|

市場調查報告書

商品編碼

1258787

垂直軟件市場 - 增長、趨勢、COVID-19 影響和預測 (2023-2028)Vertical Software Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

垂直軟件市場預計在預測期內以 11.2% 的複合年增長率增長。

垂直市場軟件具有許多明顯的優勢。 垂直市場軟件可以更有效地響應行業特定的功能和流程。 與橫向市場軟件相比,它還允許更好地集成不同的功能和程序。 由於這些特點,垂直軟件市場的市場規模預計將在預測期內呈現許多增長機會。

主要亮點

- 垂直軟件市場領導者有能力在千層蛋糕上添加“集成服務”,例如支付處理。 大多數金融服務,如支付處理、工資單和貸款,都是商品。 通過提供通常更易於使用、更便宜且與該軟件更好地集成的垂直專業產品,您將能夠確立自己作為垂直受信任的軟件供應商的地位。您有權擊敗第三方供應商。 這種方法的要點是公司不想讓客戶掏腰包購買更多的軟件。 相反,您可以讓交叉銷售感覺“免費”,並通過更換客戶已經支付的商品來減少銷售中的摩擦。

- 例如,Shopify 籌集並承銷業務資金。 具有現金流可見性的行業軟件企業特別適合發起和承銷貸款。 例如,當一家建築公司獲得新工作時,Procore 會提供貸款以資助購買建築材料。 Truckstop 將在卡車司機完成業務後以其債務為抵押貸款。 Mindbody 為未來通過 Mindbody 平台支付的款項提供預付現金。

- 一些 B2B2C 垂直軟件公司正試圖通過消費者而不是商家獲利。 FareHarbor 是一家為活動和旅遊運營商市場提供軟件的公司。 雖然它的許多競爭對手向運營商支付會員費,但 FareHarbor 通過提供免費軟件和向最終用戶收取交易費來賺錢。 這種突破性的定價讓 FareHarbor 比價格更高的競爭對手更具優勢。

- 在大流行期間,各個行業都成功地與軟件公司合作,為其客戶提供更好的體驗。 例如,著名的 ERP 解決方案提供商 Rootstock Software 最近與 Vertical Aerospace 合作,以消除這種誤解,並在全球 COVID-19 大流行期間實施 Rootstock 的雲 ERP,僅用了三個半月就完成了。

- 有更多的規則和監管合規管理在各個公司中得到發展。 監管合規流程和戰略指導公司努力實現其商業目標。 公司採用合規軟件來確保所有產品組件和生產程序符合所有相關法律要求和工業質量基準。 在許多行業的供應鏈中,監管限制變得越來越嚴格。 與氣候變化、全球化相關的環境問題以及隨之而來的跟蹤、滿足和驗證來自多個地點的法規遵從性的需求,以及大規模定制需要以更小的批次和更小的批次來滿足不斷增加的各種產品的要求,所有這些都增加了這些壓力。

垂直軟件市場趨勢

BFSI有望帶動市場

- 金融科技通過增加每個客戶的收入和使產品更強大來影響垂直 SaaS 進入市場的渠道。 換句話說,金融科技在提高生命週期價值(LTV)的同時維持(如果沒有降低)客戶獲取成本(CAC)。 例如,每個訂戶收入250美元/月的Mindbody,對軟件包收取150美元/月的費用,平均1800美元/年,同時額外賺取100美元/月的支付收入。

- 此外,金融科技可以顯著提高生命週期價值,因此垂直 SaaS 公司會在讓金融科技成為主要收入來源之前提供更便宜(甚至免費)的 SaaS 產品。這也可以吸引對數字化猶豫不決的客戶群。 Silo 是一個面向食品批發商的操作系統,目前不向客戶收取軟件費用,這使其能夠在一個歷來不願採用軟件的行業中有效地獲得客戶。我做到了。

