User

- 5.3.1 Individual

- 5.3.2 Enterprise

- 5.4 By Loan Provider

- 5.4.1 Banks

- 5.4.2 OEM

- 5.4.3 Credit Unions

- 5.4.4 Other Loan Providers

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Peru

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arad Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Rest of the World

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profile

- 6.2.1 Ally Financial

- 6.2.2 Wells Fargo

- 6.2.3 Chase

- 6.2.4 Capital One

- 6.2.5 Bank of America

- 6.2.6 BNP Paribas Financial Service

- 6.2.7 Credit Agricole

- 6.2.8 HDFC Bank

- 6.2.9 ICICI Bank

- 6.2.10 Mashreq Bank*

7 MARKET FUTURE TRENDS

8 DISCLAIMER AND ABOUT US

全球汽車金融市場規模、佔有率和成長分析:按類型和最終用戶 - 產業預測(2024-2031)

全球汽車金融市場規模、佔有率和成長分析:按類型和最終用戶 - 產業預測(2024-2031) 汽車貸款發放軟體市場規模 - 按組件(軟體、服務)、部署模式(本地、雲端)、最終用戶(銀行、信用合作社、抵押貸款人和經紀人)、區域展望與預測,2024 - 2032 年

汽車貸款發放軟體市場規模 - 按組件(軟體、服務)、部署模式(本地、雲端)、最終用戶(銀行、信用合作社、抵押貸款人和經紀人)、區域展望與預測,2024 - 2032 年 全球汽車金融市場預測(截至 2030 年):按提供者類型、用途類型、金融類型、供應商類型、服務類型、車輛類型和地區進行分析

全球汽車金融市場預測(截至 2030 年):按提供者類型、用途類型、金融類型、供應商類型、服務類型、車輛類型和地區進行分析 2024 年汽車金融世界市場報告

2024 年汽車金融世界市場報告 汽車金融市場:按提供者類型、類型、用途、車輛類型分類 - 2023-2030 年全球預測

汽車金融市場:按提供者類型、類型、用途、車輛類型分類 - 2023-2030 年全球預測 日本汽車貸款:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029

日本汽車貸款:市場佔有率分析、產業趨勢/統計、成長預測,2024-2029 汽車金融市場 - 2019-2029 年全球產業規模、佔有率、趨勢、機會和預測,按提供者類型、目的類型、車輛類型、地區、競爭細分

汽車金融市場 - 2019-2029 年全球產業規模、佔有率、趨勢、機會和預測,按提供者類型、目的類型、車輛類型、地區、競爭細分 全球汽車金融市場

全球汽車金融市場 汽車貸款市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、提供者類型、批准金額百分比、任期、地區、競爭細分

汽車貸款市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按車輛類型、提供者類型、批准金額百分比、任期、地區、競爭細分 汽車金融的全球市場 2023-2027

汽車金融的全球市場 2023-2027