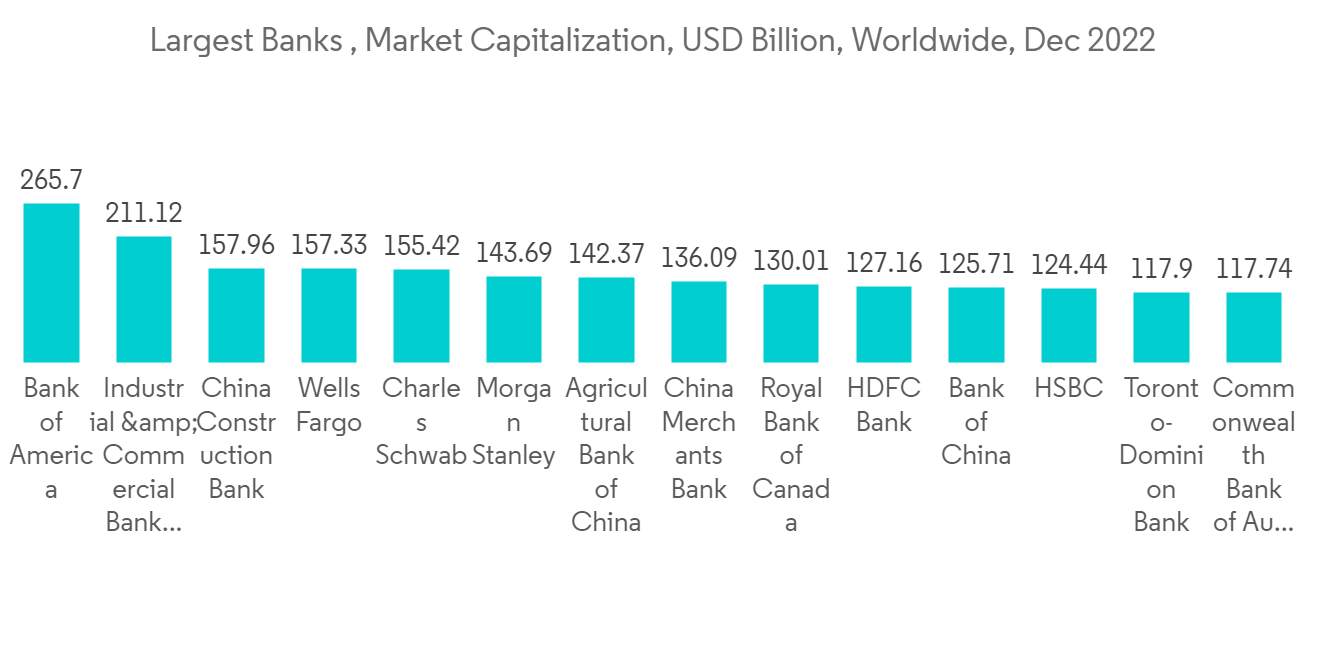

- 根據 CompaniesMarketCap 的數據,截至 2022 年 12 月 31 日,摩根大通是全球市值最大的銀行。 摩根大通當時的市值約為 3930 億美元,大大高於美國銀行的市值(約 2657 億美元)。 摩根大通是美國總資產最大的銀行,但在全球僅排名第六。 如此巨大的銀行市值為垂直軟件公司將其解決方案部署到這些銀行創造了機會。

- 隨著金融行業對垂直軟件的需求增加,公司提供了各種產品來佔領市場份額。 例如,2022 年 7 月,金融服務軟件解決方案提供商和平台 SAP Fioneer 推出了新的垂直產品戰略,顯著改變了其客戶服務。 我們的三個平台採用垂直戰略,提供適合個別市場和客戶需求的 IT 解決方案,使我們能夠應對日益複雜的金融世界。

- 同樣,2022 年 2 月,新的 Databricks Lakehouse 金融服務版將面向銀行、保險和資本市場客戶。 行業特定的技術內容,包括解決方案加速器、欺詐檢測和可持續性等金融服務用例的軟件代碼,以及與該領域常用數據集和第三方數據提供商的接口。加強您的平台。 據 Databricks 稱,Lakehouse for Financial Services 為多雲環境中的任何數據類型提供實時分析、商業智能和 AI 任務。

預計北美將佔據主要份額

- 根據 Flexera Software 對北美地區 514 名 IT 高管的調查,49% 的受訪者表示越來越多的公司將重點放在協作平台、服務、通信等方面的投資,並且該地區的 IT 投資正在增加。我們期望它會增加。 這為協作白板軟件市場的供應商開闢了新的可能性。 Micro 總部位於舊金山,擁有 2000 萬名財富 500 強協作白板用戶,包括戴爾、思科、德勤、Okta 和 Pivotal。

- 與傳統營銷相比,由於轉向數字全渠道營銷,該地區的營銷自動化軟件採用率正在上升。 根據美國營銷協會和杜克大學的 CMO 調查(n=356),2021 年 1 月,美國 B2B 產品營銷人員在次年的傳統廣告支出將減少 0.61%,而數字營銷支出預計將增加14.32%。

- 此外,2022 年 3 月,媒體和娛樂行業領先的版權和財務管理平台 Rightsline 收購了 REAL Software Systems,以擴展其核心知識產權管理服務。全面支持端到端的財務和忠誠度工作流程,同時將市場從媒體和娛樂擴展到遊戲、出版、消費品、生命科學和高科技等全球行業。

- 2022 年 12 月,總部位於蒙特利爾的專注於為垂直市場獲取和開發軟件的公司 Valsoft Corporation Inc. 宣布收購北美企業資源規劃 (ERP) 和倉庫管理系統 (WMS) Apero Solutions軟件供應商。我們很高興地宣布收購 Inc.

- 同樣,2023 年 1 月,i3 Verticals, Inc. 收購了為美國政府機構和非政府組織提供基金會計解決方案的 Accufund, Inc.。 Accufund 的會計軟件解決方案將大大改善公共部門領域公司的上市戰略。

垂直軟件行業概覽

由於多家公司的存在,垂直軟件市場競爭相對激烈。 市場參與者正在採取產品創新、兼併和收購等戰略來擴大產品組合、擴大地域範圍,主要是為了保持市場競爭力。

2022 年 12 月,Constellation Software Inc. 及其子公司 Lumine Group Inc. 宣布與總部位於美國的媒體垂直市場軟件供應商 WideOrbit Inc. (WideOrbit) 達成最終協議併計劃合併。確實如此。 交易完成後,WideOrbit 將成為 Lumine Group 的全資子公司,並將作為 Lumine Group 企業組合中的一個獨立業務部門運營。

2022 年 11 月,垂直智能軟件和解決方案提供商 NowVertical Group Inc. 欣然宣布與墨西哥城的國際載旗航空公司 Grupo Aeromexico S.A.B. de C.V. 達成新協議。 通過該協議,NOW 將幫助推進墨西哥航空公司的數據治理計劃,建立實現其成為數據驅動型航空公司的目標所需的願景和路徑。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

內容

第一章介紹

- 市場定義和範圍

- 調查先決條件

第二章研究方法論

第 3 章執行摘要

第 4 章市場洞察

- 市場概覽

- 產業吸引力 - 波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估 COVID-19 對市場的影響

第 5 章市場動態

- 市場驅動力

- 對企業特定解決方案和特定領域專業知識的需求不斷增加

- 市場壓制

- 實施複雜且缺乏敏捷性

第 6 章市場細分

- 按組織規模

- 中小企業

- 大型企業

- 按最終用戶行業

- BFSI

- 教育機構

- 法律/政府辦公室

- 娛樂和款待

- 服裝和服飾

- 醫療保健

- 農業

- 其他最終用戶行業

- 按地區

- 北美

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Constellation Software

- Verisk Analytics

- Athena

- Bio-Logic Inc.

- vetBadger

- FastBound

- Mail Technologies Inc

- Granular

- FarmBite

- RenderForest

第8章 市場展望

The vertical software market is expected to register a CAGR of 11.2 % over the forecasted period. Vertical market software includes a number of distinct advantages. Vertical market software assists in more effectively addressing industry-specific features and processes. In comparison to software for the horizontal market, it also assists organizations in obtaining superior integration with various functionalities and procedures. As a result of these features, the vertical software market size is expected to witness numerous growth opportunities during the forecasted period.

Key Highlights

- Vertical software market leaders have the luxury of adding "integrated services" such as payment processing to their layer cake. Most financial services, such as payment processing, payroll, and lending, are commodities. You have the right to win against generic third-party suppliers as the trusted software vendor in your vertical by supplying a vertical-specific offering that is often more useable, inexpensive, and better integrated with this software. This method's significance is that businesses do not require customers to dip into their pockets and purchase more software. Firms instead replace something that customers already pay for, making the cross-sell feel "free" and lowering sales friction.

- For example, Shopify sources and underwrite business financing. Vertical software businesses with cash flow visibility are especially well-positioned to originate and underwrite loans. For example, Procore provides loans to assist construction companies in financing the acquisition of building materials when new work is awarded to them. Truckstop makes loans to trucking businesses after completing work that is secured by the amount they owe. Mindbody provides a cash advance against future payments made via the Mindbody platform.

- Some B2B2C vertical software companies are attempting to monetize the consumer rather than the merchant. FareHarbor is a software provider to the activity and tour operator markets. While most of its competitors paid operators a membership fee, FareHarbor provided free software and gained revenue by charging end-users a transaction fee. FareHarbor gained an advantage over more expensive competitors thanks to this revolutionary pricing approach.

- During the pandemic, various vertical industries collaborated with software firms to provide a better experience for customers. For instance, rootstock software, a prominent provider of ERP solutions, recently collaborated with Vertical Aerospace to debunk this misconception, completing the implementation of Rootstock's Cloud ERP in just three and a half months and amid the global COVID-19 outbreak.

- There have been more rules, and regulatory compliance management has grown in many different enterprises. Regulatory compliance processes and strategies guide organizations as they work to achieve their commercial objectives. Companies employ compliance software to ensure that all product components and production procedures meet all relevant legal requirements and benchmarks for industrial quality. Regulatory constraints are becoming more intense along many industry supply chains. Climate change-related environmental concerns, globalization and the resulting need to track, satisfy, and verify regulatory compliance from multiple locations, and mass customization, which necessitates regulatory compliance for an ever-increasing various of products in an ever-smaller variety of lots or batches, all contribute to these pressures.

Vertical Software Market Trends

BFSI is Expected to Drive the Market

- Fintech influences vertical SaaS go-to-market channels by increasing revenue per customer and making the product stickier. In other words, fintech maintains, if not decreases, the cost of customer acquisition (CAC) while improving lifetime value (LTV). Mindbody, for example, earned USD 250 per month per subscriber; while it charged USD 150 per month, or USD 1800 per year on average, for its software package, it made an additional USD 100 per month from payments income.

- Furthermore, because fintech can drastically enhance LTV, vertical SaaS companies might offer their SaaS product for cheaper (or even for free) to entice a client base that would otherwise be hesitant to digitize before piling on fintech goods as the primary revenue lever. Silo, an operating system for wholesale food wholesalers, does not now charge its customers for its software, which has allowed it to effectively land customers in an industry that has previously been resistive to software adoption.

- According to CompaniesMarketCap, As of December 31, 2022, JPMorgan Chase was the largest bank in the world by market capitalization. JPMorgan Chase's market capitalization was around USD 393 billion at the time, much higher than Bank of America's market capitalization, which was around USD 265.7 billion. JPMorgan Chase is also the largest bank in the United States in total assets but only the sixth largest globally. The such huge market capitalization of banks would create an opportunity for vertical software companies to deploy their solutions in those banks.

- With the rise in demand for vertical software in the financial sector, firms are providing various products to capture the market share. For instance, in July 2022, SAP Fioneer, a financial services software solutions provider and platform, launched a new vertical product strategy that drastically altered its client offering. Using a vertical strategy, three platforms will deliver IT solutions adapted to the individual market and client needs, allowing them to negotiate an increasingly complex financial world.

- Similarly, in February 2022, the new Databricks Lakehouse financial services edition aims at customers in the banking, insurance, and capital markets. It enhances the platform with industry-specific technical content such as solution accelerators, software code for financial service use cases such as fraud detection and sustainability, and interfaces to data sets and third-party data providers typically utilized by the sector. According to Databricks, the Lakehouse for Financial Services provides real-time analytics, business intelligence, and AI tasks on all data types in multi-cloud environments.

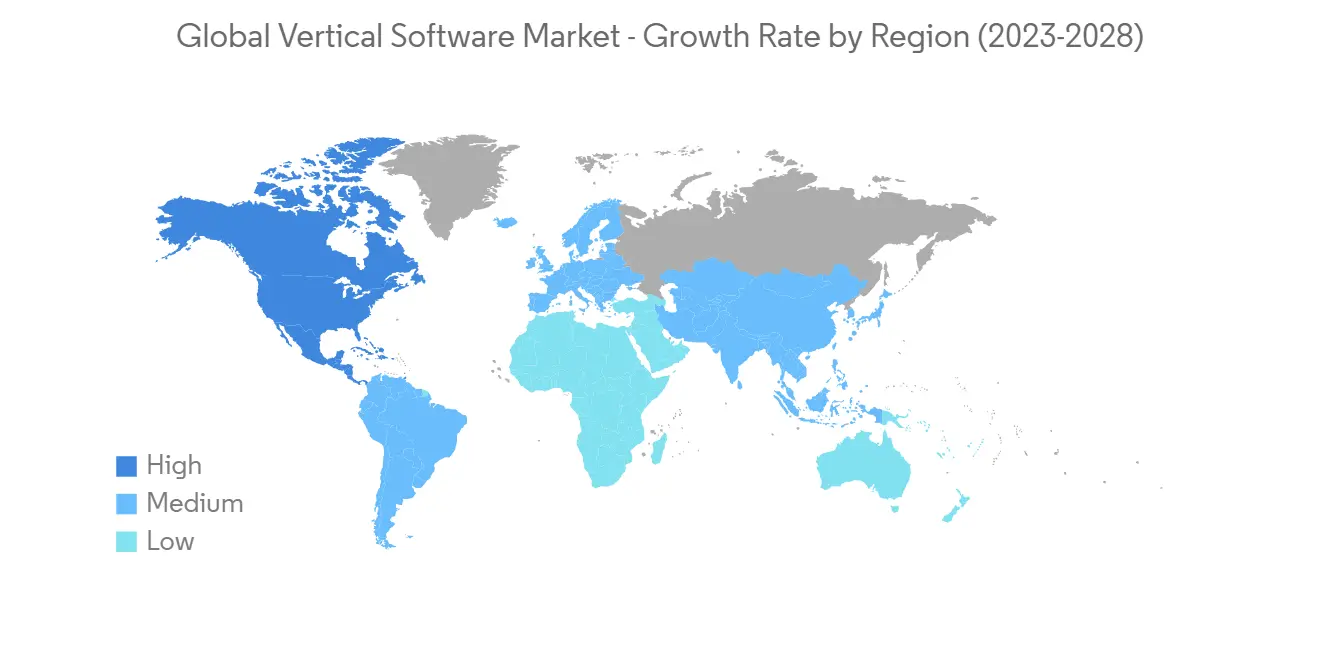

North America is Expected to Hold Major Share

- According to a Flexera Software poll of 514 IT executives in North America, 49% anticipate that IT spending in the region will increase as more firms focus on investing in collaboration platforms and services, communication, and other areas. This opens up new possibilities for suppliers in the collaborative whiteboard software market. Micro, a San Francisco-based firm, boasts 20 million users for its collaborative whiteboard, which includes Fortune 500 companies like Dell, Cisco, Deloitte, Okta, and Pivotal.

- The adoption of marketing automation software has been increasing in the region as there has been a shift to digital omnichannel marketing compared to traditional marketing. According to the CMO Survey by American Marketing Association and Duke University (n=356), in January 2021, B2B product marketers in the United States suggested that their spending on traditional advertising was expected to decline by 0.61% in the following year, while the digital marketing spending was projected to increase by 14.32%.

- Further, in March 2022, Rightsline, the leading rights and finance management platform for the media and entertainment industry, acquired REAL Software Systems to extend its core IP rights management services to fully support end-to-end financial and royalties' workflows while simultaneously expanding its market from media and entertainment into gaming, publishing, consumer products, life sciences, and high tech, among other global industries.

- In December 2022, Valsoft Corporation Inc., a Montreal-based business focusing on vertical market software acquisition and development, is happy to announce the acquisition of Apero Solutions Inc., a North American Enterprise Resource Planning (ERP) and Warehouse Management System (WMS) software supplier.

- Similarly, in January 2023, Accufund, Inc., a provider of fund accounting solutions for government bodies and NGOs in the United States, was acquired by i3 Verticals, Inc. Accufund's accounting software solutions will significantly improve enterprises' go-to-market strategy in the Public Sector area.

Vertical Software Industry Overview

The vertical software market is moderately competitive owing to the presence of multiple players. The players in the market are adopting strategies like product innovation, mergers, and acquisitions to expand their product portfolio, expand their geographic reach, and primarily stay competitive in the market.

In December 2022, Constellation Software Inc. and its subsidiary Lumine Group Inc. announced a formal agreement and merger plan with WideOrbit Inc. ("WideOrbit"), a media vertical market software supplier based in the United States. WideOrbit will become a completely owned subsidiary of Lumine Group and will operate as an autonomous business unit within the Lumine Group's portfolio of companies after the deal is finalized.

In November 2022, NowVertical Group Inc., a vertical intelligence software and solutions firm, is thrilled to announce a new contract with Grupo Aeromexico S.A.B. de C.V., Mexico City's international flag carrier airline. Under the terms of the agreement, NOW will assist Aeromexico in advancing its data governance program, establishing the vision and path it will need to take to progress and achieve its aim of being a data-driven operator.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Demand of Enterprise-specific Solution and Domain-specific Expertise

- 5.2 Market Restrain

- 5.2.1 Implementation Complexities and Lack of Agility

6 MARKET SEGMENTATION

- 6.1 By Organization Size

- 6.1.1 Small and Medium Enterprise

- 6.1.2 Large Enterprise

- 6.2 By End-User Industry

- 6.2.1 BFSI

- 6.2.2 Educational Institution

- 6.2.3 Legal and Government

- 6.2.4 Entertainment and Hospitality

- 6.2.5 Clothing and Apparel

- 6.2.6 Healthcare

- 6.2.7 Farming and Agriculture

- 6.2.8 Rest of the End-User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Constellation Software

- 7.1.2 Verisk Analytics

- 7.1.3 Athena

- 7.1.4 Bio-Logic Inc.

- 7.1.5 vetBadger

- 7.1.6 FastBound

- 7.1.7 Mail Technologies Inc

- 7.1.8 Granular

- 7.1.9 FarmBite

- 7.1.10 RenderForest